MRNA - Moderna Stock: Looking For The Future In Q4 Earnings

Summary

- The COVID-19 public health emergency is coming to end in May 2023. As a result, Moderna, Inc. is approaching a long earnings trough after a couple years of mind-blowing growth.

- The market is going to hyper-fixate on the expected year-over-year declines in earnings in the upcoming Q4 earnings report scheduled for Thursday, February 23rd.

- I believe investors should not be engrossed by the lack of growth, but they should be on the lookout for what the company is going to do next.

- Moderna is more than just a COVID-19 vaccine company with nearly 50 pipeline programs and a few in the late stages of development, or near the finish line.

- I see three topics that investors need to be focused on in the upcoming earnings. I provide my valuations and will discuss my plan for my minuscule MRNA position.

Like most of the COVID-19 stocks, Moderna, Inc. (MRNA) has been getting treated like everything else in this market that shows peaking growth… tossed out and sold off. However, I think that narrative could change after the company's upcoming Q4 earnings, which are scheduled for Thursday, February 23rd.

As the Street fixates on the year-over-year drop in Spikevax sales and the questions around the commercial sales, I will be looking for something that tells us a little bit more about Moderna's post-COVID world, both in terms of the business and their technology. Investors need to recognize that the COVID opportunity is still present, but the company's future is not preserving this single market. I believe Moderna's post-COVID roadmap already exists and the company is ready to roll it out on the 23rd.

I see three different areas that investors should direct their focus during the earnings release and conference call. I intend to highlight these three areas and will discuss why I believe they are critical. Then, I will construct a "Post COVID Bull Thesis" and will point out some of the downside risks to this position. Finally, I provide some valuations and my plan for my MRNA position going forward.

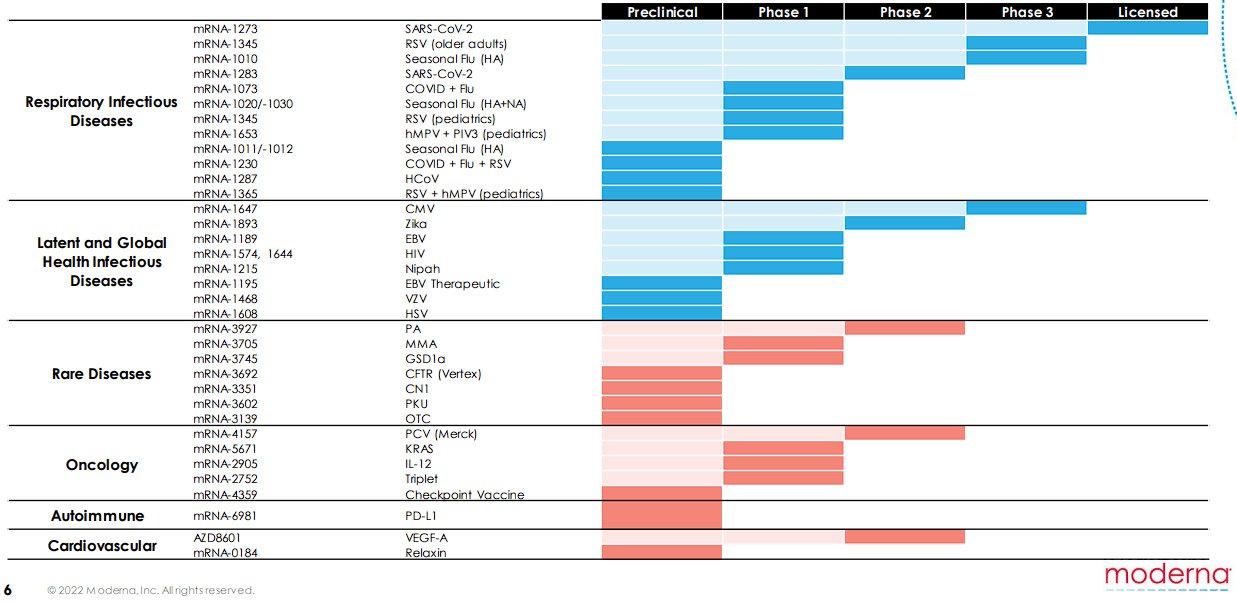

Non-COVID Pipeline

Moderna's Non-COVID pipeline is not only key to Post-COVID revenues, but it is also vital to validate the company's technology to be operative in numerous indications. Some of the company's late-stage vaccine programs include respiratory syncytial virus "RSV," Influenza "flu," and cytomegalovirus "CMV."

