CA - Midwest Energy Emissions: Tax Credit Settlement Provides The Cash For The Next Leg Of Growth

2023-11-21 15:53:24 ET

Summary

- MEEC is near the end of their multi-year lawsuit with the refined coal industry – about half the group from a volume perspective has already settled, only CERT remains.

- The first two settlements' value is being kept private; however, we now know the company is targeting $1/ton of refined coal used by each infringer.

- The significant win against Refined Coal should double or triple in the base mercury removal business over the next 12-24 months.

- SE Asia and Forever Chemicals are large opportunities for the company starting in 2024 and 2025 respectively.

- Rare Earth Element production should add meaningful revenues beginning in 2026.

Given news of the recent refined coal settlement that encompasses about half the defendants in MEEC’s (MEEC) ongoing refined coal lawsuit, we are putting together a quick update to our previous article from June 2021, which can be found here . For those who are interested in the background of the company and the lawsuit we recommend starting with our first article.

In this article, we update a few pieces from our original article, including the methane gas opportunity, the Refined Coal lawsuit as well as add a short discussion on the new forever chemicals and SE Asia opportunities, as well as update the valuation.

Refined Coal lawsuit

MEEC filed the refined coal lawsuit back in 2019, and since then the defendants have tried every trick in the book to get the case thrown out. The trial was scheduled to start last Monday, November 13 th . Based on the court updates leading to the trial, it was clear that MEEC was in a position of strength. However, at the twelfth hour, perhaps unsurprisingly, settlements started coming in fast. In total, about half of the volume associated with the Refined Coal lawsuit settled outside of trial. Generally speaking, it was the companies that actually operate coal power plants as a business who were the first to settle. The remaining defendants (The CERT defendants) are primarily financial companies that don’t have a real power generation business, and instead were set up to monetize the tax credit opportunity.

A few points to note, first, it is our understanding that the majority of the legal heft on the defense team, as well as many expert witnesses left the case when the first three groups settled. Leaving the CERT defendants scrambling to rebuild the case as we move toward the trial. The court filing stated the proceeding must be complete by Feb 2024, however, to our knowledge, no new trial date has been set yet.

Second, there is now meaningful precedent, via settlements and dismissal of the case with prejudice against the non-CERT defendants. This means it is now an uphill battle for the CERT defendants to prevail. Additionally, we find it hard to believe that a Jury would side with large financial companies who were running a tax credit program over a small environmental company trying to improve air quality for all. To us, going to a trial seems like a bad idea for the CERT defendants, and as a result we expect them to ultimately settle out of court.

The problem for CERT is, as @DanBan__ on a recent twitter thread highlighted. The group that settled first were the companies who actually have a power generation business. For them this is a smart move, as they will be required to take a license no matter what going forward. As such, they would have something to offer MEEC in negotiations to help lower the damages. Specifically, go forward licenses and supply agreements. This is not the case with the CERT defendants. Thus, MEEC is likely to play harder-ball with the remaining CERT defendants.

It is important to note however, that even though the tax credit program is over, the majority of the underlying utilities that owned the powerplants are still operating and using MEEC’s patented process. CERT are the entities that ran the tax credit program. However, the utilities that run the powerplants will also now need to take a license going forward. This will be a significant source of the expected 2-3x revenue in the base business over the next 18 months.

On November 20th, MEEC issued a press release stating that “As part of the settlements announced last week, one of the defendants has entered into a license agreement based on a rate of $1.00 per ton of accused coal sold during the applicable damages period which we believe establishes a proper base line in our efforts against infringers." Specifically, we believe this is the settlement with Alistar – who is one of the CERT defendants. We believe this can be used as a strong proxy for remaining CERT settlements.

We want to highlight that we italicized the line about entering into a LICENSING agreement at $1/ton. This is important because the refined coal case is about the damages caused associated with the tax credit program only. This line implies the first of, perhaps many, new licenses with this group of infringing utilities for go forward use.

Now that we know what damages that are being sought by MEEC, we can begin to get a rough understanding of the potential lawsuit proceeds by looking at how much Refined Coal was burnt during the life of the program.

Settlement: A range of potential outcomes

As mentioned above, we know that MEEC is targeting a $1/ton from the CERT defendants. We believe the defendants who have already settled, are likely to have settled for less than $1/ton because of a) they were the first to settle and b) they can offer go forward supply agreements to MEEC.

