MELI - MercadoLibre Looks Like Alibaba In 2019 - And That's Not A Good Thing

2023-06-20 08:19:38 ET

Summary

- MercadoLibre is "The Amazon of Latin America."

- MELI stock has been on a roll as of late, soaring nearly 100% from the lows.

- MercadoLibre continues to generate stunning revenue growth and margin expansion in spite of lapping pandemic comps.

- I highlight the parallels with Alibaba from several years ago - before the Chinese stock imploded.

- Between high inflation in Argentina and rich valuations, MELI stock is looking very risky especially for long-term investors.

MercadoLibre ( MELI ) is a popular stock among growth investors both due to its strong fundamental results as well as its strong stock price performance over the last decade. Even though the stock remains well off all time highs, I am of the view that valuations are too rich given that revenue growth must decelerate at some point, and that is before accounting for geopolitical risks. Investors seem to be forgetting about the uncertainty that comes with investing in international stocks, which is a curious observation given the multiple contraction that has taken place in former Chinese tech darling Alibaba ( BABA ). Argentina has been generating the strongest growth for MELI but I question how much of that growth is due to the inherently unsustainable factor of inflation, which has hovered around the triple digits as of late. MELI may benefit from a long growth runway from continued e-commerce adoption in LATAM, but I am skeptical of the hyper-growth multiple that the stock trades at.

MELI Stock Price

MELI has fully participated in the recent recovery in the tech sector, with its stock up nearly 100% from the lows. Even after the recovery, the stock is still down around 40% from all time highs.

I last covered MELI in April where I explained why I was taking profits on my winning position. The stock has underperformed the broader market by around 10% since then and I am growing more pessimistic regarding the near term prospects for the stock price.