The company recently posted top-line data from their ConquerRSV pivotal trial Phase III trial for RSV vaccine candidate, mRNA-1345. ConquerRSV's top-line data revealed that the mRNA-based shot elicited 83.7% efficacy against RSV lower respiratory tract disease in older adults. In addition, the data supported that mRNA-1345 was generally well-tolerated, with no safety concerns identified. Moderna intends to submit an NDA for mRNA-1345 to the FDA for regulatory approval in the first half of this year. mRNA-1345 has the FDA's Break Through Designation "BTD" and Fast Track Designation "FTD," so perhaps we see an accelerated approval that could put the vaccine's PDUFA date towards the end of this year.

If approved, mRNA-1345 would be the company's first non-COVID-related product to clear the FDA and hit the market. Obviously, this would be a big win commercially, but it is also a huge win for the company's technology, R&D team, and clinical organization. It is important to note that Moderna is not the only company approaching the finish line for RSV. Pfizer ( PFE ) and GSK ( GSK ) have their own RSV vaccines, which have produced competitive results to Moderna's vaccine. What is more, GSK has a PDUFA date in early May and Pfizer has a PDUDA near the end of May. So, it looks like both of these vaccines will be on the market ahead of Moderna's.

What is more, the CDC advisory committee is in June, which should come with an endorsement. This would give both of these vaccines a "first-to-market advantage," which could hurt Moderna's commercial upside from this product candidate. However, I will stress the importance of obtaining approval for Moderna versus GSK and Pfizer, who have multiple approvals each year. Investors need to be on the lookout for any updates on their NDA submission and the company's plans from commercialization.

Moderna's CMV vaccine candidate, mRNA-1647 , is currently in their CMVictory Phase III trial. Moderna's CMV vaccine blocs six mRNAs in one vaccine, which translate for the virus's pentamer complex and gB proteins positioned on the exterior of CMV. Both the pentamer complex and gB are critical for CMV to infect the body. mRNA-1647 is intended to trigger an immune response against both the pentamer and gB, thus preventing a CMV infection and possibly addressing latent viral infections. CMV is a leading cause of birth defects around the world, yet, we don't have an approved vaccine. mRNA-1647 stands to be the first vaccine to be approved, which the company believes is a $2B to $5B in annual sales market. Moderna's Phase III was at 40% enrollment in January, so hopefully, we hear some progress with enrollment.

The company is also working on a few Influenza vaccines, including mRNA-1010, a quadrivalent targeting A/H1N1, A/H3N2, B/Yamagata, and B/Victoria. Recently, the company reported "mixed" results from a southern hemisphere Phase III study that showed mRNA-1010 generated an immune response against influenza A strains that were equal or superior to contemporary vaccines. Conversely, it showed a lackluster response against the less-common influenza B strains. Modern said that they already updated the vaccine to improve immune responses against influenza B and "will seek to quickly confirm those improvements in an upcoming clinical study." The company is also running another Phase III study in the northern hemisphere, so there is a possibility those numbers show more promise.

In addition to infectious diseases, the company is working on mRNA programs in rare diseases, oncology, autoimmune, and cardiovascular indications.

The company's lead rare disease candidate is mRNA-3927 Propionic academia "PA," which is in a Phase II trial. PA is a pediatric disease where a patient cannot process certain parts of proteins and lipids appropriately due to a deficiency of propionyl-CoA carboxylase, which converts propionyl-CoA to methyl malonyl-CoA. Most PA cases start displaying within 3 days of life, and left untreated may lead to coma and death. mRNA-3927 is designed to improve the condition by activating propionyl-coenzyme, thus, reducing the number of metabolic decompensation events "MDEs," which regulators appear to back as a primary endpoint for the study. Like most rare diseases, there is no approved therapy for PA, so a potential approval of mRNA-3927 would be a clinical and commercial win for Moderna and patients.

