S - monday.com: Healthy Free Cash Flow And ~$950M Cash With No Long-Term Debt

2023-06-26 14:38:19 ET

Summary

- monday.com Ltd. is a holistic software platform that resembles a young Atlassian Corporation or Salesforce, Inc.

- It offers a variety of products, including project management, CRM, and developer tools, as well as a growing app marketplace.

- Ironically, the business operates from arguably its greatest position of strength in its history, while simultaneously trading near its lowest valuation in its corporate history (very roughly here).

- This irony is further compounded by the fact that it, as of today, sustainably generates free cash flow, which is something it did not do in prior years of its corporate history (including its years in private markets).

- Alongside this robust free cash flow generation, the company also possesses ~$950M in cash and no long term debt. Healthy free cash flow; 40%+ growth; successful multi-product execution, and a giant cash hoard alongside no debt. There's a lot to love.

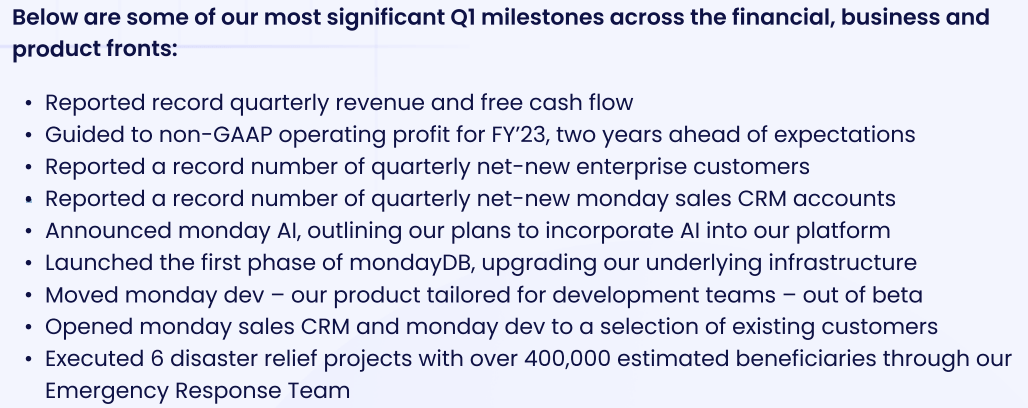

Starting With Some Highlights

While reading through the monday.com Ltd. (MNDY) (hereafter just "Monday") quarterly shareholder letter , I came across the below-illustrated quarterly highlights, and I thought that it would be a good foundation for this note.

{kind=link}

In The Greatest Irony series, which was a 12 part series I wrote and published in 2022, we spent a good bit of time exploring the business of Monday; specifically, we spent a good bit of time exploring the idea that Monday had "gone multi-product."

- The Greatest Irony 6 ( MNDY ) ( MELI ) [Wholly unnecessary for understanding the ideas presented in today's note to you on Monday, but I am sharing for those who may want even more data-based analysis following this note.]

I articulated that the natural byproduct of "successfully going multi-product" would be a "reduction in forward returns being offered."

That is, when a younger company successfully expands its product set, it naturally reduces the risk of the business; therefore, because risk has decreased, the aforementioned forward returns should naturally decrease by way of valuation appreciation .

We should expect that, as a younger company successfully finds product market fit via new offerings, the market will acknowledge this and price the business such that it offers lower returns by virtue of the business being less risky due to its diversified set of profit streams.

In order to reduce forward returns being offered, the business in question must experience valuation appreciation whereby the reduction in risk is reflected.

In TGI 6, we articulated these ideas; then revealed reality, which was in diametric opposition to our expectations based on the aforementioned set of conditions.

That is, instead of valuation appreciation, whereby prospective future returns diminish, we witnessed fairly dramatic valuation depreciation.

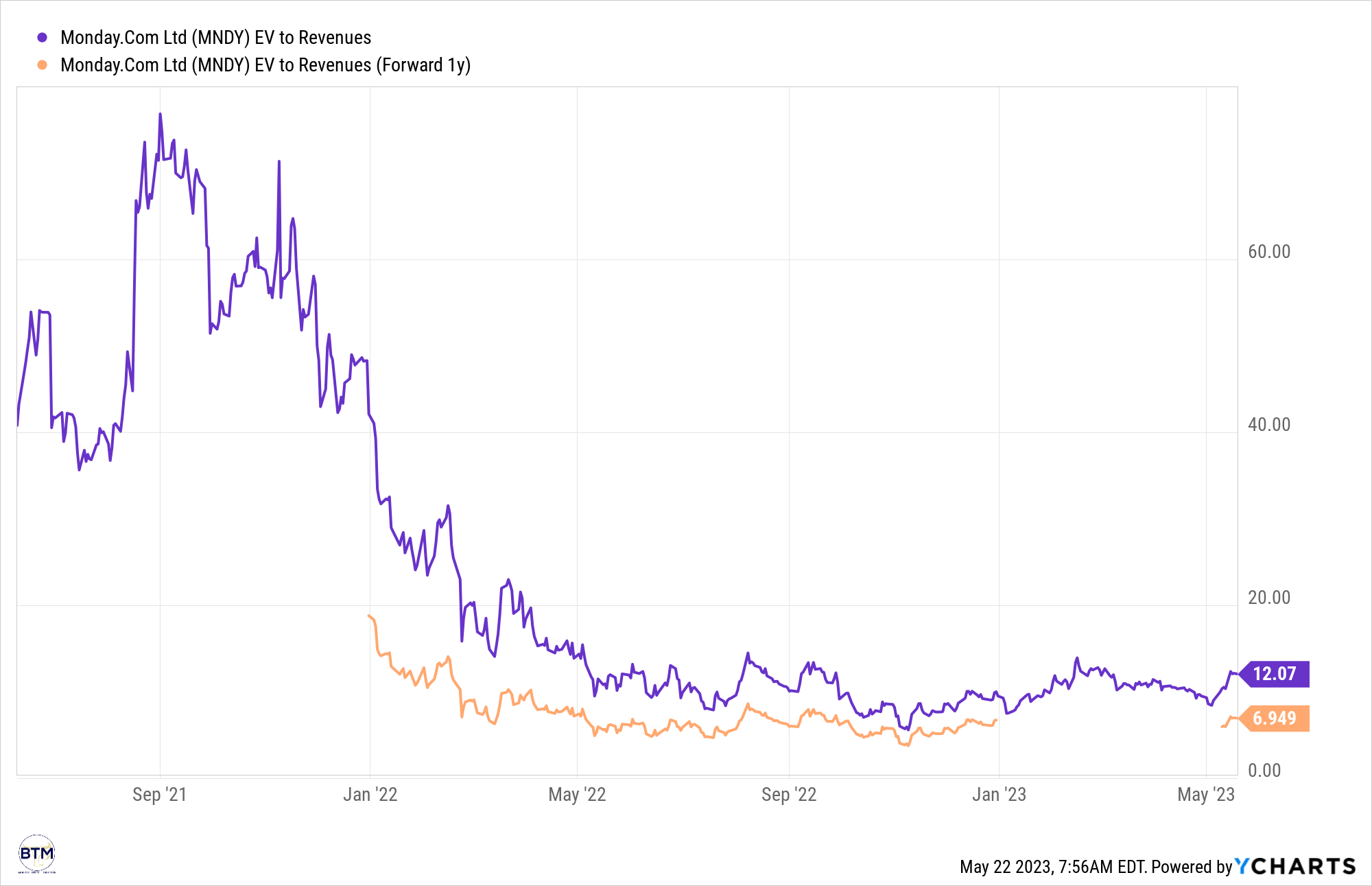

Monday's Valuation Trends Since IPO (EV/Revenues & EV/Forward 12 Mo. Revenues)

{kind=link}

I deemed this to be fairly ironic; hence, I wrote and published the aforementioned 12 part series entitled "The Greatest Irony," or TGI for short.

