ET - Midstream Energy For Income - Not Your Grandfather's MLP

2023-05-12 04:37:02 ET

Summary

- MLPs have been generating steadily increasing cash flows over the past several decades, even during recessions.

- While the energy sector has outperformed for most of the past 3 years, YTD performance has suffered offering midstream/MLP investors an opportunity to buy steady income at low prices.

- The current macro environment is challenging but many midstream operators are increasing distributions and further growing cash flows.

As an investor nearing retirement, I am constantly seeking a steady source of passive income that is sustainable even during rising inflation and with a potential recession on the horizon. Recently I wrote about one such investment - a CEF that invests in midstream energy assets, the NXG Cushing Midstream Energy fund (SRV). The SRV fund increased the monthly distribution starting in September 2022 from $0.15 per month to $0.45, now yielding over 15% annually. I received many comments and questions about SRV such as, how can a fund that basically holds MLPs (master limited partnerships) that generate 7 to 8% annual yields offer a 15%+ distribution? And is that distribution sustainable?

As part of my research into the SRV fund I contacted the CEO of NXG Investments, Mark Rhodes, who then put me in touch with the SRV fund manager, John Musgrave, Managing Partner of NXG Investment Management (formerly Cushing). I had a great conversation with John that not only discussed the strategy and inner workings behind the SRV fund, but he also shared with me some salient information regarding the midstream energy space, and how it has changed over the past several years. After our call, he offered to send me several presentations that explain some of those concepts in detail.

One of the presentations that he sent is a detailed overview and update of the Midstream Energy market. I am going to paraphrase some of the concepts that his presentation covered in my review of the macro picture of the midstream energy sector in the section below, and then review a couple of investment options to consider if you are interested in this asset class.

{kind=link}

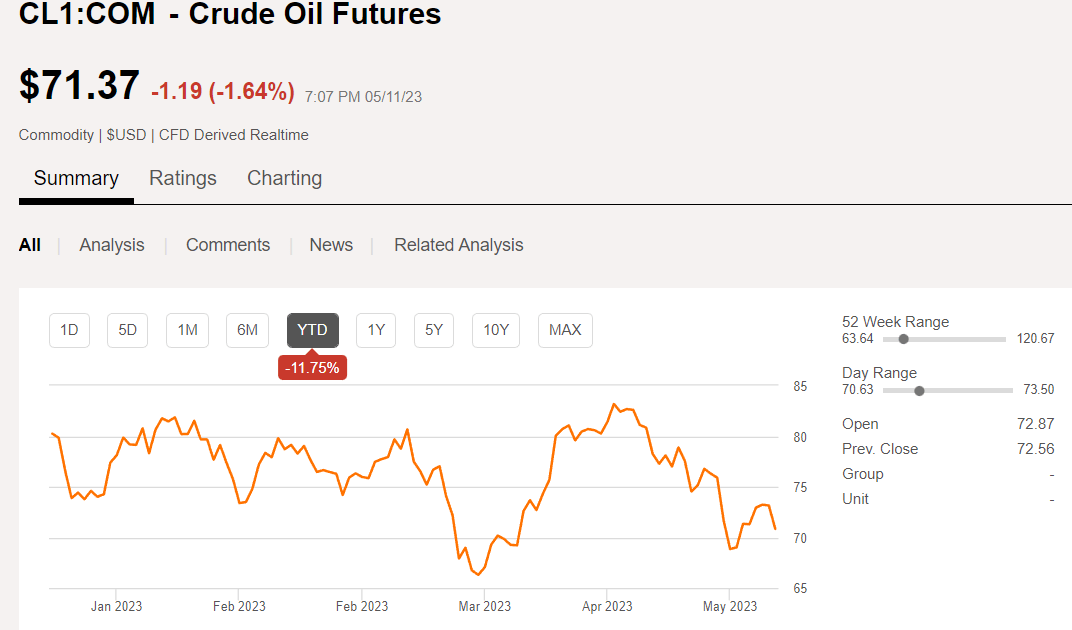

The price of crude oil has dropped more than -11% YTD, which exacerbates the situation with Midstream/MLPs.

