MELI - MercadoLibre: More To Its Profitable Growth Premium Than You Might Think

2023-12-23 10:00:00 ET

Summary

- Our initial $1.1K buy in point has proven to be excellent, with the MELI stock rallying immensely by over +45% since the dip after the previous article.

- Its prospects remain bright over the next few years, thanks to its well-diversified vertically integrated offerings across online retail, logistics, fintech, and advertising.

- MELI's management team continues to execute on growth opportunities, with the relaunched loyalty program already generating great results by FQ3'23.

- The company recorded a healthier balance sheet, with sustained share repurchases triggering the stock's consistent rise in value.

- We maintain our long-term conviction that MELI is a long-term winner, recommending investors buy at any dips, preferably at any upcoming pullback to $1.45K or lower.

We previously covered MercadoLibre, Inc. (MELI) in September 2023, discussing its solid prospects over the next few years, thanks to its well-diversified vertically-integrated offerings across online retail, logistics, fintech, and advertising.

Combined with the management's efforts to aggressively grow market share profitably, we had confidently reiterated the stock as a long-term buy, preferably after a moderate pullback to $1.1K.

In this article, we shall discuss why our previous Buy in point has proven to be excellent, with the MELI stock rallying immensely by over +30% since the dip after the previous article, thanks to its double beat FQ3'23 earnings call and excellent performance across all segments.

With the stock easily breaking out of its 50/100/200 day moving averages, we believe that the next floor may very well be at the $1.45K level, allowing interested investors to monitor there for an improved margin of safety.

The MELI Investment Thesis Remains Robust For Long-Term Investors

For now, MELI recorded double beat FQ3'23 earnings call , with revenues of $3.76B ( +10.2% QoQ / +39.8% YoY) and GAAP EPS of $7.18 (+38.7% QoQ/ +180.4% YoY).

The stickiness and increasing mindshare of its offerings have been demonstrated by the sustained growth in its Unique Active Users to 120M (+10% QoQ/ +36.3% YoY).

The same has been observed in the company's growing Marketplace ARPU of $225.84 (+2.3% QoQ/ +11.3% YoY), based on its Gross Merchandise Volume of $11.36B (+8.1% QoQ/ +31.9% YoY) and its Total Unique Buyers of 50.3M (+5.6% QoQ/ +18.3% YoY).

This naturally contributed to MELI's excellent performance in the logistics segment, with it reporting a record high of 48% for in-house shipment fulfillment ( +2 points QoQ / +8 YoY ) by the latest quarter.

Its previous capex investments have also paid off extremely well, with the company able to deliver 80% of its shipments within 48 hours (inline QoQ/ YoY) despite the greater volume of 116.3M (+4.6% QoQ/ +22.2% YoY).

Furthermore, MELI has reported greater fintech penetration, thanks to the introduction of PIX , the Instant Payment System launched by the Brazilian government in November 2020.

Despite the relatively young platform, PIX has already recorded a tremendous expansion in total number of monthly transactions to 4.08T (+5.6% MoM/ +67.9% YoY) by October 2023 and unique PIX accounts to 686.93M (+1.8% QoQ/ +27.9% YoY) by November 2023, with no signs of deceleration thus far.

As a result of the increased fintech adoption, it is unsurprising that MELI has benefited with a growing Total Payment Volume of $47.25B (+12.3% QoQ/ +46.8% YoY) and an impressive sequential increase in its Unique Fintech Active Users to 48.8M (+3.5M QoQ/ +7.2M YoY) by the latest quarter.

This further exemplifies its well-diversified strategy across physical retail through Merchant Services/ POS and e-commerce services through Digital Wallets, amongst others.

While these may have been promising developments indeed, readers must still note that MELI faces certain headwinds in its Credito segment, with its total portfolio's past due 90 days still elevated at 20.3% (-4.8 points QoQ/ -3.6 YoY) by the latest quarter, though notably improved on a QoQ/ YoY basis.

