ASAN - monday.com: Execution As Pristine As Its Balance Sheet

2023-09-14 08:30:00 ET

Summary

- I will share the key variables that will drive monday.com Ltd.'s growth in the decade ahead.

- I leaned on my recent consideration of Axon to fully articulate the value of these platforms and their multi-product structures.

- MNDY's multi-product strategy and comprehensive platform ecosystem have driven exceptional sales growth, even in a challenging software sales environment.

- Both businesses have successfully fielded multiple products that serve as distinct paths to go to market while simultaneously linking those products into a comprehensive, compelling ecosystem, akin to Apple's "Walled Garden" ecosystem.

- This combination of distinct, compelling products that have been vertically integrated into monday.com's differentiated architecture/platform will serve to drive the exceptional growth we've seen from the company as of late, despite the immense headwinds the software industry has faced.

Understanding monday.com

With those that I serve in the world of equity research and business analysis, I often share that we own:

- Category-defining platforms that possess massive cash hoards, little, if any, debt, quality cultures, robust free cash flow (profitability), and long runways for growth.

And monday.com Ltd. ( MNDY ) ("Monday") fits this description perfectly.

As of today, the business has ~$1B in cash, no long term debt, very robust free cash flow (26% free cash flow margins in Q2 2023), growth of more than 40%, and a long runway for growth still ahead.

Additionally, Monday has demonstrated that it possesses a culture that can successfully and efficiently launch new product offerings, which thereby compounds growth for the overall business, the precise metrics for which we will explore later on.

Instead of one product generating $1B of sales by 2033, Monday has demonstrated that it possesses the cultural aptitude to launch a series of billion dollar products. This aptitude is usually a defining characteristic of the best public market businesses, e.g., Salesforce ( CRM ) or Amazon ( AMZN ) or Apple ( AAPL ).

Below, I detailed the four principal frameworks we employ to select the businesses we own. Monday actually fits into multiple categories quite well. I will discuss Monday with you in each relevant framework.

- Vertically integrated product; capture market share in stagnant mature industry: We target businesses that have created a fully vertically integrated product, within a fragmented, low NPS, and mature industry, whereby that vertically integrated product offers 10x better value; therefore, it captures significant market share rapidly. [Notably, Monday's platform has become more and more vertically integrated, as it's added MondayCRM, MondayDev (for developers), and its app marketplace products in addition to its core work management product, all of which sit atop Monday's proprietary, open, and configurable architecture. It's a true, vertically integrated work operating system, which, with the creation of MondayDB is more scalable than ever, the evidence of which can be seen in the company's enterprise customer growth, which we'll review later.]

- Businesses that will execute a leveraged recapitalization in the coming years or are extremely disciplined with capital allocation via routine, robust share repurchase programs: We've explored the leveraged recapitalization framework in the past. [Examples here include Chipotle, Meta, and, in the past, Google or Apple .]

- Quality cultures that breed innovation within the larger conglomerate: We've often explored the Spawner framework (I'm working on a different name), which entails a company's ability to launch, or spawn, new successful business/product after new successful business/product, creating a nucleus of explosive, compounding sales growth. This is the idea that a business creates a culture in which its employees create new products successfully. With multiple products growing rapidly simultaneously, the business overall grows more rapidly and more durably. Some of my favorite examples that fit within this framework are Axon ( AXON ), Monday ( MNDY ), and MercadoLibre ( MELI ). Indeed, many of our businesses possess this incredible cultural structure, and that is why we've chosen to own them.

- Growth through quality, moat-building acquisitions: Lastly , we've explored the capital allocator framework by way of an exploration of Meta's ( META ) business, whereby a very large business materializes through prudent and judicious uses of shareholder capital, i.e., acquiring quality businesses and growing them over time within the larger conglomerate. Meta has acquired Instagram and WhatsApp, both of which have solidified its global monopoly.

Notably, many of the businesses we own possess shades of two or more of these frameworks.

As of today, Monday has not made any acquisitions; however, with ~$180M in annualized free cash flow and ~$1B in cash and no debt, there's a high likelihood that the business makes "sales and profit growth"-accelerating acquisitions in the future.

Going Multi-Product

As I listened to Monday's Q2 2023 earnings call , I was continually reminded of the business of Axon.

In my recent review of Axon, I detailed the idea that Axon has a series of products that are all connected within one ecosystem. That is, Axon has multiple products that it can use to sell to many different buyer personas, i.e., different customer prospects. While they are all connected, creating a compelling Walled Garden Ecosystem (embedding moat, locking in customers), they are all also distinct and can be sold as such. This duality allows Axon to both sell to more prospects and lock its prospects into its ecosystem once it's wedged itself into their wallets/businesses/agencies, which fuels value creation for the business and shareholders.

The combination of having both multiple products to sell and having an ecosystem in which multiple products connect to each other in a compelling way that creates huge value for customers is what continues to drive the exceptional growth at Axon (Axon has continued to grow above 30% despite the fastest interest rate hiking cycle in American history).

Similarly, Monday has seemingly defied gravity (interest rates create gravity for valuations and sales growth rates) by continuing to report 40%+ quarterly sales growth, while its software peers have seen their growth rates collapse in fairly dramatic fashion (for instance, AWS' growth rate fell from 40% to 12% in the last 18 months or so).

