MELI - MercadoLibre: Impressive Growth But Not The Only Player

2023-03-27 07:03:20 ET

Summary

- MercadoLibre achieved impressive growth in 2022.

- Projecting MercadoLibre’s future growth requires caution and understanding of its competitive landscape and market conditions.

- Based on my DCF valuation, MercadoLibre’s intrinsic value per share is $966, indicating that the current stock is slightly overpriced.

Investment Thesis

MercadoLibre's (MELI) Q4 2022 results demonstrate impressive growth and profitability, but we should not make assumptions that this growth rate will be sustained. Given that the e-commerce and fintech industry in Latin America is still in its early stages, with no clear dominant player, it is crucial to understand MELI's competitive landscape and its addressable market conditions to avoid making hasty decisions.

Despite this, I believe that MELI will maintain its competitive edge thanks to its powerful ecosystem. Based on my analysis, I estimate that MELI will capture 30% of the e-commerce market share, while fintech will experience similar growth.

Additionally, it is important to consider the risks associated with investing in Latin American businesses, and therefore, we should factor them into our discount rate when valuing MELI.

Based on my DCF valuation, MELI's intrinsic value is $996 per share. Although the current stock price is slightly above its intrinsic valuation, I recommend holding the position or reducing MELI's portion from your portfolio.

Review of Q4 2022 and Annual Earnings

MELI announced outstanding Q4 2022 results and strong annual performance. In 2022, the company's total revenue reached $10.5 billion, reflecting a 50% growth rate, while the operating income stood at $1 billion. During Q4 2022, the GMV experienced a 35% growth on a FX neutral basis, indicating consistent expansion over the past three years. Similarly, the TPV rose by 80% on an FX neutral basis, and the credit portfolio expanded by 68% on the same basis.

Due to reduced Cost of Goods Sold and increased efficiency in sales and marketing expenses, the operating margin for Q4 2022 improved significantly to 11.6%, up from 1.1% in Q4 2021.

Overall, MELI's growth engine continues to thrive, and profitability has seen notable improvements.

Market Condition and Comparative landscape

When it comes to valuing growth companies, it's common practice to base growth projections on their recently reported growth rates. However, solely relying on these rates can be misleading, and we risk losing sight of the bigger picture unless we take into account the company's operating environment, including future market size and the competitive landscape.

MELI operates in 18 Latin American countries and generates revenue from both its e-commerce and fintech businesses. To accurately assess the company's growth potential, we must factor in how the market is expected to evolve in the coming years and how MELI's offerings compare to those of its competitors. Only by considering these broader factors can we gain a more accurate understanding of the company's growth prospects.

Ecommerce Business

MELI provides a range of services in the ecommerce sector, including marketplaces, shipping service, classifieds, and advertising. The success of these services is closely linked to the overall size of the ecommerce market and MELI's future market share

Market Size

To make a projection about the future size of the ecommerce market in Latin America, one can take into account various factors such as the current penetration rate of ecommerce in the retail market and the growth rate of the retail market.

As of 2022, Latin America had a 15% ecommerce penetration rate, with countries like Chile and Colombia having higher rates at 19% , Brazil at 17% , and Mexico at 11% . This rate has increased significantly from the pre-pandemic level of 9% , which has been one of the driving forces behind the impressive growth of companies like MELI. Additionally, with a large population of younger generations in Latin America, over 154 million aged 15 to 29 , it's reasonable to project that the ecommerce penetration rate will reach 30% in the coming years.

Based on data from AMi , the ecommerce market volume in Latin America in 2022 was $382 billion. Using this information and penetration rate, it's possible to calculate the total retail market volume in 2022, which amounts to $2,546 billion.

Assuming that the retail volume will increase at a rate of 3.5% (the risk-free rate) and taking into account the projected ecommerce penetration rate (30%), it's estimated that the size of the ecommerce market in Latin America will reach $1,078 billion over the next 10 years.

Market Share - MELI is Not the Only Player

It is true that MELI is a leading e-commerce player in Latin America, as evidenced by the monthly number of visits in 2022 , which suggests that MELI's performance surpasses that of its competitors.

Monthly visits in Latin America online marketplaces (business.ebanx.com/en/beyond-borders-2023)

Share of monthly visits in Brazilian online retail (business.ebanx.com/en/beyond-borders-2023)

In 2022, MELI's total GMV reached $34.5 billion, and its market share in the retail section of e-commerce was 18%. However, it would be inaccurate to claim that MELI dominates the e-commerce market in Latin America because the market remains fragmented.