However, things appear to be moderately improving with the segment reporting healthier Net Interest Margin After Losses [NIMAL] of 37.4% (+0.6 points QoQ/ +7.7 YoY), up drastically from the 24.4% reported in Q1'22. This implies the management's improved ability to price risks thanks to its "credit scoring models leveraging the AI."

Most importantly, thanks to its financial institution license, MELI has been able to consolidate its credit portfolio across credit cards, instore/ online merchant lending, and consumer lending.

This naturally improves its profitability flywheel and cross-selling to its other fintech offerings, thanks to the management's laser focus on the low-to-mid risk segments without over exposing itself to Non-Performing Loans.

As a result of these promising developments, we are not surprised that MELI has generated a robust overall income from operations of $685M (+22.7% QoQ/ +131.4% YoY) and margins of 18.2% (+1.9 points QoQ/ +7.2 YoY) by the latest quarter.

Much of the tailwinds are attributed to the excellent performance in Brazil and Mexico, which have charted double-digit growth on a YoY basis at +40% and +66%, respectively.

This is thanks to the attractively-priced relaunched loyalty program in late August 2023, which offers free shipping, free content subscriptions to Disney+ and Star+ platforms, and a free music subscription to the Deezer platform, amongst others.

It is a testament to the highly competent management team indeed, which continues to maximize the company's growth opportunities across multiple channels while attracting new consumers.

The accelerating top-line and improved cost efficiency have directly contributed to MELI's improved balance sheet as well, with an increasing cash/ short-term investments balance of $5.49B (+66.3% QoQ/ +130% YoY) and moderating long-term debts of $2.14B (-12.2% QoQ/ -20.7% YoY) by the latest quarter.

Combined with its moderating share count to 50.21M (-0.94M QoQ/ -1.11M YoY), it is no wonder that the stock's value continues to rise thus far, despite the pessimism in the stock market and the region's raging inflation .

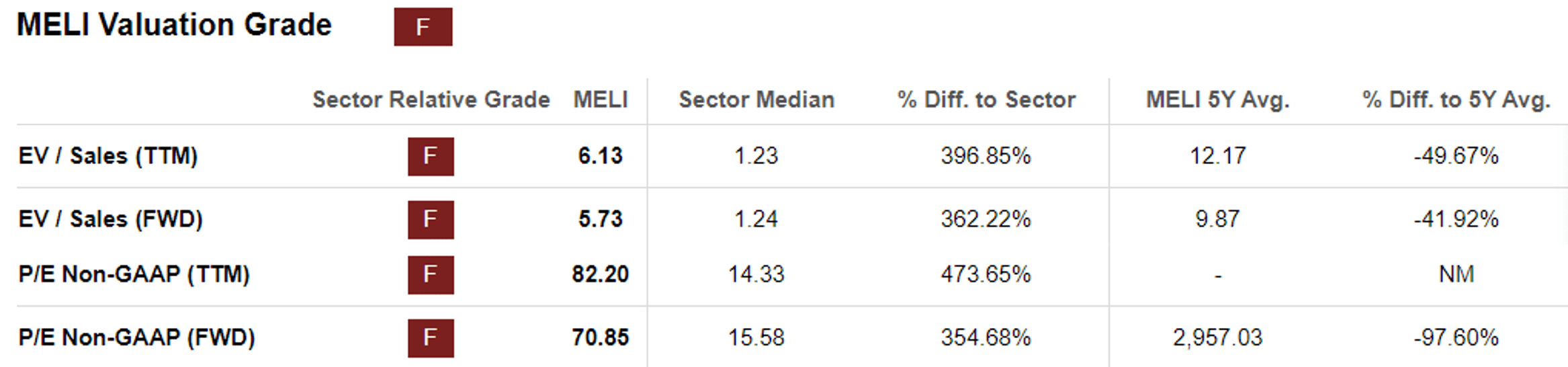

MELI Valuations

{kind=link}

On the one hand, MELI trades at a FWD P/E of 70.85x, notably moderated from its pre-pandemic mean of 98x, though somewhat elevated compared to most of its diversified e-commerce peers, such as Amazon ( AMZN ) at 56.01x, Shopify ( SHOP ) at 112.81x, and Sea Limited ( SE ) at 26.67x.

