MU - Micron: Buy While Others Are Still Pessimistic

2023-07-03 14:36:30 ET

Summary

- Micron Technology stock has pulled back over the past five weeks, but investors are still holding on despite pessimism over the company's outlook and the impact of China's ban.

- The company's inventory digestion is taking longer than expected, but it is confident in gaining market share in the high bandwidth memory (HBM3) segment for AI chips from 2024.

- Investors should focus on MU's progress as its forward guidance suggests its gross margins should continue improving from the lows two quarters ago.

- MU's long-term uptrend remains intact despite the pullback in June, suggesting dip buyers are not unduly concerned. Maintain Strong Buy.

Micron Technology, Inc. ( MU ) investors have suffered a drubbing over the past month, as MU topped out at the end of May and pulled back over the past five weeks.

As such, MU last revisited levels it reached in mid-May but remained well above its critical late-April support levels. Therefore, I assessed that despite the pessimism over Micron's outlook at its recent earnings and the worse-than-expected revenue impact from China's ban, dip buyers are still holding on.

I updated Micron investors previously that MU regained its long-term uptrend after bottoming out decisively in December 2022, but has yet to benefit tremendously from the generative AI hype. Moreover, the recent pullback has also not changed the resumption of its uptrend bias, offering more investors an opportunity to partake in the pullback.

Notwithstanding, the inventory digestion is taking longer than expected, and my previous expectation of a second-half bottoming looks less likely now, based on the company's updated commentary . Moreover, the company's ability to leverage volume production of high bandwidth memory or HBM3 for AI chips is expected to begin only from Q1CY2024.

Micron sees HBM3 as a critical growth driver, expecting it to "contribute meaningful revenue in fiscal year 2024 and substantially larger revenue in 2025." Notably, it expects to take share against the current market leaders, SK Hynix and Samsung, which reportedly " dominate the global HBM market, with over 90% market share." As such, Micron's HBM3 ramp puts it well behind SK Hynix, which is already in volume production, while Samsung is expected to move into volume production by the end of 2023.

The uplift for MU investors is the company's confidence in gaining share in this segment, which management stressed would surpass "its natural supply share for DRAM in the industry."

Hence, I assessed that Micron's forward estimates have likely not reflected the potential accretion from its HBM3 gains, which could be a potential revaluation driver moving ahead.

Despite that, the company's exposure to the twin PC and smartphone headwinds should dominate its operating performance over the next twelve months. Management's commentary indicates that the inventory challenges could persist through FY24, even though the worst is likely over.

Therefore, investors expecting to see a near-term inflection in pricing trends in the underlying markets could be disappointed. Despite that, I think what's critical is that Micron is making progress, which justifies its December 2022 bottom that FQ2 was its worst (in terms of gross margins).

Keen investors should recall that Micron posted an adjusted gross margin of -31.4% in FQ2 (quarter ended February 2023). For FQ3, it improved to -16.1%. In addition, Micron's forward outlook for FQ4 suggests a further improvement to -10.5%. As such, while China's ban is unwelcome and is expected to slow the company's recovery, it's not insurmountable and not likely to cause Micron's margins to fall back into the abyss. Investors should focus on the progress, which is important to justify whether MU's December 2022 lows could hold.

Moving forward, I expect the battle between MU bulls and bears to intensify following the steep pullback in June as dip buyers are expected to return. Let me explain the critical dip buying levels to help sustain MU's nascent recovery.

