AAPL - Money Market Funds: The Next Bubble Or The Logical Alternative To Savings Accounts?

2023-05-02 08:00:00 ET

Summary

- Money Market Funds might be a good alternative to savings accounts and their minuscule interest rates.

- I prefer Money Market Funds with a portfolio of Treasuries instead of funds that hold Federal Reserve Repurchase Agreements, despite the lower interest rate.

- Money Market Funds are not FDIC insured like Money Market Accounts or Savings Accounts, but they are a low-risk way to get some return on your cash.

- I list some of the other alternatives for investors looking for cash alternatives.

Republished From Kontrarian Korner

Money Markets

One of the things I haven't written about on Seeking Alpha before is what I am doing with my cash. Money market funds aren't discussed that frequently in investing circles (stocks are way more interesting), but I think it is a relatively low risk way for investors to get a better interest rate on their short to mid-term cash holdings. While money market interest rates won’t keep up with inflation, I think it is a logical alternative to bank savings accounts, where interest rates remain close to zero.

I have seen a couple videos and podcasts on money markets and the continued inflows money market funds have seen due to the difference in interest rates between savings accounts and money markets. Money market funds recently reached an all-time high in assets under management, passing $5T in AUM in March. While I think this is a logical reaction to the minuscule interest rates of savings accounts and the issues with the banking system after Silicon Valley Bank’s blowup, some investors are worried about potential for issues created by these continued money market fund flows.

Jason Burack of Wall Street for Main Street has talked about money markets in some of his videos, where he (rightly) points to the money market bailouts in 2019 and the potential for issues created by the Federal Reserve repurchase agreements inside many money market funds. Investors who have been around since 2008 might remember when money market funds broke the buck . Most of those consequent outflows went into safer government and treasury money markets instead of finding a home in other assets. I would be surprised to see something like this happen again, but I think there are good options in money market funds for people who are tired of the near-zero interest rates offered by savings accounts.