MELI Stock Key Metrics

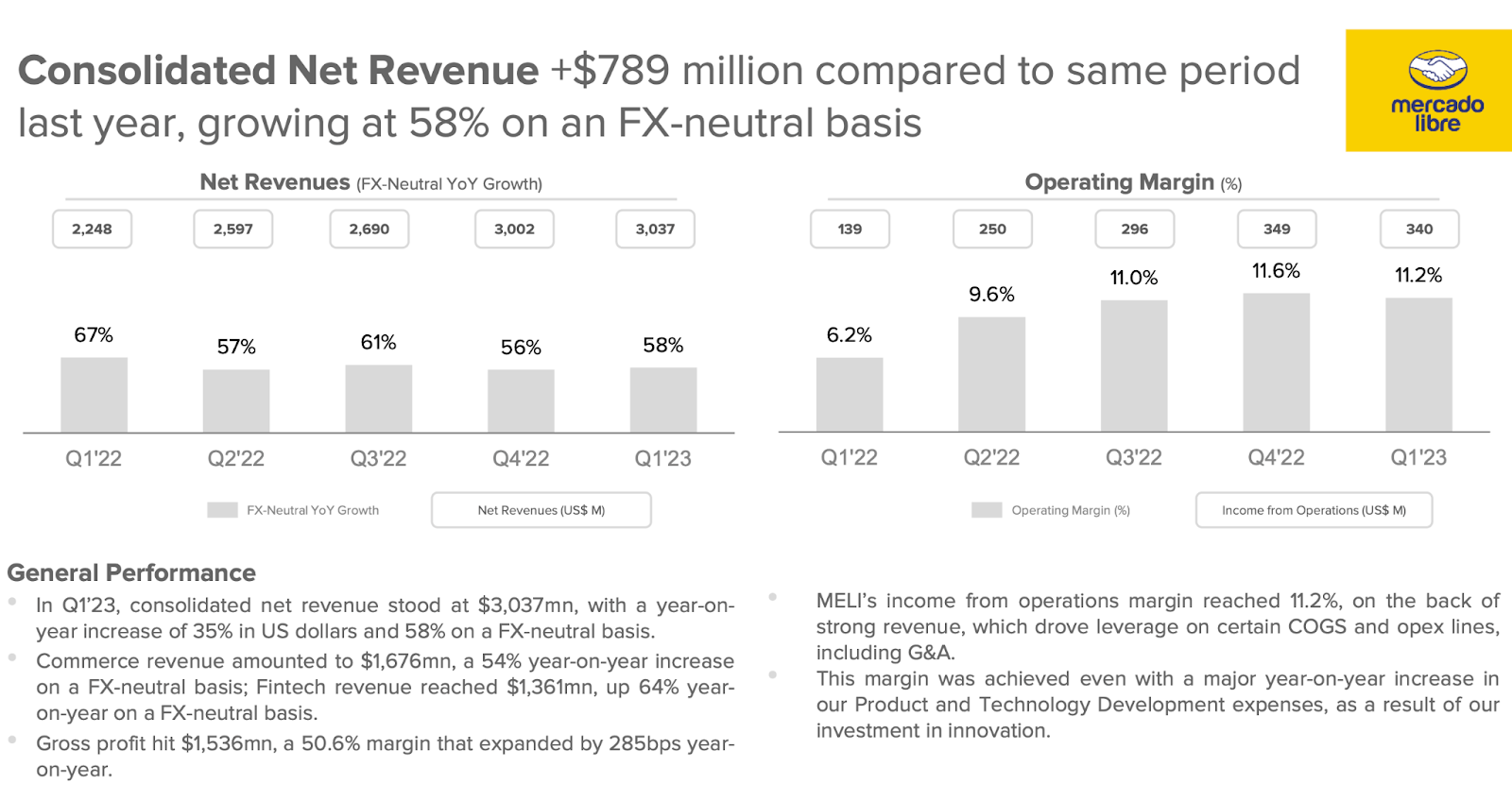

In its most recent quarter, MELI delivered jaw-dropping growth numbers, with revenue growing at a 58% constant currency basis YOY. It is stunning that MELI is able to sustain such rapid growth in spite of lapping tough pandemic comps. Most other e-commerce operators have seen growth rates decelerate meaningfully.

