FSLY - Momentum Is Now On Fastly's Side

2023-09-12 12:02:41 ET

Summary

- Fastly, a content-delivery network platform, has experienced a significant surge in its stock price this year.

- The company has shown strong execution and customer diversification, reducing reliance on single large customers.

- Fastly's usage-based business model and economies of scale position it for further growth and margin expansion.

- Trading at ~5x FY24 revenue, Fastly has room for further upside. I'd hold on until a price target of $27.

Time and time again, I've emphasized the importance of individual stock-picking, but never has that been more important than in the current market environment. With interest rates yielding roughly 5% risk-free, we have to make sure that the stocks sitting in our portfolios merit the trade-off with income.

And within individual stocks, I aggressively favor "growth at a reasonable price" names and have no problem taking on "fallen angels" that are trading at valuation discounts but are enjoying fundamental rebounds. Fastly (FSLY), a content-delivery network (CDN) platform that is a critical component of internet infrastructure, falls squarely into this bucket. Year to date, the stock has surged nearly 3x, with gains taking hold after the company's latest Q2 earnings release in early August. Still, the stock remains substantially down from 2021-era highs above $100.

In spite of Fastly's sharp YTD rally, I remain bullish on this name (see my previous bullish article on Fastly, published when the stock was at ~$15 in May, here ). The key piece here: even though Fastly's valuation has started to recover, so have fundamentals: in Fastly's most recent quarter, which we'll cover in the next section, the company enjoyed both a rebound in revenue growth rates as well as net expansion rates.

In an industry environment where most tech stocks are struggling to close deals, especially to enterprise clients, Fastly has shown tremendous execution. The company implemented new pricing tiers and packages, that have been very well-received by customers. The company has also signed on a bevy of new enterprise-level retail industry clients, including its first-ever win at Abercrombie & Fitch (ANF), despite the fact that the retail industry continues to see headwinds from softer consumer spending.

Here is my full long-term bull case for Fastly:

- Fastly's usage-based business model opens the door to tremendous growth - Fastly, alongside other software/technology peers like Twilio ( TWLO ), was among the companies that could fully take advantage of the pandemic and the increase in internet traffic that came with it. Because Fastly's pricing is based on volumes of content delivered, as the underlying customers continue to grow their websites and traffic, Fastly's revenue will also grow proportionally. Fastly's dollar-based revenue retention rates recently clocked in the ~120% range, which is an enviable target vis-a-vis other tech growth stars.

- Greater customer diversification - 2020 caused a big disruption for Fastly when it lost its biggest customer, TikTok. Since then, however, Fastly has proven its "horizontal" nature by landing customers of various industries, and the fact that it is still growing revenue in the mid-20s proves that it has reduced its reliance on single large customers. The company now has a base of approximately 3,000 total customers, with about ~500 enterprise customers between them.

- Best of breed - Though CDN is not a new technology category, with companies like Cloudflare (NET) and Akamai (AKAM) preceding Fastly by several years (and in Akamai's case, decades), Fastly is one of the most highly regarded CDN vendors. Fastly's addition of Signal Sciences and its web application firewall (WAF) tools also flesh out Fastly's offering. The company was also recently recognized as a Challenger by the influential Gartner Magic Quadrant reviewers.

- Economies of scale - As Fastly grows, it achieves economies of scale on its CDN network. It has already started to pare down hardware spend in an effort to improve gross margins. Capex spend as a percentage of revenue is also expected to continue trending downward. As Fastly's existing customer base continues to boost usage, margins will continue to expand.

Stay long here: there's more upside left to go.

Q2 results sparked a sustainable rally

The major ace in Fastly's hand that enabled the stock to rally so sharply over the past month is a long-awaited recovery in fundamental results.