Midstream Energy - Macro Picture

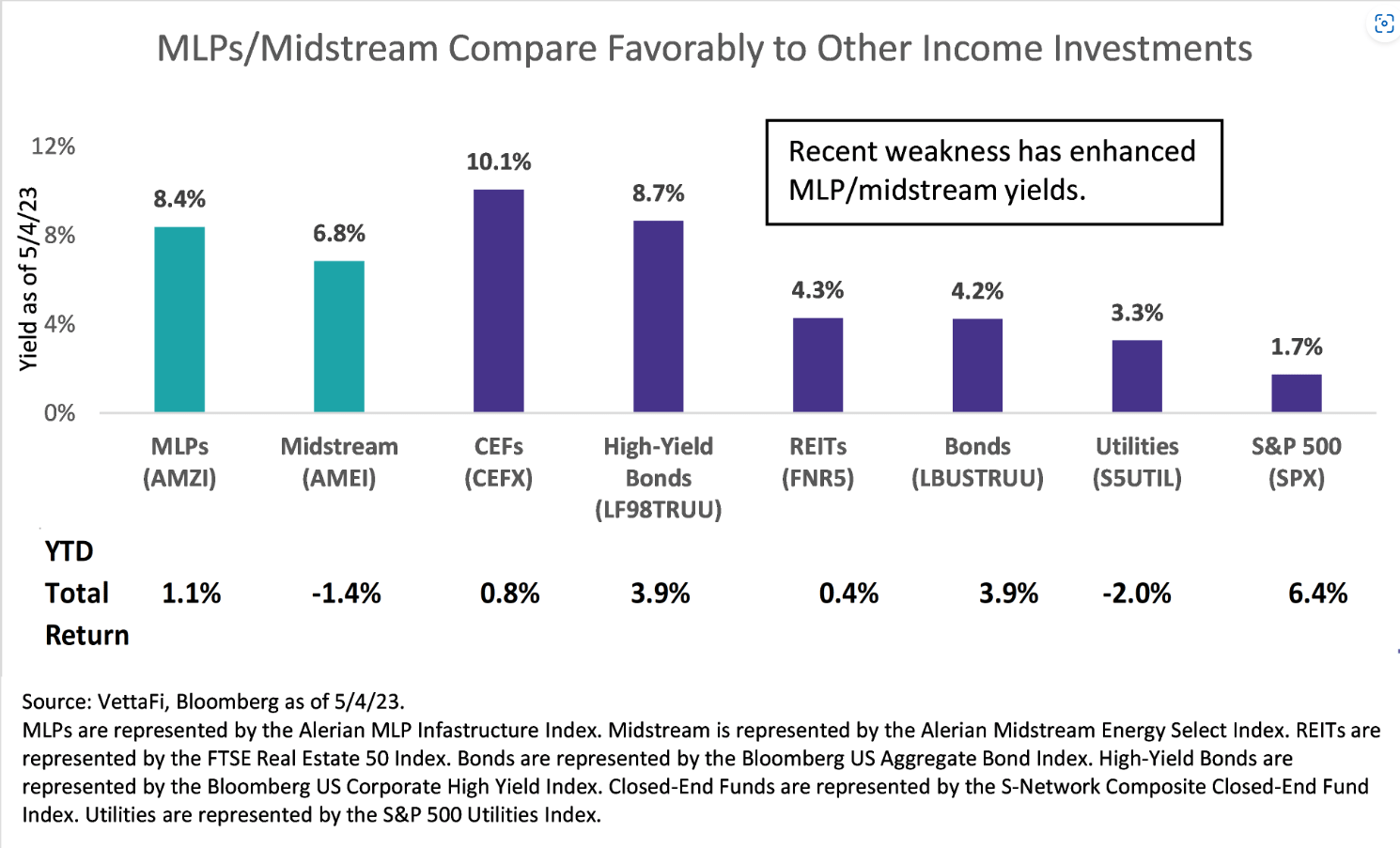

In a recent SA article on the MLP/Midstream sector, a solid Q1 in 2023 for most midstream companies reporting earnings was overshadowed by the macroeconomic environment with declining oil and gas prices pushing down prices for many MLP and midstream stocks. Yet despite the macro pressures, Midstream remains a solid choice for income-oriented investors. From the article, the chart below shows a comparison between different high yield income investment choices and MLPs/Midstream fall behind only CEFs and HY Bonds based on YTD total returns as of the time of publishing, May 10.

Even though most MLPs and midstream companies have long-term contracts, the current oil prices affect investor sentiment which leads to pricing pressure on the stock as most investors believe that earnings and cash flow will be negatively impacted by dropping oil prices. After all, look at what happened in 2020 when the Covid-19 pandemic hit.

