MELI - MercadoLibre: Q3 Earnings A Push For E-Commerce Dominance In Latin America

2023-11-04 05:28:08 ET

Summary

- MercadoLibre exhibited robust Q3 performance, showcasing significant growth in key metrics.

- Despite currency exchange rate issues in Argentina, the company achieved a remarkable 178% YoY growth in net income.

- The e-commerce segment excelled with a 45.3% YoY increase in net revenue, reaching $2.1 billion.

- While trading at a premium compared to peers, the current stock price doesn't fully reflect the company's growth potential, making it an appealing choice for investors.

MercadoLibre ( MELI ) stands out for its innovative approach to creating a business ecosystem that connects various needs and offers a comprehensive platform for sellers and buyers. Since the early days of online shopping in the early 2000s, the introduction of Mercado Pago was a pivotal move to facilitate and secure online transactions, dispelling the prevailing skepticism at the time.

This skepticism has largely vanished today, with nearly 60% of consumers in Latin American countries, such as Brazil, Argentina, and Mexico, making up to five monthly online purchases, especially in niche categories. Consequently, MercadoLibre's initiatives related to Mercado Pago are gaining momentum. The company's entry into the digital banking sector is one of these initiatives and has become a crucial driver for the company's substantial growth in recent quarters.

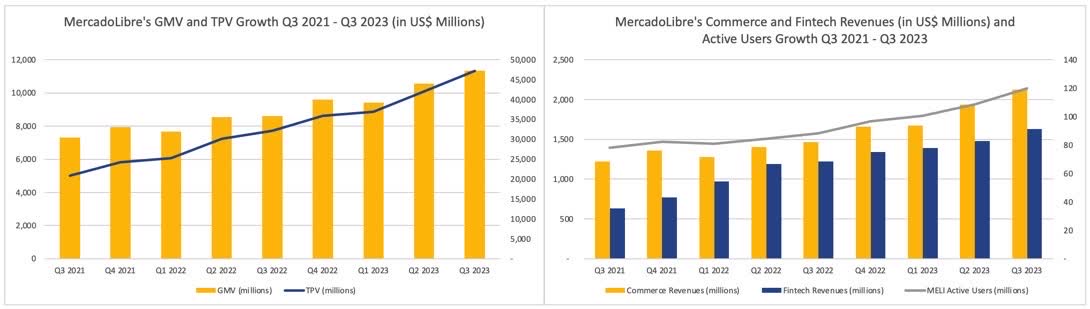

As mentioned in my previous article , the investment thesis for MercadoLibre is based on its aggressive growth strategy, consistently validated by the company's strong operational performance quarter after quarter in the past few years. This growth is evident in metrics such as GMV (Gross Merchandise Volume) and TPV (Total Payment Volume), as well as in the parallel expansion of its user base and increased revenues in e-commerce and fintech over the past two years.

Company's data, chart compiled by the author

{kind=link}

In its most recent results in 2023Q3, MercadoLibre faced challenges, including currency exchange rate issues due to the ongoing economic situation in Argentina, which impacted profitability. Despite these challenges, the standout highlight was the remarkable 178% year-over-year growth in net income. Despite concerns about Argentina's macroeconomic conditions, MercadoLibre's geographic diversification and multi-faceted business model have consistently delivered strong results, and Q3 was no exception.

As interest rates decline, particularly in the Brazilian market, with the Selic rate experiencing its third consecutive cut to 12.75%, there is increasing room for MercadoLibre to revitalize its credit origination efforts. In the e-commerce sector, investors had questions about MercadoLibre's ability to sustain its sequential growth rate.

However, a point of significant attention is the company's valuation, which is not new, as it is trading at a higher P/E ratio than Amazon ( AMZN ), for instance. Nevertheless, in my perspective, given its expanding presence in Latin America, growing market share, and continued geographic expansion, MercadoLibre remains an investment case that should yield favorable returns over the long term.