{kind=link}

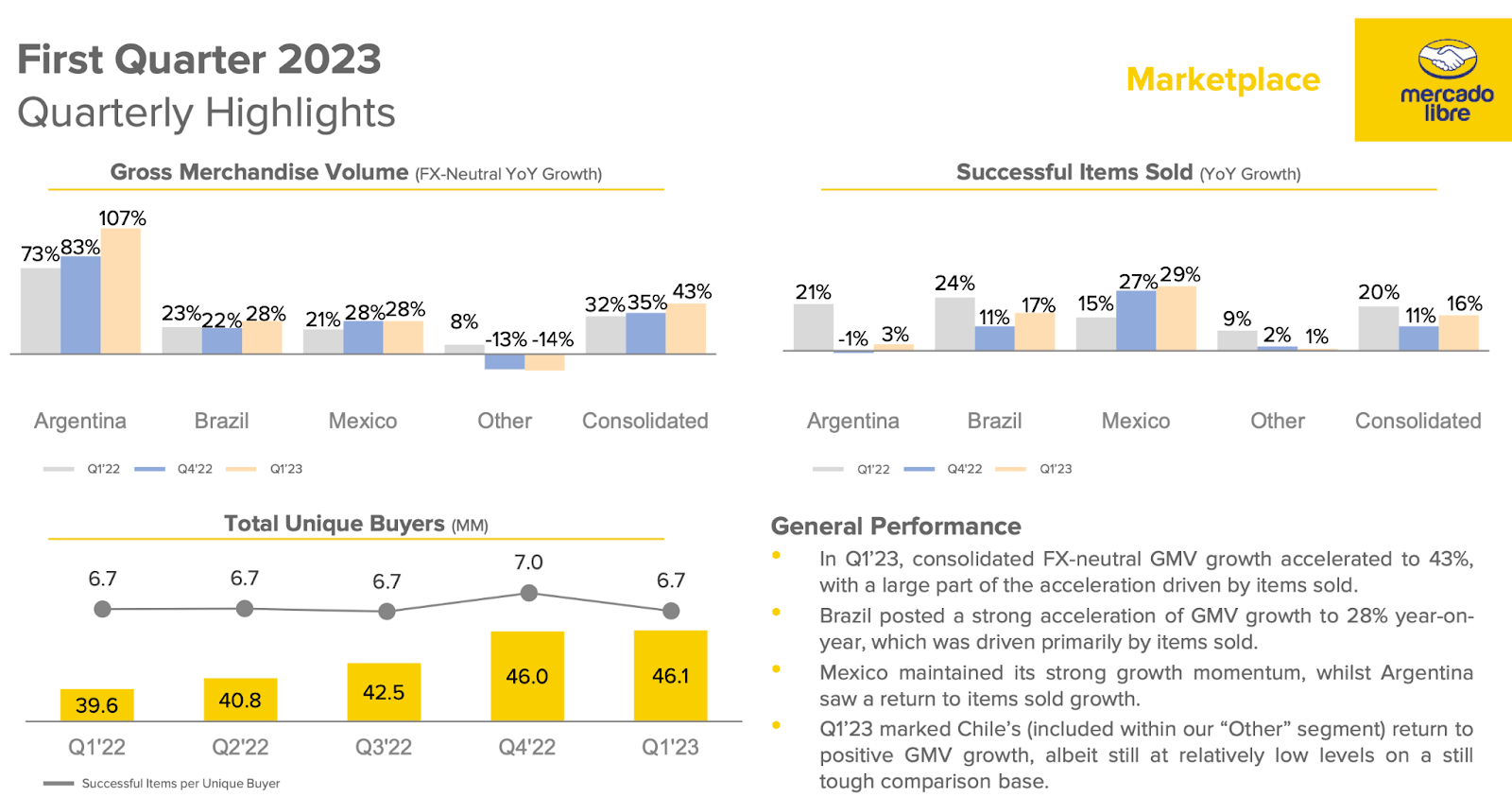

MELI may be still benefiting from the ongoing adoption of e-commerce in its core LATAM countries. As stated in my prior report, e-commerce penetration in LATAM is still only about half of that seen in North America. Even so, there's still a big gap between the 0% to 10% growth rate seen at US-based e-commerce operators and the 58% growth rates seen here at MELI. In my view, the discrepancy can be explained by the unusual circumstances in Argentina. As we can see below, whereas the consolidated GMV growth rate was 43%, Argentina saw 107% YOY growth, somehow accelerating from the 83% growth seen in the year prior. Meanwhile, "successful items sold" growth was weakest in Argentina at just 3% YOY. How does one explain this?

