MELI - MercadoLibre: Pago Is To Mercado What AWS Is To Amazon

2023-06-20 12:26:17 ET

Summary

- MercadoLibre is one of the strongest and most diversified companies in LATAM, with excellent prospects for the future.

- However, future success will depend on the success of Pago and how it defends its competitive advantages against rivals.

- But as always with these high-flying growth companies, caution is advised as the valuation is expensive.

Thesis

Often compared to Amazon (AMZN), MercadoLibre ( MELI ) is a highly interesting company in a fast-growing market with plenty of room for future growth. And with their Fintech segment Pago, they have a similar success story to that of Amazon with AWS a few years ago. Both of these innovations have made an already strong company even better and changed its future prospects for the better.

As I believe Mercado has strong competitive advantages in the LATAM region, I think this could be an interesting investment for long-term investors with a time horizon of 5+ years, with the chance to generate market-beating returns.

Analysis

{kind=link}

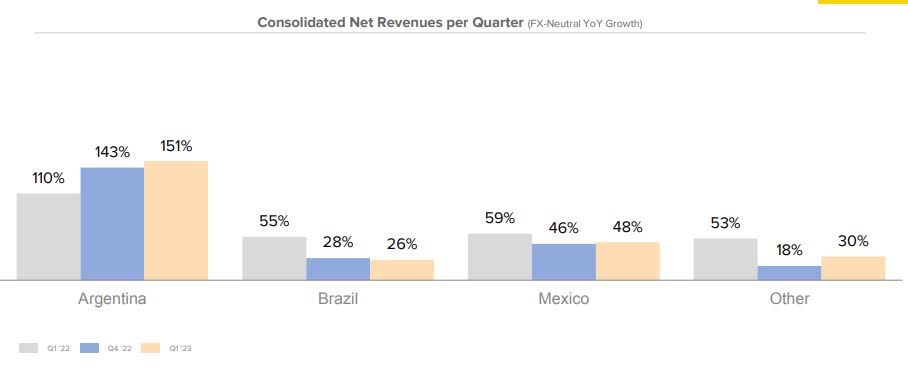

I think the other analysts have done a good job of summarizing the recent strong results, so I would just like to add a couple of things. Something we need to keep an eye on is the constant FX basis vs. the USD-adjusted growth rate, as the last results were significantly affected by the really fast and sharply rising inflation in Argentina . This made a big difference as the USD net sales growth rate was 35% and the FX neutral was 58%. The best metric would probably be an inflation-adjusted one, but that would likely mean a lot of work for Mercado, which might not be worth it.

{kind=link}

Here you can see that FX Neutral Argentina stands out, but if you look at the successful items sold in the last earnings report , Argentina's growth rate in Q1 was only 3%, so the ever-increasing inflation is affecting FX Neutral revenues. In USD, Argentina's net revenues only increased from $518m to $721m YoY, which is still a very nice growth rate, but nowhere near the FX Neutral growth rate YoY.

MercadoLibre Q1 2023 Presentation

On the other hand, I am pleased with the development of the cash position and the reduction in net leverage. Increasing cash and decreasing net debt is always good as it leads to more comfort financially.

And the very strong EBIT margin of 11.2%, despite the high level of investment in innovation, is also a strong result and would increase further if investment were to slow down.

However, I think that the investment in the Pago Fintech platform will be very important for future growth, and therefore I think that every dollar spent on this is a dollar well spent. Mercado knows what their clients need because they have a deep understanding of the LATAM countries, something that most US companies trying to compete in this region lack.

ROIC

Mercado is a quality company, there is no doubt about that, so a comparison with Amazon, the behemoth, is only fair, because if you want to be the best, you have to beat the best. And here we see one of Amazon's great strengths, which is its efficient capital allocation in the past, where they have achieved ROIC between 15% and 20% at a time when the cost of capital was low and therefore they had a wide ROIC-WACC spread.

Mercado, on the other hand, only has a 10% ROIC at the moment, but they are increasing their ROIC every year, and the companies that increase their ROIC over a long period of time have historically been some of the best investments. If they can increase it to 15-20%, Mercado's shareholders should be rewarded handsomely. In addition, the growth of the Fintech segment will lead to better margins and lower capital costs, as the commerce business is the more capital intensive.