{kind=link}

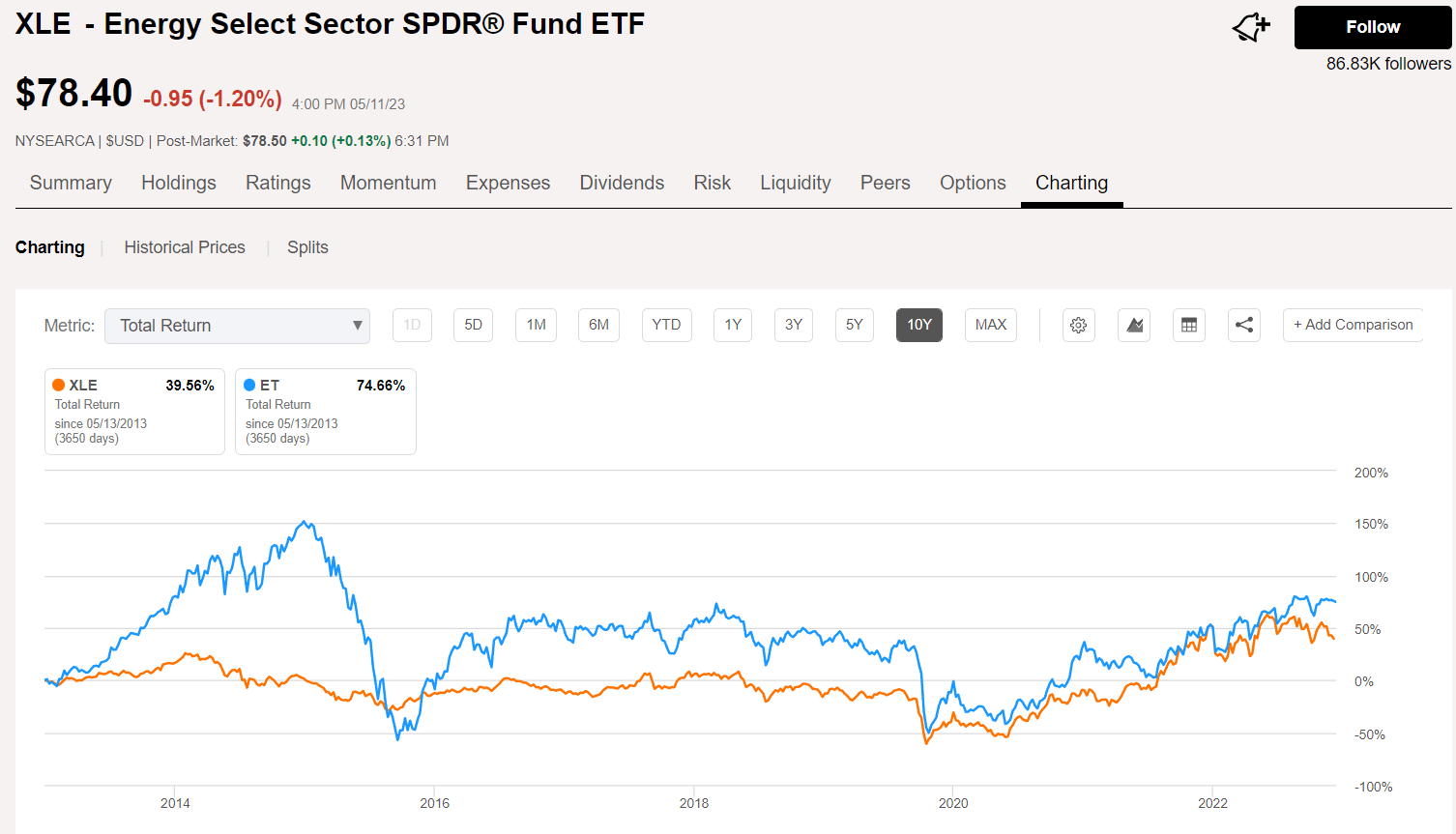

Over the past two-plus decades the energy sector has experienced long-term periods of outperformance, followed by several years of underperformance. Looking at the past 10 years using the SA charting tool, the ups and downs in the energy sector are illustrated by the chart of Energy Select Sector SPDR® Fund ETF (XLE).

{kind=link}

To visualize how midstream/MLPs have performed over that same period, I used Energy Transfer ( ET ) as a proxy as it somewhat exaggerates the extreme swings in total returns during that period. ET is also a top holding in the SRV fund. There was a substantial decline in total returns in midstream/MLPs from 2015 to 2016 due to a combination of factors including a huge drop in the price of oil and natural gas starting in 2014 that resulted in a sea change to the midstream markets. Some MLPs experienced massive corrections with a decline of more than 60% in unit prices during that time.

From 2016 to 2019 the midstream market began a slow recovery until the Covid-19 pandemic hit in 2020 and caused the bottom to drop out again due to a nearly complete global drop in demand for oil and gas. Due to the extreme and sudden drop in oil and gas prices along with the oversupply from the shale revolution and expanded OPEC production that had been taking place since about 2017, the MLP and midstream sector got hit again. However, this time, some investors began to realize that even though the price of oil and gas declined, and volumes dropped dramatically, the cash flows were still coming in steadily for many midstream companies. In fact, at least one savvy analyst on SA in March 2020 recognized and wrote about the unique buying opportunity at the time due to changes in MLP valuations since 2016.