In oncology, Moderna is working with Merck ( MRK ) for mRNA-4157 personal cancer vaccine "PCV" for stage III/IV melanoma following complete resection. Moderna just announced that their Phase IIb KEYNOTE-942/mRNA-4157-P201 trial of mRNA-4157/V940 in combination with KEYTRUDA improved recurrence-free survival "RFS" vs. KEYTRUDA and reduced the risk of recurrence or death by 44% compared with just KEYTRUDA. The combination of mRNA and immuno-oncology agents could be the basis of creating a personalized cancer vaccine that could be employed in a variety of oncology settings. Obviously, improving the efficacy of one of the world's best oncology drugs will demonstrate mRNA's ability to game changer in some of the worst cancer types, which could be a massive commercial opportunity and change the treatment paradigm. I am eyeing any updates from Moderna to see if they are expanding their efforts into other tumor types.

The company is also taking autoimmune disorders including autoimmune hepatitis with mRNA-6981, which is expected to influence the myeloid cells to provide additional co-inhibitory signals in the immune synapses by enhancing endogenous expression of PD-L1. Thus, restraining auto-reactivity without the global suppression of the immune system is a serious side effect of other autoimmune therapies. Obviously, if the company can prove they can produce operative autoimmune mRNA therapies, they could be a massive disruptor in several multi-billion dollar markets.

Moderna is also diving into cardiology by coding a molecule to treat patients with heart failure. The company has already initiated a Phase I study, so investors should remain vigilant about any potential data readouts that could determine proof-of-concept. Cardiology is a huge opportunity and treating heart failure with mRNA technology would be a massive breakthrough that could help thousands of patients live a longer and healthier life and possibly prevent the need for multiple heart surgeries. Again, another huge opportunity both clinically and commercially.

What is my point? Why is this relevant to the company's earnings report?

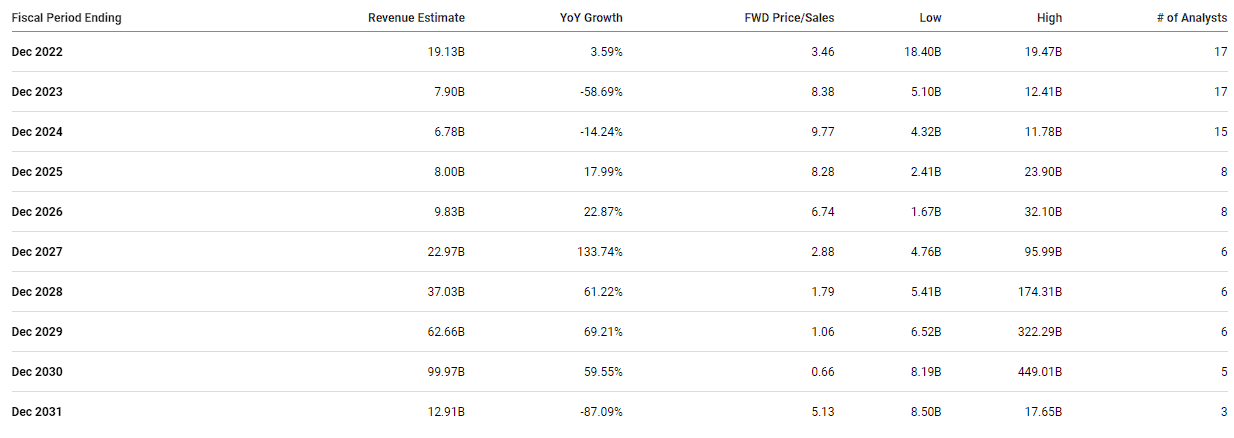

Well, the Street expects Moderna to report significant decreases in revenue year-over-year for Q4 2022 and through the end of 2023 as COVID-19 revenue fades.

{kind=link}

Since Spikevax and boosters are the company's only commercial product, investors should be prepared for wounding earnings headlines highlighting the year-over-year decreases in EPS and revenue. Instead of focusing on the unavoidable figures, investors should be focusing on how the company is taking the cutting-edge technology that provided billions in revenue to a plethora of indications and areas of medicine.

{kind=link}

Indeed, most of these programs are early in development, but the company now has a mountain of cash that can be used to open multiple trial sites and keep the pedal to the floor with R&D efforts to further expand the pipeline. In fact, Moderna expects R&D investments in 2023 to be around $4.5B, up from ~$3.3 billion in 2022.

Updates on these programs and pipeline initiatives can help investors envision what the company could achieve and potentially project future revenues. The Street believes Moderna is going to go through a transition for a couple of years, reporting year-over-year decreases in revenue.

