CA - MLPX: Midstream Energy ETF Growing 5.2% Yield Cheap Valuation Strong Performance

2023-12-06 12:20:59 ET

Summary

- Global X MLP & Energy Infrastructure ETF offers diversified exposure to midstream corporations and MLPs.

- The MLPX ETF has a good, growing 5.2% dividend yield, comparatively safe midstream holdings, and a cheap price and valuation.

- An overview of the fund follows.

The Global X MLP & Energy Infrastructure ETF (MLPX) offers investors diversified exposure to midstream corporations and MLPs. MLPX's good, growing 5.2% dividend yield, comparatively safe midstream holdings, and cheap valuation, make the fund a buy.

MLPX - Basics

- Investment Manager: Global X

- Underlying Index: Solactive MLP & Energy Infrastructure Index

- Dividend Yield: 5.16%

- Expense Ratio: 0.45%

- Total Returns CAGR 10Y: 5.1%.

MLPX - Overview and Investment Thesis

MLPX's investment rests on the fund's:

- Comparatively safe midstream holdings , with resilient business models and lower commodity price exposure than more traditional oil majors

- Good, growing 5.2% dividend yield, backed by stable cash-flows and revenues

- Cheap valuation , with most energy and midstream energy companies trading at sizable discounts to the broader equities market

The above make MLPX a strong investment opportunity, and one which seems particularly well-suited for income investors and retirees. Let's have a look at each of the points above.

Comparatively Safe Midstream Holdings

MLPX is a midstream energy index ETF. Midstream energy companies are those that generate most of their revenue from the transportation, distribution, and storage of energy products, including oil, natural gas, and refined products. The fund tracks the performance and holdings of the Solactive MLP & Energy Infrastructure Index, an index of these same companies. MLPX is not liable for corporate taxes, nor do investors have to file a K-1 form.

The index includes at least 20 midstream energy companies, narrowly defined. Most of these have to be structured as corporations, for regulatory and tax purposes. As with most indexes, there are a basic set of inclusion and exclusion criteria, centered on liquidity, size, etc.

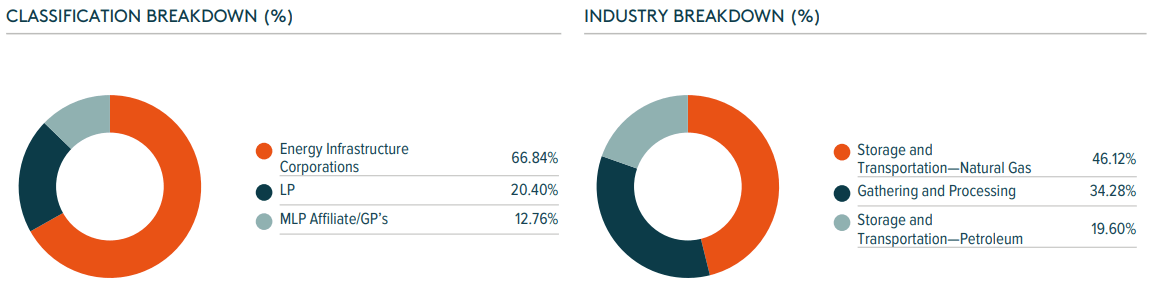

MLPX itself is about as diversified as a midstream energy industry fund could plausibly be, with exposure to most industry segments and corporate structures:

{kind=link}

The fund has investments in 25 different companies. Largest of these are as follows.

MLPX

MLPX is reasonably well-diversified for a midstream energy fund . Relative to broader equity indexes, including the S&P 500 (SP500), the fund is incredibly concentrated, as it focuses on a niche sub-segment, midstream, within a niche industry, energy. Due to MLPX's concentrated, undiversified holdings, I would keep position sizes small / moderate, and take care to not massively overweight energy in my portfolio.

On a more positive note, MLPX's midstream energy companies are much safer than the industry average, with the most resilient business models, comparatively safe revenues and earnings, and little commodity price exposure.

As an example, Enbridge ( ENB ) generates around 98% of its EBITDA from cost of service contracts with effectively zero commodity price exposure, and with low credit risk. Canadian oil producers might buy pipeline access from Enbridge to ship crude from Alberta to refineries in the Eastern Coast, for instance. Lower energy prices don't really impact these contracts, at least not in the short term.

Enbridge

Enbridge's more revenues lead to consistent financial results and growth, even under tough economic and industry conditions.

Enbridge

Enbridge's financials are much more resilient than those of most oil majors and producers, including Exxon Mobil ( XOM ) and Chevron ( CVX ). Each of these saw their EBITDA decrease by over half during 2020, and lost several years' worth of profit during the same. Enbridge saw losses too, but these simply erased one year of growth , leading to stagnant financials. Stagnant earnings are obviously not ideal, but much better than brutal losses.