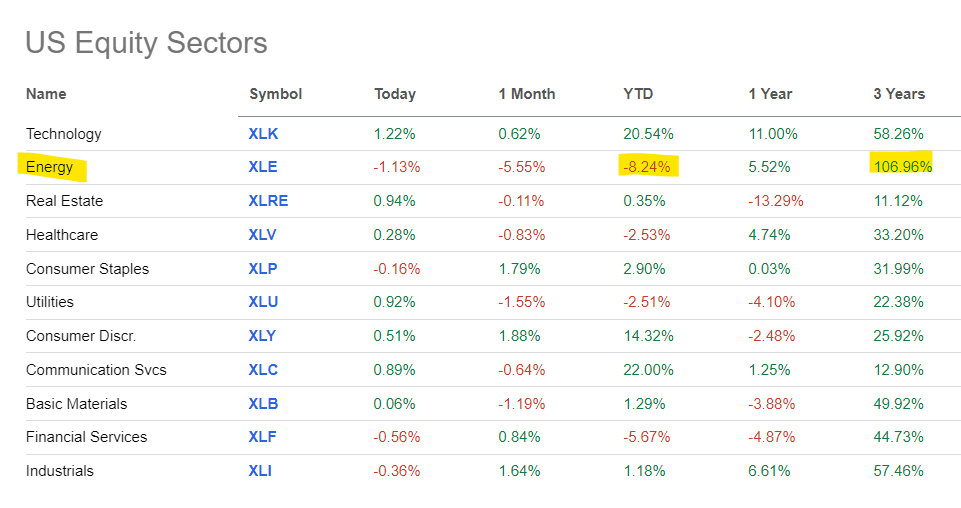

The overall energy sector has been in a new period of relative outperformance since the lows of 2020 and that is likely to persist over the next several years due to some changes that have occurred in the past 3 years. Over the last 3 years the energy sector (represented by XLE) has been the top performing sector, up over 106%. However, 2023 YTD Energy has been the worst performing sector, down -8%, as investors have lost their appetite for energy as the price of oil and natural gas began to decline again starting mid-2022.

{kind=link}

Some of the recent distrust of the midstream energy sector is based on the maligned history of overspending on CapEx without the pricing support and shareholder returns that many investors expected in the last decade. After the pandemic ended, many MLPs and midstream companies were reluctant to issue more debt to increase CapEx, especially with interest rates beginning to rise from all-time lows. With decreased valuations, companies were reluctant to risk capital as there was little incentive to take on the additional risk with regulatory and punitive policy measures in place that suppressed additional investment in new production.

At the same time, the resilient and growing demand for energy is starting to put pressure on supply, especially as the reopening of China continues and Russian supplies are constrained. Moderating constraints on shale oil production is limiting supply growth in the US and there are increased calls for limiting OPEC production to help stabilize oil prices. At the same time there is growing demand for natural gas to support the energy transition while other sources of renewable energy begin to replace some of the demand for fossil fuels.

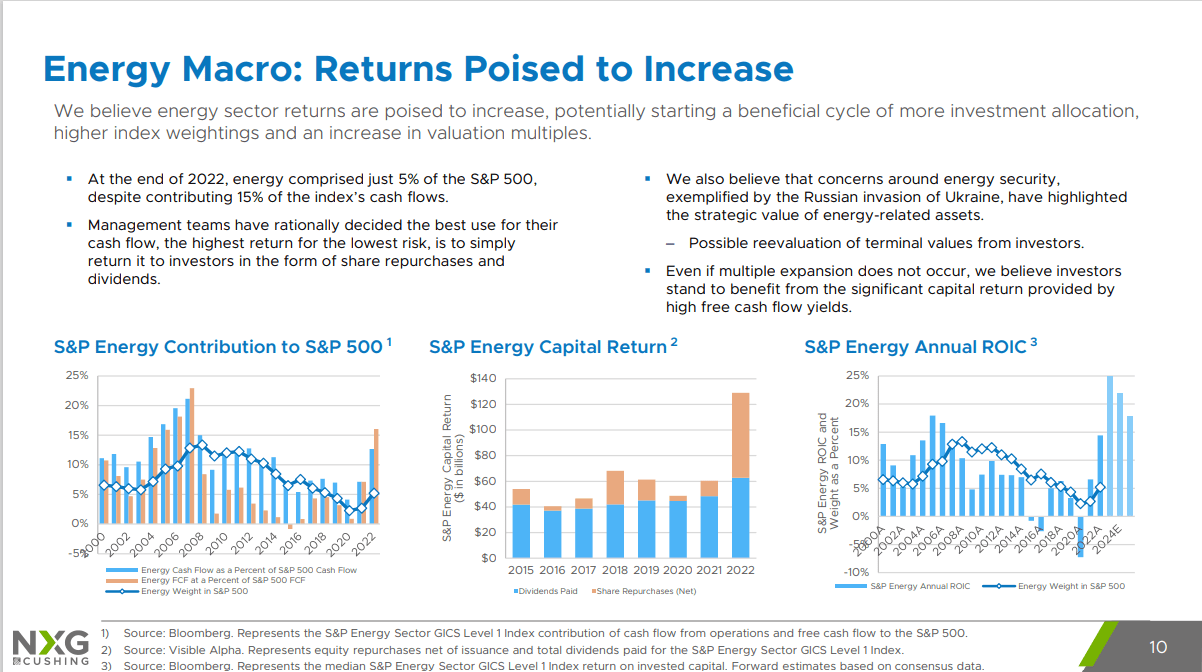

Despite those concerns, the overall picture of potential energy sector returns is expected to see an increase over the next several years. Many midstream energy managers have determined that a better use of cashflow is to increase shareholder returns by buying back shares and increasing the distribution. As company valuations increase, more capital becomes available to reinvest in the facilities and equipment that keep the cash flow growing. In a slide from NXG Investment Management, that I am using with their permission, this concept of increasing potential in energy sector returns is illustrated succinctly.