{kind=link}

However, as some of these pipeline programs potentially hit the market, we should see Moderna reestablish a growth trajectory that really accelerates in the second half of this decade. In fact, some analysts believe Moderna's revenue growth is going to explode and possibly hit ~$450B in annual revenue in 2030. Now, I think that is beyond rosy… but perhaps that analyst is onto something considering the potentially broad application of mRNA in every major area of medicine. Remember, mRNA is like "bio-software" that is sending the codes to the body's cells to make proteins to "make this," "repair that," "start that," "stop that," etc. By simply formulating an mRNA therapy, Moderna has the prospect to have a product for almost every major disease or condition. So, $450B is not as absurd as it sounds, especially if the company hits on oncology and cardiology indications.

Knowing what the company is going to do in the near term is important now because the company could establish proof-of-concept in these larger markets in the next few years, and remaining vigilant about the company's progress will allow investors to manage their positions for the future, rather than worrying about waning COVID-19 revenue.

Expanding The Business

Investors should also be paying attention to how the company is going to expand their business. Moderna has been on a streak of signing partnerships that secured manufacturing partnerships and evening striking a deal with a gene editing company called Metagenomi. Moderna also struck a deal to acquire OriCiro Genomics, who has an innovative method for cell-free synthesis and amplification of plasmid DNA, which should help improve mRNA manufacturing. In addition, the company is collaborating with CytomX Therapeutics ( CTMX ) for the "development of mRNA-based conditionally activated therapeutics for oncology and non-oncology conditions." Moderna also has a collaboration with Carisma Therapeutics working on chimeric antigen receptor monocyte "CAR-M" therapeutics for the treatment of cancer.

These collaborations, partnerships, and acquisitions are not exactly blockbuster deals, but they do indicate that Moderna is looking to expand their horizons while bolstering their position as a leader in mRNA technology.

So far, Moderna has been disciplined with their deals, but investors need to remain attentive to see where the company is placing their chips. The company might have the technology and know-how to move into other arenas, but the world of information molecules is dominated by intellectual property battles. Gene editing would be a great opportunity for Moderna thanks to mRNA technology possibly helping deliver gene-editing cargoes to difficult tissues. However, Moderna is going to have to strike more deals to move into that realm… or possibly make a bid for one of the big CRISPR or gene therapy companies.

These sorts of moves could take Moderna from an mRNA company to a leader in cutting-edge medicine and a true competitor amongst big pharma.

Shareholder Value

Typically when a company is projected to report two years of decreasing revenues and shrinking earnings, investors start looking for the doors. However, in the case of Moderna, I am looking at where to buy it. Not only because I think the company's cash position will unlock their pipeline and offer immense upside potential… but that cash position could also provide shareholder value with buybacks and potentially a small regular dividend.

The company already has a share buyback program, and they repurchased 23 million shares at an average price of $143/share to total $3.3B in 2022. The company reported that they still had $2.8B left from the $3B August authorization. However, a dividend can provide a little bit of income, which would attract more investors and provide a reason for shareholders to stick around to see the pipeline play out over the next five or ten years. A simple 1% dividend would be about $500M a year, and they already have the funds to support that for the remainder of the decade.

Any of these shareholder-friendly activities will be critical to share price performance as we wait for the company's pipeline to mature.

Post-COVID Bull Thesis

Now that Moderna has proven that their mRNA technology works with their Spikevax vaccine, the company will be able to take advantage of mRNA technology and start to intrude indications that are dominated by small or large molecules. Moderna's mRNA technology is expected to be operative in a cell's transmembrane protein, intracellular protein, and compartments of cells, such as the mitochondria, which opens the door to a lot of opportunities. As long as the company can identify the proteins, they should be able to produce a viable candidate because they use the same chemistry for every product, so they should have a higher likelihood of success of drugs getting to the clinic and getting through the FDA to the market.

This also allows the company to have a dramatically shorter development time compared to large molecules because Moderna is basically developing nearly the same product using the same processes. No need to build out a new facility and develop a manufacturing process for each new pharmaceutical or biologic. Moderna believes they could use the same manufacturing method, factory, and staff, thus improving efficiencies and maximizing CapEx. This allows Moderna to take on a " copy-and-paste " type of approach to their drug development by simply changing the order of the sequence to elicit the desired protein. These advantages helped Moderna go from 21 products in development in 2018, to nearly 50 in 2023 in seven areas of medicine.