- Note : I understand The Everything Bubble of 2021. I understand the 2nd, 3rd, and 4th largest bank failures in U.S. history in early 2023, with the 5th teetering in the aftermath. I understand the fastest repricing of credit since 1788. I understand that these variables may override the reality that Monday is the strongest it's ever been as an enterprise. TGI series was meant to illustrate, in some sense, the nature of business evolution. It was also meant to illustrate the idea that the vast majority of our businesses operate from their greatest positions of strength in their corporate histories; notwithstanding this reality, they spent large portions of 2022 trading at their lowest valuations in their corporate histories.

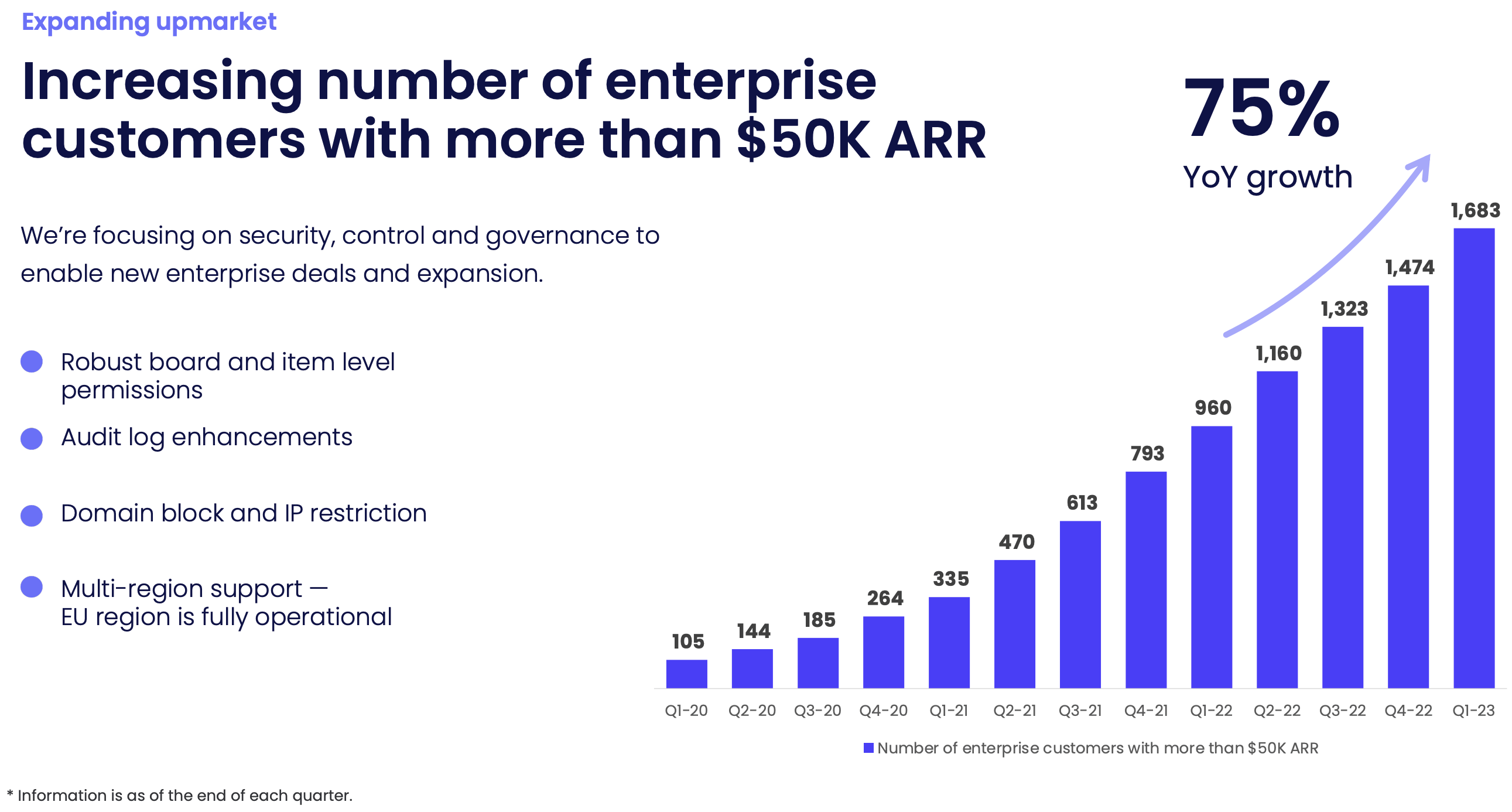

In Monday's quarterly highlights, we can see a few important developments when we consider the business through the lens of TGI framework. For instance:

- "Reported a record number of quarterly net-new enterprise customers."

{kind=link}

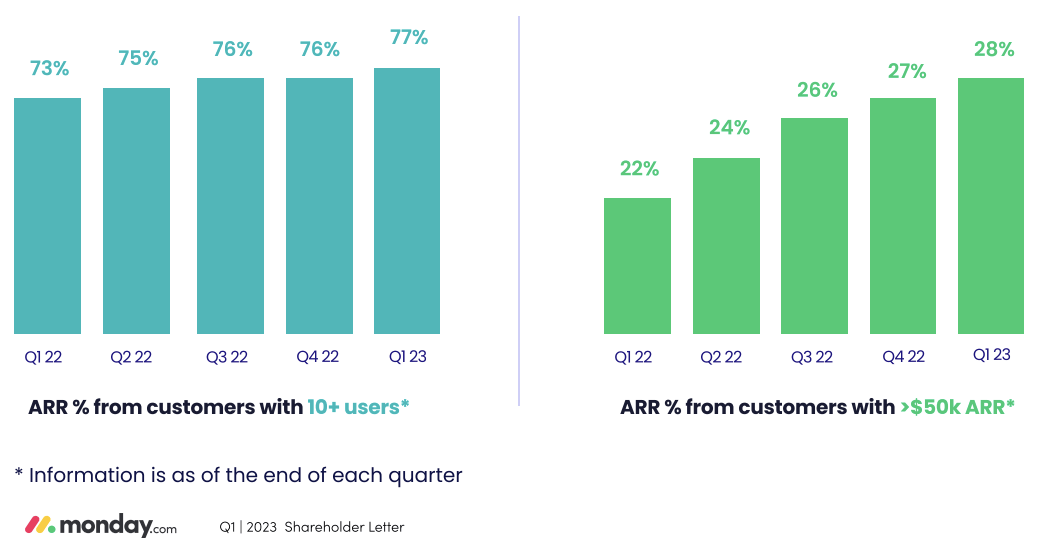

As we add more enterprise features and functionalities to our products and build out our direct sales organization, we continue to increase expansion with enterprise customers.

