MSFT - Microsoft: Uncertainty Is The Name Current Valuation A Little Pricey

Summary

- Future growth in revenues is in question.

- Other issues include the slowdown of Azure revenues and the uncertainty of ChatGPT implementation.

- The company’s financials are very healthy, but the stock is a little pricey at current valuations.

- 10-year DCF model suggests a hold rating for long-term investors, 5-year suggests selling.

- Cash-secured puts could be a way of earning extra income while waiting for the price target.

Investment Thesis

I have decided to dig into the financials of Microsoft ( MSFT ) and speculate on its future potential growth. From numerous iterations of conservative, base/street, and optimistic scenarios, I have concluded that, at the current valuation, Microsoft receives a hold rating in my opinion, due to quite a few uncertainties that I will outline below.

As earnings are just around the corner, I wanted to see if Microsoft might be a good candidate for a long position right before they announce their next earnings, due on the 23 rd of January. I went through a lot of financial information that would help me decide how to go about modeling a DCF model. All the buzz right now is around Azure's growth deceleration and how it may impact the future revenue of the company. Another big news is that the company intends to invest $10B into ChatGPT which could be a game-changer for Bing and other Microsoft applications far into the future.

Both of these are hard to value currently as Microsoft does not report Azure numbers outside of percentage growth and pools the revenues into the Cloud Computing segment's total revenues and ChatGPT is still a long way from being implemented properly into their applications.

I will give my opinion, based on the numbers I got from forecasting, why I think Microsoft might be a little overvalued right now with a good margin of safety baked into the final valuation and why I think it is a hold until we get a clearer view of the future growth.

Slow Down in Azure Growth

One big factor for not being able to justify high percentage growth in revenue is Azure’s deceleration in growth. There is no doubt that Azure has been the darling of all revenues at the company. It has been growing high double digits for a while now and is the main factor in boosting Intelligent Cloud revenues year-on-year. However, what is happening with the Azure service right now is that it is starting to decelerate . In the latest 10-Q report , the growth of Azure was 35%. This is still very good, but compared to last year 's growth at 50%, it is a considerable slowdown. The next report due on the 23 rd of this month will show how much revenue can be attributed to Azure's growth and whether it has slowed down even further.

OpenAI and Microsoft Deal

It is hard to put a value on how much the company is going to benefit in the future from the implementation of OpenAI’s ChatGPT future iterations into the ecosystem. A possible $10B injection into the future of AI is a big deal for sure, however, focusing on tangible numbers right now, it is difficult to put any sort of growth numbers into future revenue forecasts.

We can see some movement in this area already, as Eric Boyd announced on the 16 th of January that the company is making Azure OpenAI Service open to the public. This is a good start to have as many companies as possible using the available AI sources to help their clients with any type of problem they may have and provide solutions.

Acquisition of Activision Blizzard on Hold

It is worth mentioning that the acquisition of one of the biggest gaming companies in the world has seen some opposition from major players like Sony and now most recently Nvidia ( NVDA ) and Alphabet ( GOOG ) (GOOGL). Activision Blizzard (ATVI) - which is projected to bring in around $7B in total revenue and also has 360 million monthly active users according to their latest 10-Q report - could be huge for Microsoft's revenues. These users could then be added to the Xbox Game Pass and increase revenues quite considerably for that segment. Just like with everything else I have mentioned earlier, doubts loom that they would be able to buy the company. We will see in a few months what the FTC and other opposition will do.