There are two methods one could use to figure out what these settlements mean in terms of dollars to MEEC. One could go figure out how much refined coal each of the defendants powerplants burned each year and multiply it by $1/ton. Or, anyone who was using refined coal was infringing on MEEC’s patents, so we could just look at the total industries use of refined coal and multiply that by $1 and adjust for early settlements and uncollectable amounts. Our analysis uses the later approach, and is focused on the total settlement opportunity not just the CERT players.

For the purpose of this analysis, we will assume that the operating refined coal players settled for roughly $0.50/ton plus go forward supply agreements. Whereas, we expect that MEEC will target closer to $1/ton from the CERT defendants.

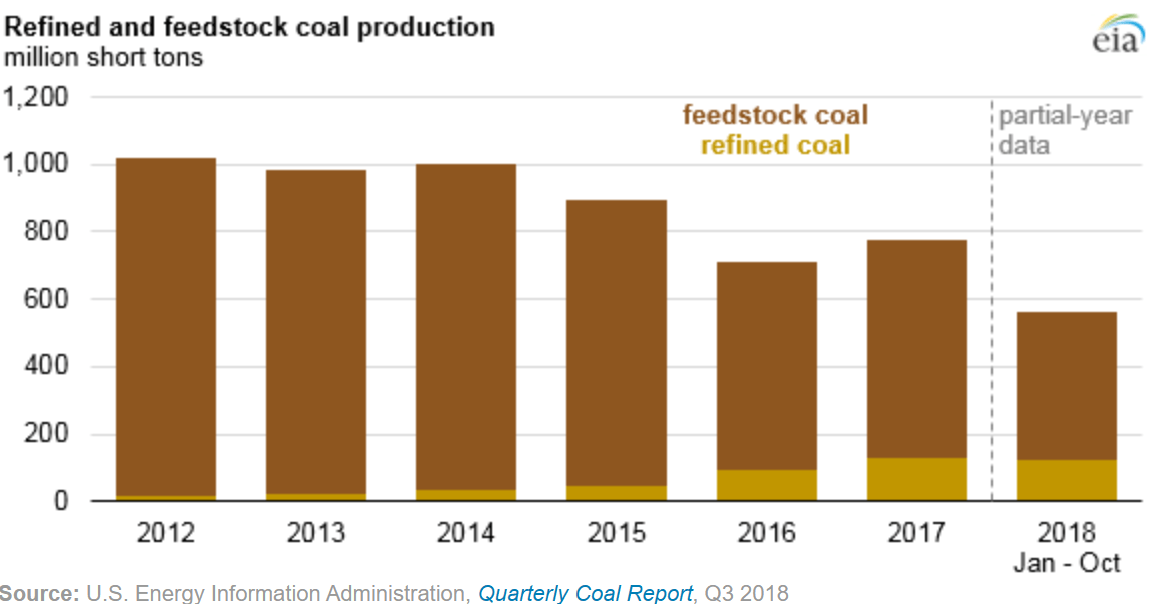

So, the billion-dollar question is, how much coal was burned during the tax credit years? Well after significant digging on the IEA website – we found two articles that show the amount of refined coal that was burned during the period of the tax credit program. The first image below shows the early years of the program, through mid-2018.

{kind=link}

Source: U.S. Energy Information Administration - EIA - Independent Statistics and Analysis