For both Axon and Monday, I believe it's the unique configuration of their businesses that has made this possible. We could define this unique configuration as follows:

- Organically create multiple compelling products that can be sold to different buyer personas/prospects. For instance, perhaps a prospect already has a Body Cam product. Well, Axon has a software suite, a vehicle/fleet camera, an industry-defining Taser, a drone product, and more that it could offer to the prospect. The prospect may ultimately say yes, choosing to buy one of those other products, resulting in Axon wedging into the customer's wallet/business/agency. From there, Axon could delight the customer with its initial wedge product and, over time, demonstrate the value of that wedge product within its entire, vertically integrated, comprehensive "Walled Garden Ecosystem." The customer may start with one product, then, seeing the value of the entire ecosystem around that product, choose to lock themselves into Axon's Walled Garden where they believe they could receive more value. Similarly, a prospect may not want Monday's work management product, but that same prospect may buy Monday's sales CRM. From there, Monday could delight that customer with its sales CRM product and, over time, demonstrate the value of that initial wedge product within its entire, vertically integrated "Walled Garden Ecosystem," which includes an app marketplace, a work management product, and a developer product, all atop a configurable and scalable platform architecture.

- Importantly, the combination of multiple products and the Walled Garden Ecosystem that those products create is what creates the nucleus of growth and value creation, and Monday and Axon have very masterfully executed this business model. Twilio ( TWLO ) needs to take notes!

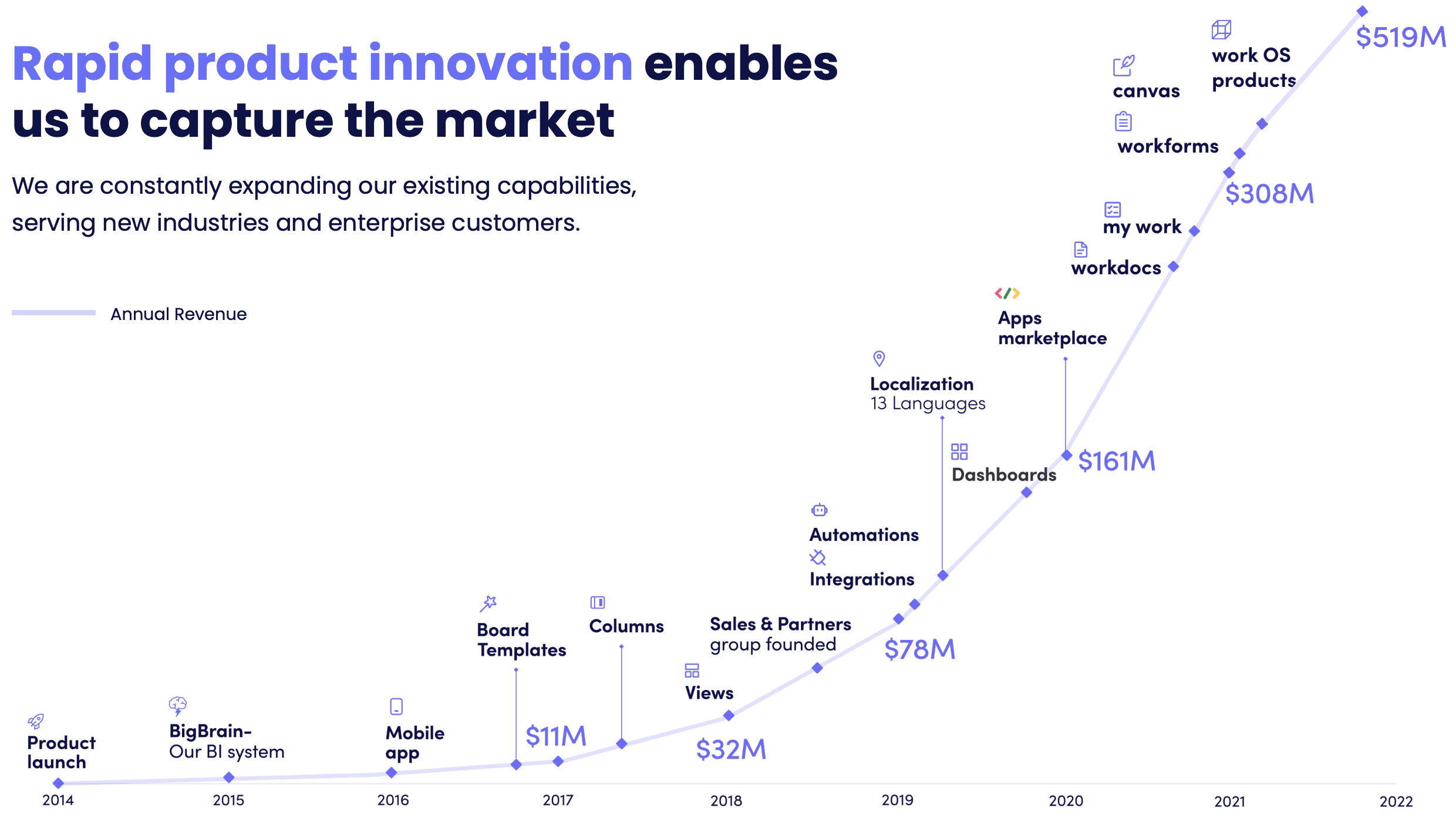

An Illustration Of Monday "Going Multi-Product"

{kind=link}

Growth Of Monday's New Products

{kind=link}

Sustained, Very Robust, Profitable Sales Growth Created By Multi-Product Platform And Sales Motion