{kind=link}

ET is Growing the Distribution

The current largest holding by percentage in the SRV fund is Energy Transfer, LP, an energy holding company that provides transportation, storage, and terminalling for NGL, crude oil, natural gas, and refined products across 41 states and an international office in Beijing. They have one of North America's largest portfolios of energy assets. ET was formed in 1996 and has its headquarters in Dallas, TX. Midstream assets are estimated to account for about 45% of 2023 capital expenditures.

One way that ET is growing is by acquisition, with the recent purchase of Lotus Midstream using $900M in cash and $44.5M in newly issued common units (ET is an MLP that issues a K-1 so units are issued, not shares). That deal will give ET about 1.5M bbl/day of additional capacity in the Permian Basin as well as another 2M in crude storage capacity at the Lotus Midstream Midland terminal.

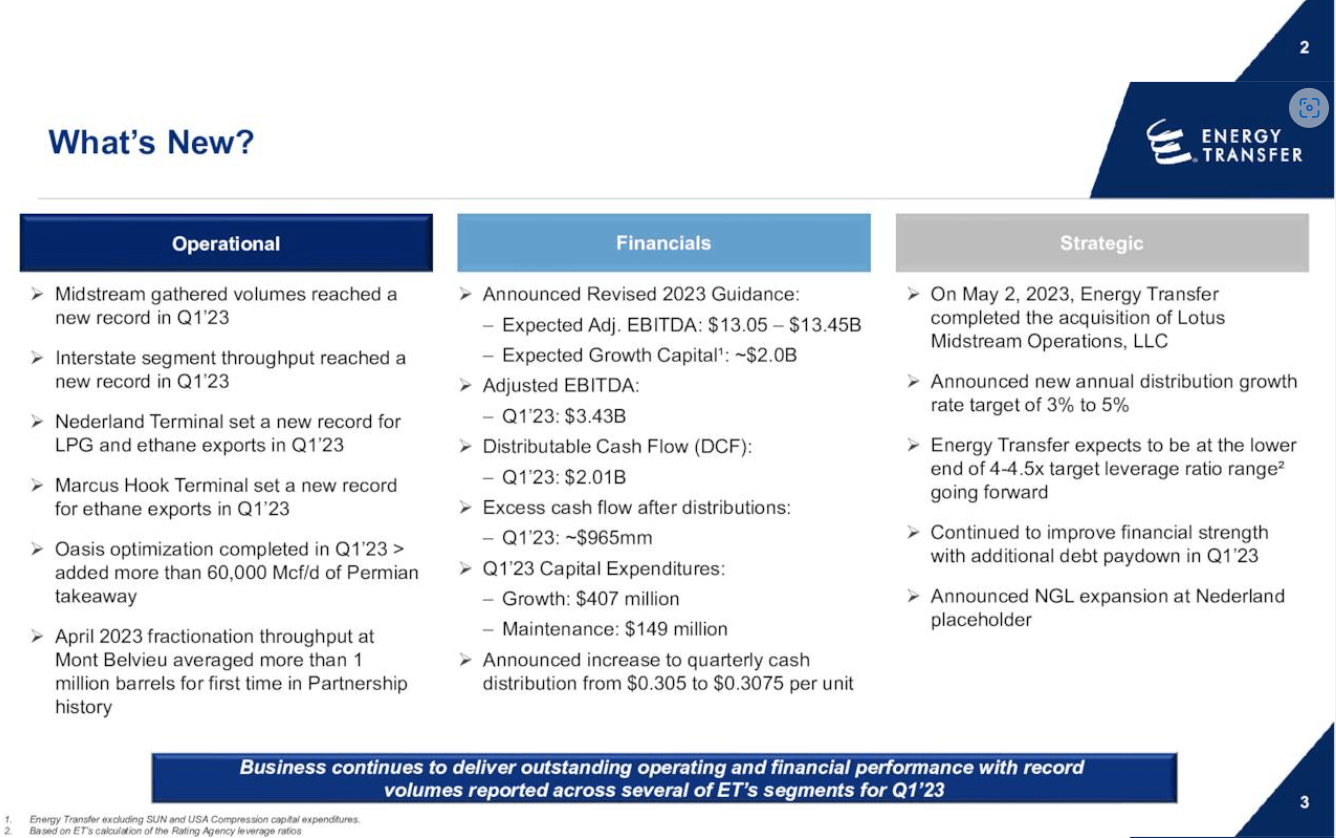

Based on the Q1 earnings report that was released on May 2, ET raised guidance for 2023 due to increasing energy demand.

