UAL - Mesa Air Group Remains Infused With Risk

2023-05-01 13:47:29 ET

Summary

- Mesa Air Group did a lot to improve liquidity and operational performance.

- Uncertainty remains on how that will improve results this year.

- Upside remains, but the risk profile might make the stock a better hold than buy.

- Investors should pay attention to block hours and attrition, but key indicators of possible improvement won't be presented until next month.

I've covered Mesa Air Group ( MESA ) several times in the past year, and it has been a rollercoaster ride for shareholders. In the ideal recovery scenario for air travel, regional airlines would be leading the way as the recovery would flow from small jets connecting local communities to big wide-body airplanes connecting world cities and economies.

The reality, however, is different as pilot retirements led to a shortage of pilots in the recovery phase and mainline carriers started attracting pilots from the regional airlines and fish from the same pilot pool that regional airlines used to fill the pipelines, rendering regional airlines unable to execute on their contracted schedules. For Mesa, that ended up in loss-making operations for American Airlines ( AAL ) and an inability to execute the contracted block hours. In this report, I will be looking at what analysts are expecting for Q1 and provide a view on the risks and opportunities for the regional airline.

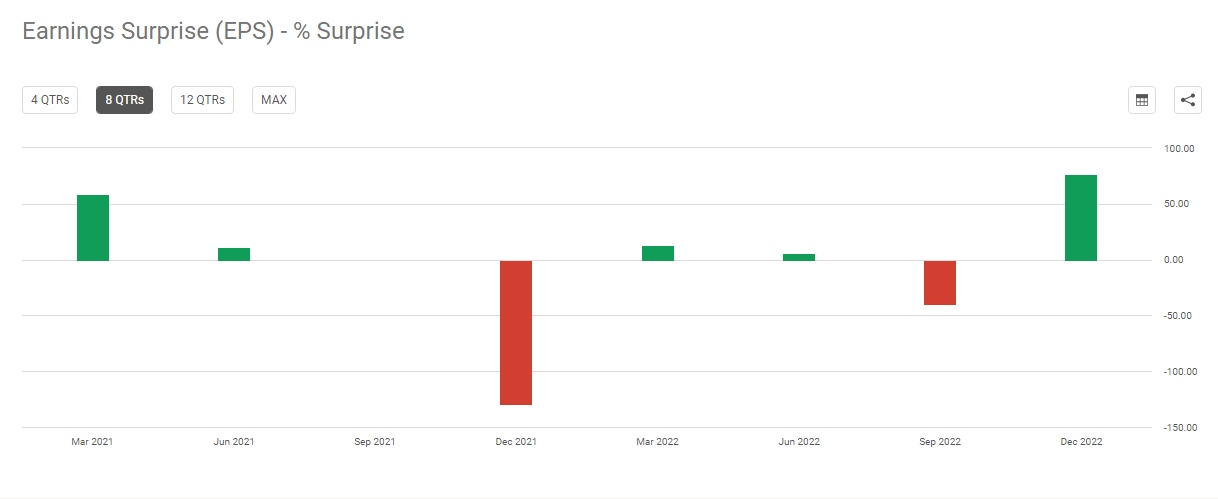

What Analysts Are Expecting For Mesa Airlines Earnings In FQ2 2023

{kind=link}

Mesa Air Group will be reporting earnings on the 9th of May after the closing bell. The consensus revenue estimate is $137.86 million, indicating 12% YoY growth with an expected loss per share of 21 cents. Over the past two years, Mesa Air Group beat EPS estimates five out of eight times while beating the revenue estimates half of the times. So, Mesa Air Group is not a company that is known for consistently beating the consensus. Over the past four quarters, however, the company only missed the EPS estimate once.

What Are The Risks and Opportunities For Mesa Air Group Stock And Operations?

Past performance should never be seen as an indication of future results and returns, so it's also important to consider the risks and opportunities for the company.

