MELI - MercadoLibre: Wide Moat Robust Growth Expensive Price

2023-04-06 10:59:17 ET

Summary

- MercadoLibre has arguably one of the widest competitive moats of any company, with no sign of narrowing.

- Management has strong capital allocation skills and is focused on creating new avenues for growth while expanding margins.

- Latin America is fertile ground for MELI’s newer business segments.

- Latin America has a greater inherent risk than other more developed regions, which directly impacts MercadoLibre.

- MELI’s 50% run-up in price YTD has taken it out of my fair value range. Investors should look for prices in the low $800s.

Investment Thesis

MercadoLibre ( MELI ) has proven to be a stellar investment over the last 10 years, returning investors over 100% annually and beating the S&P 500 by over 1,000%. The company seized first-mover advantages in a rapidly growing region and industry, Latin America ('LATAM') E-commerce, and has dominated the market ever since. In recent years, MercadoLibre has made strategic investments in new growth verticals such as Fulfillment, Fintech, and Advertising. This optionality allowed MELI to sustain annual topline growth in excess of 50% for the past 5 years and will continue to propel the company forward in my view. In addition to strong topline growth, the company is beginning to ratchet up operating leverage and should start exhibiting greater returns on capital.

Nevertheless, MELI's recent melt-up in price has pushed the stock above my max Buy price of $836 per share. The over-extended stock price combined with regional and macroeconomic uncertainty underpins my short-term Hold rating on MercadoLibre.

Competitive Advantages

Being a first-mover in LATAM E-commerce enabled MELI to establish a regional moat via brand awareness and geographic/cultural-specific knowledge. The goal of the founders in 1999 was essential to replicate the success of eBay ( EBAY ) in Latin America. eBay actually ended up being an early investor in MELI, purchasing a 20% stake in the business in 2001. MercadoLibre has grown with the broader region and E-commerce industry, gaining unique business & market knowledge that is tough for foreign competitors to attain. A few examples are relationships with governments and suppliers, more experience with LATAM economics/consumer trends, and cultural awareness.

MercadoLibre's success is also largely attributable to high-quality, experienced leadership. The company is still managed by one of its founders and has an average executive tenure of over 11 years. Harvard Business Review discovered that founder-led companies tend to outperform, in part due to a long-term, ownership-oriented approach to business. MELI also employs over 40,000 people throughout LATAM, many of whom highly approve of the company & CEO according to Glassdoor .

{kind=link}

Additionally, region-specific knowledge creates a barrier to entry for large foreign firms. Amazon ( AMZN ) began expanding globally throughout the early 2000s and is now the global E-commerce leader. Yet, it comes in second to MercadoLibre in monthly online visits and sales in several of Latin America's largest countries. MELI racks up 667.7 million monthly visits compared to AMZN's 169 million. Another example highlighting MercadoLibre's moat is Southeast Asia-based competitor Sea Limited ( SE ) discontinuing a large part of their operations in LATAM, in part due to macro uncertainty.

In addition to MELI's moat against foreign players, it has scale advantages over local competitors. MELI leads the pack in Gross Merchandise Value ('GMV'), with $34 billion in 2023 (over 20% of total E-Commerce GMV ). Americanas, MELI's largest local competitor, sold only $8 billion of GMV through its first three quarters of FY22. Similar to Amazon, MELI has built a massive fulfillment footprint (Mercado Envios) across the countries in which it operates. Enabling economies of scale, faster delivery times, and greater seller flexibility. Over 1.1 billion items were shipped through Envios in 2022. The company even has its own Airline in MELI Air. This creates a giant hurdle for both local and foreign competitors.

Optionality & Growth Potential

Robust competitive advantages & managerial experience place MELI on solid ground to continue dominating in Latin America. The past few years for MELI have been characterized by the capture of prevailing E-commerce tailwinds and the investment in new growth verticals. On the commerce front, LATAM continues to be an attractive geography harboring more than 300 million digital buyers, with that number expected to grow by 20% annually through 2027. Possibly MELI's most attractive growth opportunity is its fintech segment, Mercado Pago. Pago is heavily integrated with the MercadoLibre platform but also serves off-platform customers. Its main products are mobile point-of-sale (MPOS) solutions, Digital Wallet for P2P transactions and investment products, Merchant services for online payments, and Mercado Credito which is a credit business for merchants and consumers. Not only does this segment provide support for their core competency, commerce, it serves a wide variety of needs to Latin Americans. There are three factors that highlight Pago's potential in LATAM:

- Though this number is shrinking, about half of Latin Americans are underbanked or lack financial inclusion.