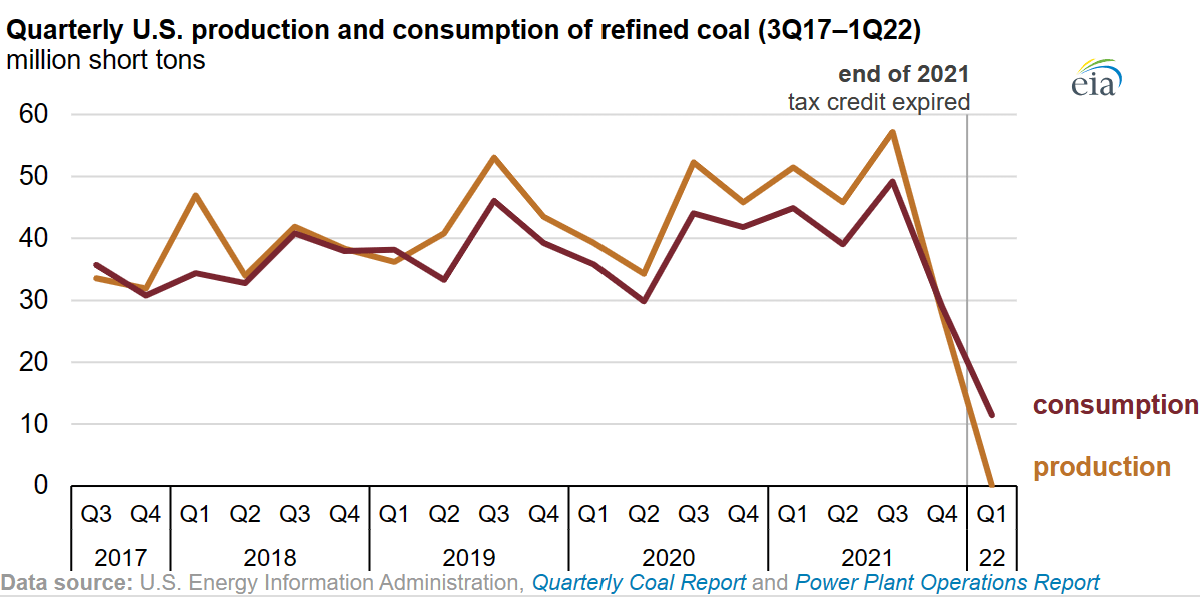

The next image below, is from a later article on the EIA website, but this shows the volume of production and consumption starting late in 2017 through the end of the program. By combining the data in these two charts, we can create a reasonably good estimate of the amount of refined coal the Tax Credit industry used. This is the basis of our settlement estimates.

{kind=link}

Source: U.S. Energy Information Administration - EIA - Independent Statistics and Analysis

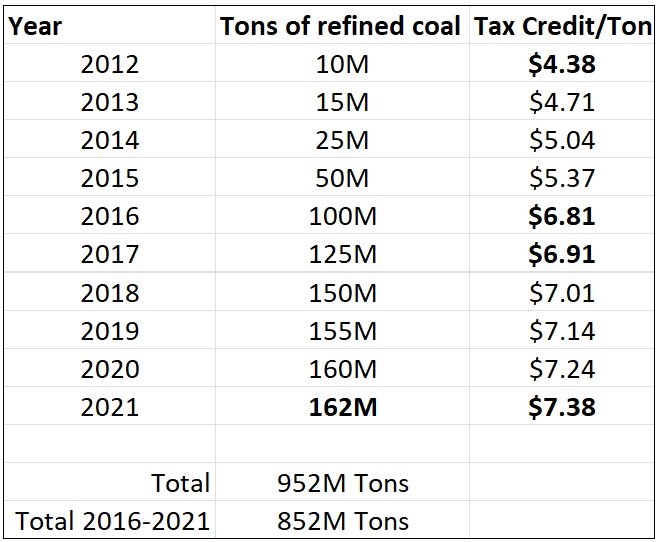

Taking the data from these two sources above we have compiled and estimated the annual Refined Coal production. As shown in the table below. If you read the articles, some of these numbers are provided, for specific years, which are the bold numbers in the table below.

{kind=link}

Source: EIA data from the links above and Author’s estimates

We think looking at the entire production of the market is a reasonable high-level way to understand the potential value of a settlement. For our damages estimate we go back 6 years, and assume that the first half of the volume will be settled at roughly $0.50/ton, then the second half should settle for around the $1/ton that Alistair licensed for.

Assuming 425M tons settled at near $0.50/ton implies that the first 3 settlements should be worth somewhere around $200M To MEEC. For the remaining CERT defendants, we anticipate a settlement closer to the $1/ton that Alistair licensed for, implying upwards of $400M in potential additional settlements. Combined this means we could see upwards of $600M in potential lawsuit proceeds.

To be clear, we think this represents the maximum amount of settlement proceeds. Given we are looking at the market from the view of total production, not based on named parties in the lawsuit, it is important to remember that not all entities involved in refined coal were named in the initial lawsuit. Furthermore, the collectability of the damages from some parties may be low. As a result, we think a reasonable estimate of the total proceeds for MEEC is in $200-400M range. Of course, we would love to prove too conservative!