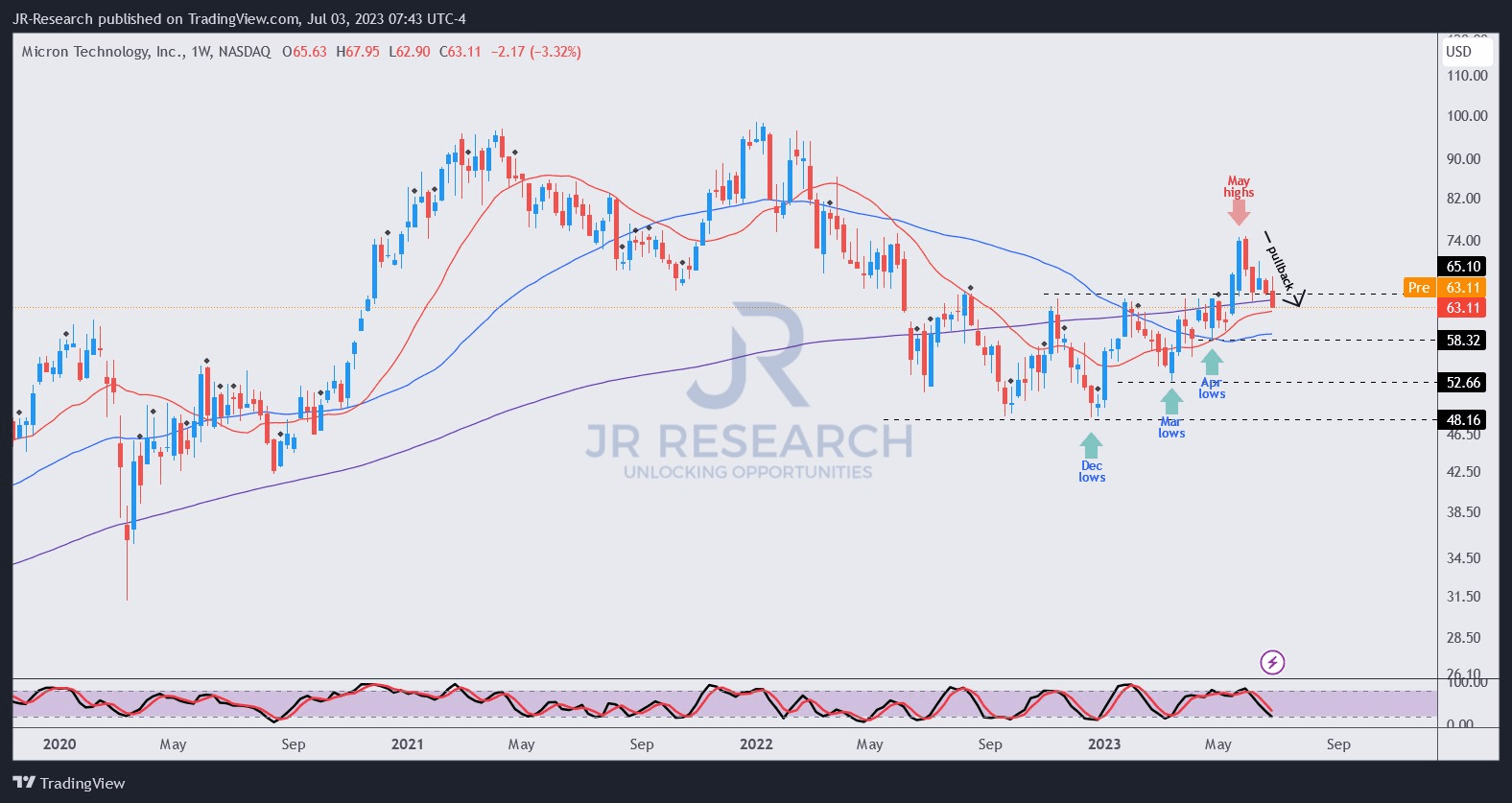

MU price chart (weekly) (TradingView)

{kind=link}

MU's breakout in May was aptly rejected, as dip buyers likely took profit and rotated out, taking advantage of MU's vertical surge, stunning breakout traders.

However, MU's nascent medium-term uptrend bias remains valid. MU's $58 levels must be keenly observed on whether dip buyers will return to defend the recent pullback.

I also see MU possibly holding out at the current levels, but there's no price action validation. Hence, investors should consider building out their exposure progressively and adding more if MU consolidates constructively at the current levels.

Also, consider keeping some spare ammo in anticipation of a steeper pullback toward the $58 levels, as dip buyers could return aggressively to defend it.

Rating: Maintain Strong Buy.

Important note: Investors are reminded to do their own due diligence and not rely on the information provided as financial advice. The rating is also not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have additional commentary to improve our thesis? Spotted a critical gap in our thesis? Saw something important that we didn't? Agree or disagree? Comment below and let us know why, and help everyone in the community to learn better!

For further details see:

Micron: Buy While Others Are Still Pessimistic