- LATAM has a near 80% internet penetration and is one of the fastest-growing regions for internet adoption.

- Almost 40% of transactions in Latin America are still made with cash.

Pago facilitates financial inclusion by giving the underbanked population access to investment products and credit digitally. Furthermore, MELI's fintech segment has already begun to outpace commerce in revenue growth (93% vs 46% in Q4 YoY, FX neutral) and has nearly caught up with commerce in total revenue ($4.7B vs $5.8B in FY22).

Another bet MELI is investing in is an Ad-Tech business. Ad-tech is a natural next step for the largest E-commerce company in Latin America as they work with millions of merchants. In tandem with expanding internet penetration in the region, LATAM is one of the fastest-growing digital ad spend markets, projected to grow 14% in 2023 to $13.7 billion.

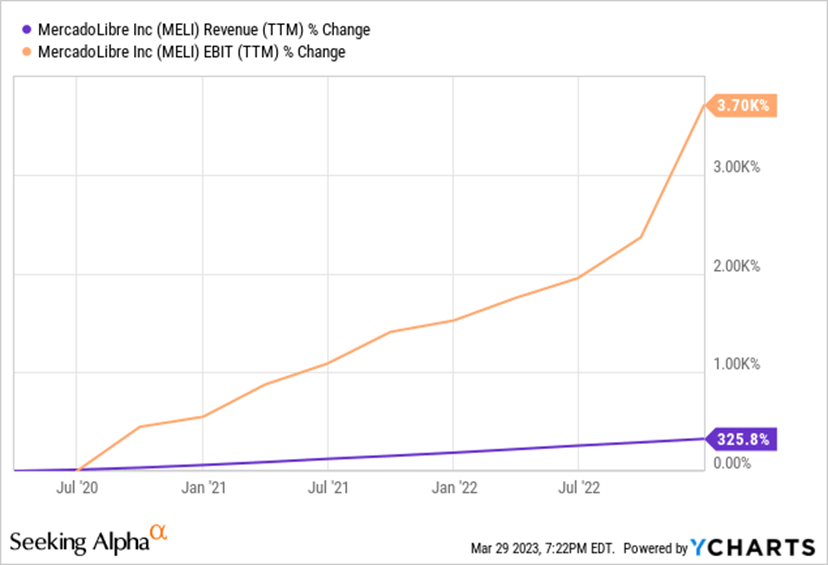

A common thread with MercadoLibre's newer business segments is the leveraging of their existing MercadoLibre user base. Instead of pursuing new growth via unrelated acquisitions, management utilizes in-house capabilities to venture into new lanes of business. It expanded into Fintech by offering payment services and credit to merchants, which led to an outgrowth of other Fintech products. Fulfillments and Ad-tech were approached in like manner. Each of these highlight management's strategic and capital allocation skills. In the company's Q4 transcript , CFO Pedro Arnt described MELI's strategic process for business segments. They aim at increasing annual EBIT while making measured investments in attractive business lines. Often a new business will start as unprofitable and over time develop more robust margins. Yet the company's overall EBIT is able to keep growing from their more established segments like Commerce and Fintech. This calculated approach appears to be paying off with EBIT growth far outpacing revenue growth since mid-2020.