Data by YCharts

MLPX's larger holdings are (mostly) comparable to Enbridge in the above. Due to this, MLPX tends to outperform during commodity price crunches, as was the case in 2020.

Data by YCharts

On a more negative note, I've found that the market sometimes perceives midstream to be riskier than it is, leading to higher-than-expected volatility and drawdowns. I went through some of the details and numbers for one company, Enbridge, in this past article, but the situation is generally the same. During recessions and commodity price crunches, share prices decline by more than EPS, and by more than warranted by fundamentals, in my opinion. One can see the process play out in the graph above. MLPX mostly performed in line with its peers during the downturn itself, during which everything was down. The fund only outperformed afterwards, as investors reassessed the situation, and cooler heads prevailed.

MLPX's comparatively safe midstream energy holdings are a significant benefit for the fund and its shareholders. Said benefit seems of particularly importance to more risk-averse investors and retirees, for obvious reasons.

Good, Growing 5.2% Dividend Yield

Midstream energy companies tend to distribute excess cash-flows to shareholders, with most of these companies sporting good, some very good, yields. MLPX itself yields 5.2%, a reasonably good figure, and higher than that of most equities, bonds, and broader energy equity indexes.

Data by YCharts

On the other hand, dividends are lower than those of high-yield corporate bonds, most closed-end funds aka CEFs, and some niche income-producing asset classes like business development companies ("BDCs") and mortgage real estate investment trusts ("mREITs"). It is a good yield, but not a great one.

Data by YCharts

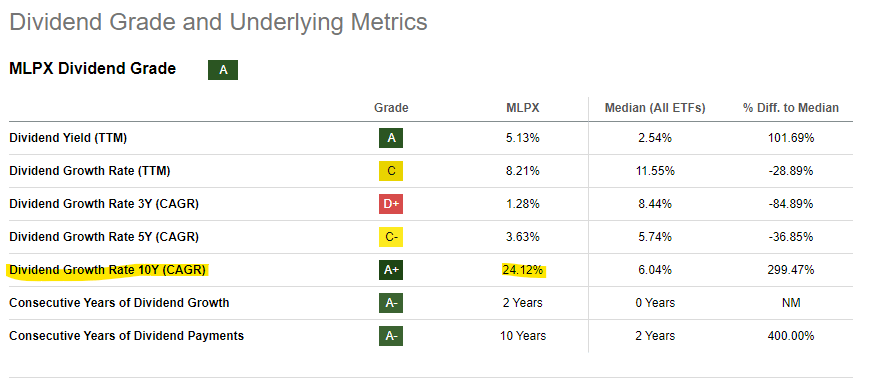

MLPX's dividend growth track-record is quite good, with significant dividend growth since inception and for the past year.

{kind=link}

Dividend growth is not consistent, with the fund sometimes seeing short-term dividend cuts, and medium-term stagnation. Dividends were last cut in 2021, in the aftermath of the pandemic. Dividends were stagnant from 2019 to 2022, in part due to the pandemic, in part due to midstream energy companies shifting to self-financing their CAPEX (better than dilutive share offerings at rock-bottom valuations, or expensive debt). Dividends resumed growing in mid-2022, at reasonably fast rates.

In my opinion, further dividend growth is likely, as industry conditions remain strong, and as several midstream energy companies have already announced dividend hikes. These include Cheniere Energy ( LNG ) and Enbridge .

MLPX's good, growing 5.2% dividend yield is an important benefit for the fund and its shareholders.