{kind=link}

The thing is, Argentina has seen triple-digit inflation for around a half a year at this point , with inflation having been on a steep upward trend since hovering around 20% in 2015. I wonder how many investors are seeing MELI's rapid top-line growth and thinking that it is only reflecting "normal" organic growth. I note that the impact of inflation in Argentina also explains why the nominal GMV growth rate was only 15% for that region in the quarter (reflecting currency exchange headwinds).

2023 Q1 Shareholder Letter

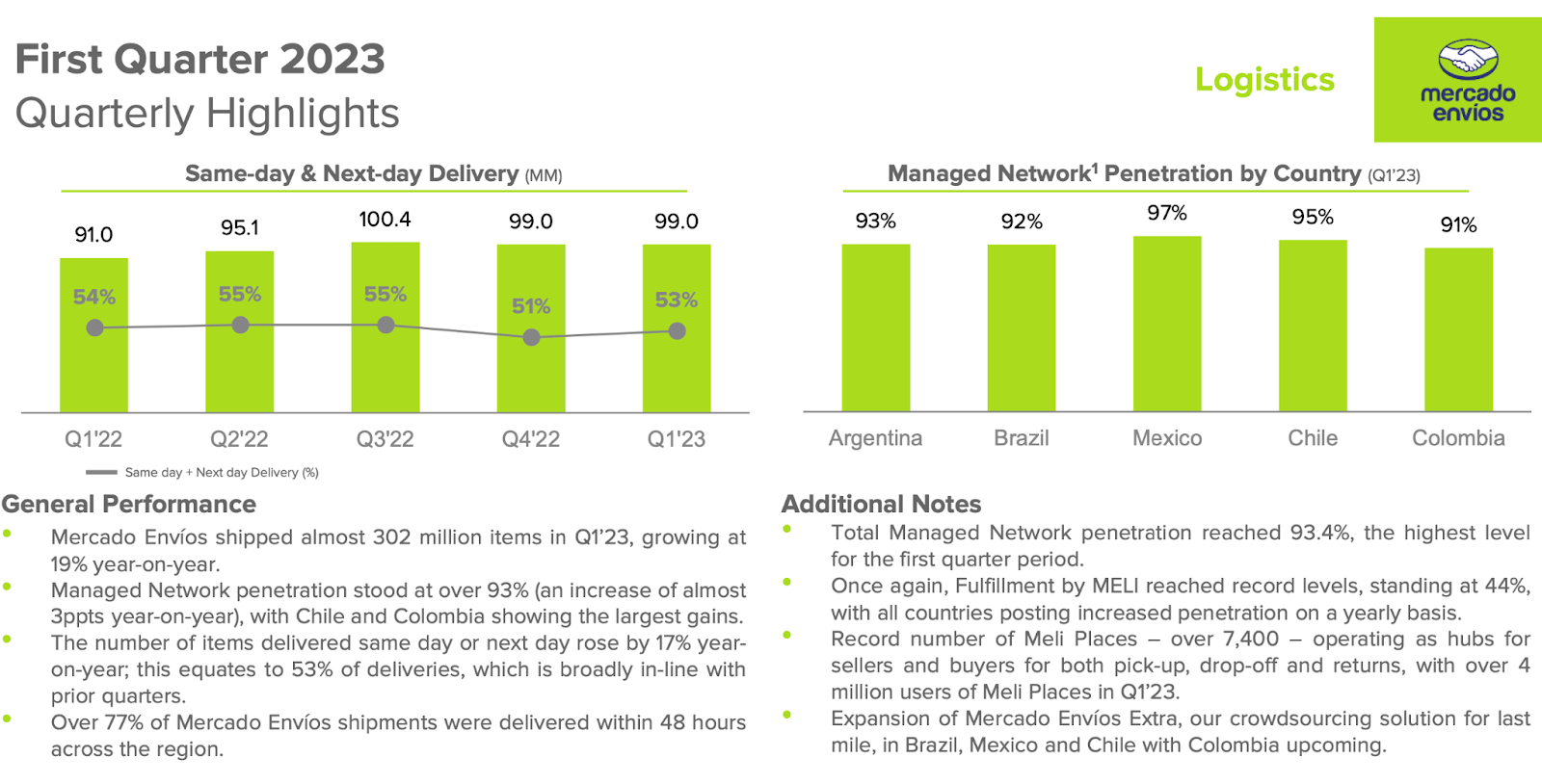

I mustn't overlook the impressive market position that MELI has earned in its core markets - this is evidenced by the company's managed network penetration and high level of fast delivery orders.