{kind=link}

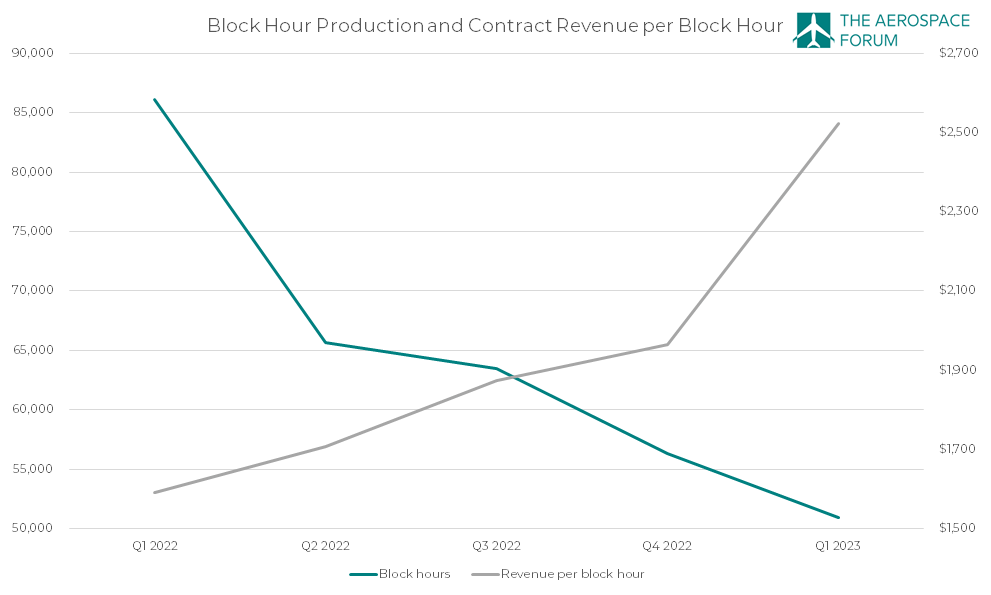

The obvious pain for Mesa Air Group is the reduced block hour production, and we see that at no point over the past five quarters, things actually got better. However, Mesa did shore up its liquidity position, as I discussed earlier. I'm not a big fan of companies selling assets to shore up liquidity, but Mesa did to secure survival amongst other actions taken. The revenues per block hour went up, primarily due to the fixed contract revenues being spread over fewer block hours.

Why things got so bad on block hour production was not in the control of Mesa. American Airlines decided to increase the pay rates at its owned regional subsidiaries but refused to do the same for Mesa Air Group. It resulted in other regional airlines and mainline carriers being more attractive for pilots compared to Mesa, resulting in an outflow of pilots. As a result, Mesa could not adhere to the American Airlines capacity purchase agreement and incurred penalties and losses of $15 million per quarter on the contracts. In some way it must have felt unfair to Mesa that American Airlines disrupted the market but didn't want to carry the consequences it had for an airline it had a contract with.

Eventually, the best course of action for Mesa was winding down the contract with American Airlines, which happened earlier last month. It partnered with United Airlines ( UAL ) which would cover the labor rate increases and provide liquidity next to a flurry of re-arrangements with stakeholders. Mesa increased pilot pay by 118% and saw attrition ease to pre-pandemic levels, which also was helped by a more predictable outflow path for pilots to mainline carriers.

With that in mind, we also can identify the risks and opportunities clearly. The opportunities are the following:

- Given lower attrition, block hours expansion might still be challenging, but it provides a base to think about block hour expansion.

- With the United Airlines CPA replacing the agreement with American Airlines $15 million in quarterly profits are being eliminated and replaced with profitable operations for United Airlines.

- There's potential to increase the operations for United Airlines to 38 airplanes.

There also are some risks and challenges for Mesa:

- The agreement with American Airlines covered 42 jets, with slightly more than 20 operational. The United Airlines agreement will not cover 42 jets but will include the operational jets with options to add more airplanes in the future. So, effectively it is a smaller contract to start with but provides little headwind as a significant portion of the 42 jets were parked.

- Mesa operates flights on behalf of DHL. If e-commerce sales soften, DHL might require less flights to be operated by Mesa.

- Mesa operates leased Boeing 737-400Fs for DHL, which the airline is not pleased with. In case of softening demand for e-commerce shipping, these leased jets could provide a cost headwind.

- It will take another 15 months in a conservative scenario to get to an industry standard utilization, meaning that the owned and leased assets will be underperforming for at least another year.

- With over $50 million in cash but over $700 million in debt and pressured operations, things remain challenging for Mesa.

Conclusion: Mesa Air Group Remains Risk Infused

I think what holds for Mesa is that it remains significantly risk infused. Attrition has come down, liquidity has improved, and operational contracts have improved, but that doesn't discount the fact that risk remains high. Probably with that in mind, my Buy rating on the stock has been too optimistic and a Hold would be more appropriate. I will revisit the valuation of the stock once the company has reported later this week, but based on current analysts' estimates and assuming those do include the elimination of losses from American Airlines operations, I continue to see a $2.60 price target in line with the industry enterprise multiple and up to $3.80 if analysts have failed to implement the loss reduction.

Either way, the hold is likely more appropriate. I await the upcoming earnings call to listen to management's comment on attrition and block hours production, but the real catalyst for the stock price could be in the next quarter when results from the United Airlines CPA should start to become visible.

For further details see:

Mesa Air Group Remains Infused With Risk