Given the acquisition as well as increasing energy demand, Energy Transfer raised its adjusted EBITDA guidance for FY 2023 to $13.05B-$13.45B from $12.9B-$13.3B previously; the partnership also expects full-year growth capital spending of ~$2B.

According to the Q1 investor presentation, Q123 midstream gathered volumes reached a new record. They generated distributable cash flow of $2.01B in the quarter and raised the quarterly distribution from $0.305 to $.3075 per unit. They also continued to pay down debt during the quarter.

{kind=link}

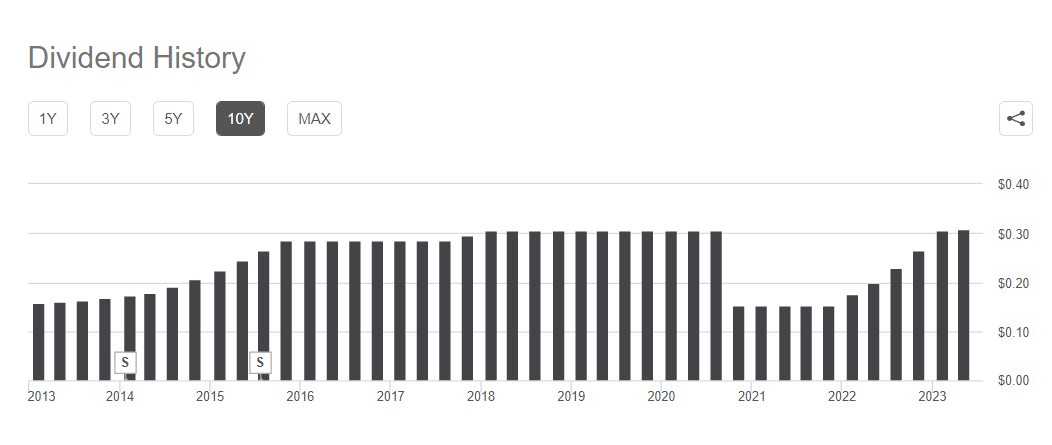

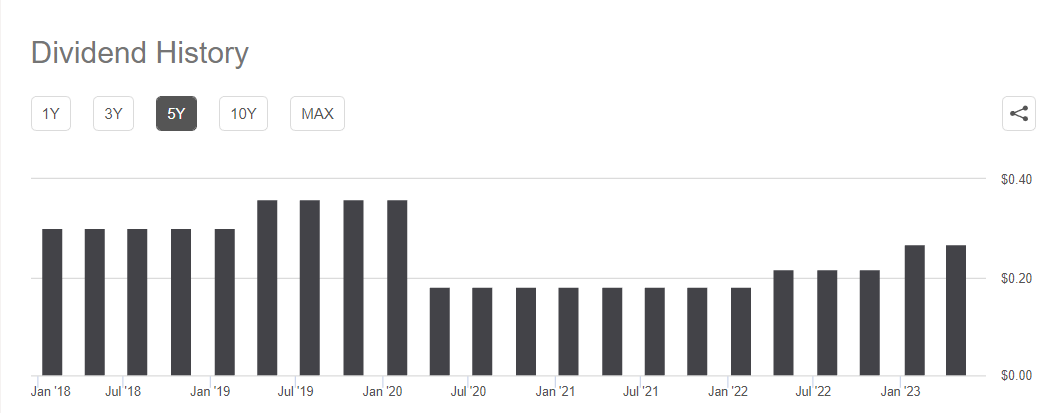

ET has paid quarterly distributions for 16 consecutive years and up until 2020 had not cut the distribution in the past 10 years (not even in 2016). Now with the most recent increase, the monthly distribution will be above pre-pandemic levels and the highest it has been in at least 10 years. With excess cash flows after distribution of $965M in Q1 it is likely that the distribution will continue to grow in future quarters.

{kind=link}

Targa Resources Grows Cash Flow

The second largest holding in the SRV portfolio as of 3/31/23 according to SA, Targa Resources Corp (TRGP) is another midstream company that is experiencing phenomenal growth in cash flows, and in nearly all levels of financial performance according to this latest article from Power Hedge. On May 4, Targa reported Q123 results that included adjusted EBITDA of $940.6M compared to $625.8M in Q122.

The company reported distributable cash flow of $729.4M and adjusted free cash flow of $314 million. Targa gets an A- grade from the Quant rating system for Cash Flow from Operations with $2.8B - about 4x the median compared to their peers and well above their 5yr average of $1.7B.