{kind=link}

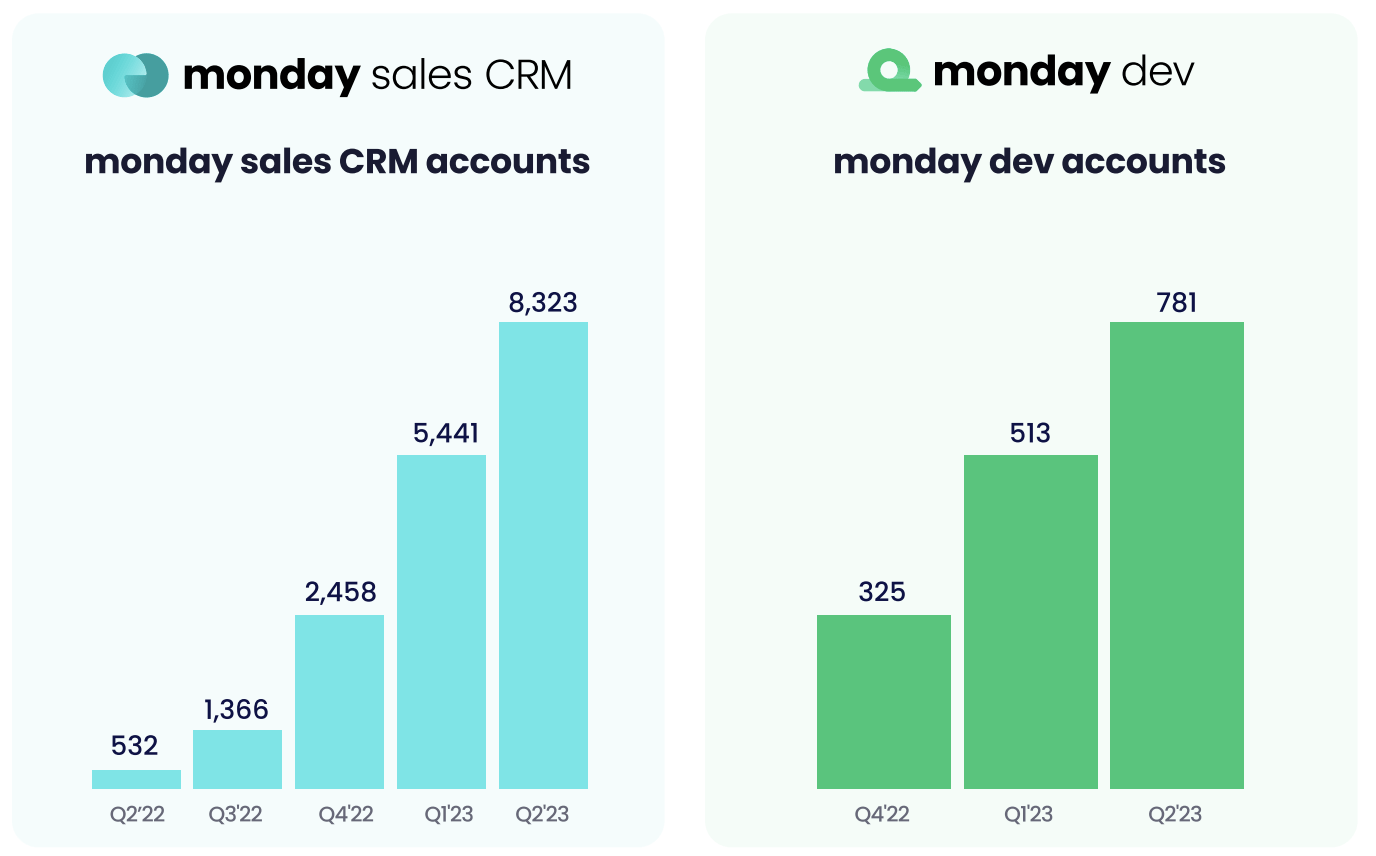

As Roy mentioned, we remain focused on our multi-product strategy and ensuring that our products can successfully enable cross-functional collaboration for our customers. Monday Sales CRM is now available to approximately half of our customers, and we continue to see strong demand for the product. We are committed to continuously elevating our sales CRM product with best-in-class features.

Monday's multi-product business model has been central to my ownership of the company, as it aligns with my key investing frameworks detailed for you earlier.

On this subject, I found management's commentary from Monday's Q2 2023 earnings call insightful.

Arjun Bhatia: And then I want to touch on the new products again because it seems you're getting a lot of good adoption on Dev and CRM, both from new customers and cross-sell into the base. If I look at the 1,600 customers that you -- that have kind of cross sold from work management, I mean there's quite a few that have just adopted CRM or Dev net new.

[Arjun is noting that Monday is selling its new CRM and Dev products independently, creating a wider top of funnel for new customers that Monday can "wedge" itself into and, hopefully, over time, sell more products to and, hopefully, over time, lock those customers into its Walled Garden Ecosystem, thereby creating robust embedding moats for the platform, resulting in durable long term free cash flow for shareholders.]

And so the question, I guess, is how do you think about Dev and CRM becoming a top of funnel landing point for customers and then cross-selling the other way into the work management platform? Is that an opportunity that still out there? Or have you seen those 8,000-plus customers adopt your work management platform already?

Eran Zinman: So I think you made a great point. Obviously, those products are more new than the work management product. So we are more focused on seeing how existing customers can move from work management to CRM or Dev. But one thing that we're really focused on from the very beginning was to make those products also a substantial go-to-market for us as a company. That was our initial focus.

So definitely, going forward, we'll see accounts moving from CRM to work management. And going back to our strategy, I think it really helps us as a company in two ways.

One, really extends our go-to-market. So instead of having just one, which is work management. Now we have multiples of both CRM and work management.

But also, it allows us to have a greater ACV for customers. So you can buy customer, but the potential revenue, potential expansion is not limited only to that specific vertical, but to have mutual products on top of that.

So I think that creates a big opportunity for us in terms of go-to-market. And going forward, we'll see the other way around people moving from CRM to work management as well.

Monday Q2 2023 Earnings Call (emphasis added).