As of the end of the first quarter, customers with 10+ users now represent 77% of Annual Recurring Revenue ((ARR)), up from 73% a year ago. Customers with more than $50k in ARR now represent 28% of ARR, up from 22% a year ago. 59% of the Fortune 500 are now customers of monday.com , up from 52% a year ago.

This development, i.e., the growth of Monday's enterprise customers, is important because larger businesses have more resources to weather periods of economic uncertainty/turmoil, such as the one in which we currently find ourselves. Below, we can see that Monday's revenue has increasingly come from larger businesses, though, to be sure, Monday serves a very large contingent of SMBs.

{kind=link}

That said, thinking of Monday through the lens of the TGI framework, based on the price action of Monday over the last 9 months, I believe it would be natural to expect that above chart was trending in the other direction. That would be the un-ironic conclusion. But, indeed, Monday has linearly "improved" in this respect.

In addition to more durable customers, Monday's new product lines have also been performing well in recent quarters. For example:

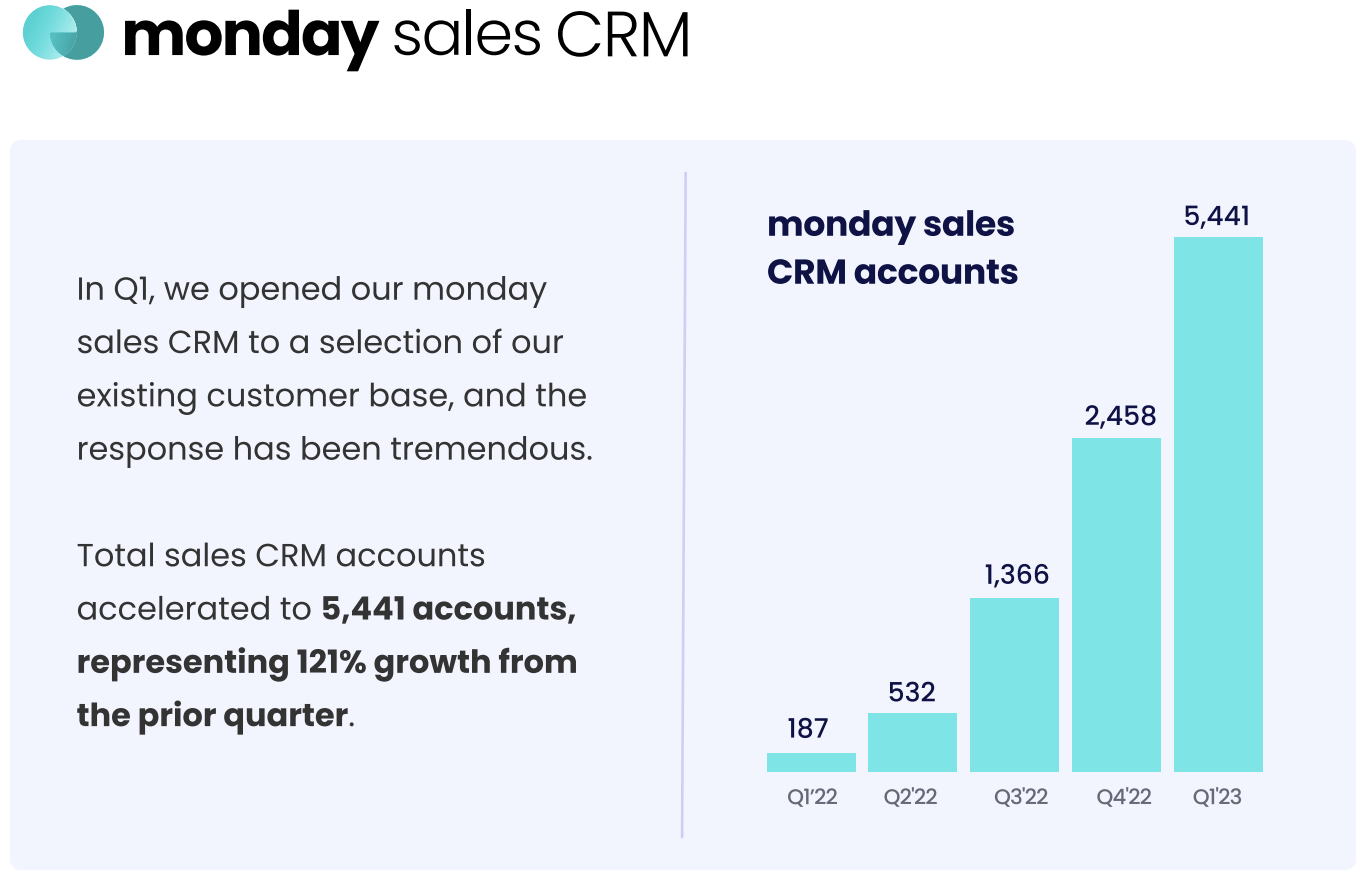

- "Reported a record number of quarterly net-new Monday sales CRM accounts."