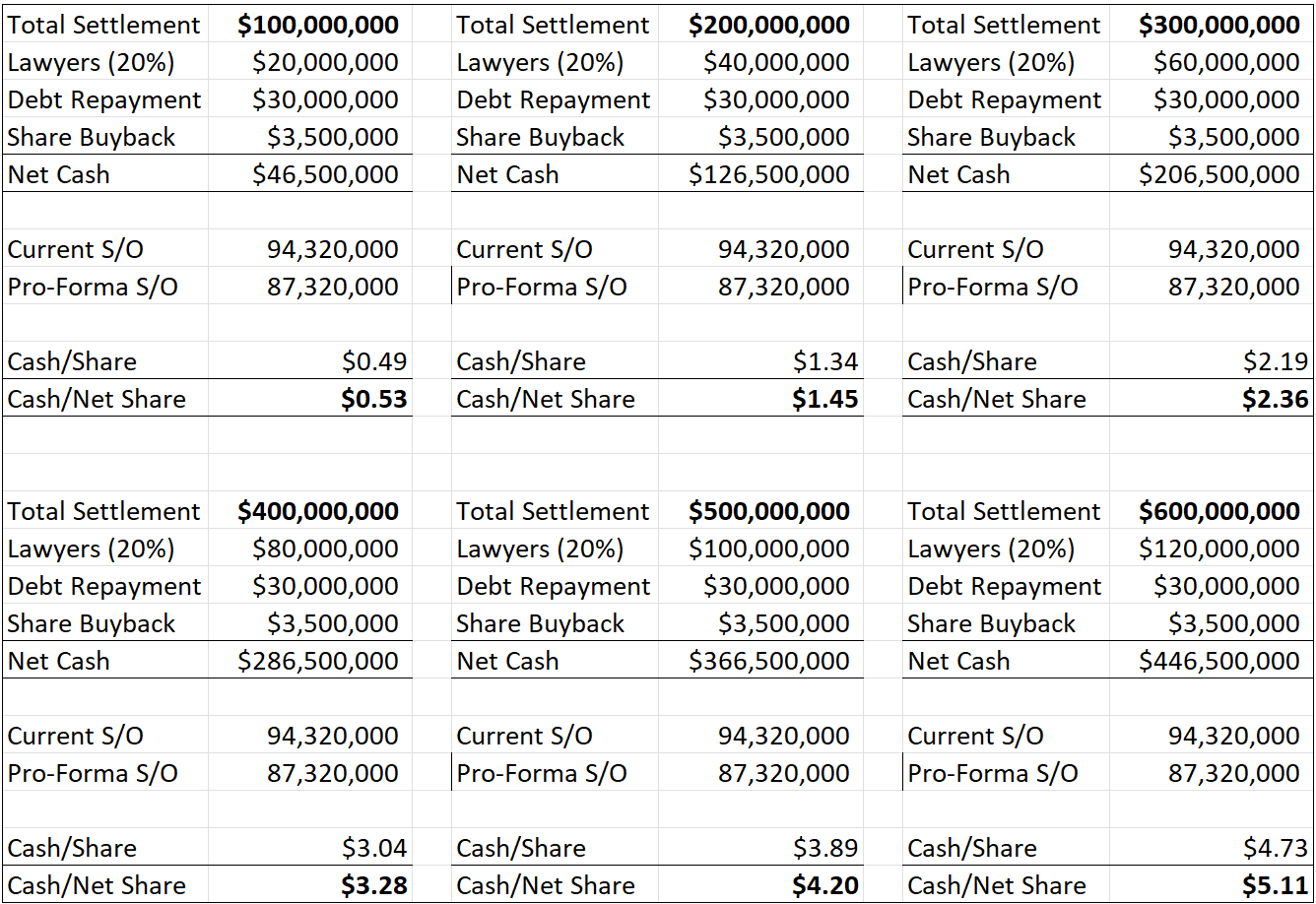

In total, MEEC owes about $30M to the current debt holder, AC Midwest. About $17M of this is not actual debt, but is a profit share on the settlement to the debt holders for working with them over the last few years to avoid bankruptcy. MEEC also has the option with the AC Midwest to buy back up to 7M shares for $0.50/share. We think that executing these two opportunities will significantly improve the equity value of MEEC by removing the debt overhead while also reducing the shares outstanding by about 7.5%

The table below is to help investors visualize the proceeds to the company based on various total settlement amounts.

{kind=link}

Source: Author’s estimates

In our conversations with Rick MacPherson, CEO, we asked about his priorities for the cash from the settlements. First, he plans to pay off the outstanding debt, then exercise the option to buy back 7M shares at $0.50, followed by investments in forever chemicals and rare earth opportunities to drive growth in 2025 and beyond.