{kind=link}

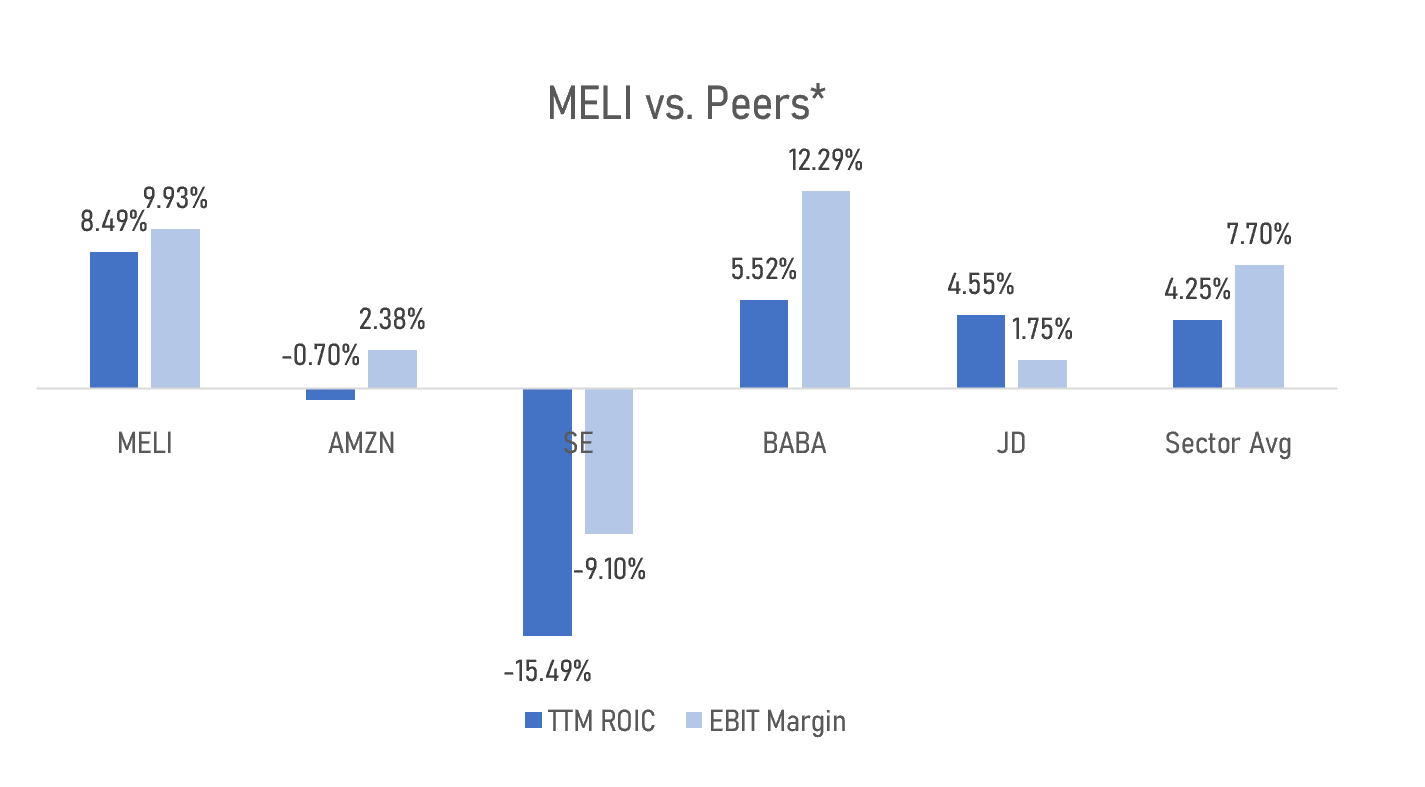

EBIT margins and ROIC vs peers are additional indicators of strong capital allocation abilities.

{kind=link}

Risks

Before diving into valuation, a discussion of risks is imperative given the nature of the Latin American region. MercadoLibre's primary risks include economic, political, currency, and credit risks. LATAM is less developed than other regions around the globe with many countries in the region considered emerging markets. Less developed, emerging economies are exposed to risks of high inflation, labor shortages, and lack of regulation. Given the current global economic challenges, LATAM runs a greater risk of adverse impacts and could be harder hit by recessions according to Deloitte . Many Latin American countries are large exporters and thus rely heavily on global demand. The region also has many governments with varying policies and regulation, which directly impact MELI's cross-border operations. In addition to this, foreign exchange risk is immense for MELI being there are more than 30 currencies in the Americas. Lastly, Mercado Credito is subject to default risk, especially given that the average Latin American borrower generally has less credit history, sometimes none at all. These risks drive up the required rate of return, and thus the cost of capital, for MercadoLibre investors.