{kind=link}

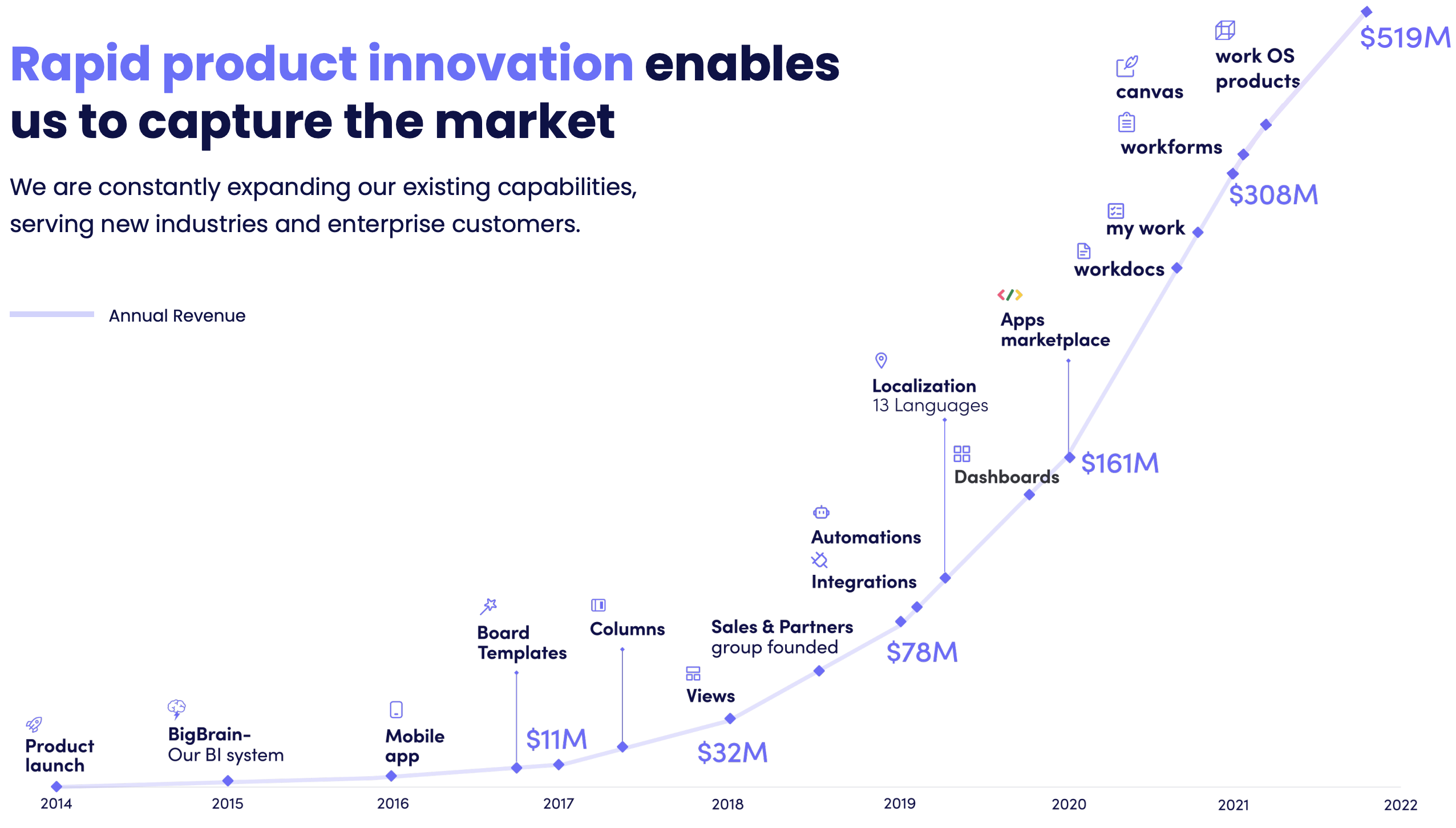

The entirety of Monday's evolution from a point solution (project management) to a comprehensive Work OS can be seen below (note TGI framework when considering the chart below):

{kind=link}

As we can see, Monday has consistently evolved its platform each year, resulting in the strongest version of itself today, with more lines of business than ever/more product offerings than ever, and with more comprehensiveness than ever.

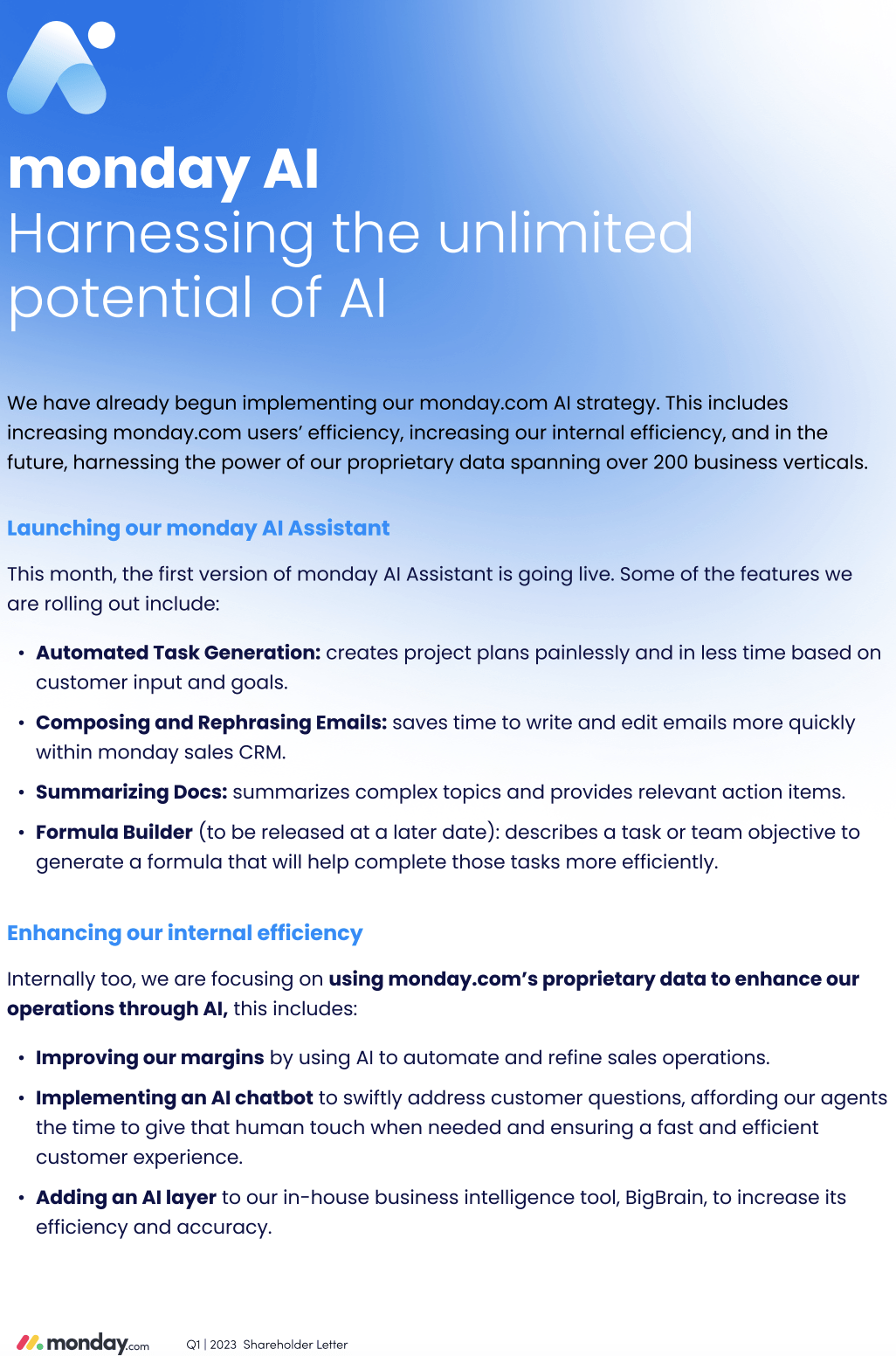

And I do not believe Monday will stop here! From the highlights snapshot with which I introduced this section, we can see further evolution underway already:

- Announced monday AI , outlining our plans to incorporate AI into our platform

- Launched the first phase of mondayDB , upgrading our underlying infrastructure

- Moved monday dev – our product tailored for development teams – out of beta.

I am quite excited to learn more about how mondayDB and mondayAI will interact in the years ahead.

To close this exploration of Monday using the TGI framework, I believe the graphics below further aid in our understanding that Monday operates from its greatest position of strength ever:

