MSFT - Microsoft: Fire On All The Cylinders And Thrive In The Era Of AI

2023-07-14 05:33:03 ET

Summary

- Microsoft's growth in the next decade will be driven by the emergence of generative AI, with the company integrating AI-powered features into all its software and platforms.

- The company's focus on cost management and operating leverage, as well as a shift towards a higher proportion of commercial cloud offerings, are expected to drive operating margins.

- Key risks include weak Windows OEM sales growth, potential hurdles in the Activision Blizzard deal, and a slowdown of commercial cloud booking growth.

Microsoft (MSFT) has successfully transitioned its businesses to the digitalization and cloud realm. Looking ahead to the next decade, I believe Microsoft's growth will be bolstered by the emergence of generative AI. With its capability to integrate AI-powered features into all its software and platforms, Microsoft is well-positioned to capitalize on this trend. I think that the combination of commercial cloud and AI capabilities has the potential to drive Microsoft's double digits revenue and profit growth.

Growth Drivers

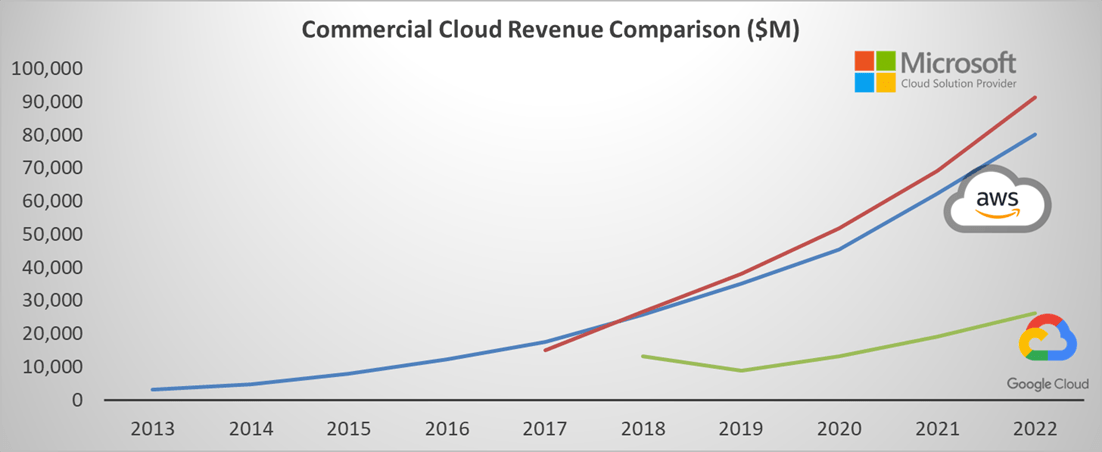

Winning in Commercial Cloud: In my article titled ‘ AWS Growth Is Underappreciated And Stock Is Undervalued ,' I discussed how Microsoft and Amazon ( AMZN ) are at the forefront of the commercial cloud competition, while Alphabet (GOOG) (GOOGL) is falling behind. Microsoft stands out by effectively leveraging their software and applications, prioritizing security, and cultivating a wide range of partner ecosystems.

{kind=link}

The ongoing workload migrations in enterprises indicate that a significant portion of workloads still remain on-premises at present. Consequently, I firmly believe that Microsoft's cloud business has immense potential for growth. Microsoft has already generated $91.4 billion in revenue from their cloud business, accounting for 46% of the group's sales. Furthermore, they continue to witness major enterprises worldwide migrating key workloads to Microsoft's cloud.

AI powered features across their platforms : Microsoft possesses the most powerful AI infrastructure, evidenced by their partnerships with OpenAI and Nvidia (NVDA). I believe that Microsoft is committed to integrating AI functionality into all their platforms and software solutions. A notable example is the addition of OpenAI services to Azure, enabling advanced models such as ChatGPT. In the coming years, I envision the possibility of all Office suites being powered by generative AI.

Furthermore, Microsoft is enhancing Dynamic 365 with AI functionality that spans across their CRM and ERP. These AI capabilities enable customers to streamline job functions and alleviate burdensome tasks such as manual data entry, content generation, and notetaking.