Valuation

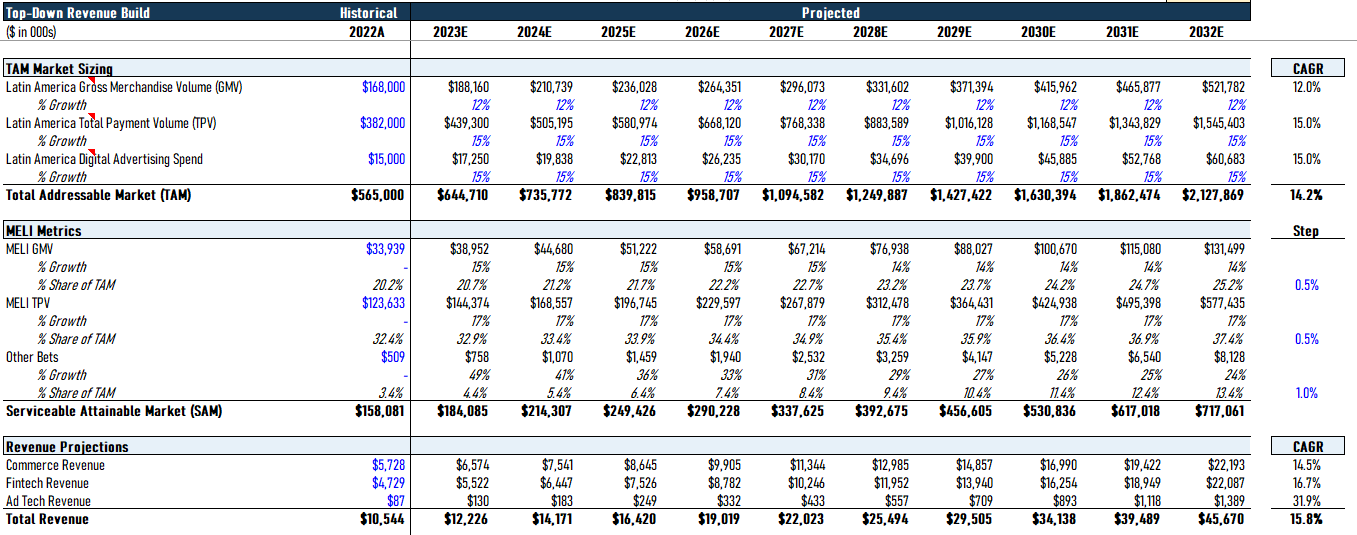

Below is a 10-year top-down revenue build for MELI starting with the company's total addressable market ('TAM') split by segment. Each segment's TAM is then projected forward 10 years using estimated growth rates from Statista. Then I projected MELI's GMV, TPV, and share of ad-spend, MELI's take rate (% that turns to revenue) of each of those metrics, and total revenue to arrive at an overall revenue growth rate of about 16% annually.