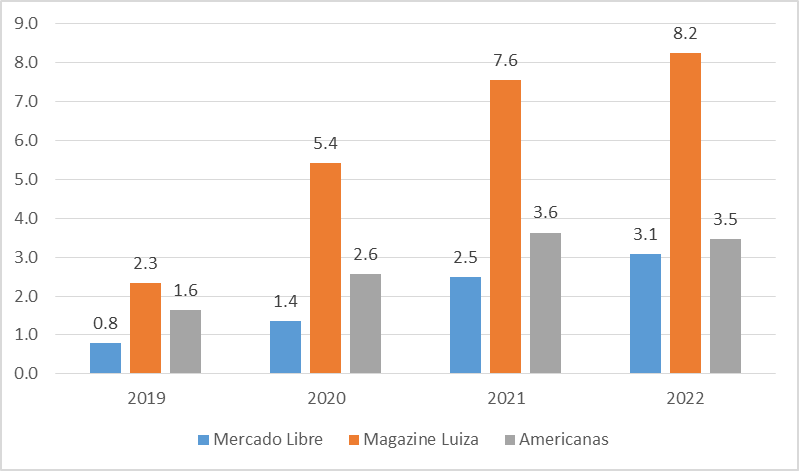

In Brazil, MELI faces stiff competition from other e-commerce players, such as Americanas (BTOOY) (BVMF:AMER3), and Magazine Luiza (MGLUY) (BVMF:MGLU3). Although Amazon ( AMZN ) does not report its revenue in Latin America separately, one research source indicates that Amazon's revenue in Brazil was $2.6 billion in 2021, while MELI's e-commerce revenue in Brazil in the same year was $2.5 billion. Nonetheless, comparing revenue between companies in e-commerce is not always useful unless we fully consider factors such as 1P and 3P business models because revenue recognition can differ between them. Still, comparing MELI's revenue growth with that of other local players, such as Magazine Luiza, and Americanas, provides valuable insights. These players have also experienced impressive revenue growth from 2019, with MercadoLibre growing by 3.9x, Magazine Luiza by 3.5x, and Americanas by 2.1x. Therefore, it is evident that MELI was not the only beneficiary of the digital transformation tailwind.

Revenue of Brazil online retail (Author based on financial reports)

{kind=link}

To remain competitive, MELI has been expanding its logistic arm, Mercado Envios, but other competitors such as Amazon and Magazine Luiza have also invested heavily in new distribution centers and boasted about their logistics capabilities. Despite these challenges, I believe that MELI will maintain its competitive position because of its large user pool, which creates a network effect, and the valuable data it gathers from its ecosystem, which provides a competitive edge.

Furthermore, the bankruptcy of Americanas could work in MELI's favor, enabling it to increase its market share in Brazil. Although my comparative analysis is specific to Brazil, which accounts for over 50% of MELI's revenue, it is a good proxy for MELI's competitive landscape, given the company's focus on the Brazilian market.

Ecommerce Revenue

Based on my projection of the retail market size and MELI's market share, I anticipate that MELI's GMV and revenue will increase approximately 9.5x.

Fintech Business

Fintech has experienced exponential growth in Latin America over the past decade, with more than 1,000 players entering the market due to the low levels of financial inclusion and underserved population. These fintech companies have transformed the digital banking, lending, payment, wealth management, personal finance, and insurance landscapes. The value of MELI's fintech business will depend on its future role in the industry.

MELI's payment solution, Mercado Pago, offers a range of services, including mobile point of sale, digital wallets, merchant services, prepaid cards, and credit services. Recently, MELI has expanded its fintech ecosystem to include insurance, investment, and cryptocurrency. However, there is no clear indication of MELI's competitive edge over other players in these new instruments. Therefore, MELI's revenue in the fintech industry will likely come from payment services and credit-based payment services, such as Mercado Credito, over the next decade.

Although MELI's fintech business has experienced higher growth than its e-commerce business, with a TPV off marketplace exceeding 70%, I expect the growth rate to converge with that of e-commerce as the latter gains more market share.

According to Mordor Intelligence , the Latin America mobile payment market is expected to grow at a CAGR of 24.5% until 2028. If this growth rate is extended to 2032 (year 10), the mobile payment market is projected to grow nine-fold.

As a result, I anticipate that MELI's fintech business revenue in year 10 will also increase by 9.5 times.

Intrinsic Valuation - Discounted Cash Flow Model

Revenue Growth

In order to estimate MELI's revenue in year 10, I conducted a reverse engineering analysis. I made the assumption that the high growth rate of 33% would be sustained for the first five years, and that the growth rate would then decrease linearly to the risk-free rate.

Operating Margin and Operating Income After Tax

Operating Margin in Year 10

To estimate MELI's operating margin in year 10, I analyzed the profitability of well-established e-commerce companies in the global market. Specifically, I looked at Alibaba ( BABA ) (despite Taobao not taking a fee from transactions) and eBay, which have business models similar to MELI's.