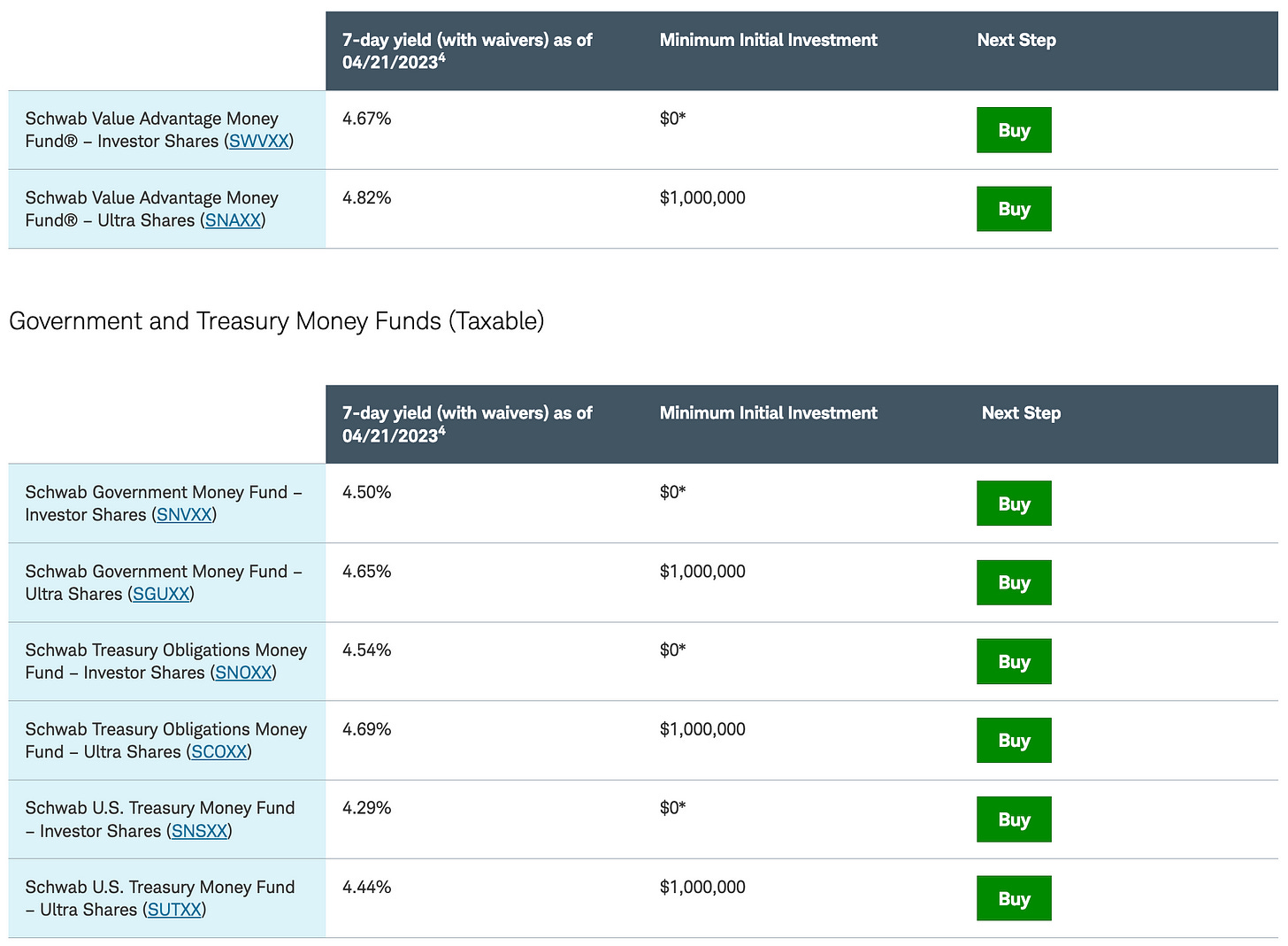

I will primarily focus on Schwab because that is where I have my cash sitting in a money market. While Vanguard money markets (VMRXX, VMFXX, and VUSXX) have lower fees (~0.1% vs. 0.34% for Schwab) on its money market funds, the main funds with competitive interest rates all have a large amount of Federal Reserve Repurchase agreements in their funds. Fidelity (SPAAX, [[SPRXX]], and [[FTEXX]]) has higher fees than Schwab, while their main money markets also have Repurchase agreements in their funds.

{kind=link}

Schwab Money Market Rates (schwab.com)

For investors that are visual learners, this is how I look at money market funds: money market funds are like meatpacking plants, and each fund has different characteristics based on the underlying portfolio. With the money markets that have Federal Reserve Repurchase agreements in them, I view it is the meatpacking plant where you can buy mystery meat. It might be cheaper and lower quality meat (i.e. higher interest rates), but you don’t know what is in there or what could happen if financial conditions deteriorate. For the money market funds that hold exclusively Treasuries (like Schwab’s ( SNSXX )), you are paying for higher quality (i.e. lower interest rates), but you are getting the equivalent of ribeyes and filets in the form of Treasuries.

Cash - Interactive Brokers

Money market funds are not insured by the FDIC, while money market accounts and savings accounts are FDIC insured up to $250,000. Money market accounts have the FDIC insurance, but they generally have lower interest rates. If you want to stay in cash, I would take a closer look at Interactive Brokers ( IBKR ). They are a low-cost brokerage (and where I have my main investment account). They don’t offer interest on balances below $10,000, but they have the some of the best rates on cash that I have seen above that amount.

{kind=link}

IBKR Interest Rates (interactivebrokers.com)

If you have seen better rates on cash, I would be curious to hear about it in the comments section below. I know Apple ( AAPL ) recently announced it was partnering with Goldman Sachs ( GS ) to offer a savings account with a 4.15% interest rate . You need an Apple Card to open it, but it could be another alternative if you are willing to open an account with Goldman Sachs and Apple.

Treasuries

While I don’t think bonds will be a good long-term investment for a couple reasons, some of the shorter-term Treasury bonds could be a good cash alternative. As a general rule, they will also have higher interest rates than money market funds. Right now, you can get a 1-year Treasury yielding 4.76%. These rates will vary depending on the maturity and what is going on in the market, but if you are willing to take the time to buy individual Treasury bonds, you will probably be able to get better yields without incurring the fees of a money market fund.

I-Bonds

I-Bonds (inflation bonds) are another alternative worth mentioning, but there is an annual limit on the amount you can purchase. You can only purchase $10,000 electronically and $5,000 in paper bonds by using your tax refund each year, for a total of $15,000. These bonds have a 30-year maturity and carry a low fixed rate, but the variable rate adjusts twice each year depending on inflation. Like the other options I have covered, these probably won’t keep up with actual inflation, but right now these bonds have the highest interest rates (6.89%) of anything I have mentioned in this post. These aren’t a great alternative for cash that you will need in the short to medium term, but I-Bonds might be worth considering if you are planning on sitting on that cash for years instead of months. You can go to the Treasury Direct website for more information on I-Bonds.

Certificates of Deposit

Certificates of Deposit are another alternative for investors that are willing to lock up their cash for a certain period of time. I prefer money market funds for their liquidity (you can get your cash any time), but if you are considering CDs, I think it would make sense to look at Treasuries instead. Some banks might offer attractive CD rates, but chances are that they will be below the interest rates offered by Treasuries with the same maturity.

Conclusion

I have two savings accounts, which are generally empty, but I have received 21 cents in interest so far this year (it probably wasn’t much more in 2022 despite the fact that I kept my cash in a savings account for most of the year). While it’s not a huge issue for me and my relatively small cash holding, a lot of people have money in savings accounts becoming worth less (not worthless, that will take a lot longer) each year due to the silent tax of inflation. If you happen to be sitting on $100,000 in cash (an easy round number), you can either get next to nothing in a savings account, or close to 4% in Schwab’s SNSXX money market fund after fees. It won’t keep up with inflation, but it’s better than the alternative.

If you want to go through the process of buying treasuries, you can get a 1-year Treasury yielding 4.76%. Different maturities will have different yields, but if you are willing to go buy Treasuries, you can get better yields without paying the management fees of a money market. Other alternatives like I-Bonds or CDs might also be worth a closer look depending on your individual situation.

While we have gone from one asset bubble to the next in recent years, I don’t think we will see money market funds have issues like some of them did in 2008. I prefer Schwab’s SNSXX money market fund due to its Treasury holdings and liquidity, despite the slightly lower interest rates compared to Schwab’s other money market funds. While the continued money market inflows have some people worried, I think it is just a logical response to the huge difference in interest rates between savings accounts and money markets.

For further details see:

Money Market Funds: The Next Bubble Or The Logical Alternative To Savings Accounts?