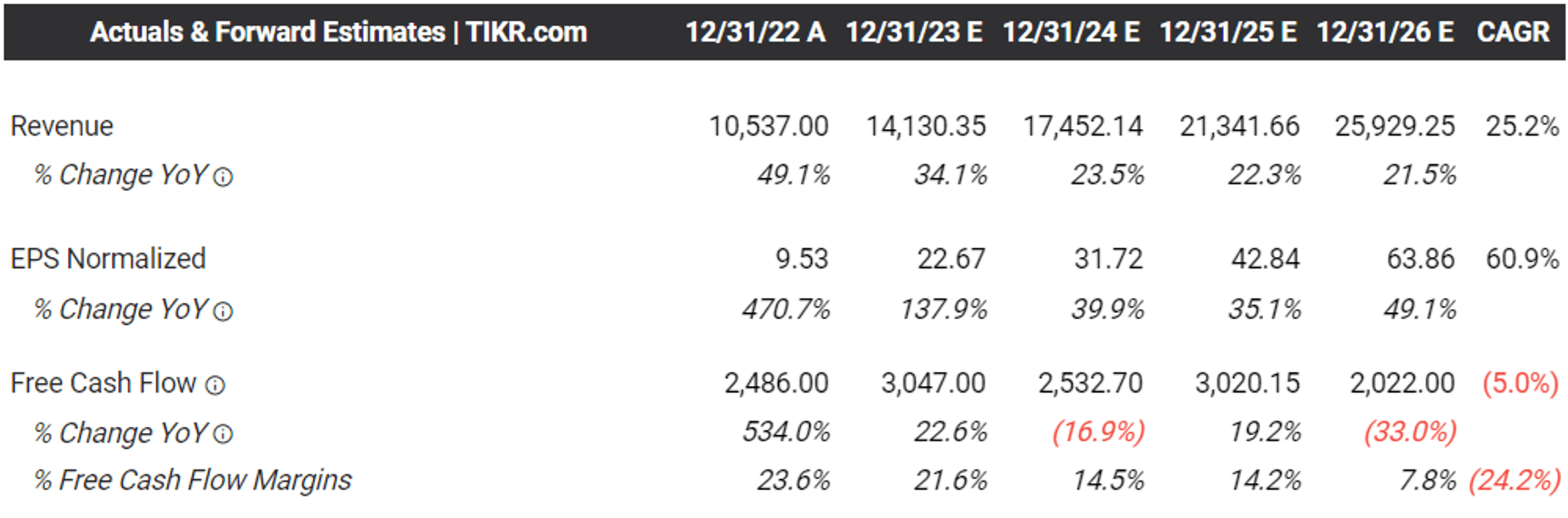

The Consensus Forward Estimates

{kind=link}

On the other hand, thanks to the excellent FQ3'23 results as discussed above, the consensus have also moderately raised their estimates, with MELI expected to generate an improved top and bottom line expansion at a CAGR of +25.2% and +60.9% through FY2026.

This is compared to the previous estimates of +22.5%/ +57.1% and historical growth of +52.3%/ +19.2% between FY2016 and FY2022, respectively.

If anything, MELI's projected top/ bottom line growth well exceeds AMZN's at +11.3%/ +31.4%, SHOP's at +10.2%/ +40.6%, and SE's at +21.4%/ +37.9% over the same time frame, implying that the former may deserve its highly profitable growth premium after all.

So, Is MELI Stock A Buy , Sell, or Hold?