Now that the company has basically de-risked their technology with Spikevax, they can accelerate the development of new therapies using that $18B in cash to become the undisputed leader in mRNA therapies. With a near-limitless amount of mRNA applications and indications, Moderna's upside appears to be equal. The opportunity comes from the market's hyper-fixation on the forecasted COVID-fade, which could have a negative impact on the share price and might prevent a resurgence for a prolonged period of time. Thus, allowing an investor to amass a respectable position while enjoying a respectable share buyback program, and the possibility of booking some profits on spikes in the share price around pipeline catalysts.

Downside Risks To The Thesis

Despite my bullish outlook, my Moderna, Inc. thesis does have some risks that investors need to be aware of.

First, there is the possibility that apprehensions about mRNA technology will persist following the COVID-19 vaccination campaign and the government's botched PR efforts. Not only could this have a harsh impact on Spikevax's commercial sales, but it might also hurt patient demand for future mRNA therapies. Obviously, a worse than projected drop in Spikevax sales and slow adoption of new therapies will hurt earnings, which will translate to the share price. The company's singular focus is mRNA technology, so they need their products to perform well in the clinic, as well as all mRNA products to prevent a catastrophic outcome to their entire pipeline and commercial portfolio.

Second, Moderna has a strong list of competitors that utilize mRNA, as well as pharmaceuticals and biologics. Clearly, Pfizer is the most concerning considering their mRNA COVID-19 vaccine and new mRNA R&D endeavors. Similar to CRISPR and CAR-T, I suspect the legal battles of mRNA IP are going to be a long and ruthless. In fact, Moderna is taking on Pfizer and BioNTech SE ( BNTX ) in London High Court over the mRNA technology used to develop their COVID-19 vaccine, Comirnaty. Moderna claims "This groundbreaking technology was critical to the development of Moderna's own mRNA COVID-19 vaccine, Spikevax. Pfizer and BioNTech copied this technology, without Moderna's permission, to make Comirnaty." Admittedly, I haven't performed a deep dive on the specific claims and what patents were potentially violated, but rest assured, this legal battle is not going to be settled in the near future. What is more, it is possible we see this IP skirmish occur numerous times as these top mRNA companies race to gobble up additional patents for other indications.

Third, there is the possibility of investor fatigue during the upcoming earnings trough. As I mentioned above, Moderna is expected to go through a rough patch for at least a couple of years, with the possibility the company returns to reporting a negative EPS.

{kind=link}

Even if the company outperforms with Spikevax in the commercial market and they have a strong winning streak in the clinic, it is possible the market will continue to punish the ticker because of its previous success. The COVID-fade is a legitimate concern, as is even hurting Pfizer which has a long track record of success and a healthy dividend, yet their share price performance is a concern. Investors need to accept the possibility the market will punish the share price for an extended period of time.

Considering the risks above, I am assigning Moderna, Inc. a conviction level of 3 out of 5 at this time in the Compounding Healthcare Marketplace Service.