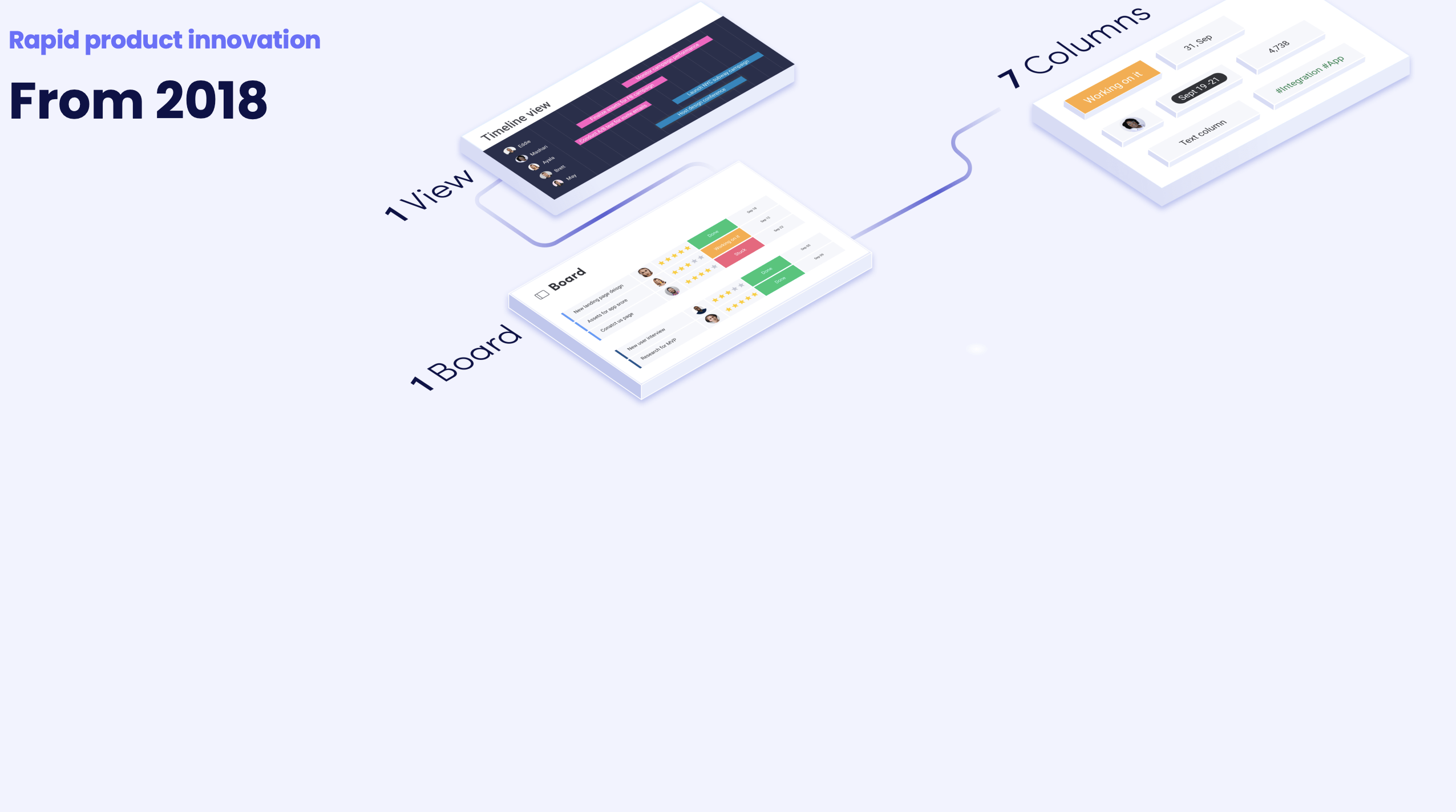

A Depiction Of The Breadth Of The Monday Platform In 2018

{kind=link}

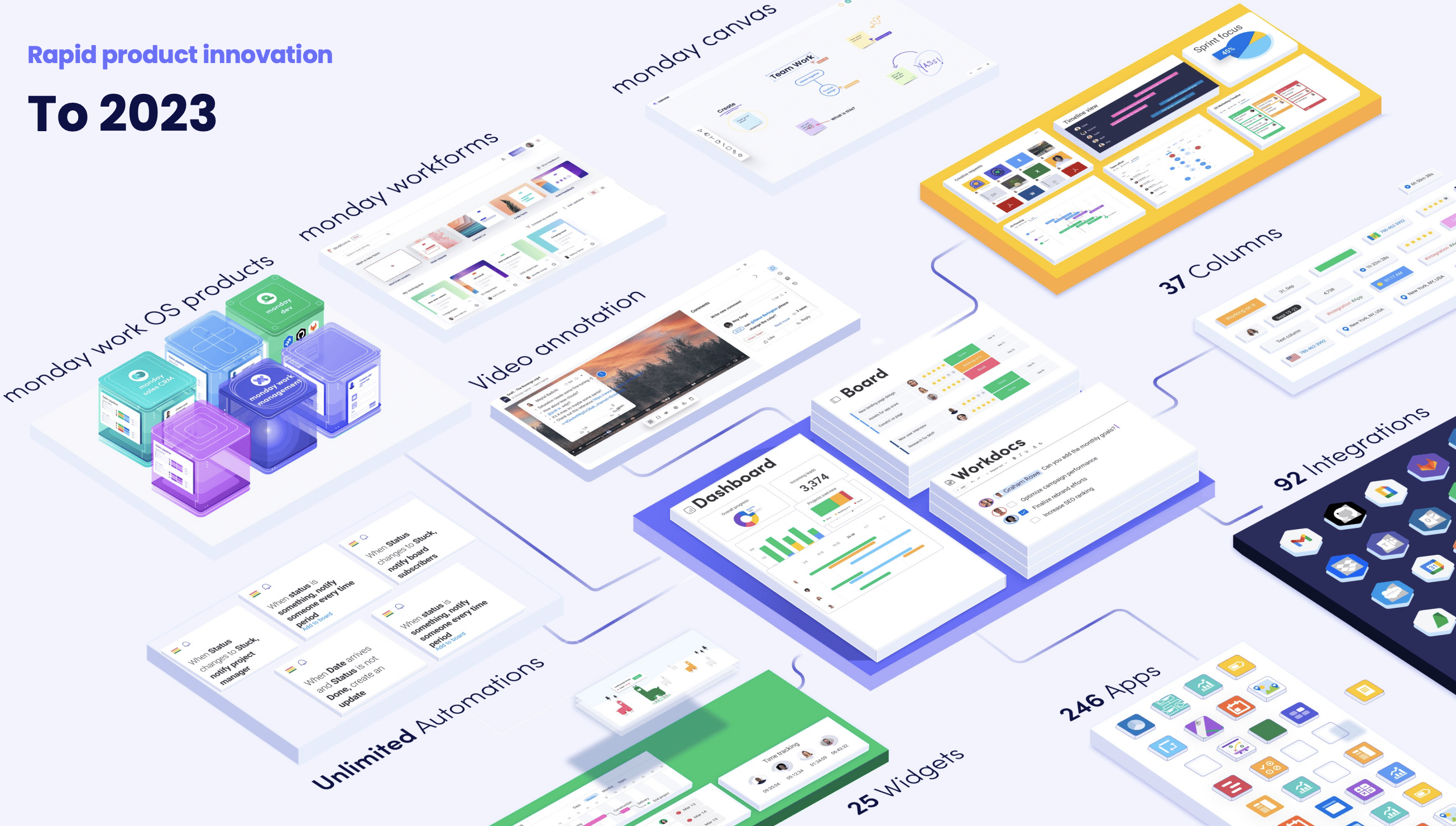

A Depiction Of The Breadth Of The Monday Platform In 2023

{kind=link}

I am looking forward to the further evolution of the Monday platform in the years and decades ahead.

