MELI - MercadoLibre Is Becoming A Cash Flow Monster

2023-10-11 10:00:00 ET

Summary

- MercadoLibre continues to gain operating leverage.

- All KPIs move in the right direction.

- At the current price, MercadoLibre looks significantly undervalued.

- Major risks include bad credit debt and the general LATAM emerging market risk.

MercadoLibre (MELI) is a core holding in my portfolio at over 6%. In February, I published my last update on the stock . In this article, I talked about a few main KPIs I watch for MELI:

- Credit business development

- Gross Merchandise Volume (GMV)

- Total Payment Volume (TPV) and TPV OFF (TPV outside the MercadoLibre ecosystem)

- Take rates for eCommerce and Fintech business segments

Let's see how the company developed in the last two quarters and how the future might look.

The headline numbers

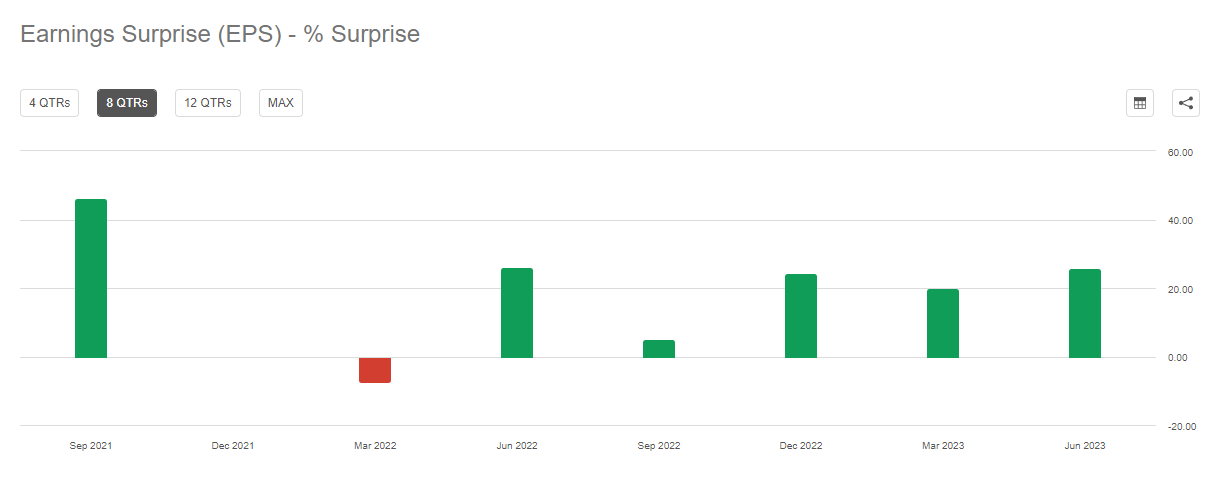

Over the last few five quarters, MercadoLibre has seen impressive consistency in beating EPS by large margins. Besides Q3 22 at 5%, all other quarters were 20% EPS beats. Revenue has largely met expectations without surprise, with beats between -1% and +5%.

{kind=link}

The numbers clearly show that MercadoLibre has started to optimize the business for profits, with Q1 seeing operating margins expand from 6.2% to 11.2% and net income margins from 2.9% to 6.6%. Q2 saw a similar trend, with operating margins improving from 9.6% to 16.3% and net income margins from 4.7% to 7.7%. The primary driver for the outperformance in operating margin was the contribution from provisions for doubtful accounts (300 bps in Q1 and 520 bps in Q2), an estimate for accounts receivable that might need to be written off. My last article reiterated that investors must monitor the credit business and see how it develops. Management is learning as they go and I believe they will achieve better risk management over time. Net income benefited from higher interest rates on customer and corporate funds and added 390 bps in Q1 and 370 bps in Q2.