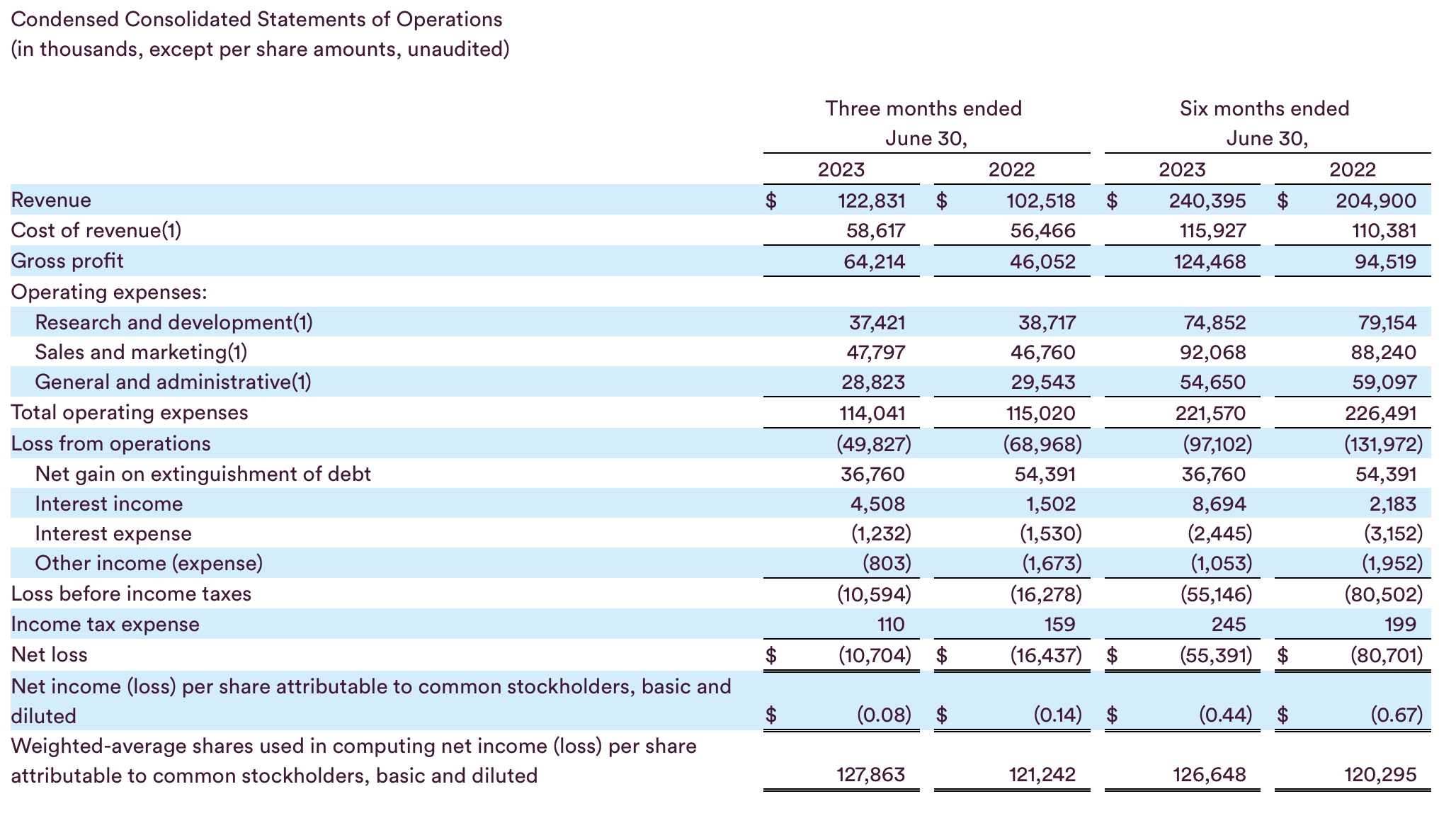

The Q2 earnings summary is shown below:

{kind=link}

Fastly's revenue climbed 20% y/y to $122.8 million in the quarter, besting Wall Street's expectations of $118.9 million (+16% y/y) by a wide four-point margin. It's worth noting as well that revenue growth accelerated substantially versus just 15% y/y growth in Q1.