I think these AI add-ons will significantly contribute to Microsoft's top-line and bottom-line growth.

Operating leverage and Mix shift towards more cloud sales : In recent years, Microsoft's management has shown increased focus on cost management and operating leverage, which I consider to be a positive factor for Microsoft's bottom-line growth. Furthermore, Microsoft's shift towards a higher proportion of commercial cloud offerings has the potential to further drive their operating margins. The operating margins for both Productivity and Business Processes and Intelligent Cloud segments exceed 40%, whereas More Personal Computing lags behind with a margin of only 35%. Hence, as Microsoft continues to increase its cloud-related sales, it is likely to see a boost in operating margins.

Key Risks

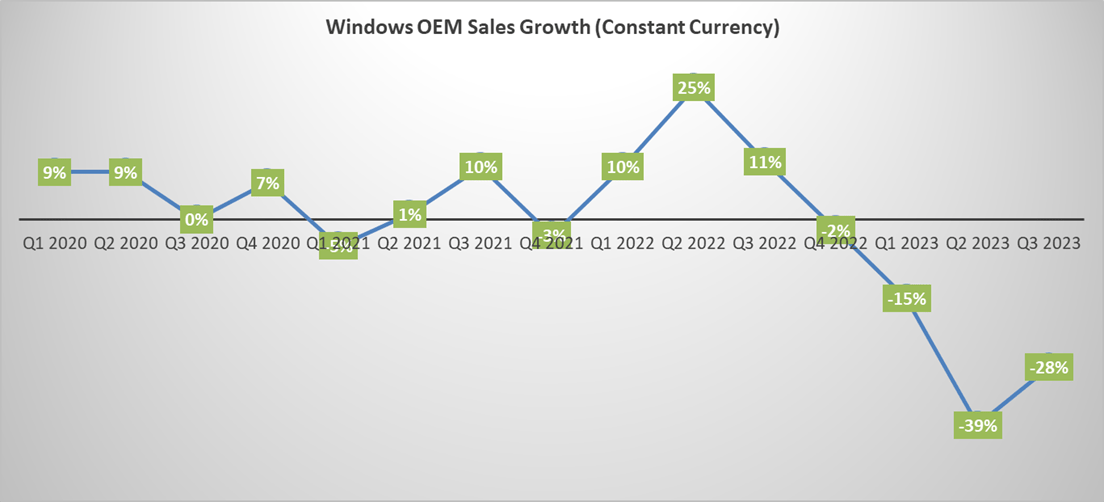

Weak Windows OEM Sales Growth: I believe that the PC market is currently encountering challenges, primarily due to high channel inventories, which pose significant obstacles to Microsoft's Windows OEM sales growth. In Q3 FY23, Windows OEM revenue witnessed a year-over-year decline of 28%, while Devices revenue decreased by 30% and 26% in constant currency.

{kind=link}

In my opinion, Windows sales are closely tied to PC sales and are unlikely to become a significant growth driver for Microsoft in the future. Over the past decade, as Microsoft embarked on its cloud transition journey, the proportion of Windows sales as a percentage of group sales has declined from 29% in 2010 to 12.5% today. This indicates that Microsoft is increasingly relying less on Windows sales, and the volatile risks associated with the PC market are manageable for the company.

Activision Blizzard deal : Microsoft cleared significant hurdles in its pursuit to acquire Activision Blizzard (ATVI) on July 11, 2023, as a U.S. judge approved the $69 billion deal, and a British regulator hinted at reconsidering its opposition. If the deal is eventually finalized, Microsoft will emerge as the world's third-largest gaming company. However, the U.S. Federal Trade Commission is appealing the judge's ruling in favor of Microsoft. While the outcome remains uncertain, it is evident that there are still numerous obstacles and uncertainties to overcome in order to close this substantial deal. If the acquisition does materialize, I believe that the combination of Microsoft's and Activision Blizzard's online gaming capabilities could generate immense value for Microsoft.