Mercado Credito

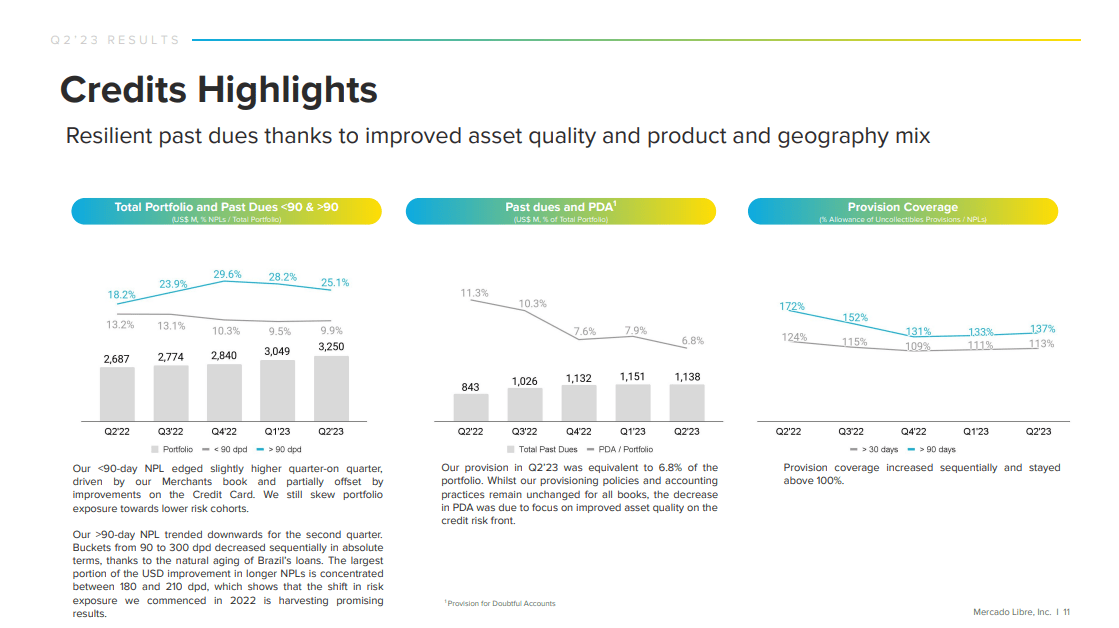

In the credit business, we can see a new trend in the last two-quarters of bad debt (>90 days past due) declining as a percentage of the portfolio. Overall, the credit portfolio's growth has slowed as the company started to focus more on the quality of the credits they are giving out. This is also represented in the percentage of provisions for doubtful accounts divided by the total credit portfolio. The credit business is highly profitable and reached a net interest margin after losses (NIMAL) of 30.6% in Q1 and 36.8% in Q2. As the credit business started to scale over the last years, I began to worry a bit about the rising levels of bad debt, but management seems to have found a way to handle it now with better risk management, resulting in higher quality debt.

MercadoLibre Credits highlights (MercadoLibre Q2 Presentation)