At the time of writing, MEEC’s share price was about $1.15/share. We believe this price implies investors are valuing MEEC near the net cash the company will receive from the lawsuit proceeds. Investors are not giving any credit for the cash flow positive base business that should double to triple revenue on improving margins in the next 18 months, or the optionality of forever chemicals, Rare Earth Elements or SE Asia.

Newsworthy updates: Methane, Forever Chemicals, SE Asia and REE

In this section we will provide some quick updates to our previous article. Much of the first article holds true including a significant opportunity to grow market share in mercury removal, of course the refined coal lawsuit opportunity, and the opportunity in REEs.

However, one area that is no longer likely to play out as anticipated is the opportunity in methane gas. In recent conversations, Rick has informed us that they need to do more work on that area. As a result, we don’t expect much progress here in the near term given the emerging opportunities in forever chemicals, SE Asia and Rare Earths. As a result, we think the methane opportunity has moved to the backburner.

With the success of the recent lawsuit, we think MEEC is well positioned to grow the base mercury removal business by 2-3x over the next 18 months in the US. This is in contrast to current 2024 estimates which assume only 40% revenue growth.

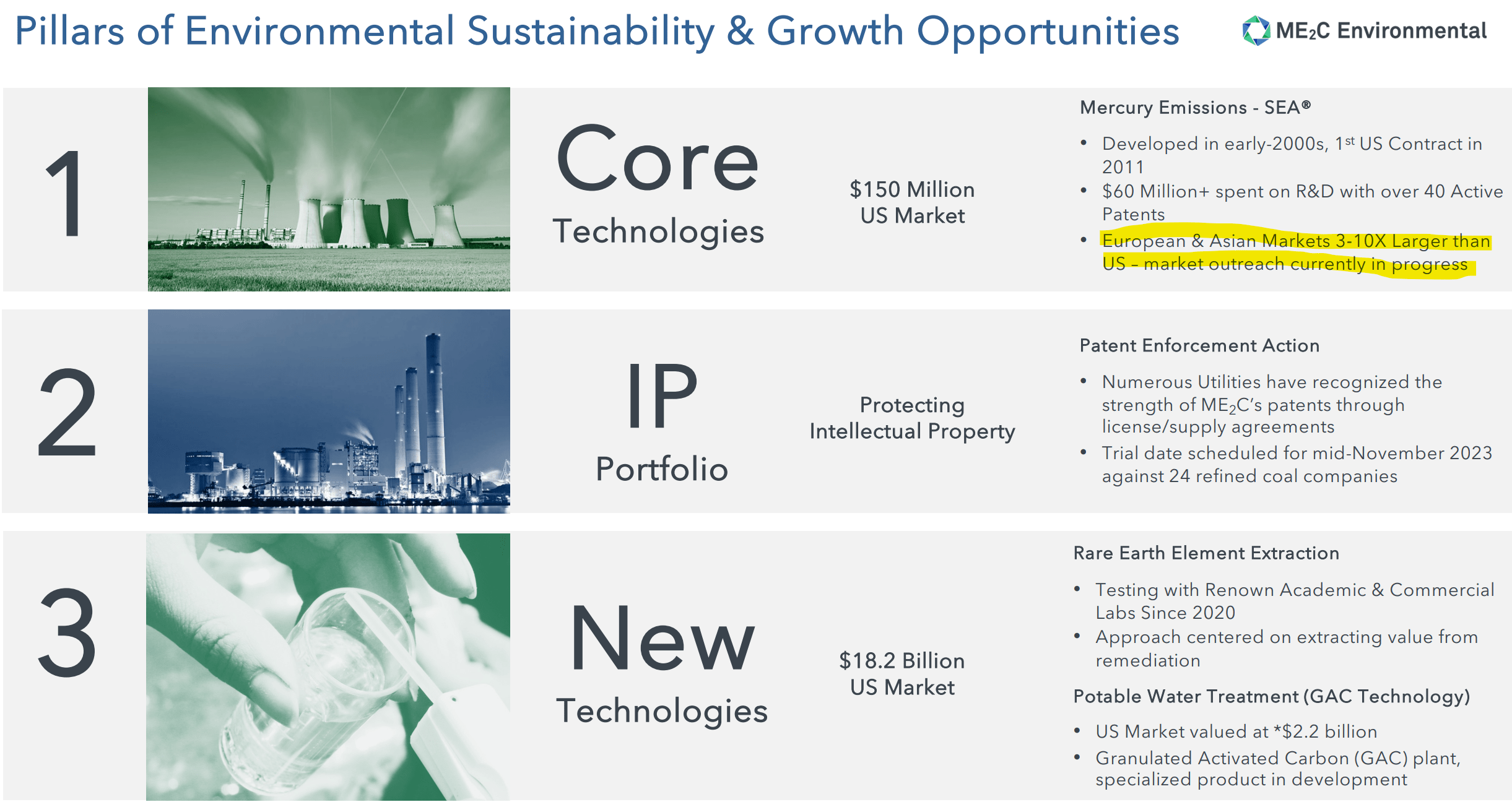

In addition to the anticipated strong revenue growth in the base business we anticipate seeing first revenues from the South East Asia consulting opportunity in mid-2024. While this likely won’t be more than a few million dollars, it opens up a very significant long-term opportunity to grow the business internationally. The total market for mercury removal in Asia could be as much as 10x the north American opportunity, as shown in the most recent investor presentation.

{kind=link}

Source: MEEC investor Presentation September 2023

During 2024 we also expect to learn a lot more about MEEC’s plan to enter the Potable Water Treatment market via the recently announced forever chemical opportunity. This is a big market with minimal other effective competitive solutions currently. If MEEC can successfully penetrate this market, which we anticipate they will, it should provide meaningful revenue in 2025, driving the next leg of growth for the company.

Based on our conversation with management, the size of the opportunity, the anticipated timing of regulations and the availability of MEEC’s solution lead us to believe MEEC has a very sizable near-term opportunity in this new market. We expect that water treatment will overcome the core mercury removal business in terms of both revenue and profitability by late 2025 or early 2026. Most importantly, this business will carry margins well above the core mercury business, which should add a turbocharger to the company’s profitability going forward.