Key Highlights from MercadoLibre's Q3 Business Performance

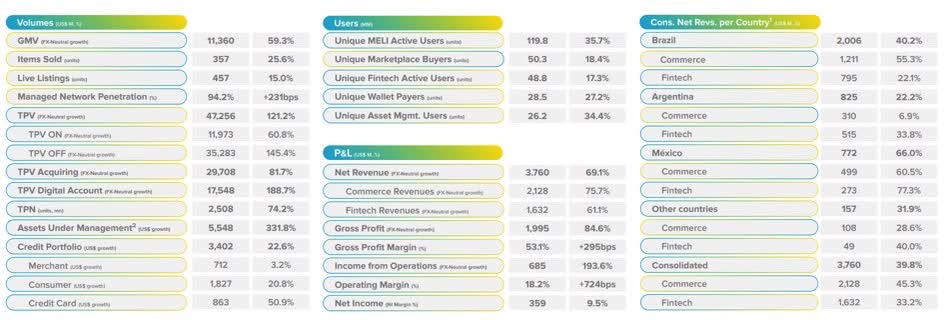

MercadoLibre has reported a strong quarter marked by robust revenue growth in its core e-commerce business. The company's e-commerce segment recorded a remarkable 45.3% year-over-year increase in net revenue, reaching $2.1 billion.

{kind=link}

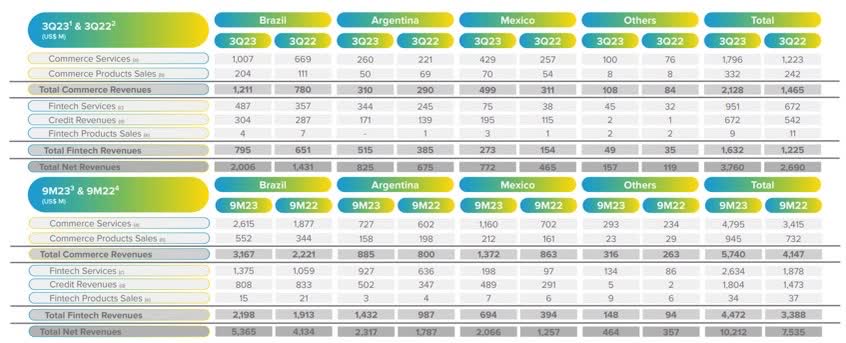

MercadoLibre's Commerce segment has maintained its market share and achieved significant growth in Gross Merchandise Volume (GMV), which reached $11.4 billion, growing by 31.8% year-over-year and showing a sequential acceleration of 8.1%.

Brazil, one of MercadoLibre's key markets, demonstrated strong performance, driven by a 27% year-over-year increase in the number of items successfully sold, reaching the highest growth rate since 4Q21. The expansion of items sold spanned across all product categories, thanks to promotional activities conducted during the quarter. GMV in Brazil stood at US$5.3 billion, marking a substantial rise of 38% year-over-year and 13.5% quarter-over-quarter. Mexico also delivered outstanding results, with a 59% year-over-year growth in GMV, totaling $1.6 billion.

The company's commerce take-rate, a measure of the revenue generated per transaction, reached 18.7% in 3Q23, reflecting an impressive annual growth of 170bps, driven by a sequential increase of 30bps. Several factors contributed to this robust growth, including higher penetration of Ads revenue, a revision of the marketplace flat fee in July, and increased shipping revenue.

MercadoLibre's IR

In the Fintech segment, merchants migrating to premium segments bolstered Total Payment Volume (TPV). The transaction volume reached $47.2 billion, with a 46.9% year-over-year increase and 12.3% quarter-over-quarter growth. TPV Acquiring, another significant component of the Fintech business, reached $29.7 billion, demonstrating a solid performance with a 37.7% year-over-year increase and 9% quarter-over-quarter growth.

With the addition of 6.1 million new "wallet payers" in the last 12 months, MercadoLibre expanded the volume transacted through digital accounts by 65.7% yearly. TPV Digital Accounts reached $17.5 billion, accounting for 65.7% year-over-year and 18.4% quarter-over-quarter. The company has attracted a substantial user base for Mercado Pago interest-bearing accounts, particularly in Argentina, where the demand for inflation-resistant financial solutions has led to over 10 million users.