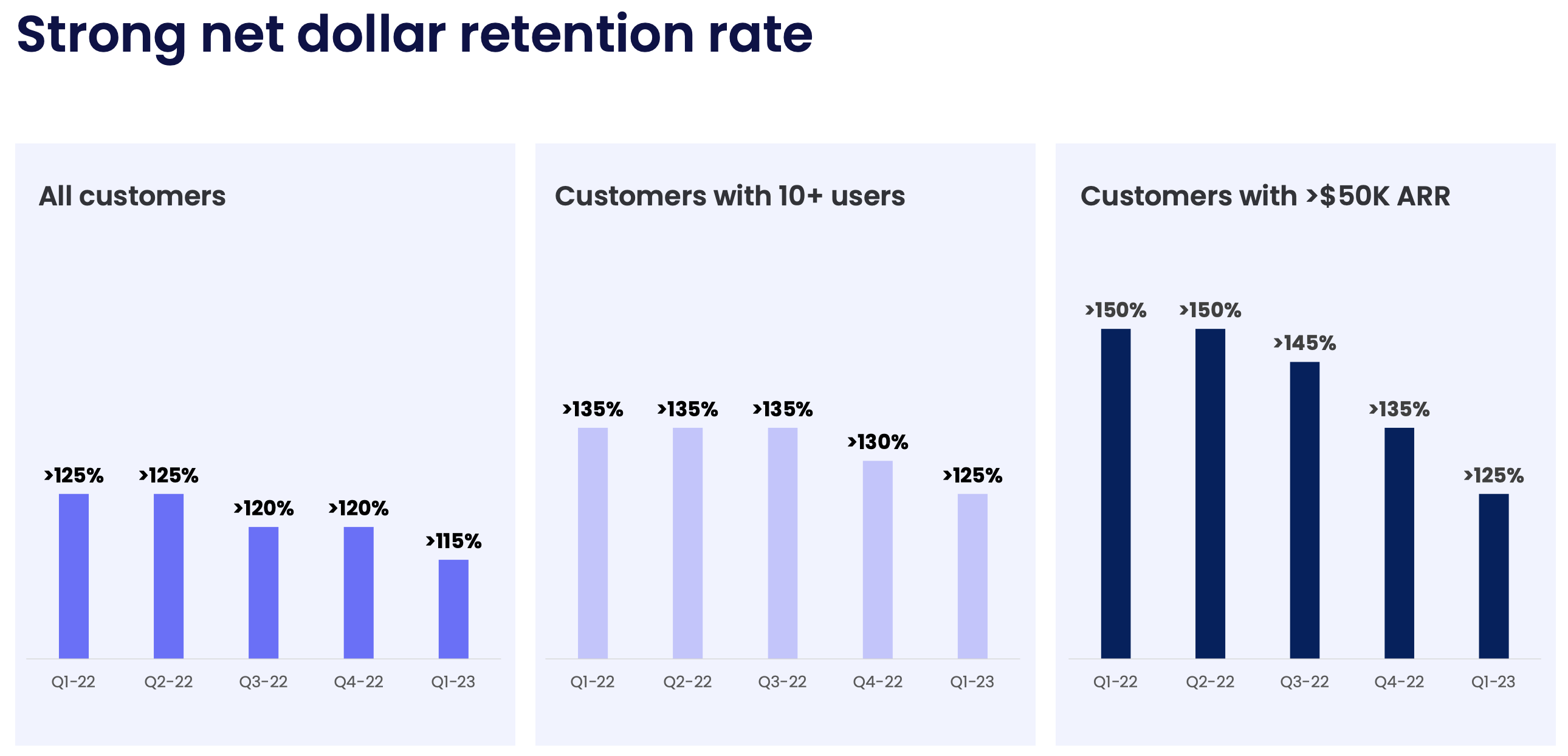

Net Retention Rate

In assessing Net Retention Rate within Beating The Market, our thinking is predicated on these ideas:

As we've shared in the past, HubSpot ( HUBS ) has been a company from whom we've learned and whom we've made a role model for our earlier stage businesses, such as Monday.

We specifically shared the lessons HubSpot taught us apropos of Monday in this note:

- The State of our Stocks 50 ( MNDY ) + Lessons From HubSpot

- If you'd rather not read that note, a quick Google search will yield great results in understanding NRR, which is a metric that is as applicable to Apple ( AAPL ) and Amazon ( AMZN ) as it is to SaaS businesses.

I would say that reading that note's section on HubSpot would be worthwhile prior to reviewing Monday's NRR. It provides substantial context for the numbers we're about to consider.

And, remember, HubSpot is one of the best software companies of all time!

Alright, with those ideas as our firm foundation, let's check out Monday's most recent NRR data!

And, below, we can see that Monday's Net Retention Rate has been falling somewhat precipitously lately; however, in light of the contextualizing data presented above, I believe Monday's Net Retention has remained quite strong.

{kind=link}

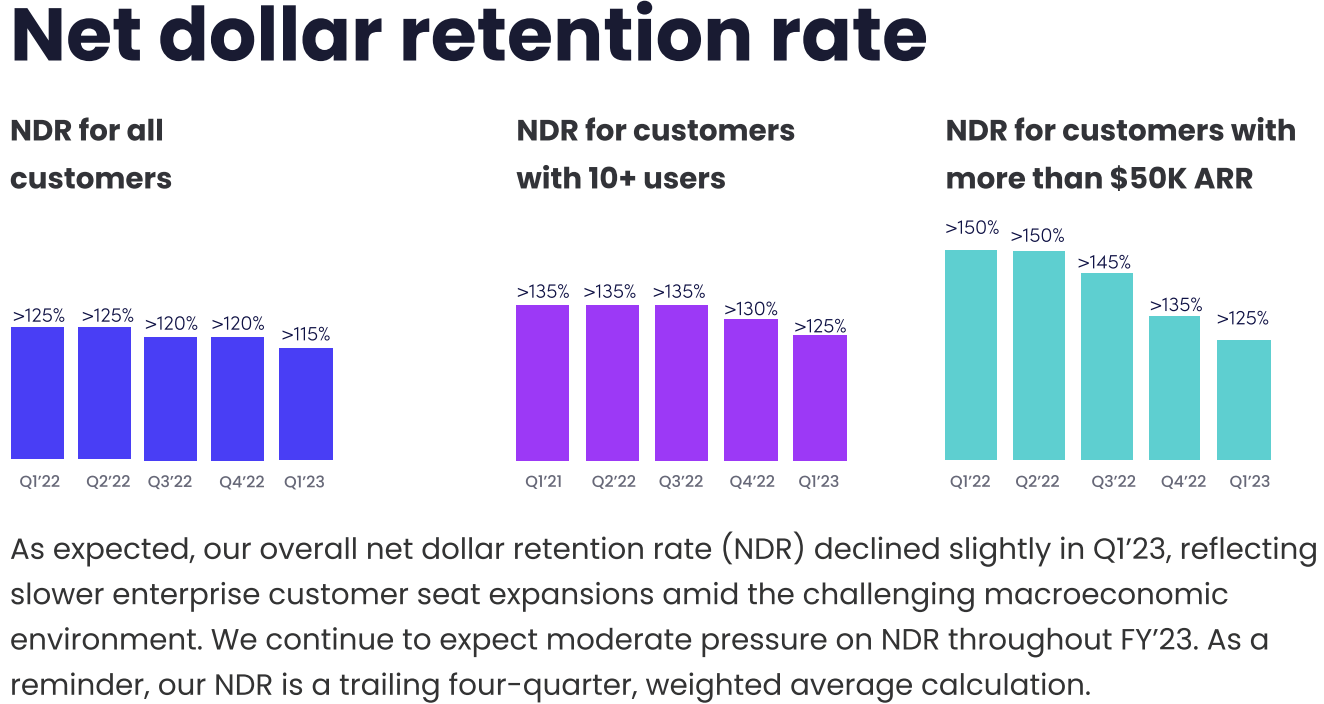

In Monday's Q1 2023 shareholder letter, the company shared the following on the subject of Net Retention Rate:

{kind=link}

Of course, we'd rather have this metric trending in the other direction, but, as we know from the lessons learned from Garena of Sea Limited ( SE ), business is often non-linear.