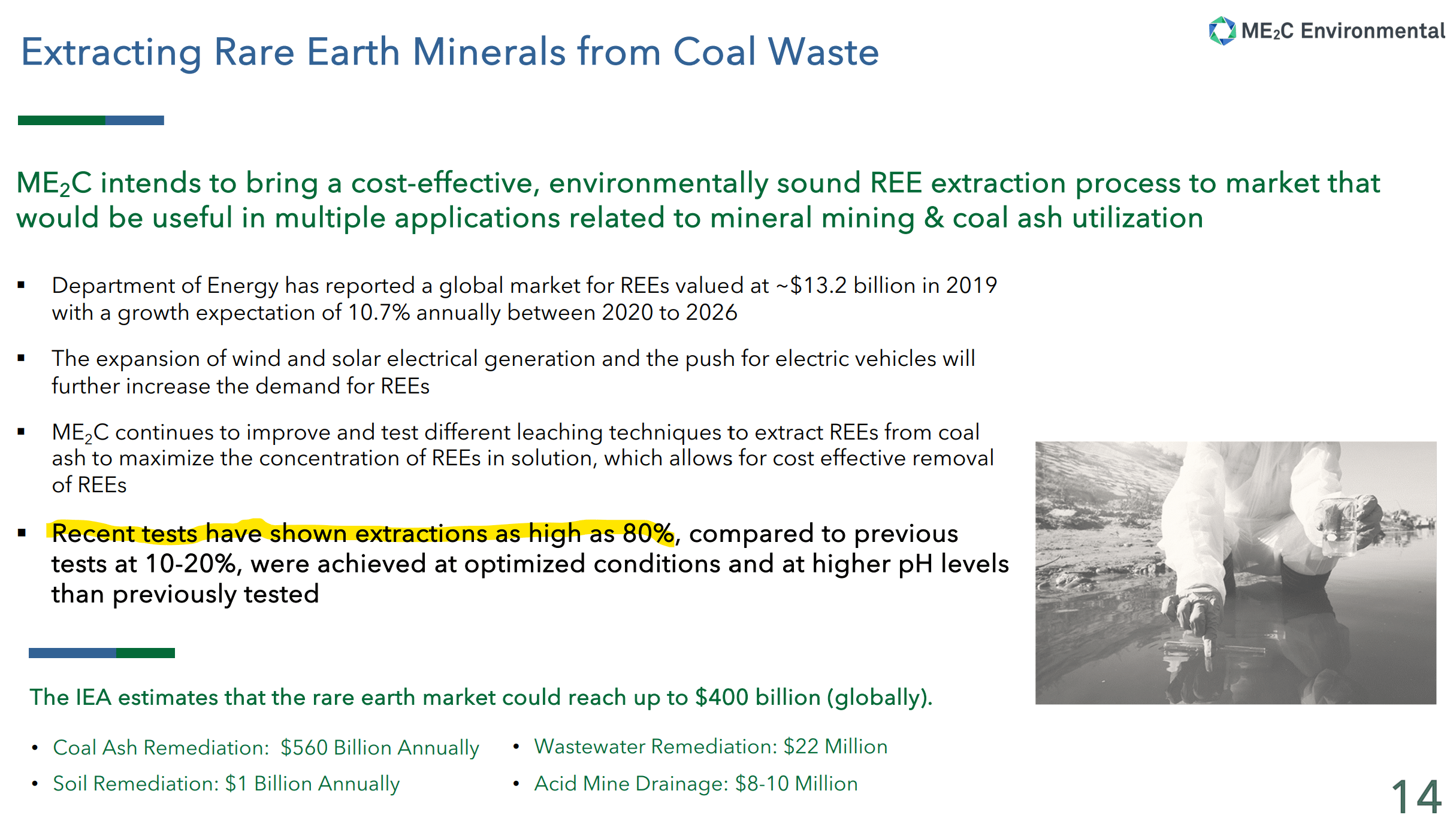

Rare Earths have had a much more difficult time working than we or the company anticipated back in 2021. The project was beset with setbacks relating to the preparation of the precursor liquid that MEEC’s technology is then applied to. Without writing a dissertation on the subject – the gist of the story is as follows. In order to be able to extract a commercially viable amount of rare earth metals from coal ash ponds, the liquid needs to first be concentrated. MEEC was assured by numerous labs that this step would be no problem. Unfortunately, each time the labs were called upon to deliver the concentrated liquid, they would fail to reach the thresholds laid out by MEEC.

Eventually, MEEC decided to develop a method to concentrate the fly ash pond liquid on its own, in addition to their extraction technology, so they could move forward with this product. We are happy to report that the company has successfully developed the concentration step, and has run lab test pulling up to 80% of the REE’s from concentrated fly ash liquid. MEEC is finally ready to begin field trials of the REE extraction technology. We expect the field trials to begin in the 1H24, with meaningful revenue adding to the company’s growth in 2026.

{kind=link}

Source: MEEC investor Presentation September 2023

Like the forever chemicals business, REE will be another high margin opportunity for MEEC as they plan to license this technology. Utilities and environmental remediation companies are actively looking at ways to clean up these ponds. However, in most cases the work has yet to begin because it is an expensive process with limited funding parties. MEEC’s technology allows the environmental remediation companies to capture and re-sell the REEs to fund the cleanup effort. This should provide the economics that will help fund cleaning up one of the most significant environmental disasters facing the US today, fly ash ponds.