{kind=link}

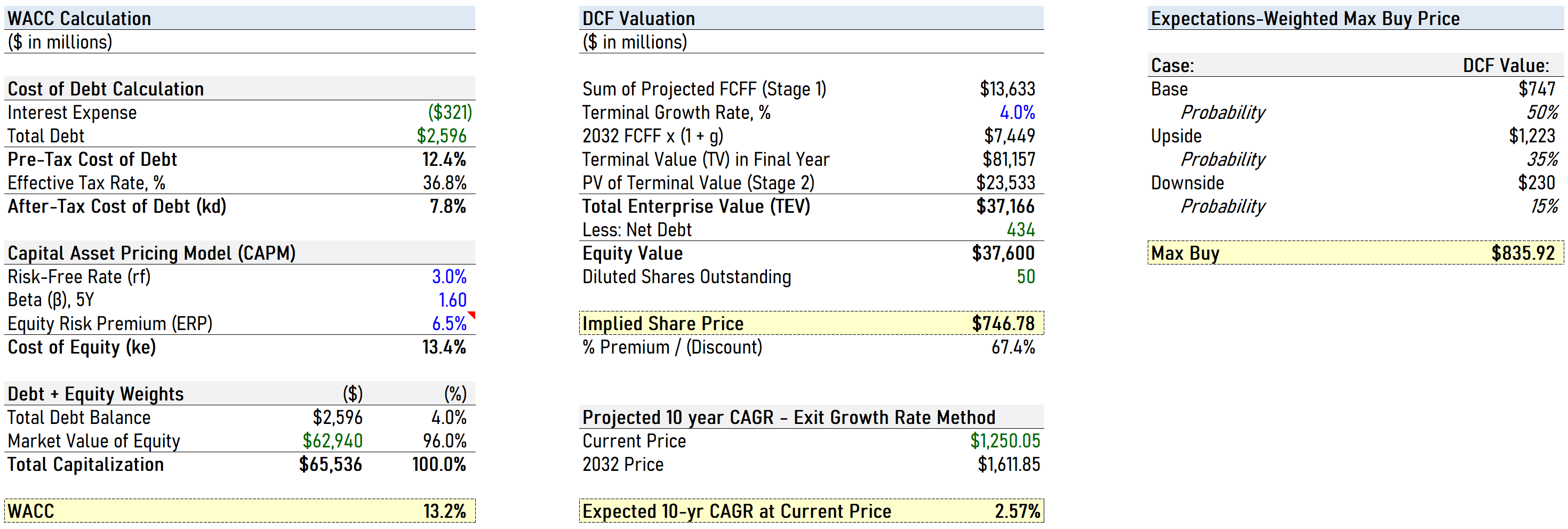

Moving down the income statement, I expect gross margins to slowly expand to 55% in year 10 driven by continued competitive pricing power. I also see MELI reducing SG&A margins over my forecast to 33% of revenues (currently 36%) driven by demonstrated operational efficiencies. I expect R&D margins to stay relatively consistent as MELI continues to invest in in-house capabilities. This results in EBIT margins climbing to the mid-teens by 2032. I expect a change in net working capital, depreciation & amortization, and capex to remain relatively consistent with historical numbers as a percentage of incremental revenue. The WACC I used for the DCF model is a relatively high at 13% given MELI's greater risk profile. Using a 4% terminal FCF growth rate, my base case DCF scenario resulted in an intrinsic value of $746.78 per share. MELI looks to be trading at a nearly 70% premium currently.

To evaluate different scenarios, I adjusted these assumptions slightly to the upside and downside. With three different scenarios (Base, Upside, Downside), I estimated the probability of each of these outcomes taking place based on my conviction. I see the base case as most likely with a 50% probability, and the Upside case as second most likely at 35% given MELI's historical ability to outperform expectations. This resulted in an expectations-weighted Max Buy price of $835.92. Investors should look to buy MELI anywhere below this price to capture annual returns of at least the cost of capital (13%) based on my assumptions.

{kind=link}

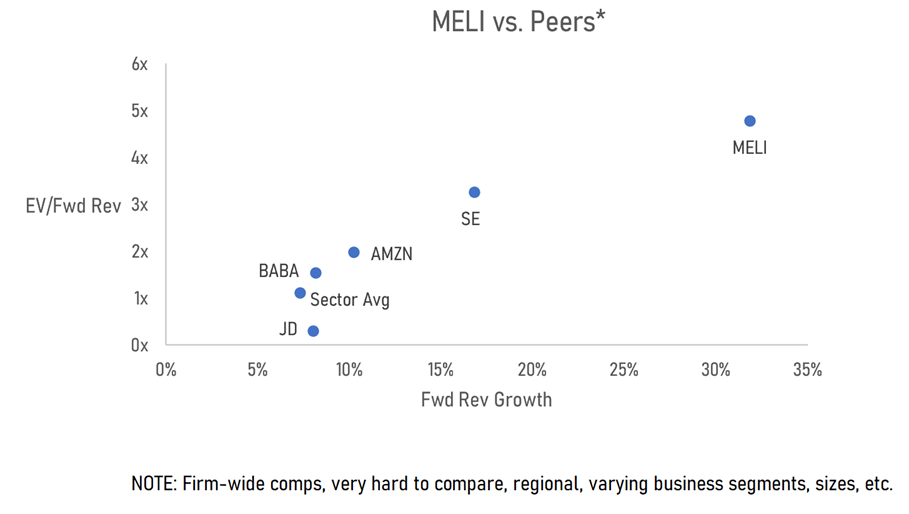

Looking at comparable valuation multiples confirms the stock price's current overvaluation. MELI tends to always be relatively more expensive but outpaces competitors in terms of topline growth.

{kind=link}

Conclusion

To summarize, MercadoLibre has possibly one of the widest competitive moats of any company and it shows no sign of narrowing. Management's ability to allocate capital effectively and create new avenues of growth makes the company's future look bright. Fintech and Ad-tech are already showing promising results, with LATAM ripe for this innovation. Nonetheless, MELI carries greater risk than similar firms in more developed economies and appears to be trading too far above a fair price for its stock. Investors should patiently hold until prices reach the $800s to capture the most long-term gains.

For further details see:

MercadoLibre: Wide Moat, Robust Growth, Expensive Price