Financial Analysis

I wanted to begin my review of Monday's Q2 2023 with the previous section's discussion because I believe Monday's financials cannot be genuinely understood without first understanding the mechanisms underlying the exceptional growth demonstrated below.

{kind=link}

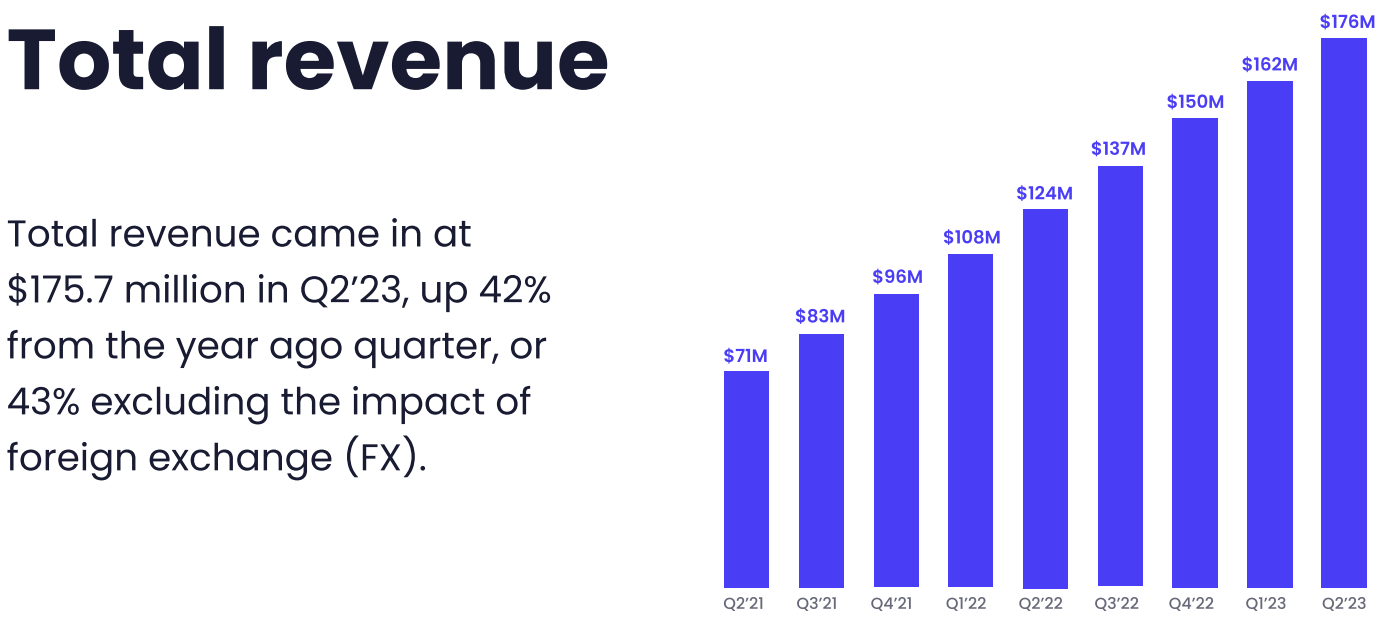

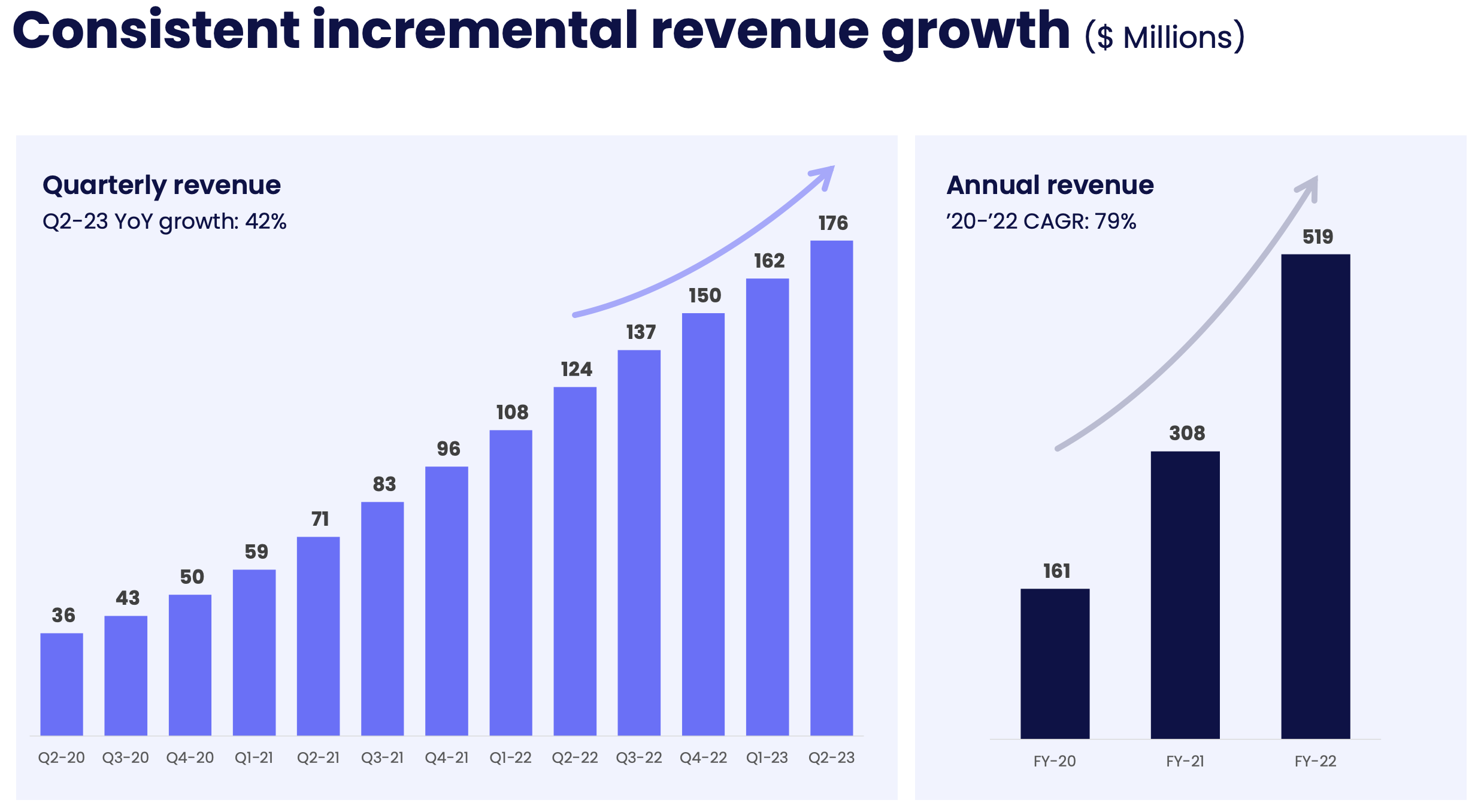

In Q2 2023, Monday grew at 42%, which is incredible growth in this environment.

I have provided you a good bit of data that illustrates how challenging this environment has been for software sales generally, with growth rates for most public company software companies collapsing.

Median Growth Rate Of U.S. Software Company

Clouded Judgment

With this as our context, Monday's Q2 2023 growth rate was fantastic, but what was more noteworthy was that Monday accelerated its sequential net addition of revenue, as we can see in the chart below.

{kind=link}

As we can see, Monday actually added more net revenue Q2 to Q3 than it did Q1 to Q2, which is very impressive considering downcycle in software underway currently.

But it makes sense: Monday's multi-product sales motion and comprehensive platform ecosystem continue to drive exceptional value creation for the business in the form of rapid, sustained sales growth.

Monday's multi-product offering, despite layoffs that have occurred in a handful of sectors within the economy, has also continued to propel its net retention rate with larger customers, as can be seen below:

{kind=link}

For a company of Monday's age and size, who also serves SMBs (small to medium sized businesses) this net retention rate [NRR] is brilliant.

And, lastly, one of the reasons I sold down most of my Asana ( ASAN ) position starting at $140/share and then again at $45/share (after originally buying at ~$20/share), and instead focused on Monday, was because Monday demonstrated to us that it had a superior culture of execution.