In closing, I am satisfied with Monday's NRR as of today.

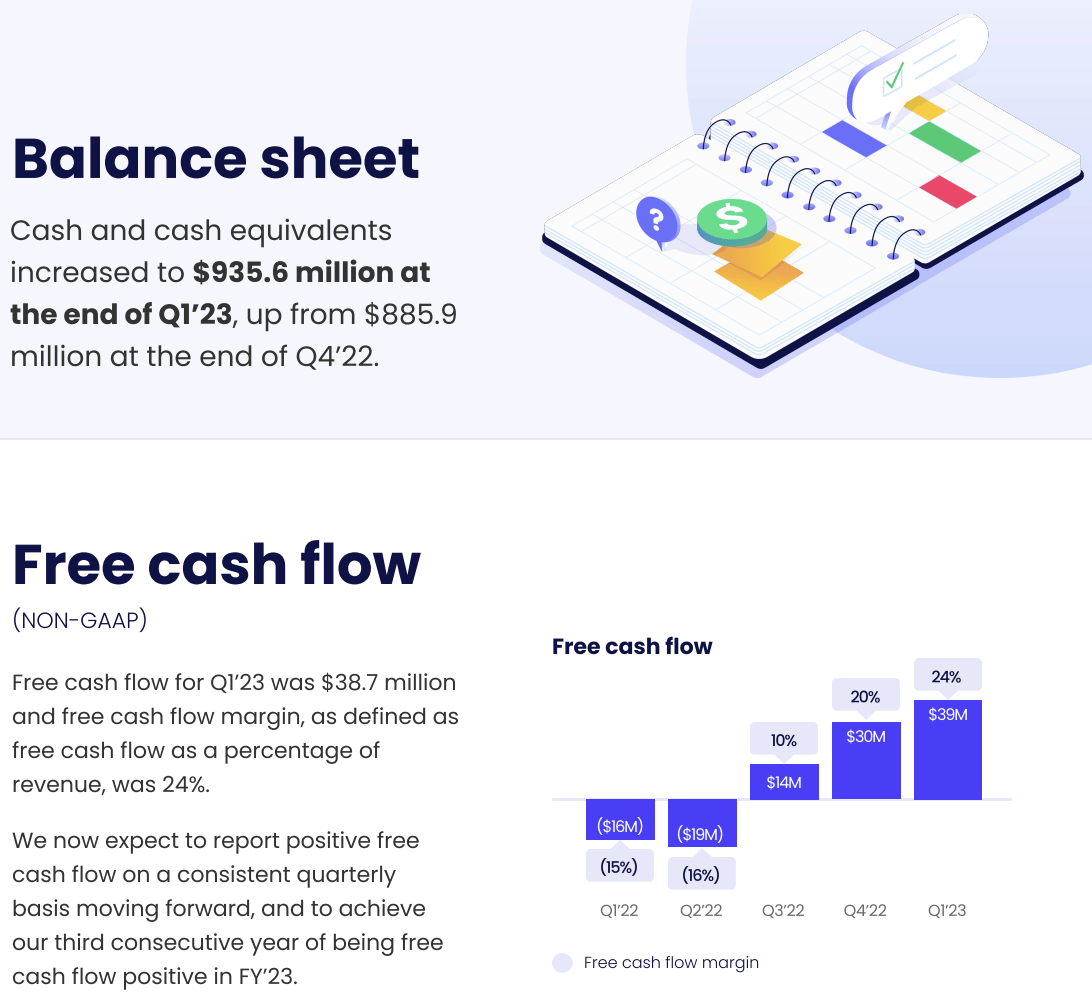

Monday's Cash Hoard

In the bullet points of this note, I shared that Monday has begun producing free cash flow sustainably, as they projected they would.

Naturally, this results in the growth of Monday's cash hoard on its balance sheet (when a company generates free cash flow, all else being equal, it adds to its cash balance).

As of today, Monday's cash hoard is approaching $1B, as can be seen below:

{kind=link}

Of course, this ~$935M in cash, alongside sustained free cash flow generation and no long term debt, is attractive; however, it's worth noting that companies like Marqeta ( MQ ) and SentinelOne ( S ) have even larger cash hoards ($1.5B in cash/no long term debt and $1.2B in cash & equivalents/no long term debt, respectively).

For all three businesses, I believe their exceptional service to their customers and their exceptional cultures are reflected in the nature of their financials.