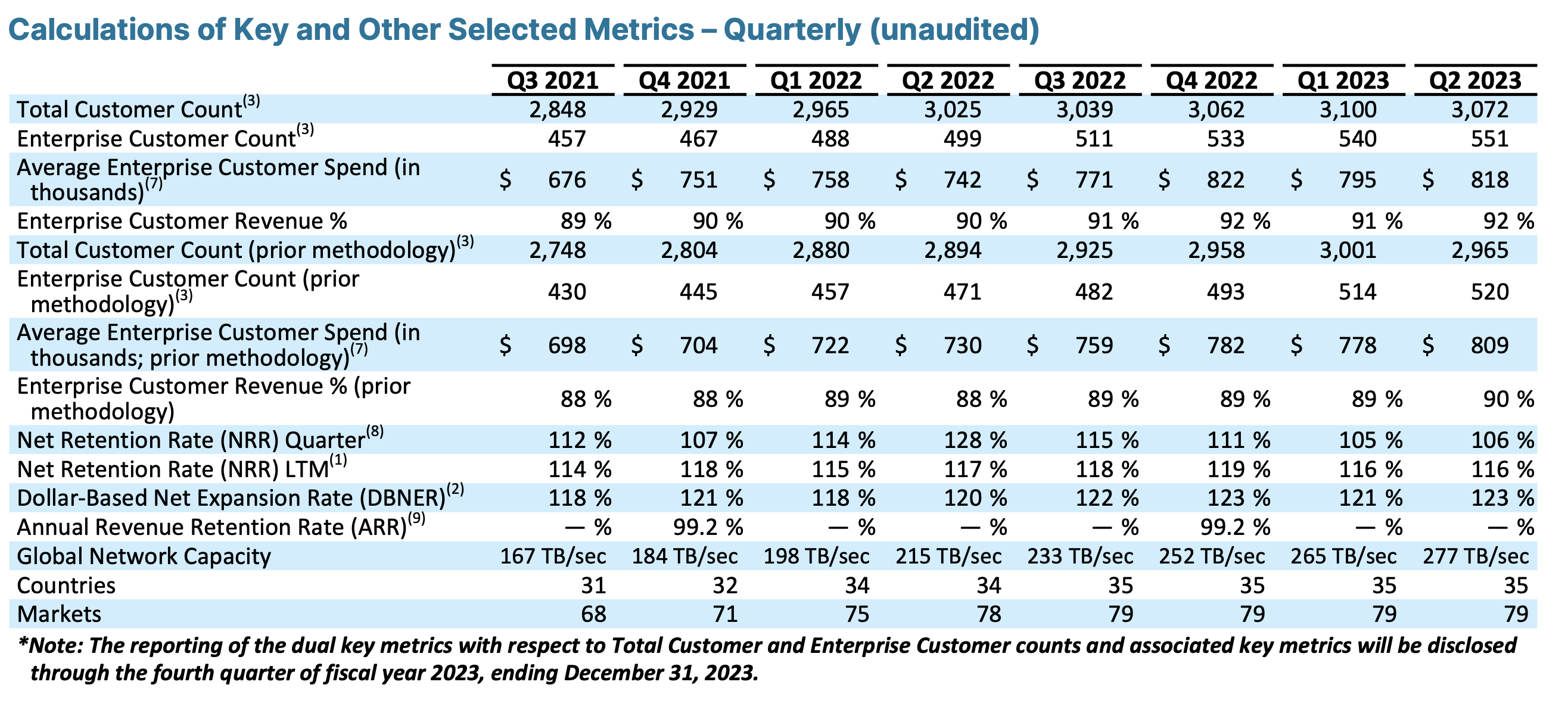

A number of factors are at play here. The company saw dollar-based net expansion rates tick back up to 123%, up two points sequentially and representing a high watermark over the past three year-period, as shown in the chart below:

{kind=link}

Management attributed this increase to wallet share expansion, as well as customers' favorable adoption of the company's new pricing plans. Per CEO Todd Nightingale's remarks on the Q2 earnings call :

Our DBNER was 123% in the second quarter, up from 121% in Q1 and also from 120% in Q2 of last year. Both of these metrics are indicative of healthy wallet share gains with existing customers. Thanks to our platform's expansion, we continue to cross-sell more functionality and more traffic to our existing customers [...]

Our average enterprise customer spend was $818,000, representing a 3% quarter-over-quarter increase as well as a 10% increase from Q2 of last year. We've seen continued wallet share expansion with customers as we've aligned our teams to be more focused on customer success and expansion [...]

We introduced our new pricing and packages for Fastly's portfolio, including flat-rate pricing and tiered packages, making it easier for customers of all sizes to try, buy and use Fastly's platform. The reception from our customers has been incredibly favorable so far."

The company has also landed 11 net-new enterprise customer wins, ending its enterprise customer base in the quarter at an all-time high of 551. Note that the slight reduction in total customer counts to 3,072 is due to customer consolidations. And as previously noted, Fastly has seen particular strength in the retail space this quarter, landing 9 net-new retail clients.

Profitability also shone. Note that gross margin expanded 620bps y/y to a pro forma level of 56.6% (also up 100bps sequentially) driven by economies of scale on the company's substantial fixed-cost investments.

