MU - Micron Is Positioned To Enjoy The Semiconductors Next Cycle

2023-11-04 01:39:41 ET

Summary

- Micron is an attractive investment opportunity in the information technology sector, operating in the growing semiconductor industry.

- The company has shown strong fundamentals with consistent sales and EPS growth, and has recently initiated dividend payments.

- Micron has growth opportunities in AI and electric vehicles, but faces risks such as negative gross margins and challenges in the PC market.

Introduction

As a dividend growth investor with a diversified portfolio, I seek new investment opportunities in income-producing assets. I often add to my existing positions when I find them attractive. I also use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income for less capital.

The information technology sector is attractive, and Micron (MU) in particular. The company is a new dividend-paying company, so we have a short track record to examine. However, the company is operating in the growing semiconductor industry, making it an exciting possibility to increase exposure. Therefore, the current market weakness is a good time to examine this company.

I will analyze Micron using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company's fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it's a good investment.

Seeking Alpha's company overview shows that:

Micron Technology designs, develops, manufactures, and sells memory and storage products worldwide. The company operates through four segments: Compute and Networking Business Unit, Mobile Business Unit, Embedded Business Unit, and Storage Business Unit. The company offers memory products for the cloud server, enterprise, client, graphics, networking, industrial, and automotive markets, as well as for smartphone and other mobile-device markets, SSDs, and component-level solutions for the enterprise and cloud, client, and consumer storage markets.

Fundamentals

The revenues of Micron have increased by almost 40% over the last decade, a CAGR (compound annual growth rate) of roughly 3%. The business, as can be seen in this graph, is highly cyclical as sales grow when clients have to replace their hardware. We are now at the bottom of the cycle, and there is optimism that we will again see sales growth in 2024. In the future, as seen on Seeking Alpha, the analyst consensus expects Micron to keep growing sales at an annual rate of ~30% in the medium term.

The EPS (earnings per share) shows an even more extreme figure than the sales. You can see in the graph below how cyclical the business is here and how the EPS is more volatile than sales. While EPS has increased over 400% during that decade, the company has shifted to loss as demand decreased, and it had to lower prices while maintaining its production and R&D operating. Like the sales, this downward is also expected to change. In the future, as seen on Seeking Alpha, the analyst consensus expects Micron to shift to positive net income in 2025 and grow it by almost 30% in 2026.

The company is a new dividend payer. It initiated the dividend payment 2021 and raised it by 15% in 2022. The company is paying a modest 0.65%, but the genuine concern investors may have is regarding its sustainability. The company lost money in 2023 and is likely to do it in 2024 as well. However, the payout ratio in 2025, when the EPS returns to be positive, is expected to be below 10%. Therefore, assuming the long-term trajectory of the semiconductor industry is intact, the dividend is likely to be sustained.

In addition to dividends, Micron has spent $4.2B towards repurchasing 63 million shares to reduce the share count between 2020 and 2023. Therefore, the number of shares outstanding has increased by only 4%. In 2023, the company spent $425M, yet it halted the buybacks temporarily to conserve cash and maintain the dividend. Buybacks are highly efficient when the share price is low, and if it drops while the business environment improves, Micron should consider buying back stock.

Valuation

The P/E (price to earnings) ratio of the company cannot be measured as the company lost money in 2023, and it is also forecasted to lose in 2024. However, as the company recovers and based on analysts' forecasts for the next year, the company is trading for 13 times future EPS. This is a reasonable and even attractive valuation for a company expected to enjoy growth in semiconductor demand.

