MELI - MercadoLibre: Looks Better Than Amazon Based On Its Growth

2023-03-29 09:00:00 ET

Summary

- As the Latam giant offering e-commerce, fintech, logistics, and advertising services all under one roof, it is no wonder that MELI commands leading mind-share in its markets.

- The synergistic effect from the sum of its parts may further drive cost optimization, while growing consumer adoption and its top/bottom lines ahead.

- Based on our conservative estimates, MELI may record FY2025 revenues of $18.5B and EPS of $26.50, suggesting a sustained CAGR of ~20% and ~40%, respectively.

- Therefore, we believe MELI stock is still a buy at these levels, given the attractive upside potential to our aggressive price target of $1,860.

There Is Much More To MercadoLibre Than Meets The Eye

The MercadoLibre ( MELI ) stock has recorded a massive rally of 93.7% since its June 2022 bottom, further sustained by its double-beat FQ4'22 results . The company had reported stellar revenues of $3B (+11.5% QoQ/ +40.9% YoY) and GAAP EPS of $3.25 (+26.9% QoQ/ +353.2% YoY).

Its FY2022 results were impressive as well, with expanding top and bottom lines: revenues came in at $10.54B (+49.08% YoY) and GAAP EPS were $9.53 (+470.6% YoY), respectively.

We reckon much of the recent optimism is also attributed to MELI's forward commentary . As the region's leader in e-commerce and fintech, it expects to deliver consistent margin expansion while increasing its market share. It also aims to achieve healthy bottom-line growth over the next three to five years.

In our opinion, its success was highly attributed to the stringent operating efficiencies thus far, with the SG&A and R&D expenses only expanding by +142.4% from $1.25B in FY2019 to $3.03B in FY2022. This was despite the tremendous growth in its revenues by +359.8% from $2.29B to $10.53B at the same time.

Given the drastic difference to Amazon (NASDAQ: AMZN ), with a top-line expansion of +83.2% and operational cost increase of +111.9% since FY2019, we concurred with Pedro Arnt's, CFO of MELI, commentary in the recent FQ4'22 earnings call:

MELI in a way is in an island within the tech world and that no layoffs. If anything, we've said we will continue to increase the size of our engineering teams, we see that as a key competitive advantage. And one where because we were disciplined throughout the pandemic, I don't think we over-hired or we overspent on capacity by and large. That puts us in a unique position now where we can continue to hire. ( Seeking Alpha )

This feat was admirable indeed, since it grew in conjunction with MELI's growing ambitions to be a one-stop-shop solution across e-commerce (Mercado Libre), fintech (Mercado Pago & Credito), logistics (Mercado Envios), and advertising (Mercado Ads) need for sellers/ buyers in the Latam region.

We believed that the vertically integrated ecosystem had proved to be highly beneficial in expanding the platform's adoption and top/ bottom line growth indeed. By FQ4'22, the company had already processed 100% of its e-commerce Gross Merchandise Volume through Mercado Pago, compared to 98% in FQ4'21 , 97% in FQ4'20 and 94% in FQ4'19 .

The company had also grown its off-platform payment businesses through QR payments and POS business, with TPV of $87.4B (+80.9% YoY) in FY2022. This was naturally attributed to MELI's well-diversified fintech strategy across payment, banking, investments, lending, insurance, and credit card products.

Furthermore, 94% (+5 points YoY) of MELI's e-commerce items were shipped through Mercado Envios by the latest quarter. While there was no breakdown for the logistic segment, the management had reported an expansion in its monetization rate despite the rising inflationary costs.

It was also important to highlight that the company made the wise decision to utilize third-party carriers and other logistics service providers, while leasing its fulfillment, cross-docking, and service centers. This strategy allowed the company to offer highly competitive rates, while similarly being asset-light since it owned only 0.2% of total operating facilities.

Despite nearly 76% of its orders being delivered within 48 hours, the company's overall net shipping cost remained stable as a percentage of its GMV, suggesting improved operating costs and efficiencies thus far.

While MELI did not break down its advertising revenues (included within e-commerce services ), Insider Intelligence estimated that adoption grew +70% YoY, with the company accounting for 2.7% of the region's digital ad spending in FY2022. Considering its e-commerce and banking offerings, we reckon more advertisers may flock to the company for improved targeted advertising, similar to AMZN's success thus far.

Therefore, given the strategic end-to-end product offerings, it was unsurprising that MELI had emerged as the leader in the region, with an outstanding mind share of 667.7M in monthly visits by January 2023, compared to AMZN at 169M and Americanas at 129.6M.