Valuations & Plan

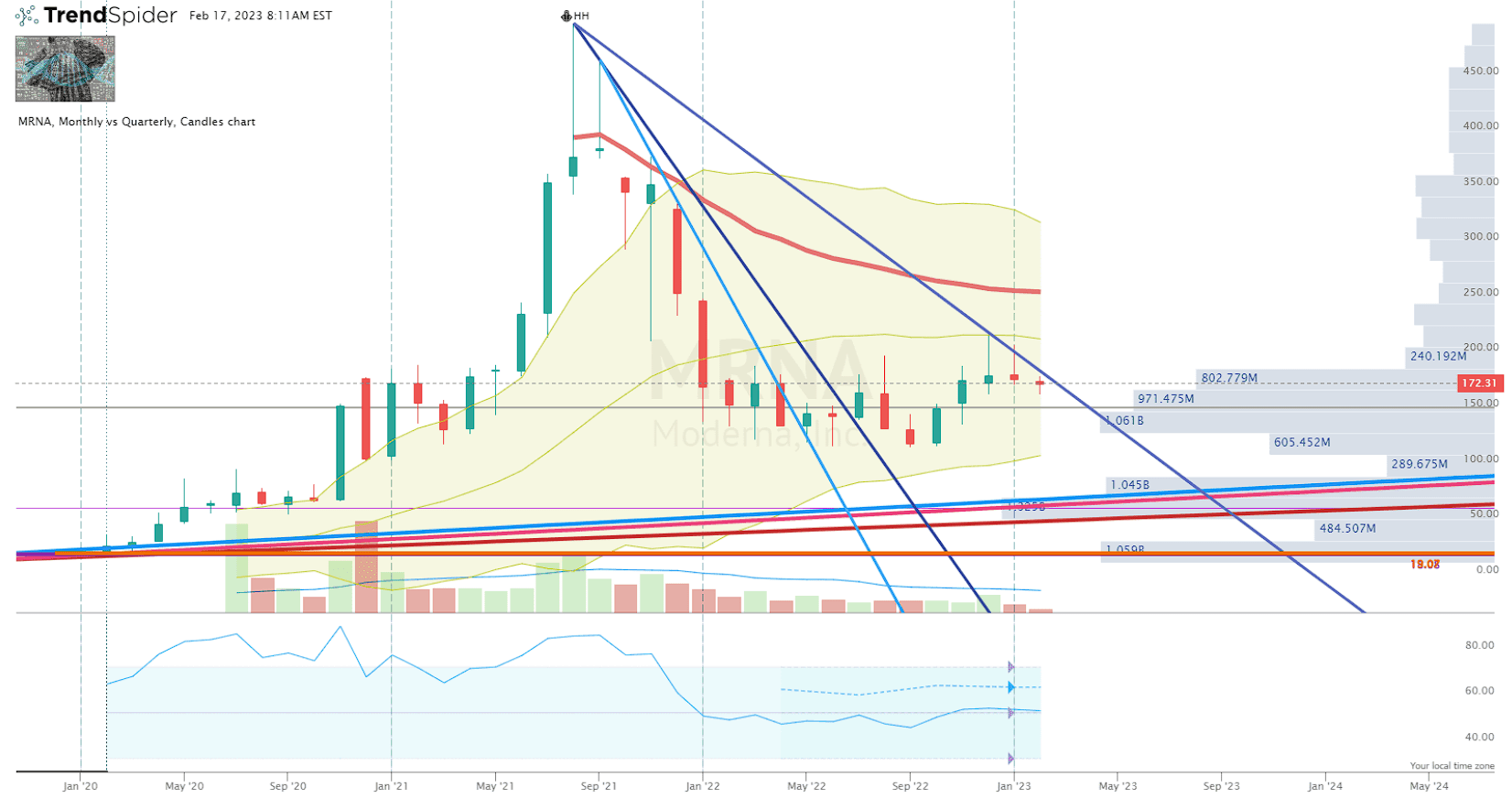

As usual, the market took MRNA too far to the upside and nearly hit $500 per share in 2021 with a market cap equivalent to MRK.

{kind=link}

MRNA Monthly Chart Enhanced View ( Trendspider ).

Now, we are facing an equal and opposite reaction to the downside, with MRNA trading around $170-$180 per share.

So What Should MRNA Be Trading At?

Using several valuation models, I see Moderna, Inc.'s fair value fluctuating from $140 to $570 per share, which is obviously a broad range.

{kind=link}

Personally, I am going to focus on the Discounted Cash Flow "DCF" five-year growth exit with a moderate WACC of 8.8% and a 1% growth rate, which points to MRNA's fair price of $255.34 and a 48.2% upside. On the low end, I used a WACC of 7.5% and 0.5% long-term growth rate, which suggests a fair price of ~$213.50 per share and a 24% upside. So, I am looking to adjust my Buy Thresholds and Sell Targets off these valuations in order to amass a hefty MRNA over the next couple of years.

At the moment, I have a laughably small Moderna, Inc. position after nabbing some around my Buy Threshold of $118 back in October. However, I set my Sell Target 1 to $177 per share, but I really don't have enough to book profits. Obviously, I am anticipating elevated volatility around the earnings, so I am adjusting my MRNA Buy Threshold to $135 per share, and moving my Sell Target 1 to $214 per share. The goal is to take advantage of the volatility by trading the range to book profits, while also amassing a large Moderna, Inc. position of a long-term investment.

For further details see:

Moderna Stock: Looking For The Future In Q4 Earnings