ASAN - monday.com: A Better SaaS Stock But Still Too Expensive

2023-10-04 10:27:58 ET

Summary

- monday.com displays impressive revenue growth, achieving quarterly rates ranging from 40% to 75% in the past five quarters, outshining the competition.

- monday.com boasts financial stability, with a solid balance sheet, no debt, and approximately $990 million in cash and cash equivalents, providing room for strategic investments and innovations.

- However, concerns arise regarding heavy sales and marketing spending potentially fueling growth artificially, lower R&D allocations in the evolving AI landscape, and the significant portion of non-operational income affecting earnings.

- The stock's extremely high valuation, including a 2024 P/E ratio of 127 and optimistic 2025 projections, makes it challenging to justify as an investment.

monday.com (MNDY), a prominent player in the realm of productivity software, exhibits several noteworthy attributes that might distinguish it from competitors such as Asana (ASAN) and Atlassian (TEAM). With a trajectory that suggests imminent profitability, commendable revenue growth rates, far above the industry, and impressive customer retention figures, monday.com might appear as a better SaaS stock among the competition. Furthermore, its financial standing is robust, devoid of debt, and supported by a substantial cash reserve.

However, delving deeper into the company's financials unveils a more nuanced narrative. While its growth is undeniably robust, it relies heavily on sales, and a closer examination of earnings, discounting interest income, portrays a less optimistic scenario. Furthermore, the company's valuation appears extremely expensive, with a 2024 P/E ratio (non-GAAP) soaring to a staggering 127, a figure that is difficult to justify. Considering these factors, monday.com might still not be the best investment choice in the near future.

The good: monday.com demonstrates solid performance, overshadowing the competition

monday.com has been on an impressive revenue growth trajectory, outshining its competition over the past few quarters. Despite the economic slowdown and global uncertainties, the company has managed to achieve quarterly revenue growth rates ranging from 40% to a staggering 75% in the last five quarters. Moreover, looking ahead, monday.com is expected to sustain this remarkable growth, with estimates suggesting annual revenue growth of at least 30% over the next four years. These figures not only showcase that the company's strategy is working, and its product is in demand but also position it favorably compared to its competitors, as monday.com consistently surpasses companies like Asana or Atlassian in revenue expansion.

Moreover, monday.com exhibits promising signs of financial stability when compared to its peer, Asana. Notably, monday.com is much closer to achieving profitability, already having positive earnings on a non-GAAP basis, a milestone that Asana has yet to reach. This places MNDY in a potentially more secure position for investors seeking companies on the brink of financial sustainability.

Furthermore, monday.com maintains a competitive edge with its impressive net dollar retention rate of 110%, surpassing Asana's rate of 105% in the recent quarter. This means that the company is not only keeping its current customer base but also generating higher additional revenue from upsells, cross-sells, or expansion within those existing customer accounts, which in short means the customers like MNDY's offerings.

Finally, we must mention MNDY's impressive balance sheet. With no debt and a solid cash position on the balance sheet, investors can be everything but sure that the company will be able to sustain its operations without running out of cash before achieving actual GAAP profitability.

Hence, at the end of FQ2 2023, MNDY had approximately $990 million in cash and cash equivalents. This financial stability provides the company with a strong foundation, minimizing financial risks associated with debt obligations and ensuring ample liquidity for potential growth initiatives or strategic investments. For instance, with this cash, the company could hypothetically cover its quarterly R&D expenses more than 20 times, which gives it room to experiment with innovations, like AI tools. To compare, Asana had about $530 million in cash and cash equivalents, while spending more than $80 million a quarter on R&D.

The bad: The quality of earnings was not particularly strong, and the valuation remains challenging to justify

Despite the positive points outlined above, it is still hard to recommend MNDY as a buy.