Last, but not least, Rick recently announced that the company has begun to explore opportunities to bring environmental technologies to SE Asia. We believe the company is very close to starting their first demonstration project, which should begin early in 2024 leading to revenues later in the year. This is another attractive opportunity for the company to add high margin licensing and consulting revenue to the business. Since the company will primarily play a consultant role this will not require MEEC to undertake large projects or hire employees in foreign countries.

Positioning for an imminent uplisting to NASDAQ

Over the last year and a half management has positioned MEEC to be uplisted upon reaching the appropriate share price. There are only two remaining hurdles to uplist the company to a major exchange, first, pay off the debt, which they will do with the lawsuit proceeds. Second, get the share price above $2 which we anticipate should not take long as more and more of the lawsuit news filters out to the market.

Why do we like MEEC now?

At 1035 Capital, we aim to uncover overlooked stocks that are undergoing positive catalysts for fundamental change. We specifically focus on catalysts to improve sales growth rates, margin levels, and asset efficiency. MEEC appears to fit all of these categories and is a type of stock we refer to as a “triple threat” which can often become a massive wealth compounder once the market understands the significance of the improvements occurring.

MEEC is very overlooked being on the OTC with limited sell-side coverage. The numerous catalysts related to the mercury control market alone support a significantly higher stock price but when we consider the substantial opportunities in forever chemicals, SE Asia and rare earth elements, the upside to this stock is enormous.

The manufacturing assets in place combined with the company’s accelerating contract awards and the ramp of the supply contracts from the recent lawsuit wins all position the company well for accelerating growth and improving margins for the next few years. We believe that the company’s manufacturing assets in place (that are already funded) can support considerable growth without needing significant new capital over the next few years.