Most importantly, the Latam e-commerce giant had also grown its average items/ payment volume per user to 7.46/ $835.35 by FY2022, compared to 6.87/ $552.62 in FY2021 and 5.1/ $382.60 in FY2019. This growth naturally supported the tremendous expansion in its Gross Merchandise Volume [GMV] at a CAGR of 35.01% and Total Payment Volume [TPV] at 63.30% since FY2019, despite the region's rising inflationary pressures from 3.3% in 2020 to 8.3% in 2022.

Furthermore, MELI had outperformed its e-commerce peers, such as AMZN which only recorded top and bottom line growth of +9.3%/ -108.3%, Shopify Inc. (NYSE: SHOP ) at +21.4%/ -93.7%, and Sea Limited (NYSE: SE ) at +25%/ +42.9% in FY2022. It appears MELI has flourished indeed, despite the macroeconomic headwinds.

In our view, the company had succeeded in bringing these complementary services under one roof, with the synergies optimizing its operations and costs, while similarly growing its top and bottom lines. This was significantly aided by the region's lower average labor costs of $7.74K, compared to the US at $70.93K.

Market analysts also expect the Latam e-commerce and fintech market to further expand at a CAGR of 14.78% and 20% through 2026, with the e-commerce penetration doubling to 16% by 2025 . Therefore, given the relatively low e-commerce penetration in the region compared to China at 27% , the US at 20%, and the rest of the world at 17%, we reckon MELI's prospects remain excellent over the next few years.

As a result, it is unsurprising that the company has guided further investments in its logistics fulfillment centers in Mexico, due to the peak utilization of Mercado Envios. This was on top of the aggressive R&D efforts in the fintech and advertising segment at $1.09B (+86.2% YoY and +392.8% since FY2019) in FY2022.

We reckon these efforts may naturally improve MELI's delivery times, while accelerating innovation across its entire product offerings, eventually improving its market share in the Latam region.

So, Is MELI Stock A Buy , Sell, or Hold?

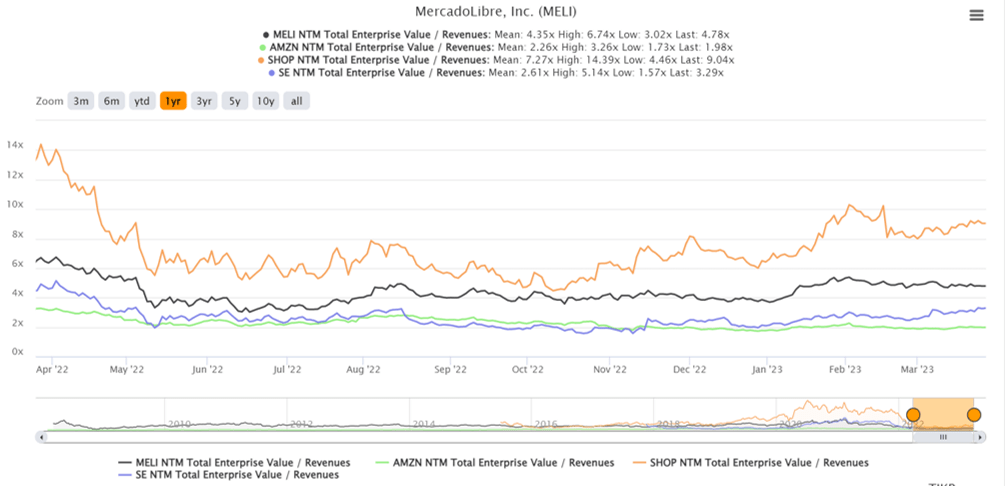

MELI & Peers 1Y EV/Revenue

{kind=link}

Hence, we remain highly invested in MELI's forward execution, with the company potentially recording revenues of $18.5B and EPS of $26.50 by FY2025, based on our estimates of a top-line CAGR of ~20%, bottom-line CAGR of ~40%, and moderate expansion in market share.

Given the impressive rate of growth at a time of peak recessionary fears, its premium valuations appear to be justified, at EV/NTM Revenue of 4.78x and NTM P/E of 70.30x, significantly aided by the sustained shift in consumer spending habits post-reopening cadence. These compare well to AMZN too, at EV/NTM Revenue of 1.98x and NTM P/E of 68.12x, given the latter's maturing top and bottom line growth.

While SE and SHOP have yet to report sustained GAAP earnings, it is also important to highlight that they continue to report excellent top-line expansion of 25.1% and 21.4% YoY, justifying their EV/NTM Revenue of 3.29x and 9.04x, respectively in our view.