Alibaba's adjusted EBITA margin for its China commerce was 34% in both 2021 and 2022. On the other hand, eBay's operating margin is approximately 25%. However, unlike Alibaba and eBay ( EBAY ), MELI operates its own logistics network, Mercado Envios, which means that its profitability in the e-commerce business will likely be lower than its peers.

To gain insights into the profitability of MELI's fintech business, I reviewed PayPal (PYPL), which maintains an operating margin of around 15%.

Taking into consideration the differences in business structures, I believe it is a reasonable assumption that MELI's operating margin will reach 20% in year 10.

Tax Rate

When conducting my DCF analysis of MELI, I factored in a US marginal tax rate of 27.5% (which is the sum of the federal tax rate of 25% and a state tax rate of 2.5%) for the company's operating income after taxes.

Reinvestment

To maintain a high growth rate, it is necessary to allocate resources towards reinvestment, which is precisely what MELI has announced it will do. The company plans to invest a whopping $3.6 billion in Brazil in 2023, specifically targeting its Mercado Envios, MELI Ads, and Mercado Pago businesses.

Typically, excess cash and cash equivalents are not considered as part of invested capital, and according to Michael J. Mauboussin , only two to five percent of cash should be included based on a general rule of thumb. However, in the case of MELI, I have chosen to include cash and cash equivalents as part of the invested capital because the company's 10-k report clearly states that a significant amount of cash and cash equivalents, restricted cash and cash equivalents, and short-term investments should be counted as working capital. This has resulted in MELI's sales to capital ratio being calculated at 2.79 in 2022 and 3.45 in 2021.

For my valuation, I have chosen to use a sales to capital ratio of 3 for the high-growth period and 4 for the final five years.

Discount Rate

Typically, we pay little attention to the discount rate, or cost of capital, when valuing companies. Some might use a flat rate of 10%, which can work for companies operating in developed markets like the United States.

However, when valuing a company operating in an emerging market, such as Latin America, we must pay close attention to the cost of capital. Inflation rates are high, especially in countries like Argentina, where the rate was a staggering 94.8% in 2022. Political instability is also a common occurrence in the region.

To account for the added country risk in Latin America, I used the excess CDS spread over the United States as a proxy for the country risk premium. Using data from Aswath Damodaran's dataset , I calculated a weighted country risk premium of 6.1%.

MELI's country risk premium (Author)

For the cost of equity calculation, I used a risk-free rate of 3.59% based on the US 10-year treasury yield. Additionally, I factored in a beta of 1.07, an equity risk premium of 5%, and the previously mentioned country risk premium of 6.1%. These inputs resulted in a cost of equity of 15%.

Regarding the cost of debt, I used a risk-free rate of 3.59% and a default risk of 1% for the company. This led me to conclude that the cost of debt was 4.59%.

After considering the equity and interest-bearing debt ratio, I determined the cost of capital for the company to be 14%.

Terminal Value

It is my conviction that MELI's ecommerce operations will reap the benefits of network effects, positively impacting both buyers and sellers. As the platform expands and draws in more users, it generates a virtuous cycle that attracts even more buyers and sellers. This ultimately leads to a greater number of products available for purchase and a reduction in search costs.

Moreover, MELI will have a significant advantage stemming from the valuable data it collects from marketplace transactions, fulfillment services, and payments. This data will aid in sales forecasting, reducing friction in the purchasing process, and improving delivery times, while simultaneously decreasing risk in the credit business.

Based on this analysis, I believe that MELI will maintain a competitive edge and predict that the company's return on invested capital will remain robust, reaching 30% in the terminal year of my valuation. To determine the growth rate, I have used the US 10-year Treasury yield (which stands at 3.59%) as a proxy. By applying these assumptions, I have calculated the reinvestment rate to be 12%.