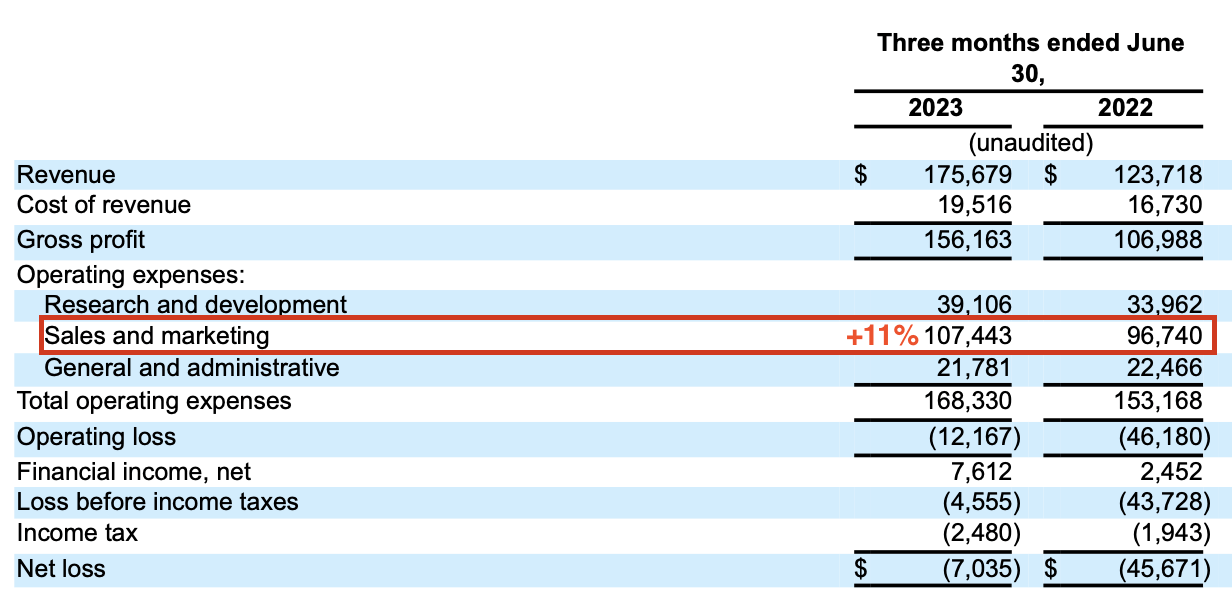

monday.com's financial performance comes with some notable caveats. While the company shows impressive revenue growth, it spends significantly on sales and marketing, a trend that continues to rise. For instance, the company increased its sales and marketing expenses by 11% in the recent quarter from about $96 million to about $107 million, In contrast, Asana decreased these expense categories by about 13% from $110 million to $96 million, while still maintaining solid revenue growth. monday.com's aggressive spending raises questions about whether the growth is somewhat artificially fueled, relying more heavily on marketing rather than organic demand.

{kind=link}

Furthermore, monday.com allocates about half the budget to research and development compared to Asana, which, while potentially cost-effective, may pose challenges in the rapidly evolving and expensive landscape of AI-driven tools. As AI becomes increasingly important, it's crucial to monitor whether monday.com can keep up with innovations. For instance, Asana's AI tools appear more comprehensive, offering a potential advantage in providing advanced functionalities to users, which might be a key consideration in the competitive tech market.

It's also worth noting that MNDY's earnings picture becomes even less favorable when we subtract financial income, primarily driven by interest income. Without this financial boost, the net loss per share nearly doubles for FQ2 2023, shifting from $0.15 to $0.30. This highlights that a significant portion of the company's reported earnings is derived from non-operational activities, which slightly dims MNDY's profitability profile.

Then comes the question of valuation, and similar to Asana, which I consider too expensive, MNDY's valuation is still difficult to justify. With a staggering non-GAAP 2024 P/E ratio of 128, the stock is trading at an exceptionally lofty valuation, which may not be warranted even in light of its high revenue growth rates.

Looking ahead to 2025, the P/E projections remain notably optimistic, with an expected 91% earnings growth for that year. Despite this robust growth estimate, the P/E ratio for 2025 remains elevated at 67, indicating that the stock's valuation might remain excessively high even if the company expands its earnings significantly, which leaves no margin of safety for years to come. Moreover, when compared to similar companies in the industry, MNDY's price-to-sales (P/S) ratio is nearly double that of Asana and on par with Atlassian, even though Atlassian boasts a higher level of profitability. Therefore, the stock remains overvalued in my view, despite its high revenue growth and the appearance of performing better than some of its competitors.