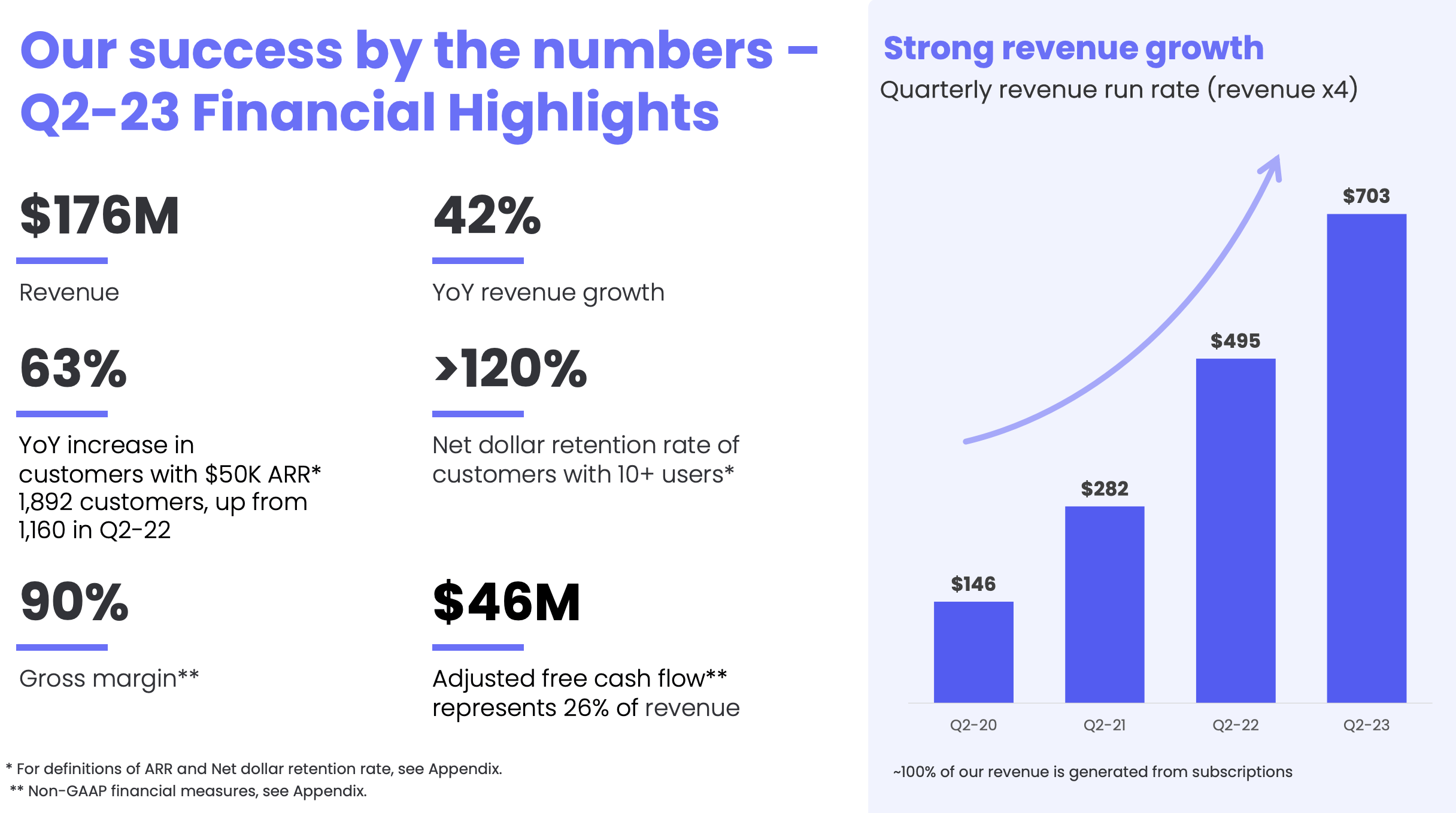

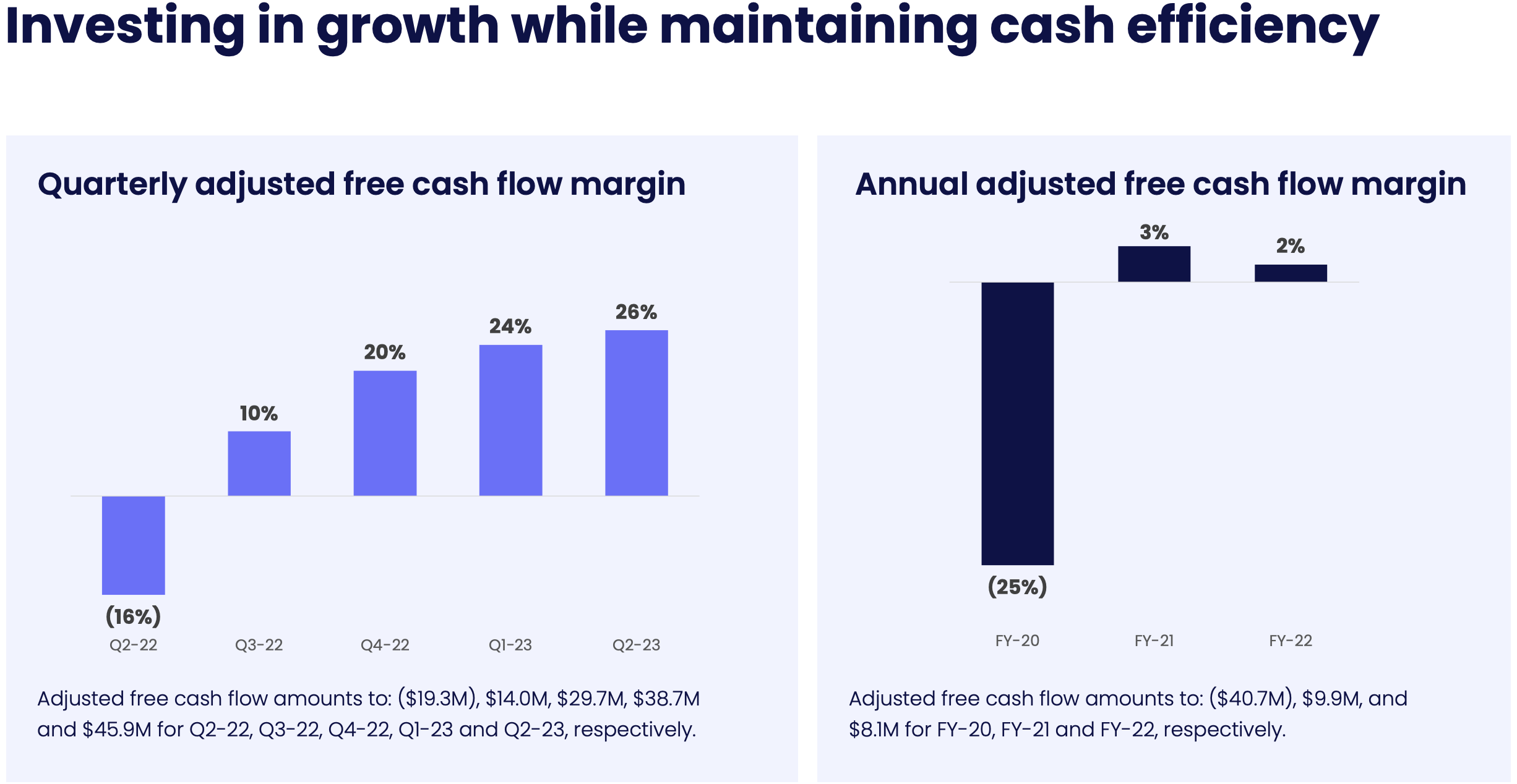

As a result of this superior culture of execution, Monday has produced incredibly robust free cash flow margins (it brings in a lot of cash each quarter on to its balance sheet), as can be seen below:

{kind=link}

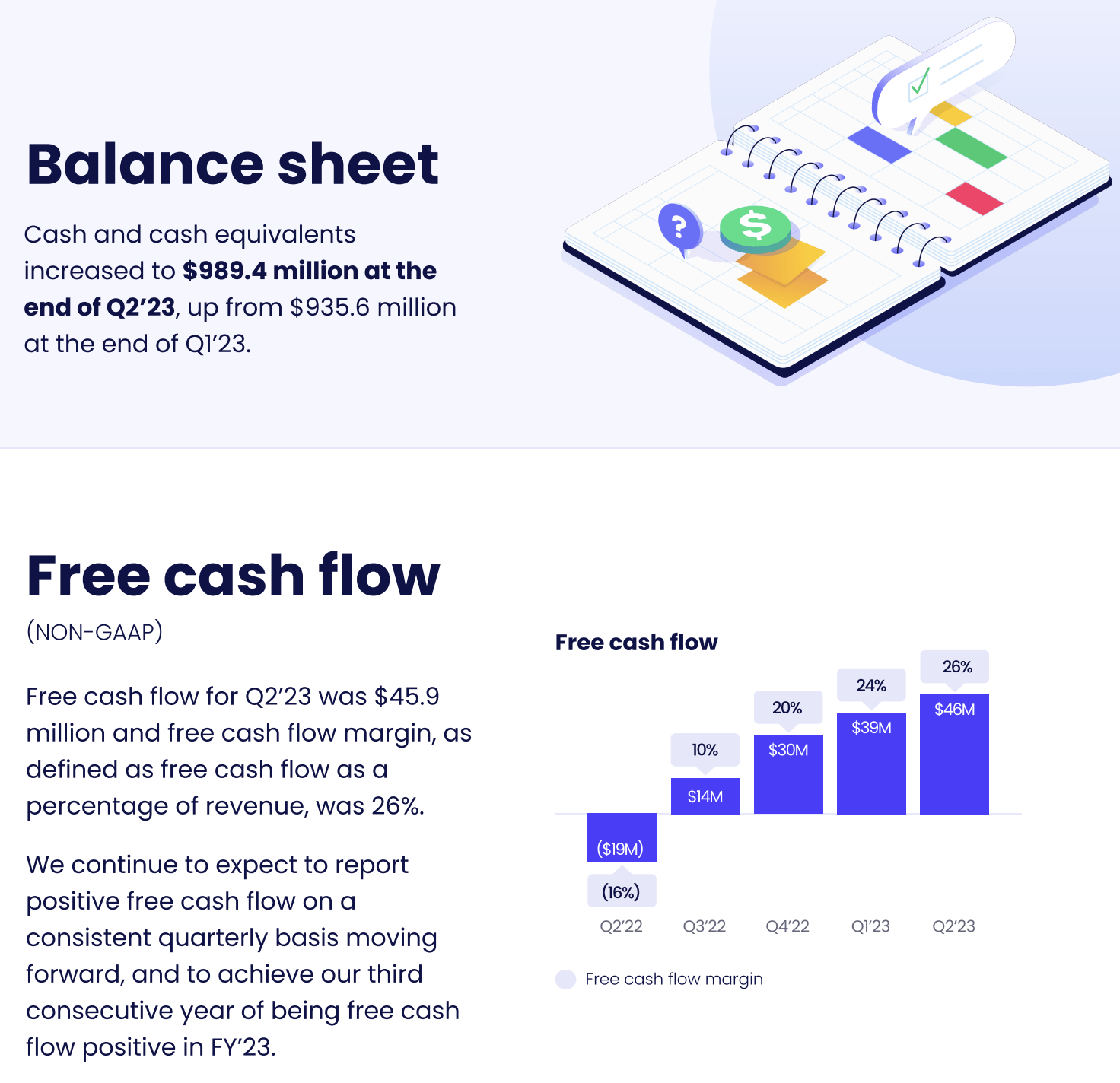

And this has served to create a hulking nearly $1B balance sheet , alongside no debt.

{kind=link}

With 26% free cash flow margins, 40%+ growth, $1B in cash and no debt, and a very long runway ahead for growth, Monday is an exceptionally financially sound business.

MondayDB: Further Vertical Integration

For those who have been curious, MondayDB will not compete with general purpose databases on the market.

It will serve strictly as underlying infrastructure for Monday's comprehensive Work Operating System platform.

This quarter, we are thrilled to announce the completion and release of Monday DB 1.0 to all our accounts. This is the initial version of our brand-new infrastructure for the Work OS platform. With Monday DB customers are already experiencing large and more complex boards loading 5 times faster, enabling them to work more efficiently and handle data-intensive and complicated workflows.

Future releases of Monday DB will provide even more speed, enhancement, scalability and functionality.

Roy Mann, CEO, Q2 2023 Monday Earnings Call (emphasis added).

To further elaborate the nature of this underlying infrastructure, I found the following exchange insightful:

Derrick Wood: Got it, that's helpful. I guess just staying on product discussion. Now that you're through 1.0 of MondayDB, what's the next phase, I guess, the 2.0, can you just give us some color as to what things we should be expecting out of 2.0 and what that timeline may look like?

Eran Zinman: Yes. First of all, we have a complete timeline on our website, which we share with our customers as well. But overall, Nexa, which is the Monday DB 1.1 is going to be released in Q4. This year, the focus is going to be on large dashboards. Just as a reminder, dashboard contains data from multiple boards. So that will go through a radical transformation in terms of performance and capability.

And then we plan another minor release of Monday DB 1.2, which is going to focus on our API. Going into next year 2024, we're going to do a major release of Monday 2.0, which will be a really game changer in terms of accommodating larger and larger accounts. And we're going to focus a lot on just sheer size of databases and accommodating very large enterprise accounts. So we have a lot of releases in the pipeline, but having Monday DB 1.0 already released is, I think, the most significant part because now all customers are using a new engine and incremental releases are going to be much easier to get out in to our customers.

Monday Q2 2023 Earnings Call (emphasis added).