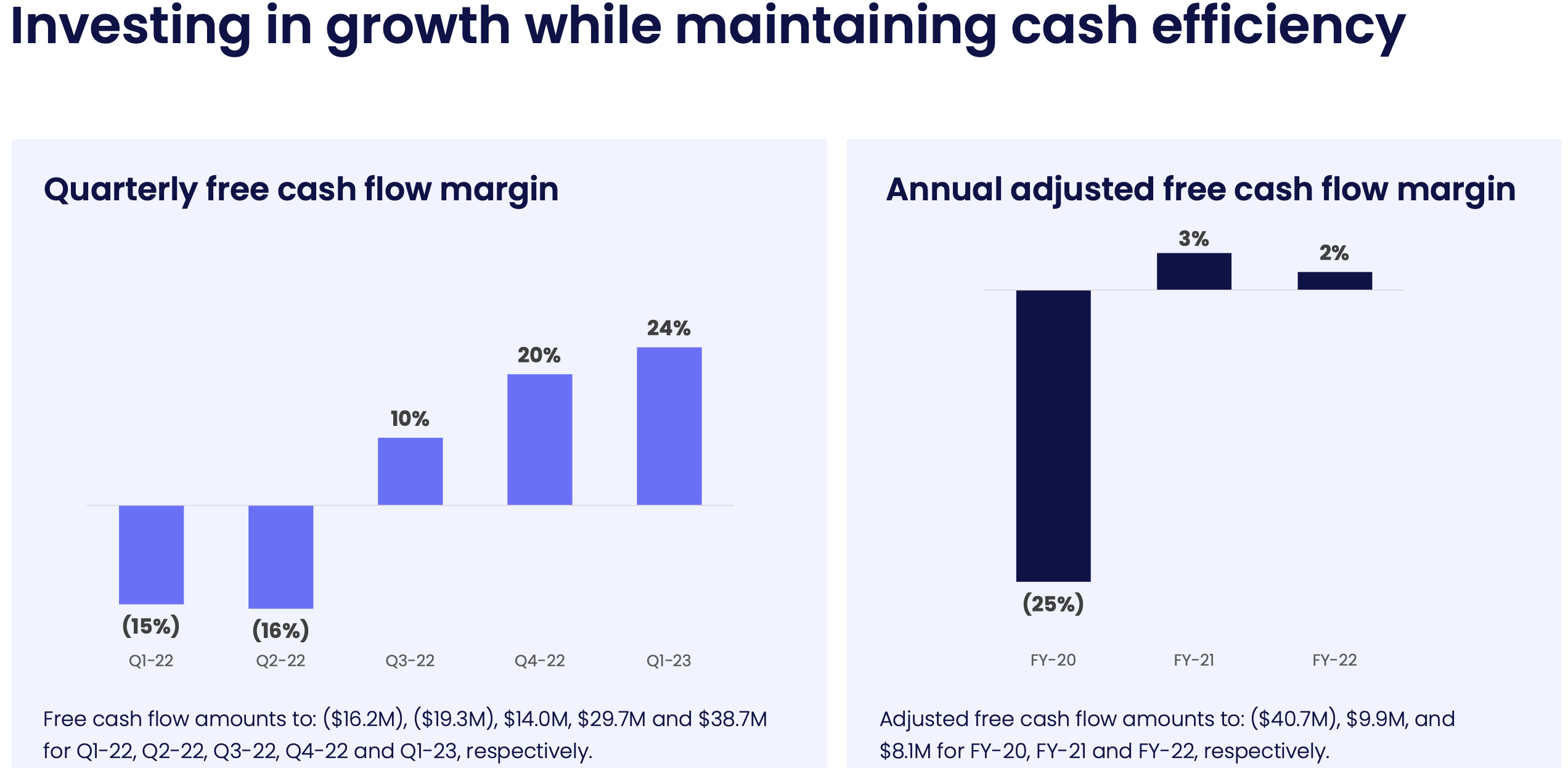

With this in mind, below, we can see Monday's expanding free cash flow margin:

{kind=link}

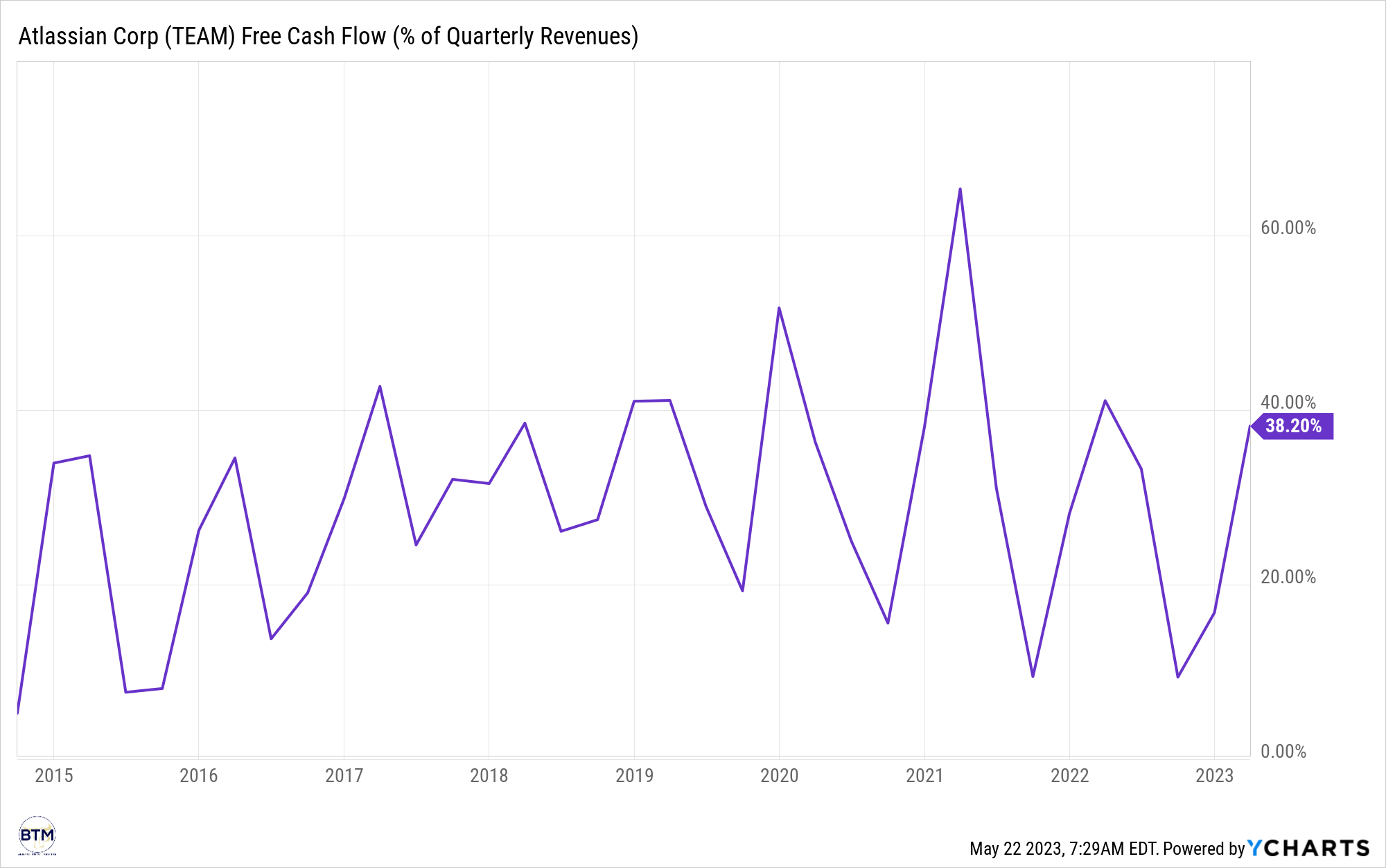

Monday's management has shared in the past that they look up to Atlassian Corporation ( TEAM ), and they plan to achieve margins that resemble those of Atlassian in the future.

Atlassian's Free Cash Flow Margin

{kind=link}

In light of Monday's recent progress, I believe management when they state that the above-illustrated margins are achievable for Monday, and, to this end, in light of Monday's growth, the business is likely much cheaper than Mr. Market may realize.

Using a long term free cash flow margin of about 30%/using Monday's TTM sales as of today (~$550M), Monday currently trades at about 40x EV/fcf.

Considering the business will likely grow at over 40% this year, I believe this is rather attractive.

To be sure, we have recently experienced the 2nd, 3rd, and 4th largest bank failures in U.S. history, following the fastest repricing of credit since 1788. This has resulted in extremely tight credit conditions, which could lead to further economic deterioration, which could impact Monday, though no one can be sure of what the macro will bring looking forward.

Concluding Thoughts: Beating The Market Has Owned And Will Continue To Own Mostly AI-Centric Businesses

To close out our time reviewing Monday's Q1 2023 report, I'd like to share a few "data points" that illustrate that Monday has and will continue to proactively implement AI infrastructure in a variety of contexts whereby it maximizes consumer surplus/optimizes its users experience with the Monday platform.

And, from Monday's Q1 2023 shareholder letter, we read:

{kind=link}

I think that a benefit of purchasing earlier stage businesses is that they have less in the way of "Value Networks" that must be restructured during periods of technological change.

We recently discussed this idea, which was popularized in the book entitled, "The Innovator's Dilemma," on the Beating The Market podcast. I linked both resources below:

- The Innovator's Dilemma

- How Beating The Market Incorporates The Thinking Of Mr. Christensen In Its Business Selection .

That said, IBM's mainframe business, while not growing, still generates fairly significant free cash flow for the business! (By which I mean that IBM's outmoded mainframe business is still producing healthy cash flow for the company, despite it becoming outmoded decades ago. I shared to highlight the idea that tech embedding moats last far, far longer than most have been led to believe.)

To this end, as Dee Hock (founder of Visa ( V )) said in One From Many, [paraphrasing] "Evolution has a gentleness about it."

As always, thank you for allowing Beating The Market to serve you in building your business of owning business

For further details see:

monday.com: Healthy Free Cash Flow And ~$950M Cash With No Long-Term Debt