Consolidated Financial Results for 3Q23

In the Q3 consolidated results , MercadoLibre has demonstrated impressive growth in net revenues, reporting $3.8 billion. This represents a year-over-year increase of 39.8% and a quarter-over-quarter growth of 10.1%.

{kind=link}

The company's costs for the quarter amounted to $1.8 billion, reflecting a 31.5% year-over-year increase and a 4.1% increase from the previous quarter. These cost increases are primarily attributed to new logistics investments to expand the fulfillment footprint.

The substantial improvement in MercadoLibre's gross profitability during Q3 can be attributed to several key factors. One of these is the more significant dilution of costs related to enhancing the customer experience. Additionally, the increase in "collection fees" resulting from a higher volume transacted via its acquiring and more substantial margins in the 1P (first-party, direct sales) segment significantly bolstered profitability. These dynamics offset the pressure of rising logistics costs, resulting in a significant margin gain. The gross margin exhibited a robust expansion in a year-over-year context of 295bps and sequentially 269bps, ultimately reaching 53.1%.

MercadoLibre's IR

MercadoLibre's SG&A expenses increased, totaling $1.3 billion, marking a 24.5% year-over-year growth and a 12.7% rise from the previous quarter. This increase can be attributed to higher sales and marketing expenses, with marketing costs rising by 32.4% year-over-year and 15% in the quarter. The marketing expenses were mainly incurred due to media efforts and activations related to new initiatives like Meli+, the company's streaming service.

Additional factors contributing to the rise in SG&A expenses include increased Research and Development (R&D) spending, which amounted to $396 million, representing a 7.6% increase from the previous quarter and a substantial 42.4% year-over-year growth. This was primarily driven by higher headcount, in line with the expansion plan initiated at the beginning of the year.

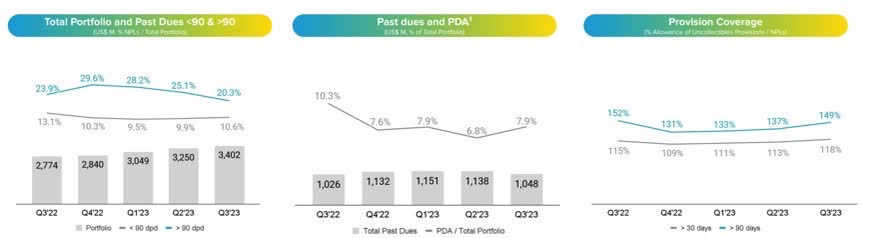

Provisions for doubtful debts ((PDD)) also played a role, with expenses totaling $277 million, reflecting a 24% increase from the previous quarter. These expenses increased due to a slightly higher pace of originations, resulting in the representation in the portfolio standing at 8.1%, compared to 6.8% in the previous quarter. Despite this, there was a significant reduction of 225bps year-over-year (compared to 10.4% in Q3 2022), leading to gains on an annual basis.

The rate of non-performing loans (NPL) over 90 days decreased for the third consecutive quarter, accounting for 20.3% of the total portfolio, as opposed to 25.1% in 2Q23. This decline can be attributed to a conservative approach to lending over the past year, focusing on lower-risk cohorts. On the other hand, delinquencies below 90 days (NPL<90) increased to 10.6% of the loan portfolio, up from 9.9% in 2Q23, an expected trend as the company accelerated the pace of originations.

{kind=link}

The EBIT continued to demonstrate growth and margin expansion, reporting $685 million, indicating a 22.9% increase in the quarter and a substantial 131.3% year-over-year increase. This positive result was fueled by more robust revenue growth and slightly lower costs, with the EBIT margin witnessing a significant rise of 721bps year-over-year and 189bps quarter-over-quarter. This was primarily a result of the dilution of expenses, especially in the General and Administrative (G&A) category, and an improved gross margin.

