TEAM - monday.com Q2 Earnings: A Buy As Customers Embrace The Platform

2023-08-14 11:23:39 ET

Summary

- monday.com Ltd.'s Q2 results beat expectations on both the top and bottom lines.

- The company's guidance, while not exceptional, demonstrates that customers are still adopting its services.

- The strong customer adoption curve, along with a favorable macro environment, supports a buy rating on monday.com stock.

Investment Thesis

monday.com Ltd. ( MNDY ) delivered Q2 results that beat on the top line (marginally) and the bottom line (a large beat). But the main headline here is monday.com's guidance. It's not an eye-watering impressive guide, but I argue that it didn't need to be.

All monday.com had to do was show that customers are still ready to use its services years after the ''digitalization'' movement began, which also happened to be the onset of the pandemic. And these outcomes unequivocally support my bull thesis.

Consequently, I continue to rate this stock a buy.

Rapid Recap,

In my previous analysis two weeks ago, as we headed into monday.com's Q2 earnings results, I said :

The results we've seen from many companies thus far into earnings season show that companies' results are looking better than feared. Moreover, IT departments are once again inclined to spend on software, albeit in a more selective manner.

Given monday.com | A new way of working's strong customer adoption curve, together with a more favorable macro environment, I argue this bodes very well for this small-cap company.

I went on to say,

Any time you see a customer adoption curve where customers are moving in droves to a platform at higher than 30% y/y, you know that is a company that has something special that makes it a growth company. There's no need to overcomplicate this insight.

With that in mind, let's discuss monday.com's customer adoption curve. As you can see below, customers spending more than $50K in ARR were up 63% y/y. That's the good news.

MNDY Q2 2023

The bad news is that his customer adoption pace is slowing down. Case in point, in the same period a year ago, monday.com's customer spending of more than $50K was up 147% y/y.

That being said, I believe that anything higher than 30% CAGR continues to reflect a thriving and growing platform.

Or to put it more concretely, revenues could be up or down, but paying customers flock to a platform for one reason only, because they see an attractive value proposition. With that in mind, let's discuss monday.com's outlook.

As Expected, monday.com's Outlook Continues to Improve

{kind=link}

In my previous analysis, as we headed into the earnings results I said:

[...] with more visibility into the end of 2023, I believe that monday.com will be well-placed to upwards revise its full-year 2023 revenue outlook.

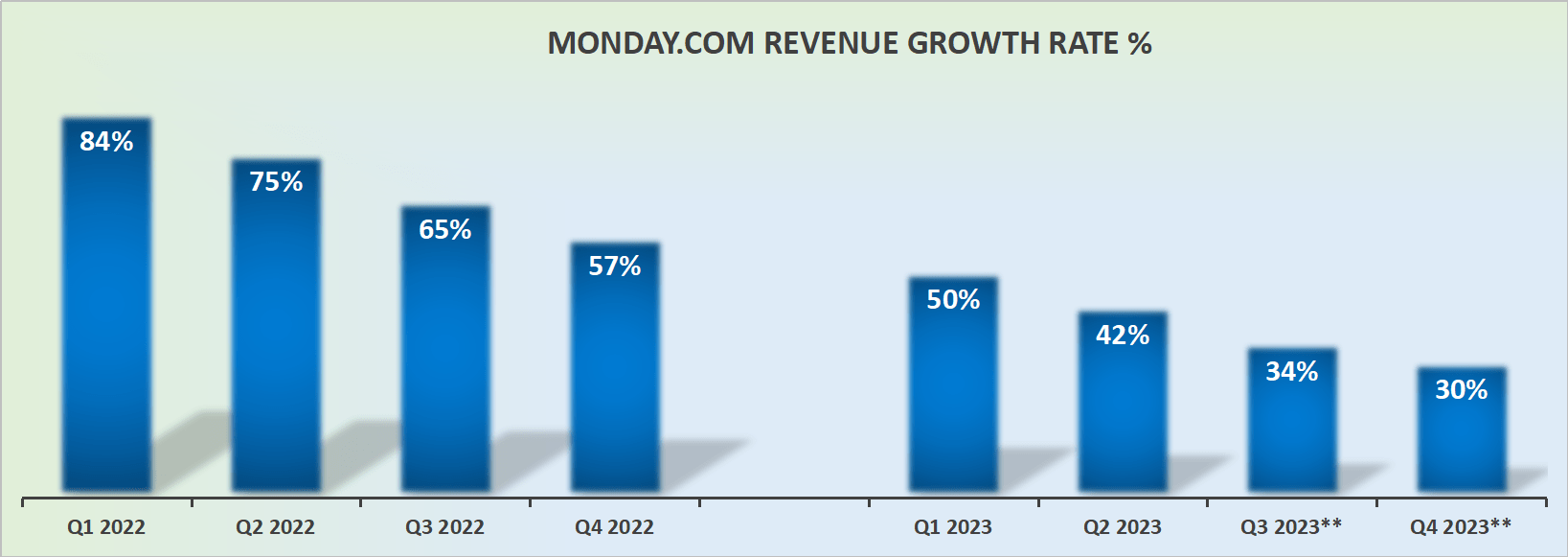

Monday.com raised its full-year outlook from 36% y/y growth rates for 2023 to 38% y/y (not shown above). This is a sufficient beat to grab a headline, but it's not too aggressive such that it leaves the company too stretched.

The takeaway here is that monday.com is still in growth mode. Of that, there should be no ambiguity. Yes, one could make the case that investor reaction relative to Atlassian ( TEAM ) had more fireworks and that in comparison monday.com's reaction has been more muted. But that's because investor expectations for Atlassian had become so gloomy. The same cannot be said about monday.com.

MDNY Stock Valuation -- Attractively Priced, ~85x 2024 Operating Profits

monday.com has more than doubled its full-year non-GAAP operating profits guidance to close to $30 million, at the high end. Needless to say, investors are not chasing monday.com for its paltry non-GAAP profitability. After all, this would leave the stock priced at around 250x this year's operating profits.

On the other hand, the fact that monday.com guided for around 4% operating margins for 2023 as a whole leads one to believe that in 2024 monday.com could be on a path towards 5% to 8% non-GAAP operating margins.

This means that at the high end of this range, monday.com could in 2024 deliver close to $90 million of non-GAAP operating profits, leaving the stock today priced at 85x next year's operating profits. This is a figure that I believe is more than reasonable, given its strong customer adoption rates and ability to continue raising its revenue guidance.

The Bottom Line

monday.com Ltd. announced its Q2 results, showing a marginal beat on the top line and a significant beat on the bottom line. However, the standout aspect is its guidance. While not exceptionally impressive, it didn't need to be.

With its strong customer adoption curve and favorable macro environment, I maintain my buy rating on this stock. Despite a slight slowdown in customer adoption pace, any growth rate exceeding 30% CAGR signifies a thriving platform.

monday.com has raised its full-year 2023 revenue outlook from 36% to 38% year-over-year growth, further indicating its growth trajectory.

Although its non-GAAP profitability is not the main driver for investors, the prospect of 5% to 8% non-GAAP operating margins in 2024 supports its attractively priced valuation of around 85x next year's operating profits, considering its robust customer adoption and continual revenue guidance revisions.

For further details see:

monday.com Q2 Earnings: A Buy As Customers Embrace The Platform