Based on MELI's NTM P/E of 70.30x, we are also looking at an aggressive price target of $1,860, suggesting an excellent upside potential of 56.3% from current levels.

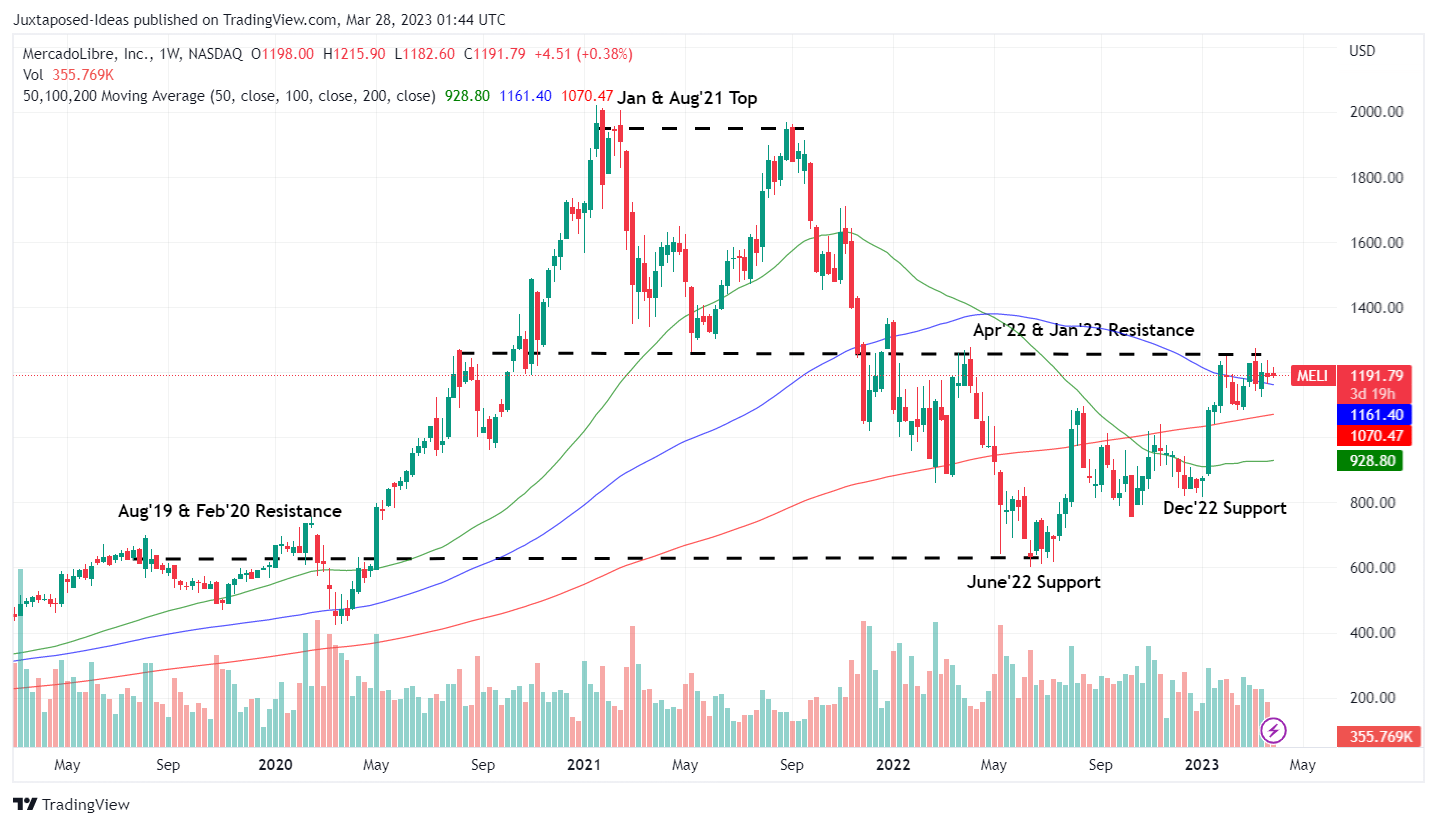

MELI 3Y Stock Price

{kind=link}

Therefore, we continue to rate the MELI stock as a Buy here, given its attractive risk-reward ratio. In the meantime, bottom fishing investors may potentially wait for another retracement to the $850s, due to the excellent support at the December 2022 bottom, since it is uncertain if we may see June 2022 levels of $600s again.

For further details see:

MercadoLibre: Looks Better Than Amazon Based On Its Growth