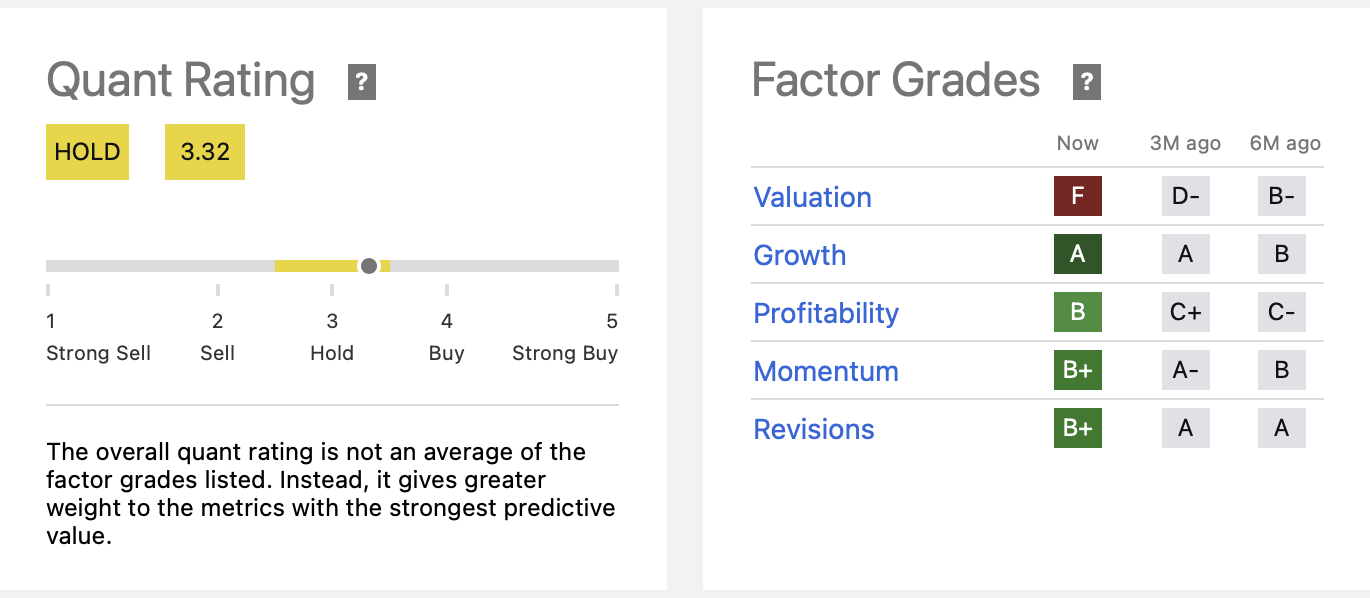

Notably, Seeking Alpha Quant rating gives MNDY an extremely low F grade as well.

{kind=link}

Key takeaways

To sum up, monday.com does look like a better SaaS stock, compared to some of its competitors, like Asana or Atlassian. Despite economic challenges and global uncertainties, the company has achieved remarkable quarterly revenue growth rates ranging from 40% to an astounding 75% over the past five quarters, much higher than the competition. MNDY's net dollar retention rate surpasses that of its competitors, indicating customer satisfaction, and its strong balance sheet offers a strong foundation for future endeavors.

However, there are notable drawbacks to consider. Heavy spending on sales and marketing, coupled with lower investments in research and development, raises concerns about the sustainability of MNDY's growth and its ability to innovate, particularly in AI. Additionally, a significant portion of reported earnings comes from non-operational activities, impacting profitability. The key concern remains the stock's exorbitant valuation, with a 2024 P/E ratio of 128 and optimistic 2025 projections, offering little margin of safety. These factors make it challenging to recommend MNDY as an investment, necessitating caution for potential investors.

For further details see:

monday.com: A Better SaaS Stock, But Still Too Expensive