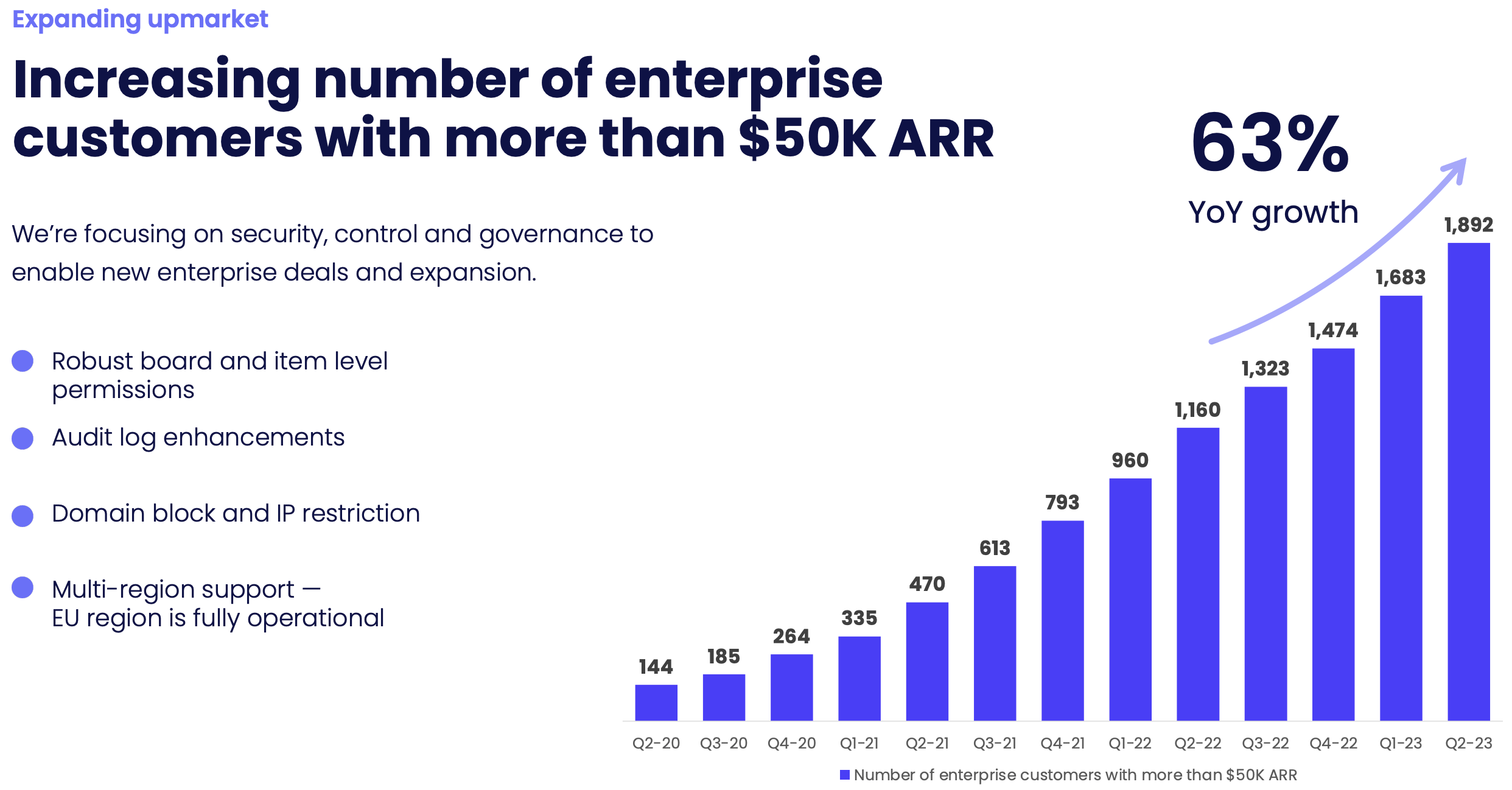

To a large degree, I believe MondayDB has been built out of necessity; in that, as it targets larger and larger enterprise customers, in order to optimally serve them, it must provide an architecture that can scale seamlessly to accommodate any size business.

Monday Continues To Grow Its Large Enterprise Customers Rapidly

{kind=link}

Monday's App Marketplace

As you know, Monday's goal has been to build a comprehensive, multi-product ecosystem; not just a work management solution.

It's demonstrated that it has the aptitude to do this, and its various products have performed well thus far.

To tie the entire ecosystem together, Monday has created a proprietary database infrastructure, which I detailed for you in the previous section, and it's also created an app marketplace native to its platform.

To elaborate the nature of this app marketplace, I found the following exchange useful:

Pinjalim Bora: I wanted to ask you about the platform itself as you were talking in the previous question mainly about the marketplace. It seems like the percentage of apps that are being monetized are kind of going up steadily. I see it about 45%. You recently launched the API version. One of your partners said it could accelerate third-party development. You are exposing the AI layer as well as the workflow engine seems like to the partners. Do you think marketplace starts emerging as a material growth driver in 2024?

Roy Mann: It's hard to say how much it will [contribute to sales] because we have our core product and the CRM, which is the main growth driver. We do believe that the marketplace will help us close larger deals . There's a lot of, like you mentioned, partners are working on it and making each of those products, more complete, more suited for long-term solutions. And so we put a lot of emphasis on the marketplace and a lot of investment and in the ecosystem. And I think it's a longer-term play rather than just like making the numbers for next year.

Monday Q2 2023 Earnings Call (emphasis added).

I believe this is a core component of the vertically integrated, comprehensive, and proprietary platform that is Monday, and I look forward to how the platform evolves from here. We've come a very, very long way in just two years, and we've done so while generating robust free cash flow and staying below our fully, fully diluted share count of 52.7M (Monday reported ~51.5M in Q2 2023).

Thank you for reading, and have a great day.

For further details see:

monday.com: Execution As Pristine As Its Balance Sheet