One notable concern in the quarter was the foreign exchange losses that continue to impact the operations. MercadoLibre reported a loss of $239 million, marking a 31.3% increase from the previous quarter and a significant 236% year-over-year increase. This is primarily attributed to the deteriorating macroeconomic situation in Argentina, with the country experiencing high inflation rates, with an accumulated rate reaching 146% in October. The persistent inflation crisis has been eroding the population's purchasing power, making it a challenging environment for sales volume. It's essential to mention that the market exchange rates significantly exceed the country's official figures.

But in the end, profitability remained robust, with a 178% annual growth and a 37.1% quarterly increase. Furthermore, MercadoLibre recorded a substantial increase in net margin, with gains of 188 bps quarter-over-quarter and 475 bps year-over-year.

Not Cheap Doesn't Make Unattractive

MercadoLibre stands out as the leader in growth and operations, particularly in the retail sector across Latin America. It holds the top in the Brazilian e-commerce market, commanding approximately 33% of visitors across its website and app. Nevertheless, maintaining this dominant position comes with a cost.

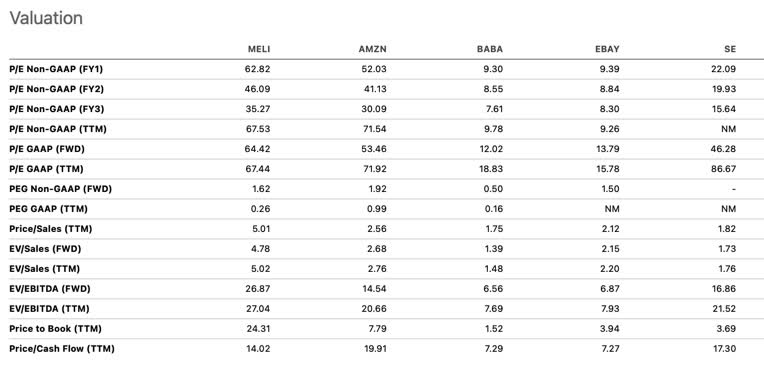

It's worth noting that MercadoLibre already holds a premium position compared to its domestic and international peers, including Amazon, Alibaba ( BABA ), eBay ( EBAY ), and Sea ( SE ). It trades at stretched valuation multiples, with an estimated forward EV/EBITDA of 26.8x.

{kind=link}

While it's recognized that MercadoLibre isn't a low-cost investment, this doesn't necessarily make it unattractive.

Despite its relatively high valuation, it's essential to consider that the current indicator is below the pre-2018 historical average of 29.0x, the period before the company's significant investments in logistics and financial solutions. MercadoLibre trades at a PEG ratio of 0.27, indicating how much investors will pay for each dollar of earnings the company generates. This may indicate undervaluation, as investors are willing to pay 73 cents less for each unit of earnings growth.

The Bottom Line

In the third quarter of 2023, MercadoLibre demonstrated improvements in nearly all key metrics, maintaining its robust growth pace, which aligns precisely with the core of the thesis. However, there were some minor issues in specific areas, such as a sequential increase in short-term delinquencies (NPL<90) in the credit portfolio and foreign exchange losses affecting the bottom line due to the economic situation in Argentina.

Despite concerns that e-commerce growth might slow down, the company has sustained robust sequential growth in Gross Merchandise Volume (GMV), outperforming its domestic competitors. This suggests that MercadoLibre still has room for expansion and growth in the e-commerce sector. Conversely, the declining interest rates in Brazil, MercadoLibre's largest market, create an opportunity for the company to expand its credit origination efforts.

Considering these factors, in my opinion, despite trading at a premium compared to its peers, the current stock price does not fully capture the numerous growth opportunities I foresee for the company, which I believe are substantial and robust. Therefore, I maintain my bullish outlook on MercadoLibre after its Q3 performance.

For further details see:

MercadoLibre: Q3 Earnings, A Push For E-Commerce Dominance In Latin America