Furthermore, MEEC is well-positioned to benefit from a realization of the importance of developing a reliable source of rare earth elements while also cleaning up the environment within the US. These materials are critical to many of our current technologies and will become increasingly important going forward. Concurrently, MEEC is providing a solution to the forever chemical problem that is beginning to be widely recognized as a significant health issue. The current administration is very focused on climate change as well as building green industries in the US. While the increasing recognition of the health threats posed by forever chemicals are likely to lead to new regulations in the near term. MEEC appears poised to benefit from both of these trends.

In addition, MEEC is standing at the precipice of uplisting to a major exchange. Upon uplisting, we anticipate seeing several new sell-side companies will pick up coverage of the company. We would not be surprised to see B Riley, Roth, Lake Street, Northland, Craig Hallum, and others pick up coverage of this profitable and growing green tech player shortly after uplisting.

The additional sell-side coverage combined with an uplisting to a major exchange is likely to drive increased institutional interest and ownership of the company. This influx of institutional ownership is likely to drive a much higher share price over time. Taking this into consideration, as well as our belief that the company is primed for an inflection in growth, margins, and asset efficiency, which historically has also been an excellent combination for driving a much higher share price, and we think the time is right to open a position before the crowd notices what they have been missing. Because the stock is still on the OTC, almost nobody knows about the company, which provides smaller investors an excellent opportunity to profit. We expect MEEC’s under-the-radar status is about to change for the reasons described above and this should benefit early shareholders.

Valuation

Pinning down a precise value for MEEC is quite difficult given the lack of comparable companies. For this article, we use a sum-of-the-parts analysis. We assume total proceeds from the tax lawsuit of about $200M or ~$1.50/share after the buyback. The base mercury business should double or triple revenue into the 50-60M range over the next 18 months. Assuming 2x sales for this revenue adds at least another $1.25/share to the valuation. We think the potential in forever chemicals is worth at least $1/share. We conservatively see the SE Asia opportunities and REE at another $0.50/share each. Finally, cleaning up the balance sheet is worth at least $0.33 in equity value. In total, we get to a sum-of-the-parts valuation of at least $5.00 today.

We are assuming $200M in total lawsuit proceeds, however, as shown in the section above, each additional $100M in proceeds from the lawsuit adds another 80-90 cents/share. In addition, as MEEC moves toward commercial success in their new market initiatives more value for these opportunities will become embedded in the share price.

Risks

- Faster transition to green energy leads to declining coal revenue

- Unexpected regulatory changes, or lack thereof

- Inability to penetrate new markets

- Loss of major customers

- Loss of patent protection on the SEA® Technology

- Negative outcome of Refined Coal lawsuit

- Competition pressures pricing

- Inability to add new partners

Conclusion

At the current share price, we think the market is entirely discounting the proceeds of the refined coal lawsuit as well as the optionality of new emerging growth markets. We believe a significant part of this discount is due to a lack of awareness about the company and the fact most institutional investors cannot invest in OTC companies.

Despite this, MEEC is in a very attractive position as the company executes its patent protection strategy driving a double or triple in the revenue over the next 18 months while developing their new end markets, forever chemicals, REE and SE Asia, that will drive growth for years to come.

Each of the new markets MEEC is entering are likely to become larger portions of the business than mercury control over time. Forever chemicals are the nearest term opportunity, with significant revenue expected in 2025. We expect to hear significant news on this front in the next 6 months. Next rare earth elements will move to commercial revenue in 2026 primarily through licensing agreements with utilities and waste remediation companies.

Each of these new products are based on the company’s core SEA® sorbent technology providing ample opportunities to leverage infrastructure and know-how to ramp asset efficiency and margins over time. Furthermore, the company’s existing plant infrastructure means the company can ramp sales significantly without the need for additional cap-ex. The minimal cap-ex requirements, soon to be 0 debt on the balance sheet, significant cash and positive earnings mean the company has very few significant drawbacks, with one notable exception being that it is still listed on the OTC.

This drawback should not remain as management is laser-focused on uplisting to the NASDAQ as soon as possible. We believe this uplisting will prove to be a significant turning point for the company leading to greater sell-side coverage as well as more liquidity in the company’s shares. We anticipate that increased awareness, sell-side coverage and increasing institutional shareholder demand will drive shares of MEEC toward our $5.00 price target in the coming months.

If you enjoyed this article and would like to be alerted of new publications, please follow us by going to the top of the page and clicking the "Follow" button or click here.

For further details see:

Midwest Energy Emissions: Tax Credit Settlement Provides The Cash For The Next Leg Of Growth