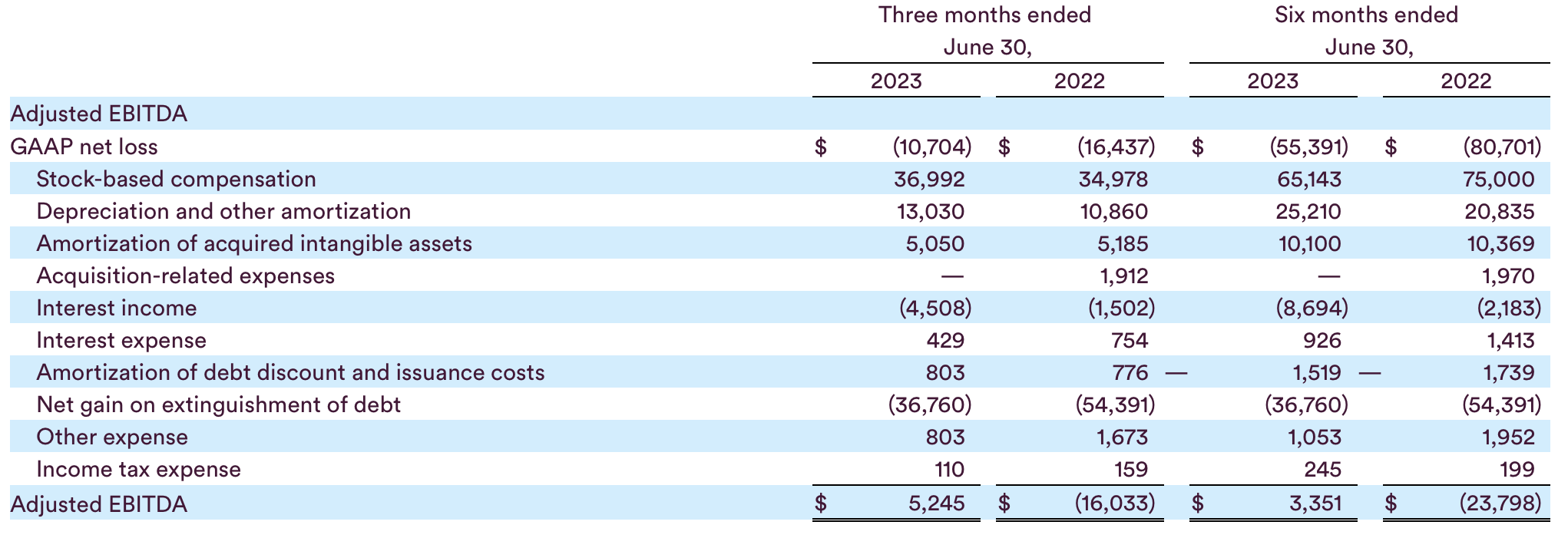

Adjusted EBITDA, meanwhile, swung to a gain of $5.2 million, or a 4.2% margin - a substantial win over a -15.6% margin in the year-ago quarter.

{kind=link}

Note, however, that the company acknowledged $3.4 million of a one-time tax benefit recognized in G&A expenses (worth 2.8% of margin) that is non-recurring. Still, even absent this benefit, Fastly would have generated positive adjusted EBITDA.

Valuation and key takeaways: Hold on until the high $20s

At current share prices near $23, Fastly trades at a market cap of $3.01 billion. After we net off the $475.3 million of cash and $472.4 million of debt on the company's most recent balance sheet, its resulting enterprise value is $3.00 billion.

For next year FY24, Wall Street analysts are expecting Fastly to generate $586.3 million in revenue, up 16% y/y. Taking these estimates at face value, Fastly trades at 5.1x EV/FY24 revenue.

Now, a word of caution here: in its heyday in 2020-2021 when a pandemic-fueled market poured money into all manner of internet stocks, Fastly was able to command a mid-teens multiple of revenue - but now, with high interest rates abound and Fastly's own growth rates having moderated, I think it will be challenging for Fastly to even reach a double-digit revenue multiple again.

That being said, I do think Fastly has room to glide up to at least 6.0x EV/FY24 revenue, representing a price target of $27 and ~16% upside from current levels.

Monitor this position and don't get too greedy, even while momentum is on Fastly's side: but hold on until the high $20s for further upside.

For further details see:

Momentum Is Now On Fastly's Side