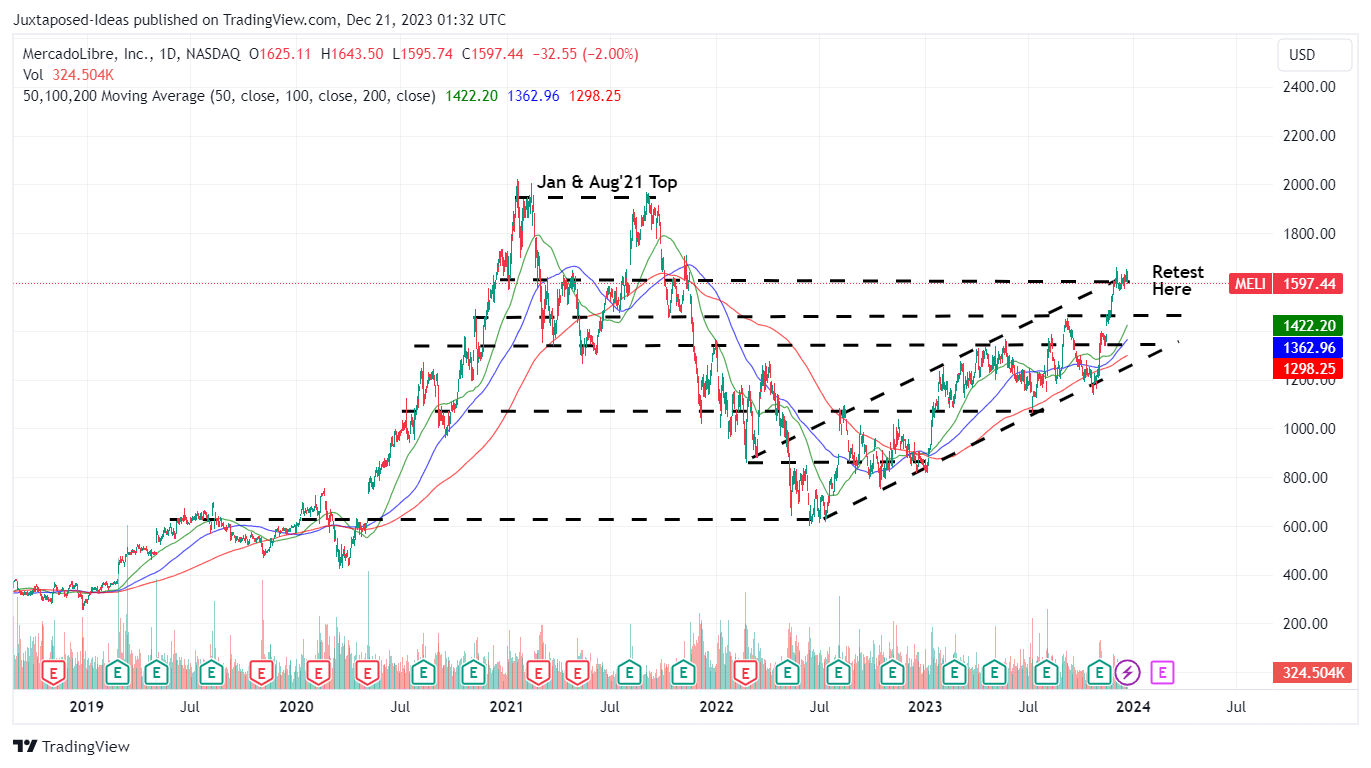

MELI 5Y Stock Price

{kind=link}

For now, MELI has risen tremendously by +34.5% since the October 2023 bottom, with it currently retesting its previous resistance levels of $1.6K while easily breaking out of its 50/100/200 day moving averages.

Assuming that this momentum holds, it appears that the stock may very well find its next floor at $1.45K, further sustaining its upward rally ahead.

As a result, investors may consider waiting for a moderate pullback to those levels, implying a -9.3% downside from current levels for an improved margin of safety.

We maintain our Buy rating, since MELI remains highly attractive for long-term investors seeking high growth, with a great upside potential of +88.9% to our long-term price target of $3,035, based on the consensus FY2025 EPS estimates of $42.84 and the FWD P/E valuation of 70.85x.

For further details see:

MercadoLibre: More To Its Profitable Growth Premium Than You Might Think