{kind=link}

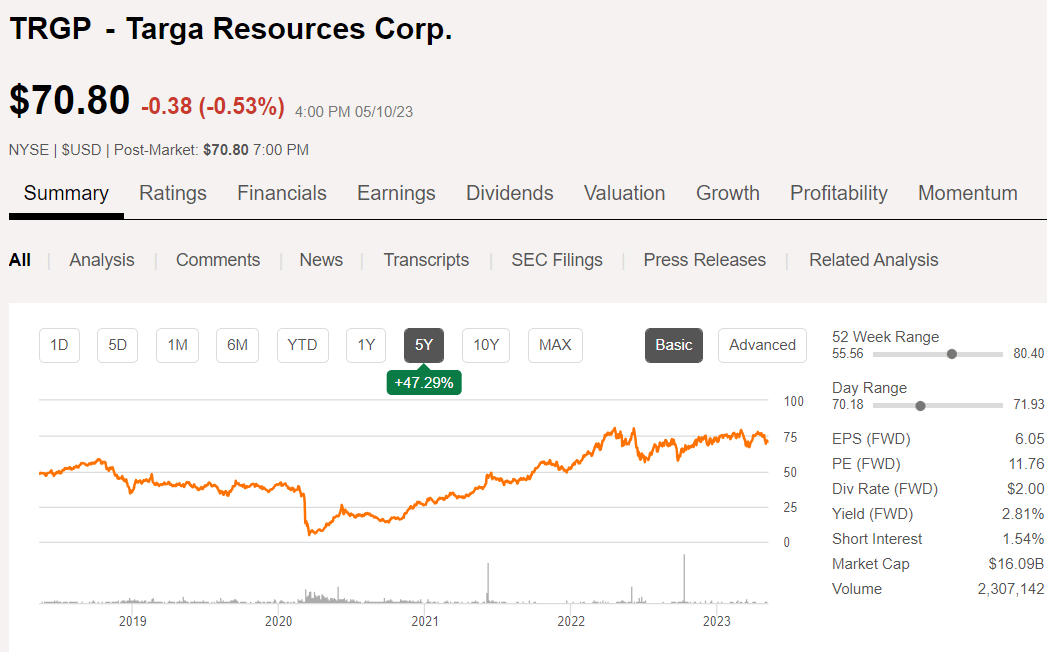

The distribution was increased by 43% to $0.50 per common share (was $.035 per share previously). Note that TRGP is a C corporation and not an MLP, so they issue shares. Targa has also seen its share price increase by more than 47% in the past 5 years yet still trades at an inexpensive forward P/E of less than 12x earnings. The company also repurchased $52 million in shares during the quarter.

{kind=link}

During the Q1 conference call , CEO Matt Meloy had this to say about the future growth outlook:

We remain excited about the long-term outlook at Targa. Looking ahead, we continue to execute on our strategic priorities will drive increasing EBITDA, a higher common dividend and reduced common share count while maintaining leverage within our target range. We announced this morning that our Board has approved a new $1 billion common share repurchase program, which provides us with flexibility going forward to continue to be opportunistic on repurchases.

Plains GP Holdings, LP ( PAGP )

Plains All American Pipeline ( PAA ) is another midstream MLP (that does issue a K-1 at tax time). PAA owns an extensive network of pipeline transportation, terminalling, storage, and gathering assets in key crude oil and NGL producing basins and transportation corridors in the US and Canada.

Plains GP Holdings, LP was founded in 2013 with headquarters in Houston, TX and owns a non-economic controlling general partner interest and an indirect limited partnership interest in PAA. PAGP is the 3rd largest holding in the SRV fund and currently pays a forward distribution yield of about 8%. PAGP issues a 1099 at tax time rather than a K-1.

In order to evaluate PAGP it is also necessary to review PAA because the 2 companies are intertwined. On May 4, Q1 results were reported for PAA/PAGP and guidance for 2023 was updated and reaffirmed. Although the revenue reported missed analyst estimates and declined by -10% YOY, the company reported net income of $422 million and net cash provided by operating activities of $743 million. Adjusted EBITDA of $715 million attributable to PAA was also reported. Free cash flow of $823 million was reported, including approximately $284 million of asset sales. Total debt was reduced by about $450 million.

First quarter crude oil adjusted EBITDA increased by 14% relative to Q122 (primarily due to higher volumes) and first quarter NGL adjusted EBITDA increased by 19% comparable to 2022 results. Guidance was reaffirmed as follows:

- Reaffirming full-year 2023 Adjusted EBITDA guidance attributable to PAA of $2.45 - $2.55 billion, year-end 2023 leverage of +/- 3.5x and common unit distribution coverage of +/- 215%

- Expect to generate approximately $1.6 billion of Free Cash Flow in 2023, underpinning our previously announced capital allocation framework that includes meaningfully increasing returns of capital to equity holders and further absolute debt reduction

- Remain focused on disciplined capital investments, anticipate full-year 2023 Investment and Maintenance Capital of $325 million and $195 million, respectively, net to PAA

The distribution for PAGP was also maintained in line with the previous quarter with PAGP Class A shares paying $0.2657 on May 15 to shareholders of record as of May 1. Looking at the distribution history of PAGP, it is also apparent that the dividend was slashed in 2020 due to Covid and has slowly increased again to near its pre-pandemic level as cash flows continue to grow.

{kind=link}

Current Cash Flows from Operations are about 10% above the 5-yr average and more than 3 times higher than the median for the sector.