{kind=link}

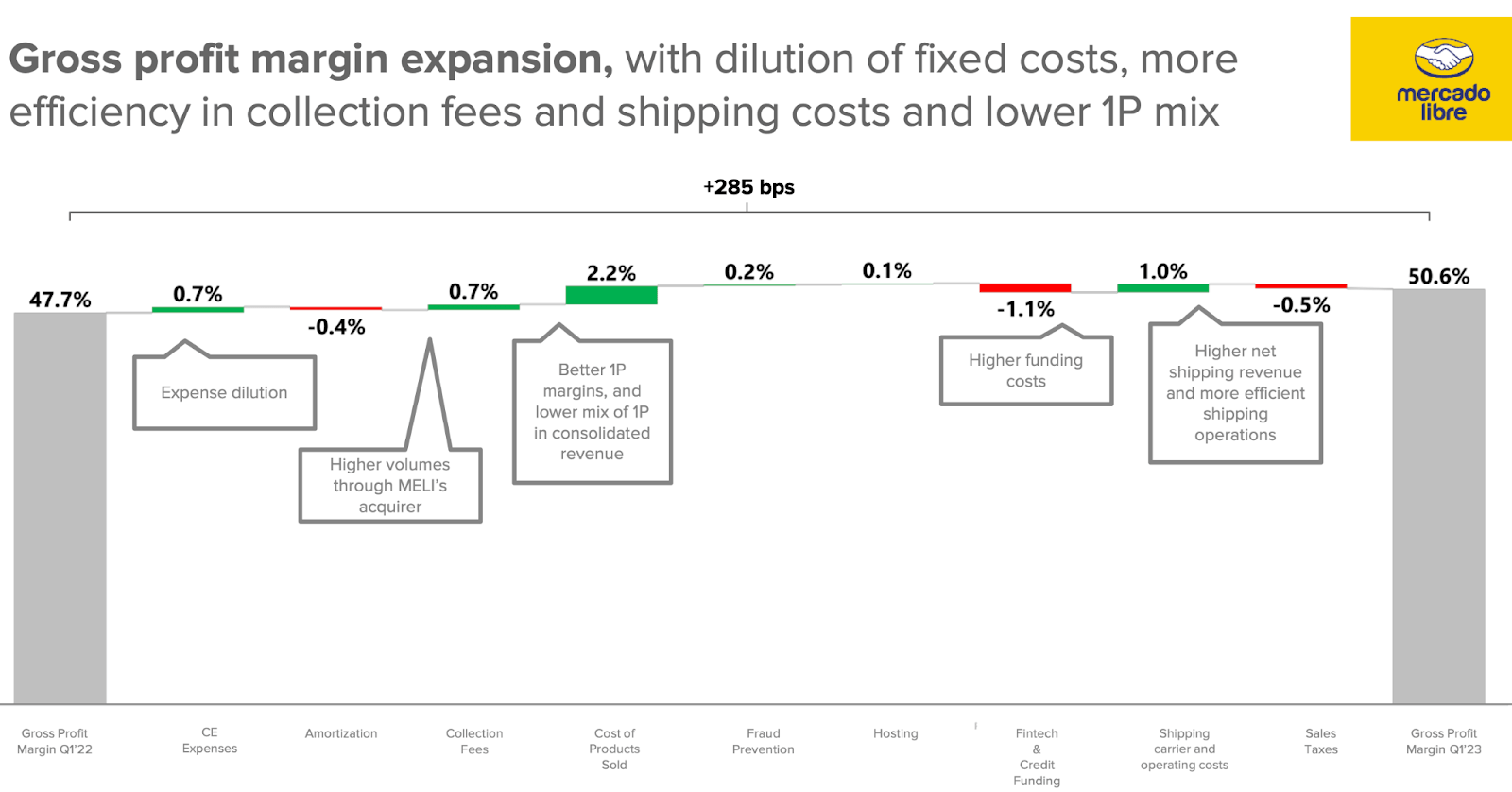

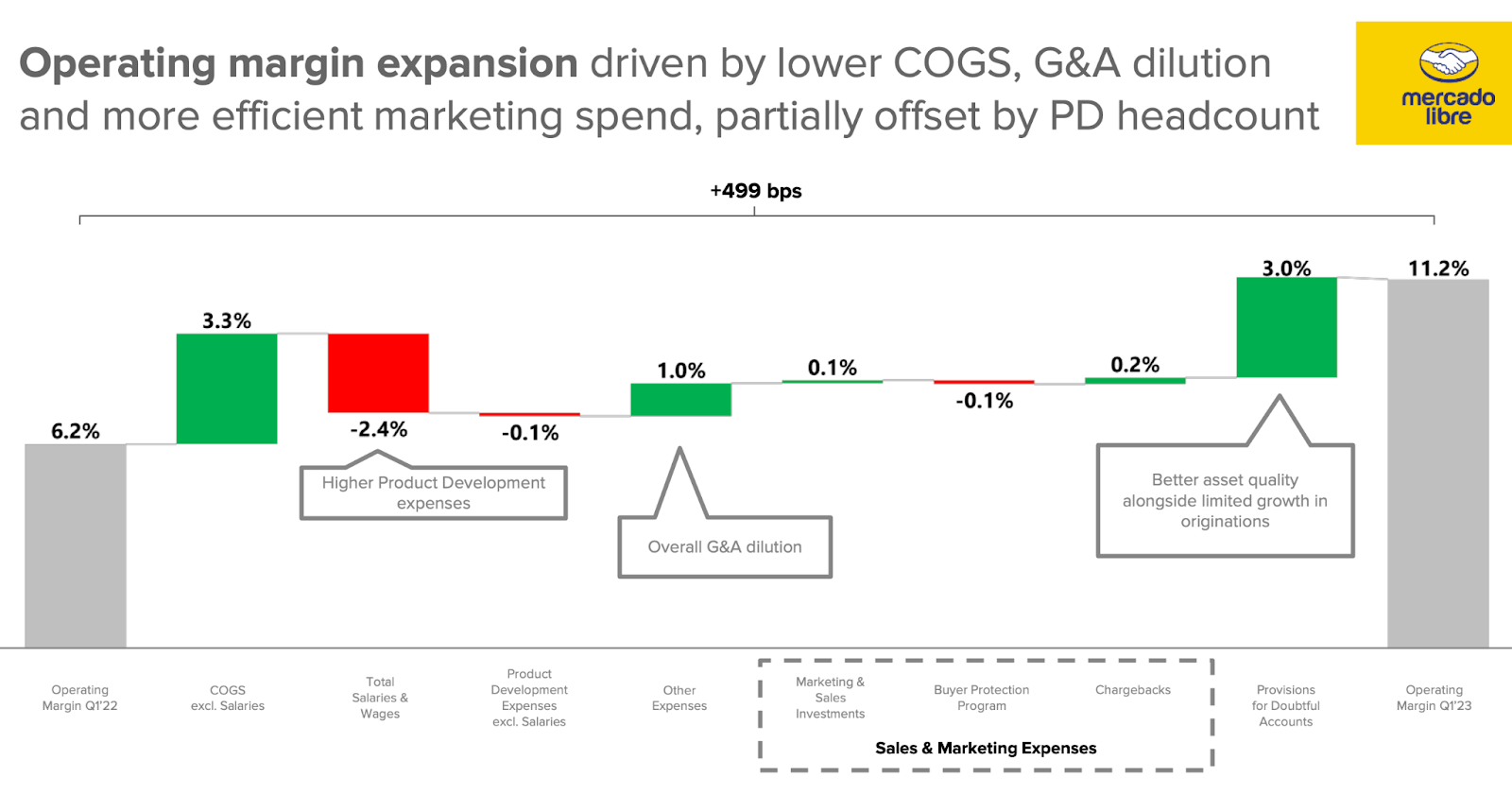

Besides the surprising tailwinds from Argentina, MELI has somehow been able to drive 285 bps in unit-level margin expansion, with gross margins rising to 50.6% in the quarter. On the conference call , management cited pricing power from being able to selectively increase shipping rates to boost profitability.

{kind=link}

That in turn helped operating margins expand 499 bps to 11.2%.

{kind=link}

With revenue growing at a 58% rate and earnings growing even faster, it is not too hard to understand why MELI has performed so strongly. I however wonder if this is a case of too much, too fast.