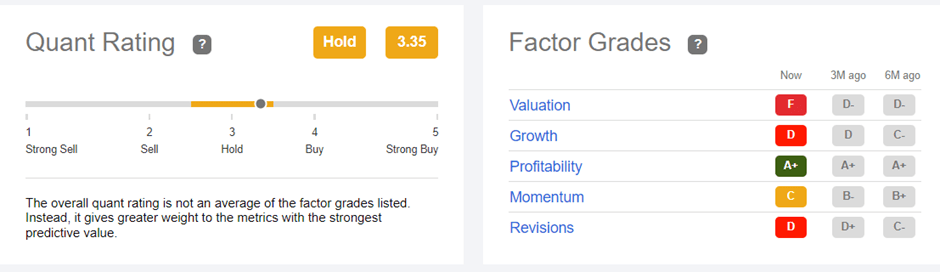

Ratings Support the Thesis

Looking at the quant ratings here on SA, we can see that most of the ratings, except for profitability, align with my opinion on Microsoft that it is not the right time to invest your money into the company. The ratings have gone down since 3 and 6 months ago also.

Quant Ratings MSFT (Seeking Alpha)

{kind=link}

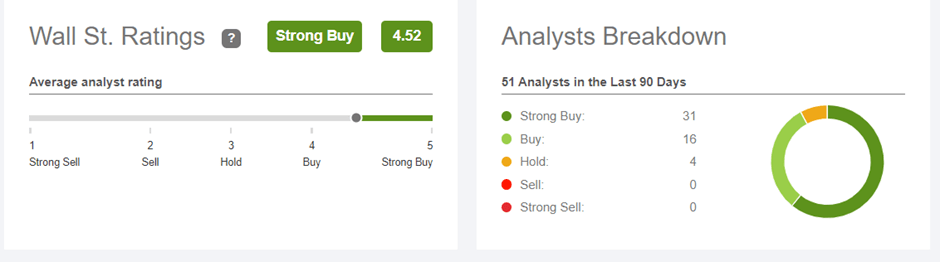

On the other hand, Microsoft is a darling of Wall Street, where most analysts suggest a Strong Buy rating for the company with an average price target of 294. This leads me to believe that the street is very optimistic about the company's growth rates and the deal with OpenAI. The numbers I see from my DCF valuation (below) and these types of diversions of opinion are what support my view on the Hold rating for now.

The Street's Sentiment on MSFT (Seeking Alpha)

{kind=link}

Financial Metrics

Now let's have a quick look at the company's balance sheet to see how it is doing. Overall, the company is a well-oiled machine. It has been for quite a while too. The growth numbers are outstanding. For a company this big to keep growing in double digits is remarkable.

Liquidity of MSFT (Own Calculations)

Cash and short-term investments have been very healthy for a while, with a slight dip most recently.

Cash Ratio graphically (Own Calculations)

Historically, the cash ratio has been much healthier than in most recent years, which could become a little bit more problematic if this trend continues. As of right now cash ratio is a little over 2 so it is considered healthy still. The cash and short-term investments can still cover total current liabilities without a problem.

The three returns that are important in a good business are ROIC, ROA, and ROE. These three are very healthy at the company also and are increasing.

Return on Invested Capital (Own Calculations) ROA & ROE (Own Calculations)

The financials of the company tell me that this is a good business in the long run. Very little debt on the books is a plus for me also, as I like to invest in companies that have very little leverage. Microsoft has a very healthy balance sheet, and for now, I do not see this changing anytime soon.

DCF Valuation

The figures above could alone justify investing in the company, however, when I modeled my DCF with a margin of safety of 25%, the share price is a little high right now. It is quite difficult to speculate on the growth numbers for the company, as I mentioned Microsoft is a mega-cap company already and we do not know how long the company can sustain such double-digit growth into the future.

For my assumptions, at least for 2023 and 2024, I chose 7% and 13% growth in revenues, because there were around 40 analysts that covered these predictions, and I would take it as a good estimate of growth. The number drops to 20 analysts in the next year and so that is when I started to rely on my realistic assumptions for the growth after 2024. On the last 10-Q report we saw good, but declining growth in revenues, I had to model a little more conservatively on the base case. Another reason for a more conservative approach is that, as I mentioned, Microsoft is a big company, and it is hard for large companies to keep growing at a rapid, high double-digit pace. After separating the revenues into its segments of Productivity and Business Processes, Intelligent Cloud, and More Personal Computing, my total revenue growth is 13% in 2025 and decrease by around 1% every year until 2032 which has a growth of 8%.