{kind=link}

MercadoLibre marketplace

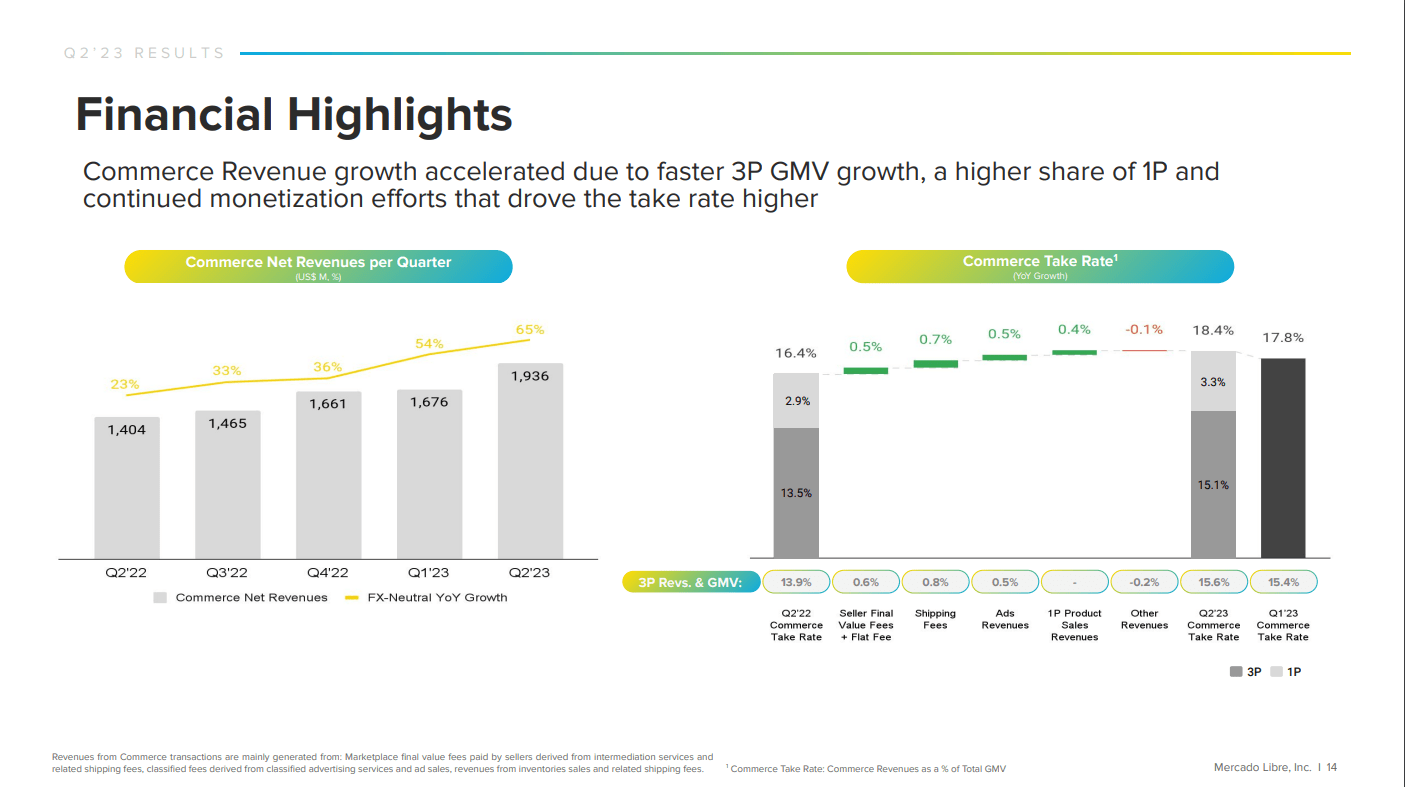

In the most recent quarter, the marketplace saw its GMV increase by 47% to $10.5 billion, with an 18% increase in sold items to 325.3 million. Unique buyers increased 16% Y/Y to 47.6 million. The take rate expanded nicely from 16.4% to 18.4% in Q2. Q1 also saw an increase from 16.7% to 17.8%. MELI sees increased margins from its logistics business, adding 80 bps and 60 bps to the take rate. Total managed network penetration reached 93.9% in the most recent quarter, a continued improvement. Ads are also becoming an increasingly relevant business for MercadoLibre. Ads grew 70% in Q2, hitting 1.6% as a percentage of GMV, that's $168 million. Ads are very profitable with EBIT margins of around 80%, so around $130 out of these 168 million should translate into EBIT. Like Amazon (AMZN), MercadoLibre is becoming a big player in the advertisement market. Marketplaces are uniquely positioned to offer ads that directly lead to sales conversion, a large advantage. While ads on Google (GOOGL) (GOOG) or Facebook (META) need to redirect users to a page, Amazon or MercadoLibre users can directly purchase items with the click of a button. I expect this ad revenue momentum to continue.

MercadoLibre Marketplace take rate (MercadoLibre Q2 Presentation)

{kind=link}

Mercado Pago (Fintech)