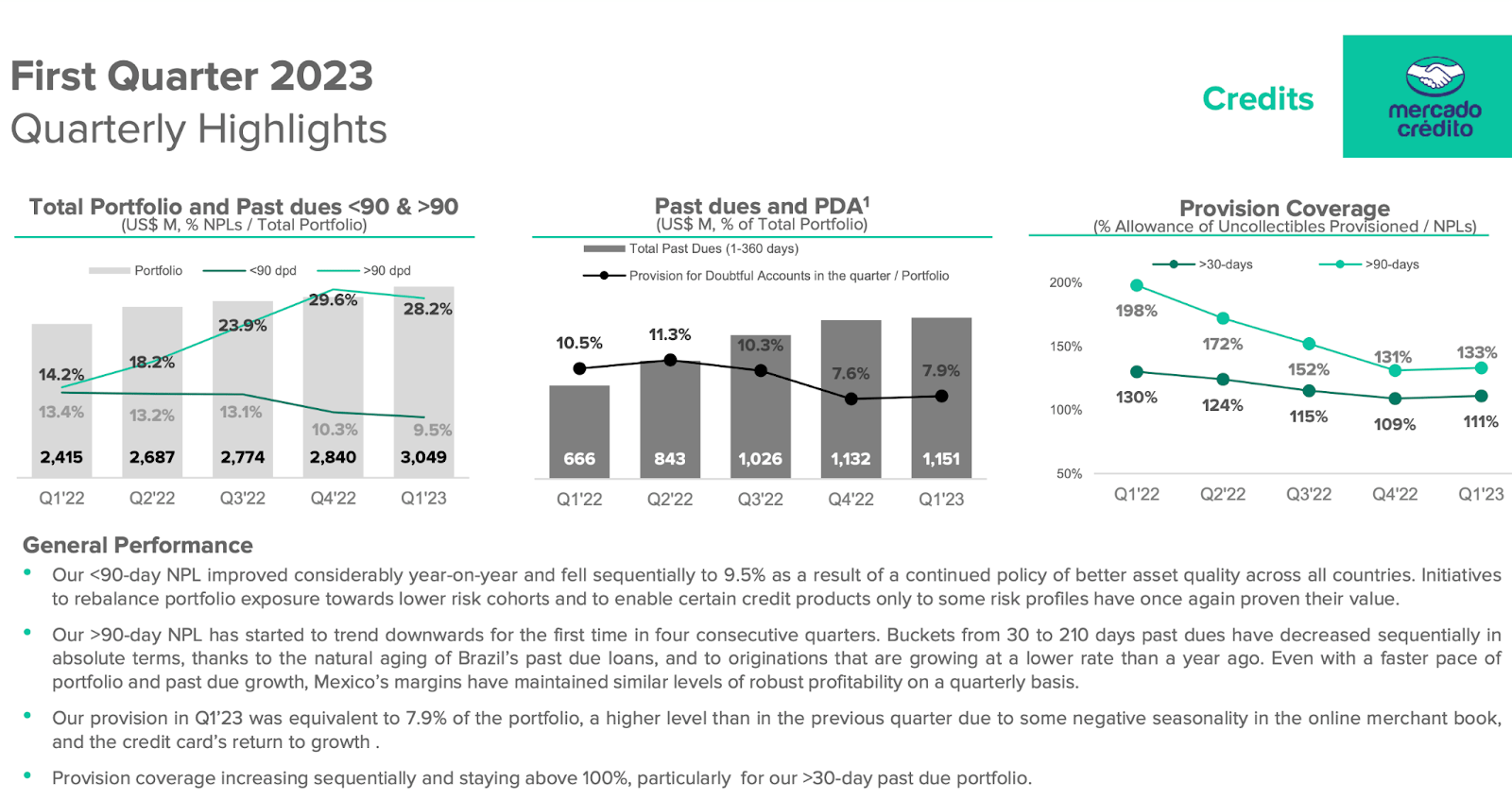

MELI has a significant credit portfolio with an unusually high percentage of loans past due. While the delinquency metrics have improved slightly in recent quarters, the high amount of loans past due is potentially concerning, especially considering the high inflation rates seen in Argentina.