Cheap Valuation

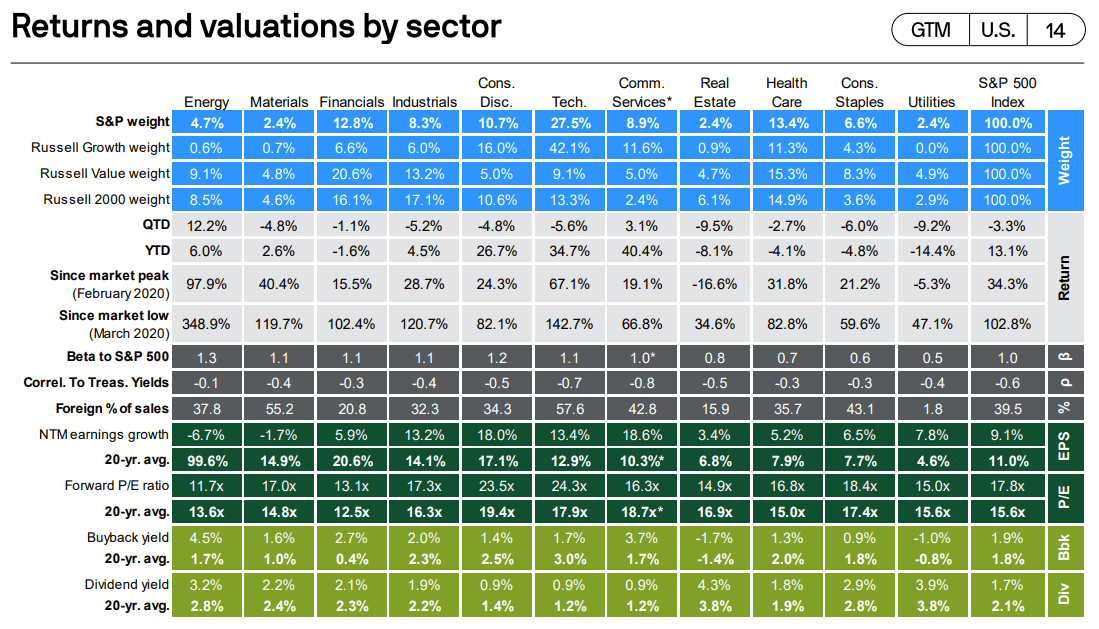

Energy stocks have traded with significant discounts for years, due to bearish investor sentiment and weak performance in prior years. Energy stocks currently trade with a 11.7x PE ratio, a significant discount relative to the 17.8x S&P 500 average, and a moderate discount to the industry's long-term historical average. Table below, you might have to squint a bit.

{kind=link}

Midstream energy companies tend to trade at discounted valuations too, with MLPX itself sporting a 13.6x P/E ratio, and a 2.0x P/B ratio. The fund trades at a significant discount to the S&P 500, but a small premium to broader energy equity indexes.

Morningstar - Table By Author

MLPX's cheap valuation benefits investors in two key ways.

First, cheap valuations boost the impact of dividends and buybacks. MLPX currently yields 5.2%. If it traded with the P/E ratio of the S&P 500, yields would drop to 3.7%. That 1.5% differential is due to the fund's cheap valuation, and is an important, straightforward benefit for shareholders.

Buying back shares is more accretive to EPS for cheaper companies, and they can buy back more shares for the same amount of cash. Midstream energy companies focus on dividends, but many have announced sizable buyback programs these past two years, including Cheniere and Enbridge .

Second, cheap valuations can always normalize, leading to significant capital gains and market-beating performance. This is ultimately dependent on investor sentiment, which is quite fickle, and not always rational. Energy sentiment has markedly improved since the pandemic, leading to significant capital gains since the same. MLPX benefitted from these, as expected.

Data by YCharts

Moving forward, I am not sure that investors should expect improved industry sentiment or (significant) capital gains. Investors seem focused on growth, and I see no catalyst that might precipitate a change towards value or energy. Importantly, dividends and buybacks are not dependent on investor sentiment, and benefit shareholders regardless of what the market does or thinks.

MLPX - Performance Analysis

MLPX's performance track-record is, well, complicated.

Long-term returns are quite weak, as energy returns stagnated from 2013 to 2020. MLPX significantly underperformed relative to the S&P 500 during said time period. The fund did a bit better than broader energy equity indexes, but results were still mediocre.

Returns since the pandemic have been much stronger, due to a combination of higher energy prices, improved investor sentiment, cheaper valuations, and a strategic shift towards more sustainable CAPEX and distributing excess cash-flow to shareholders in the industry. MLPX has significantly outperformed the S&P 500 these past three years, slightly underperformed the last five.

MLPX tends to perform quite similar to broader energy equity indexes, although their returns have diverged this past year, especially these past three months. I am not sure why this is the case.

Seeking Alpha - Chart by Author

In my opinion, MLPX's future returns are likely to remain strong, as the fundamentals that led to present strength remain in place. Valuations remain cheap, dividends and energy prices remain (reasonably) high, investor sentiment remains adequate. Buying MLPX one decade ago would have led to underperformance, but the fund yielded 2.0% one decade ago, less than half what it yields now. Conditions have changed since then, as has performance.

Data by YCharts

Besides the above, I would like to reiterate the fact that MLPX has performed much better these past few years. I've been covering the fund since 2018, and the fund has outperformed the S&P 500 in each of my bullish articles, including the first one :

MLPX Previous Article

and the latest one :

MLPX Previous Article

I have been bullish about the fund before, during, and after the pandemic, before and after the rotation into value in 2022, and during the rotation into growth of 2023. MLPX has consistently outperformed in the past and will, I believe, continue to outperform moving forward.

Conclusion

MLPX's good, growing 5.2% dividend yield, comparatively safe midstream holdings, and cheap valuation, make the fund a buy.

For further details see:

MLPX: Midstream Energy ETF, Growing 5.2% Yield, Cheap Valuation, Strong Performance