{kind=link}

In discussing the Q1 results and 2023 guidance, CEO William Chiang had this to say about PAA/PAGP:

"Plains remains focused on execution, and our company is off to a strong start to the year despite macro uncertainty. We remain confident in our ability to deliver on our 2023 plan with our contracting profile and significant hedging within our Crude Oil and NGL segments serving to mitigate risk. Our Free Cash Flow generation enables Plains to execute on our previously announced capital allocation framework focused on increasing returns to our equity holders while further enhancing our financial flexibility. Over the long-term, we remain well positioned as North America will continue playing a critical role in global energy supply."

Summary and Recommendations

Based on my research and what I am seeing with respect to the macro picture for the energy sector, there appears to be a growing opportunity for midstream energy investors to capitalize on the steady and increasing cash flows from many of the midstream energy markets and companies that provide services including ET, TRGA, PAGP, and others. The SRV fund has recognized this trend and has determined that the best way to narrow the discount in their fund, which is structured as an RIC (registered investment company) and not as a C-Corp blocker like most other MLP funds are structured, is to increase the distribution rather than to buy back shares. The distribution coverage is excellent, but the underlying holdings only deliver about 7 to 8% of the yield, so the other half (roughly) of the distribution is provided as ROC.

It is often misconstrued that ROC is "bad" and is just a way for fund managers to return an investor's capital, and that is partly true in the case of SRV. With the SRV fund the ROC is acting like a share buyback because the NAV is at a premium to the market price so the capital being returned is generating another 5 to 10% premium (based on the current discount) from what investors initially contributed. It also helps to narrow the discount, which is what a share repurchase program would do, but it's a better use of cash based on what the fund manager told me.

For more information on the good and bad effects of ROC, take a look at this article from Steven Bavaria who explains why ROC is not always bad, and in fact is a useful way for managers of RIC funds to return value to shareholders that is not based purely on "taxable income". These paragraphs summarize the approach that SRV is taking with respect to the use of ROC in "juicing" the distribution:

For most equity funds, (including both closed-end funds and traditional open-end mutual funds), capital appreciation is a big deal because it is their major source of income, and therefore the primary source of their distribution flow. Typically an equity fund only collects dividends of 2 or 3% (at most for a growth fund; maybe more for a utility fund) on its portfolio of stocks, and depends on annual growth of another 5, 6, 7% or more to achieve its total equity return goal of 10% or so.

So most of the fund's total return will be capital appreciation. But to the extent the fund doesn't sell its "winners" but continues to hold them from one period to the next, a lot of its market appreciation, and therefore its "total return," won't actually be part of its "taxable income" for that year, because the gain hasn't been realized yet.

So a successful equity fund whose managers have done a good job selecting stocks that have risen and continues to hold them in portfolio hoping they'll rise even further, will show total return (including its as yet unrealized and therefore un-taxable income) that is greater than the taxable income it is required to pay to shareholders.

So, in essence as the prices of those underlying holdings in the SRV fund increase the total return in the form of unrealized capital gains increases, allowing the fund managers to return some capital to shareholders without too much of a negative impact on the NAV of the fund. That is only possible because of the long-term growth prospects for the energy sector and the increase in market value of the underlying holdings over the past several years.

Tax and Accounting Considerations in Midstream/MLPs

I am by no means an expert on taxes or accounting issues, but I do know that anyone holding the SRV fund in a taxable account can also benefit from the high amount of ROC, which as I understand, can help to reduce the cost basis of your investment. Also, because the SRV fund is structured as an RIC there is no more than a 25% investment allowed in MLPs that issue K-1s. That is why some companies such as PAGP are structured as a C-corp. This enables funds like SRV to hold a larger position than they would be able to hold in PAA, for example.

Also, most MLPs that do issue K-1 forms at tax time are better held in a taxable account as opposed to a retirement account such as an IRA or 401k. This is because MLPs throw off UBTI. The reason why that can become a problem is explained in more detail here , and this is not a one size fits all situation so you may wish to discuss with a tax adviser if you need more information about your personal situation.

In addition, there are other tax considerations for holding MLPs in taxable accounts, including the way that distributions are handled and how they can reduce the tax burden for investors. Essentially, the ROC from distributions acts like depreciation, which reduces your cost basis. More information on the tax benefits to holding MLPs can be found here .

As a unitholder of an MLP, you're providing capital to the venture and being rewarded with cash distributions from ongoing operations. This makes MLPs a good option to consider for retirees or anyone else looking for a consistent income stream. Since distributions are a return on capital, they are mostly tax-deferred. But when you sell, you will pay taxes based on the difference between the sales price and your adjusted basis .

I have reviewed several different midstream and MLP investments in this long-winded article. I hope it provides some food for thought and helps you to make wise decisions regarding your future passive income stream. Shoot me a comment below if you have anything helpful to add or if you would like additional info on any of these selections.

For further details see:

Midstream Energy For Income - Not Your Grandfather's MLP