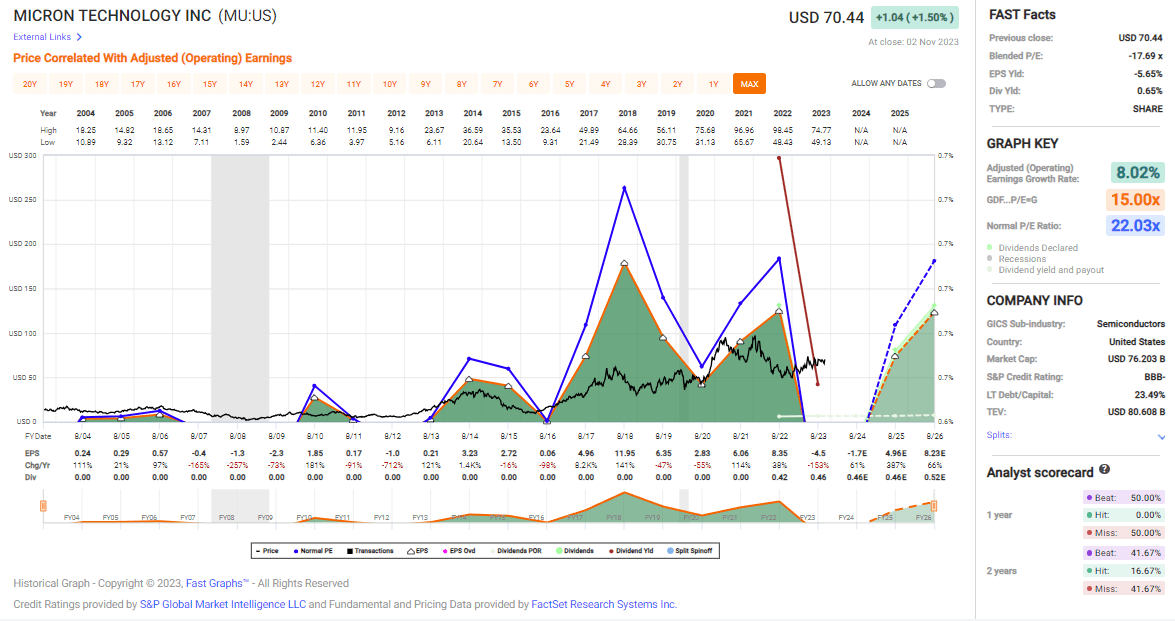

The graph below from Fast Graphs also shows that Micron is attractively valued. The average P/E ratio of the company stands at 22, and the average growth rate of the company's EPS stands at 8% annually. Therefore, once the company returns to profitability as it did in previous cycles, it will trade for a much lower valuation and will be in a position to offer much faster growth. Therefore, the shares are attractive at the moment.

{kind=link}

Opportunities

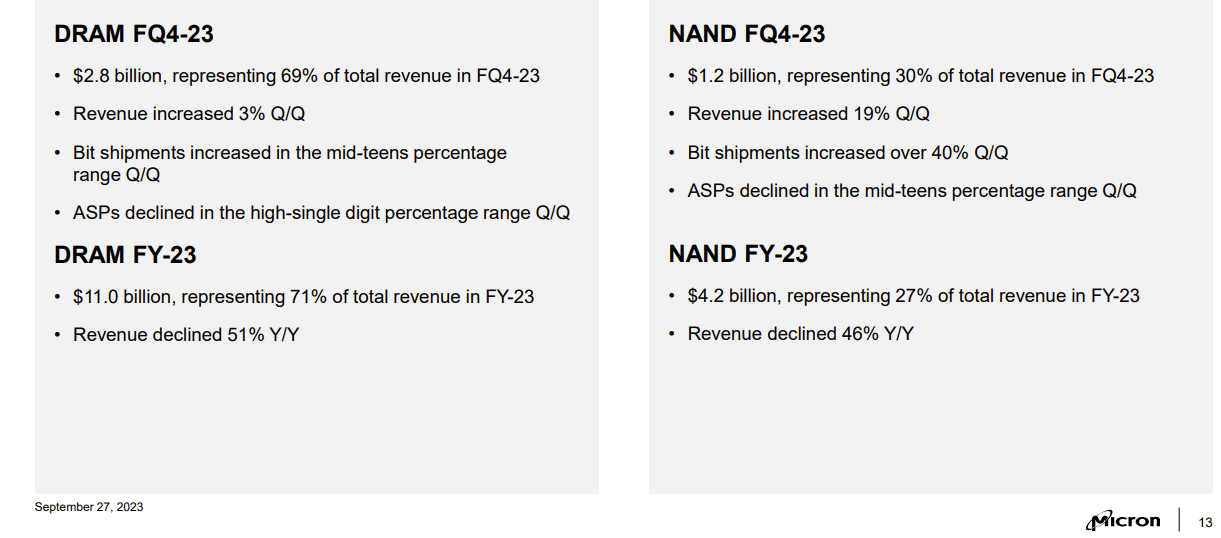

When looking forward, the first opportunity is the coming turnaround. Unlike vague turnarounds that companies promise, in the case of Micron, we can see it happening already. The company's revenues have decreased by ~50% in 2023. However, in Q4 of 2023, the company started enjoying an increase in sales Q/Q, which represents a good sign that the steep downward trend has come to an end. Moreover, the margins also improve. The gross margin that was negative 8% in 2023 is expected to be negative 4% in 2024, according to the company's outlook.