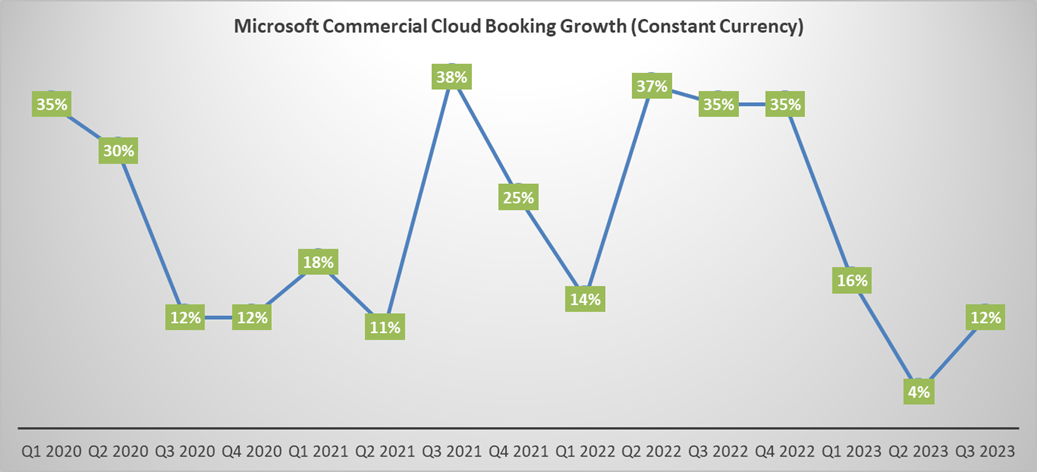

Slowdown of commercial cloud booking growth : It is unsurprising to witness enterprises actively seeking ways to optimize their cloud spending amidst challenging economic conditions. Microsoft's commercial cloud booking growth has shown a slowdown in recent quarters. Furthermore, Microsoft's commercial cloud business is facing high comparable from the previous year. In Q4 FY22, Microsoft's commercial cloud witnessed a growth of 35% due to significant volume from large, multi-year commitments. However, they anticipate a flat growth in commercial cloud sales in Q4 FY23.

{kind=link}

Outlook and Valuation

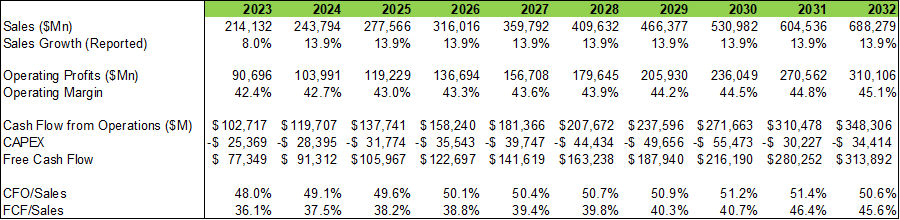

In my model, I assume a normalized sales growth rate of 10% for Microsoft's Productivity and Business Processes business, 15% for Intelligent Cloud, and 2% for More Personal Computing. Based on these assumptions, the estimated normalized growth rate is 13.9%. With the anticipated operating leverage, the operating margin is forecasted to reach 45.1% in FY32 according to my model. Additionally, my calculations indicate an estimated free cash flow margin of 45.6% in FY32.

{kind=link}

The model is using 10% of WACC and 4% of terminal growth rate. With all these assumptions in my model, the present values of FCFF over the next 10 years and terminal value are estimated to be $625 billion and $2 trillion, respectively. Adjusting the cash and dent, the fair value is $368 per share as per my estimates.

Microsoft DCF Model - Author's Calculation

End Notes

Among all the mega tech companies, my preference lies with Microsoft and Amazon as I believe both have achieved notable success in the cloud era. The integration of AI-powered features can enhance the relevance of Microsoft's commercial cloud and platforms, leading to improved productivity and cost savings for enterprises. In my opinion, Microsoft deserves a 'Strong Buy' rating.

For further details see:

Microsoft: Fire On All The Cylinders And Thrive In The Era Of AI