{kind=link}

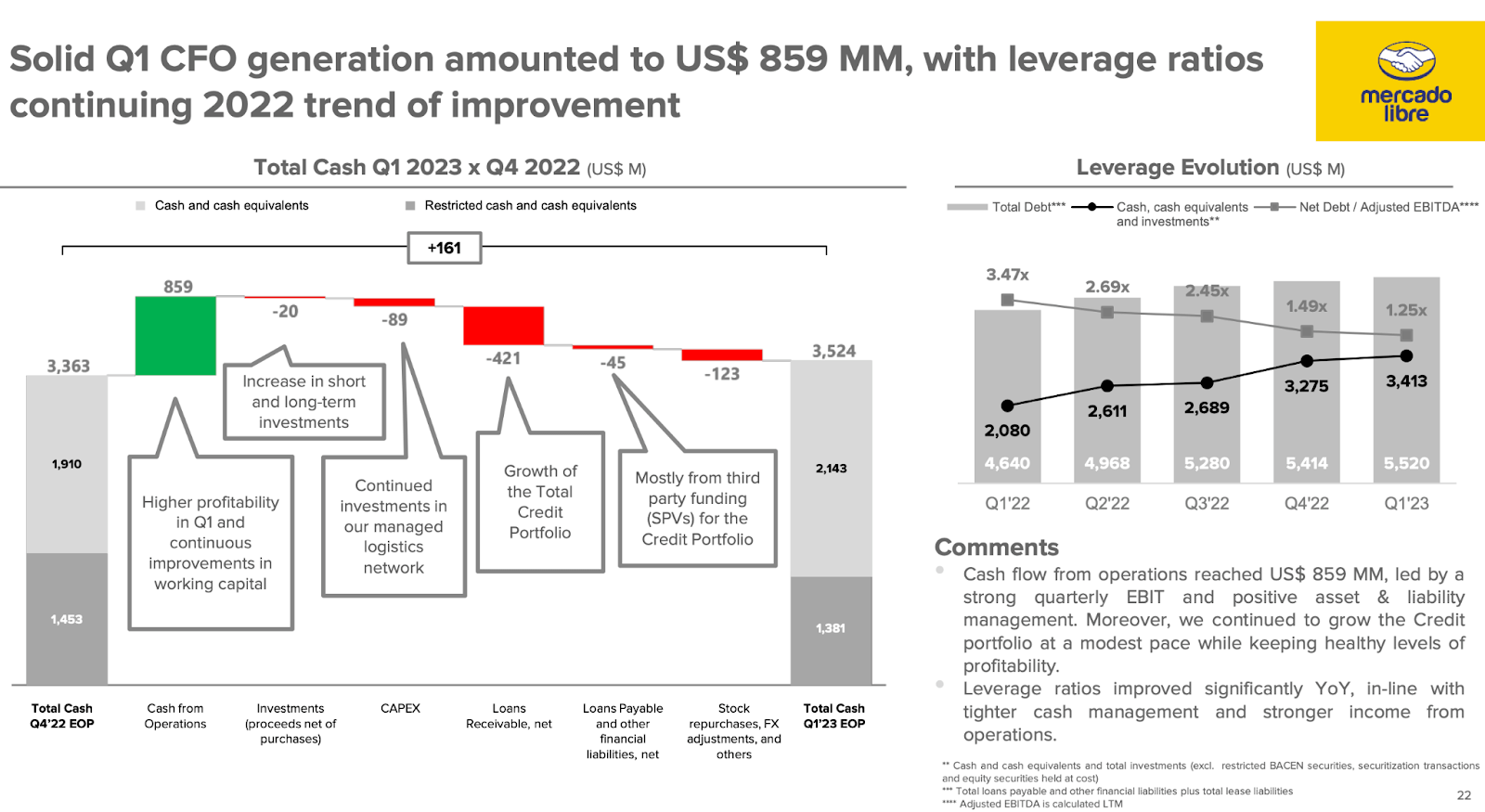

MELI has a net debt position which may be a catalyst for downside in the event of a breakdown in the credit markets.

{kind=link}

Is MELI Stock A Buy, Sell, or Hold?

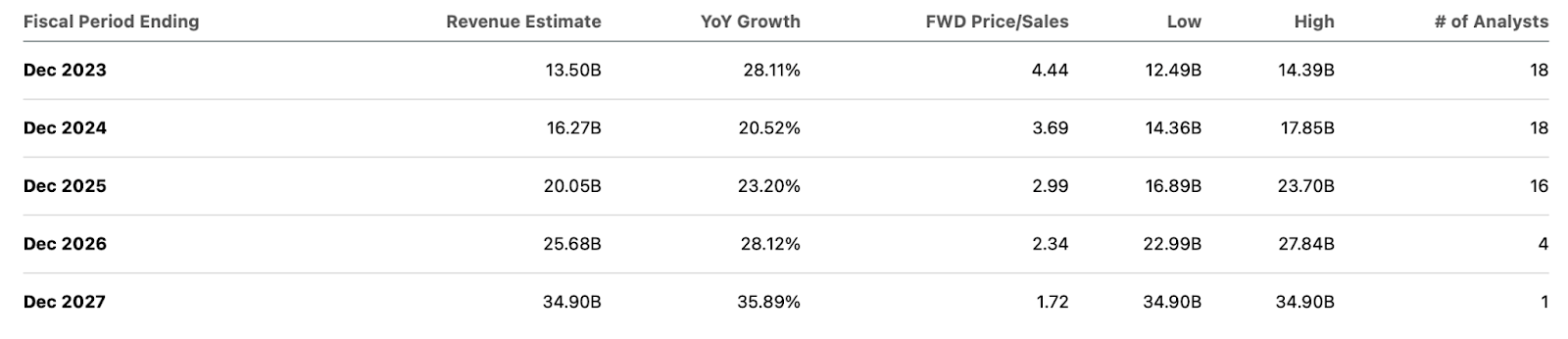

As of recent prices, MELI stock traded hands at just under 5x sales. That valuation does not look unreasonable considering consensus estimates - if anything, they look downright cheap.