For the optimistic case, my total revenues from 2025 are 16% growth and decrease to 11% growth in 2032. For the conservative case, my assumptions are 11% and go down to 6% growth.

I gave a little bit more revenue growth in the Intelligent Cloud segment, which has been growing around 25% year over year, but I could not be this optimistic about it in the future as we already see Azure’s revenue growth decelerating.

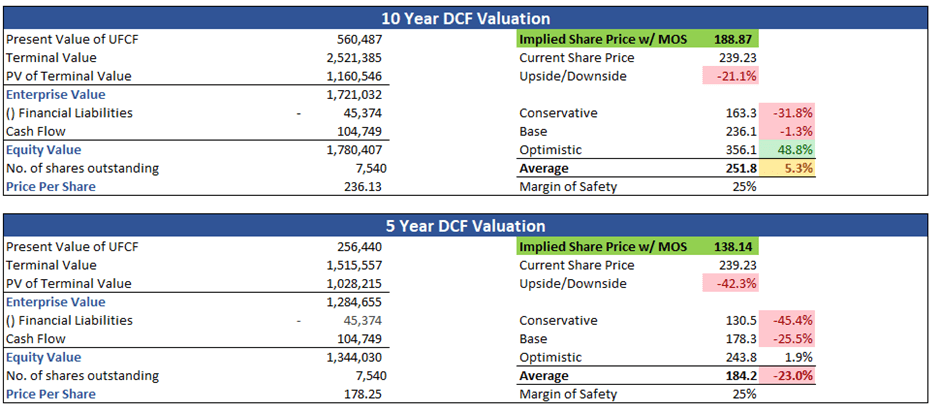

With my calculations for 5-year and 10-year DCF models, I concluded that the company at the current market valuation is a Hold on 10-year and borderline Sell on the 5-year model in my opinion, with 188.87 price target on the 10-year and 138.14 price target on the 5-year model.

10-year and 5-year DCF (Own Calculations)

{kind=link}

If you are a current investor in the company, I would say it is a better time to hold onto your shares now, than it was when the price hit all-time highs in October 2021. Plus, the dividend growth is around 10% per year, which is decent. For anyone who is still debating whether to invest or not, it is up to you, but in my opinion, there may well be a better time in the future. While you wait for that better price, set a price alert when it hits lower, and if you are knowledgeable in options, sell some cash-secured puts at a price you would be happy owning Microsoft. Collect premium, rinse, and repeat. If it does not reach your target price, the upside is you get to keep that premium. The downside is if it goes lower than your price target and you’re forced to buy at a higher price, but after collecting premiums all the way, you are going to buy at a slight discount to your target price.

Conclusion

As I mentioned above, the company is in a good shape overall, with great growth numbers, however, with a few uncertainties that I have outlined, the company is a bit overvalued for new investors, and long-term investors in the company can weather the uncertainties and average down if it does fall further. They can keep collecting those dividends as Microsoft is a safe long-term play regardless, just a little pricey right now. New potential investors can take advantage of options and sell cash-secured puts, collect premiums and wait for their ideal price to hit.

The earnings are just around the corner, which will shed some more light on Azure's growth prospects, AI implementations into their ecosystem, and guidance from the management. I may revisit the model after the earnings if there will be some major news announced.

Some of you might think that the MoS I chose is a bit high at 25%, but I would rather give myself a bigger margin of error than buy into a company that might be overvalued. If it never reaches my target price, then it is fine. I will be able to find some companies that match my estimates from time to time, for example, I just wrote an article on Meta Platforms (META) with the same MoS and the company is still an attractive investment.

For further details see:

Microsoft: Uncertainty Is The Name, Current Valuation A Little Pricey