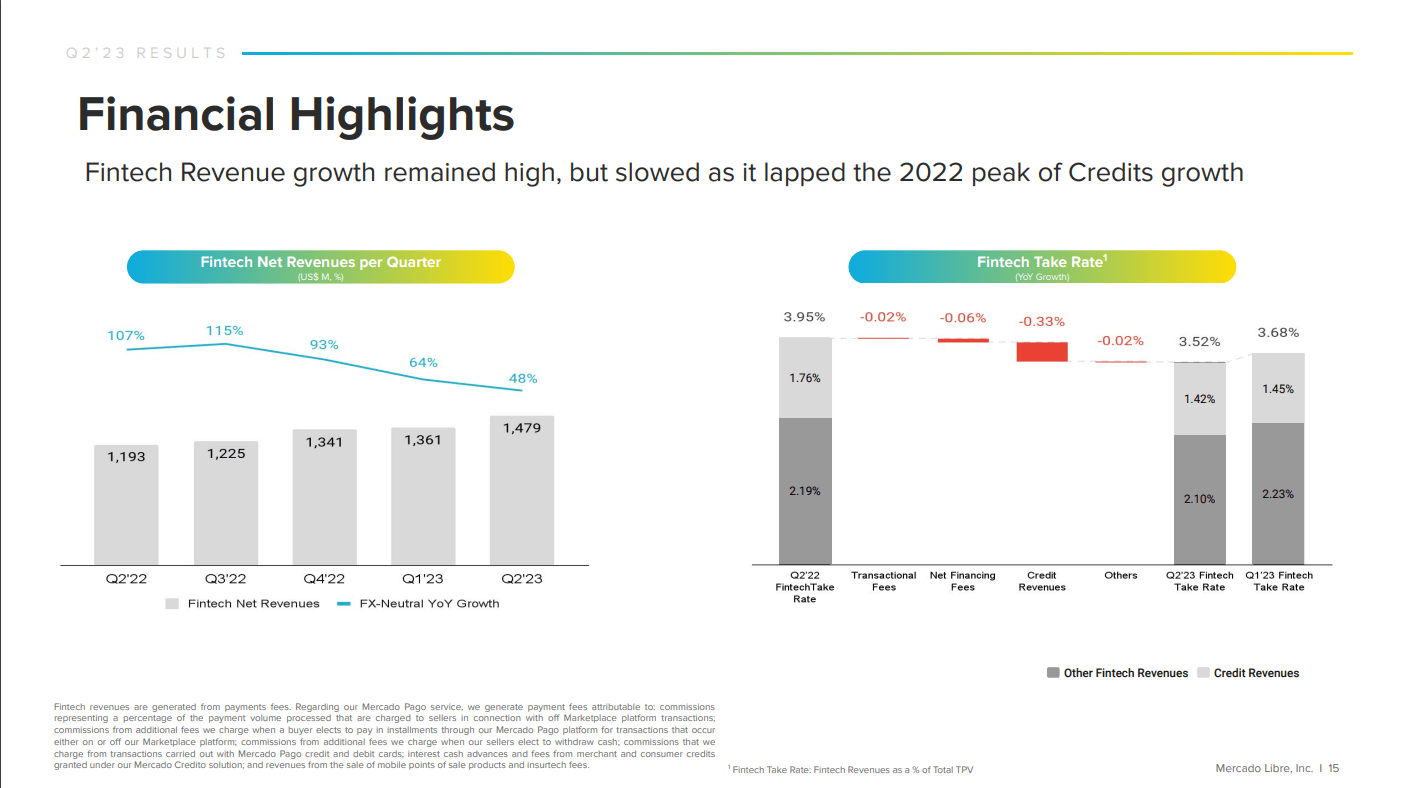

TPV (Q1 +96.1% and Q2 +97%) and TPV OFF (Q1 +120.8% and Q2 +129%) saw rapid growth again. We can also see that take rates have decreased Y/Y due to the slowing credit business. Fintech is a competitive business, so it is not unusual to see dropping take rates. This is fine as long as volumes continue increasing, as it does for Mercado Pago. This is nothing I'd worry about, but something to watch.

{kind=link}

MercadoLibre looks very compelling

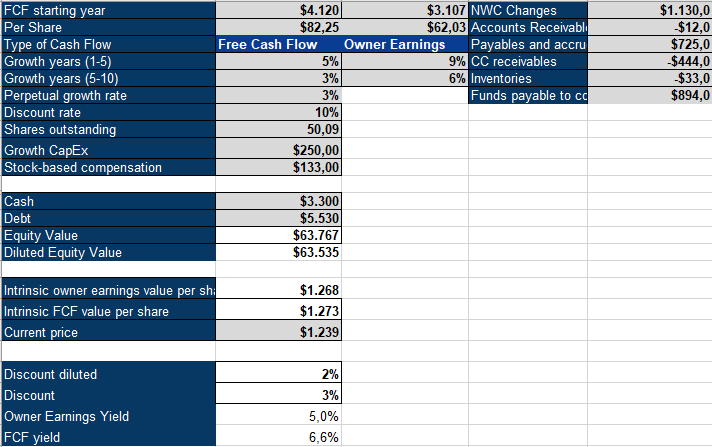

To value MercadoLibre, I use an inverse DCF model. Net working capital changes make a big difference for MercadoLibre due to working capital movements in the credit business. Over the last year, MELI started to gush cash flow and generated an impressive $4.12 billion over the last year, up from just $1.09 billion a year ago. The company also started to tamper with its capital expenditure spending, but it continues building its logistics network. Therefore, I included $250 million out of the $421 million (down from $597 million peak spending) in total capEx as growth capex. We can see that MELI would only need to achieve single-digit growth rates at the current owner earnings and free cash flow yields. This looks very reasonable compared to its 55% 5-year revenue CAGR. Before the pandemic, MELI still had a 5-year CAGR of 23%, at its lowest point in 2016. Especially as we see the business model continue to create operating leverage, profits should rise even faster than revenue. While I believe that we'll see a deceleration, MELI should be able to grow significantly in the double-digits.

There are two major risks I'd say keep the stock down:

- Worries about the credit business and credit losses eating into cash flows

- Emerging market discount

MercadoLibre is a core position in my portfolio and continues to be a strong buy at these levels.

{kind=link}

For further details see:

MercadoLibre Is Becoming A Cash Flow Monster