Reverse DCF

{kind=link}

The reverse DCF is based on diluted EPS of $12.15 and the assumption that the EPS multiple will be 34x in 10 years. This leads us to conclude that EPS needs to grow by 25% over the next 10 years to justify the current share price.

Not an easy task, but Mercado is likely to generate strong FCF going forward, so there is a good chance they will buy back shares aggressively or invest in growth, both of which would lead to strong EPS if they use capital efficiently.

Risks

With a LATAM company, there are always the emerging market risks that some people don't like, and there is also the difficulty of different governments and their regulations. Especially in Fintech, it is difficult to get approvals from all the different countries. But once you have them, it is like a very big barrier to entry that other players have to overcome first.

Competitive Advantages

I believe Mercado understands the economic and environmental difficulties and differences, as well as the way of doing business in LATAM. This is an invaluable advantage over foreign companies. Amazon has been operating in Brazil for about 10 years and Mercado is still the leader . They have also built a brand that is very strong and very well known. It is no coincidence that Mercado is often referred to as the Amazon of LATAM, the PayPal (PYPL) of LATAM or the eBay (EBAY) of LATAM, as it is so diversified and the go-to platform for many things in LATAM.

With Pago, they are also building a digital payment platform that will be like a complete ecosystem for everything Fintech, and once it is big enough, they should have strong economies of scale and network effects. Even now, they offer a yield that is higher than the current accounts of most of the established banks in LATAM.

Plus, they already have the largest e-commerce platform in LATAM. So, in my opinion, the competitive advantage is strong and is likely to grow in the future.

Proxy Statement

Proxy Statement MercadoLibre

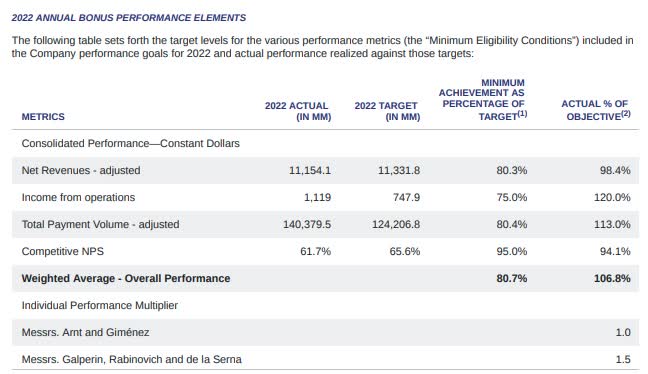

It is always good to know what the incentives of a company's directors are and whether they are aligned with the interests of shareholders. So I like to look at the proxy statement and I think net income and operating income are good measures for long-term considerations and so I like those metrics.

Payment volume and NPS are also two metrics for the Fintech segment that I think are good measures.

{kind=link}

Now, if we look at the results for 2022, we can clearly see that they have exceeded the targets and achieved an overall result of 106%. This reinforces my view that Mercado is clearly a success from a business perspective.

In addition, Marcos Galperin owns 7.57% of the outstanding shares, which should further underline his alignment with shareholders as most of his net worth is in the company's shares.

Valuation

{kind=link}

Yes, Mercado is extremely expensive with an EV/EBIT multiple of 49x. But their 5Y EBIT CAGR is also 88.69% , which is very strong, and even if they only achieve half of that, namely a 40% EBIT CAGR going forward, this could very quickly make today's prices look like a bargain in the future.

But I understand anyone who is frightened by this high valuation, I would rather see a 30x multiple, but quality growth stocks usually have their price. And sometimes it works, but there are plenty of examples where it has not worked for shareholders. So caution is advised.

Conclusion

Most analysts expect growth to revert to the mean, but there are those special companies that buck the trend and just keep growing, outperforming the industry for 10 years or more. And Mercado could be one of those companies, operating in an underpenetrated market where they have strong competitive advantages. In particular, the LATAM Fintech market has the potential for long-term growth. In total, LATAM has a population of over 650 million , so the opportunity is huge, and most of these countries have higher birth rates than the western world, so the population is likely to grow.

The focus on long-term success rather than short-term profitability is also one of the things I like about Mercado, as this is often a good indicator of strong future performance. All in all, I like the prospects for Mercado and think that even at this price, the likelihood of market-beating returns is relatively high at the moment. But of course I would not mind a lower entry price.

For further details see:

MercadoLibre: Pago Is To Mercado What AWS Is To Amazon