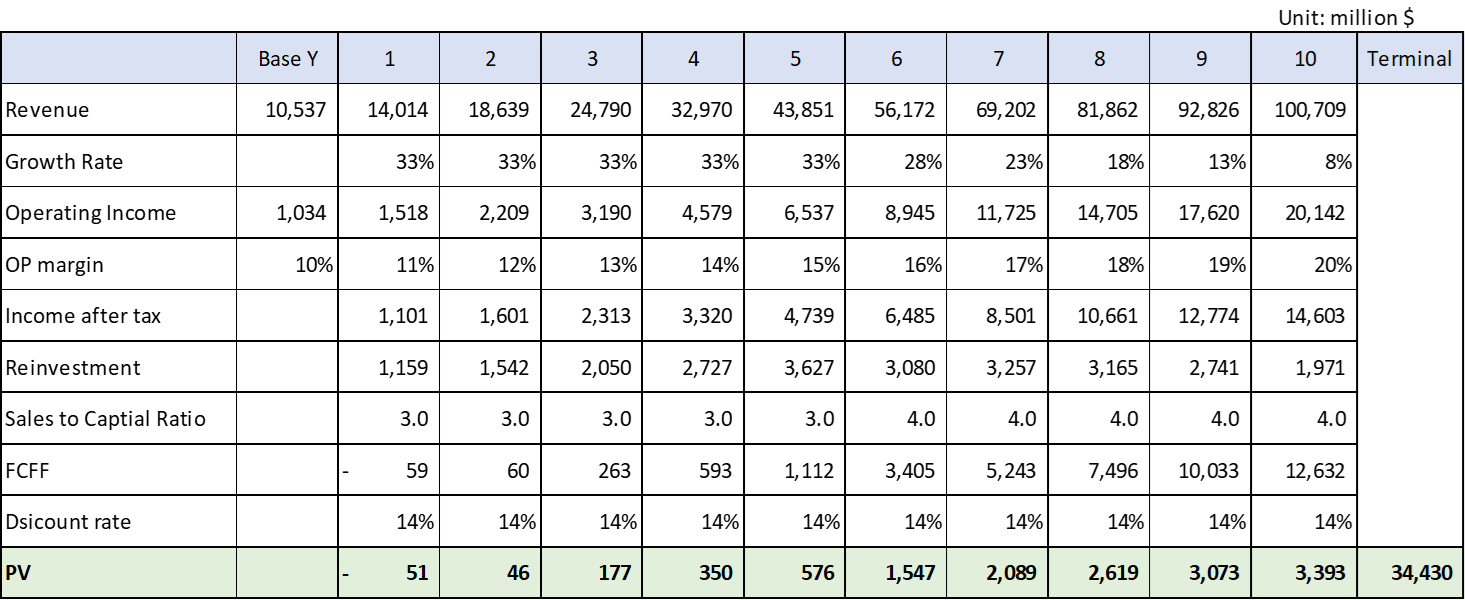

DCF Valuation Model

DCF Valuation Model - MELI (Author)

{kind=link}

After conducting a DCF valuation, my estimation suggests that the present value of MELI's future cash flows is approximately $48.2 billion. In order to derive the company's intrinsic value, I have added MELI's cash and cash equivalents, restricted cash and cash equivalents, as well as short-term investments, which totals $5.7 billion. I have then subtracted MELI's interest-bearing debt of $5.4 billion, resulting in a total intrinsic value of $48.5 billion.

Intrinsic Value - MELI (Author)

Given that MELI currently has 50,257,751 outstanding shares, my calculations indicate that the intrinsic value per share for MELI is approximately $996.

Reality Check

While some individuals may contend that my projected growth rate for the initial five years is overly cautious, a closer examination of the revenue figure for year ten ($100 billion) reveals that my estimation is in fact optimistic rather than conservative. For instance, consider Alibaba's revenue for 2021, which reached $109 billion. It is worth noting that unlike MELI, Alibaba holds a commanding 47% share of China's ecommerce market, and China's population is over two times larger than that of Latin America. As a result, it is understandable that some may find my estimation to be quite ambitious.

Investment Risk

Political instability : Latin American countries are known for their political instability, characterized by frequent changes in government, social unrest, and corruption. This can pose a significant risk to MELI's business as it creates an atmosphere of uncertainty that can adversely affect the company's operations, growth, and profitability.

Legal and regulatory risks : The legal and regulatory environment in Latin America is often complex and unpredictable, with varying laws and regulations across different countries and regions. This can create significant challenges for MELI in terms of complying with local laws, obtaining permits and licenses, and expanding its operations.

Conclusion

MELI has demonstrated impressive growth, but it's important to exercise caution when projecting its future growth rate. Strong growth from MELI's competitors and their preparations for fierce competition suggest a challenging market ahead. Nonetheless, I believe that MELI's powerful ecosystem will continue to give it a competitive edge, and I estimate that MELI will capture 30% of the e-commerce market share, with fintech growing at a similar pace.

As is well-known, doing business in Latin America carries more risk than in developed markets, due to various factors such as high inflation rates and political instability. For this reason, I have factored in a country risk premium of 6.1% when calculating MELI's cost of capital, which amounts to 14%.

My DCF valuation suggests that MELI's intrinsic value is $996 per share. While the current stock price is slightly above this valuation, I would recommend either holding the position or reducing MELI's portion in the portfolio.

For further details see:

MercadoLibre: Impressive Growth But Not The Only Player