{kind=link}

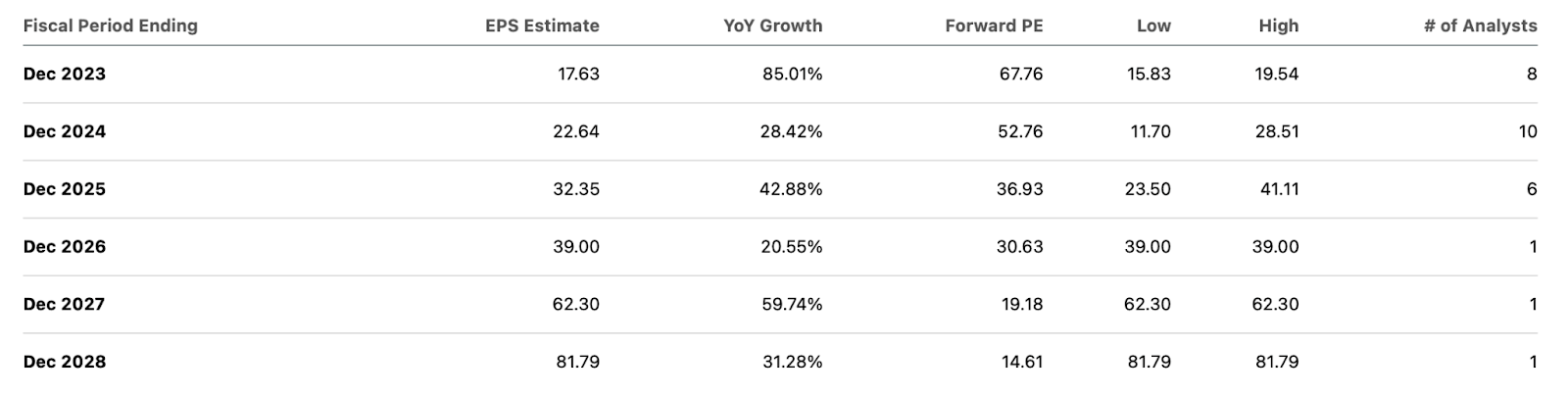

On an earnings basis, the value proposition is less clear as the stock is trading at 15x 2028 estimates.

{kind=link}

At current levels, the stock is clearly priced like a hyper-growth machine firing on all cylinders. That's a problem, and I have seen this story before. Several years ago, I was blinded by a similar story in Alibaba . At the time, BABA was growing very rapidly in the then-fast-growing country of China but the stock did not look obviously cheap based on near term earnings estimates. BABA stock has since declined precipitously due to both an increased geopolitical risk premium as well as deteriorating fundamentals in its home country. I am not quite prepared to predict that the same scenario is imminent for MELI, but the parallels are striking. The high inflation rate at Argentina and the high amount of loans past due in the credit book may be foreshadowing potential issues down the road. Due to the company's high exposure to Argentina, I wouldn't be surprised if the stock sold off heavily simply due to association. Argentina is estimated to have 40% of its population living in poverty - that does not make for a comforting backbone of the growth thesis. Moreover, consensus estimates call for minimal deceleration in growth rates moving forward, but how reasonable is that? Like other e-commerce operators, MELI saw growth rates accelerate dramatically during the pandemic and intuitively I am expecting the company to eventually see steep deceleration in growth just like North American peers. Sure, revenue growth might not come to a complete standstill given the lower adoption of e-commerce in LATAM, but one mustn't ignore the possibility that LATAM might not see such a rapid narrowing of that gap. If forward revenue growth rates instead decelerated to around 15%, far below the 25% consensus estimate, then I can see the stock trading down sharply. Based on 15% long term net margins and a 1.5x price to earnings growth ratio ('PEG ratio'), I could see the stock trading at around 3.3x sales, implying around 25% potential downside. I note that those assumptions are arguably optimistic, given that the company's operating margins recently stood at around 10% and a 1.5x PEG ratio is not incorporating much of an international discount. Based on a 0.75x PEG ratio, the stock might trade at 1.7x sales, implying considerable downside. I note that there are still some US-based companies that trade at similar PEG ratios, indicating that the downside from a widening of the geopolitical risk premium may be understated.

Meanwhile, if MELI can achieve consensus estimates of 25% growth, then I can see the stock trading at around 5.6x sales. That may imply that the stock can deliver around 20% forward returns based on growth, but this math illustrates how critical growth rates are for the valuation at these prices. While momentum and recent fundamental results may be pointing to more upside, I caution that the stock price is not pricing in a large enough margin of safety given the somewhat visible downside risks. I reiterate my neutral rating as it is difficult to gain the conviction to own the stock even in small position sizes.

For further details see:

MercadoLibre Looks Like Alibaba In 2019 - And That's Not A Good Thing