{kind=link}

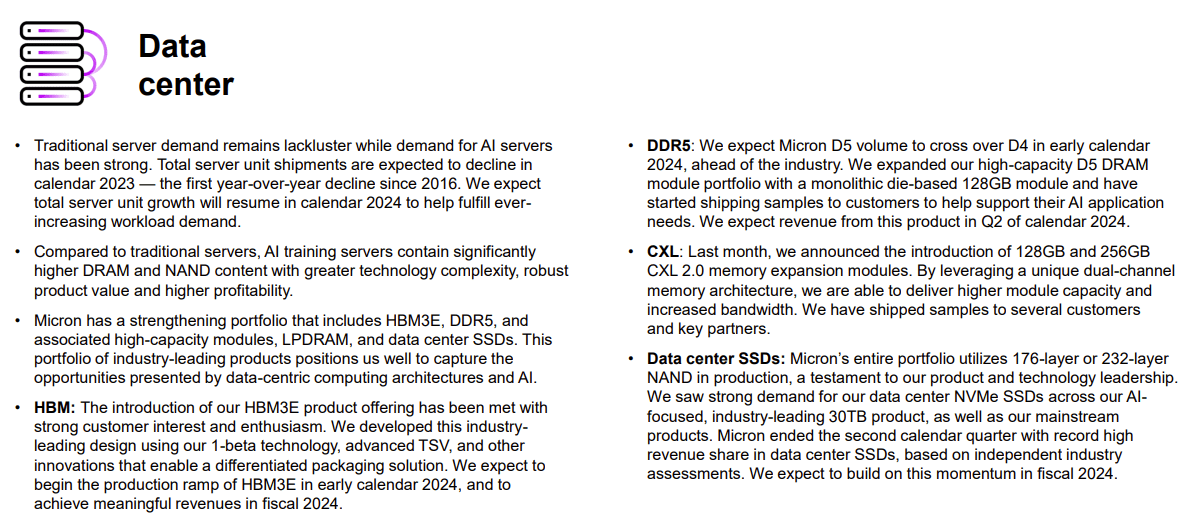

AI is an opportunity as the demand for AI servers remains strong. Micron's robust product portfolio, featuring high-capacity memory modules like HBM3E, DDR5, and data center SSDs, positions the company to capitalize on this growing market. AI training servers, with their complex technology requirements, offer higher profitability compared to traditional servers, and Micron's offerings are well-suited to answer this demand.

{kind=link}

In the automotive and electric vehicles, in particular, Micron's continued growth underscores its potential. With the increasing integration of advanced driver assistance systems (ADAS) and in-cabin applications in cars, the demand for memory and storage content per vehicle is set to rise. Additionally, the flourishing EV market, which tends to incorporate higher memory and storage components, presents Micron with a compelling growth avenue.

Risks

Investors face a risk with Micron due to the company's negative gross margins in 2023, which are expected to continue into 2024. These negative margins, initially at around -8% in 2023 and later at -4%, could impact the company's dividend if it remains. Additionally, there's a risk of a delayed turnaround, where the company may take longer than expected to become profitable. This delay could be attributed to unforeseen market challenges or global economic uncertainties. The signs are positive, but there is a risk of underachieving.

While there are signs of easing tensions between the U.S. and China, as demonstrated by China's openness to Micron Technology's expansion in its market, the ongoing political and economic uncertainties remain a risk for American companies operating in China. The recent gestures of goodwill may not guarantee a stable and secure environment for U.S. businesses, given the history of fluctuating relations between the two nations.

The PC market faces a risk with an expected decline in unit sales for 2023 and modest growth in 2024. Economic and supply chain disruptions may challenge the reliance on AI-enabled PCs for growth. Despite some increases in specific components like LPDRAM and SSDs, the PC industry remains vulnerable to external factors. The company is working to decrease the share of PCs in its sales, but the decline may still be challenging.

Micron Q4 Earnings

Conclusions

To conclude, Micron is an excellent company with a long track record of success in the semiconductor industry. It operates in a highly cyclical business, which presents a challenge. Yet, it showed strong fundamentals with long-term growth of sales and EPS and even returning capital to shareholders with dividends and buybacks. The company has several growth opportunities, mainly around AI and electric vehicles.

The company's risks are highly relevant as it operates in a competitive environment that amplifies them. The company has to shift back to profitability and overcome weaknesses in PC sales. However, at the current valuation, especially when using the future EPS, I believe that there is enough margin of safety for these risks. Therefore, I think shares of Micron are a BUY at the current price and in the current business environment.

For further details see:

Micron Is Positioned To Enjoy The Semiconductors Next Cycle