SAH - Monro Warrants A Revision

Summary

- Monro continues to struggle from a revenue and profit perspective, though the situation could certainly be worse.

- This has caused the firm to become a bit pricier, as has the fact that shares have risen in recent months.

- All combined, the company probably doesn't offer significant upside relative to the market at this time.

In the US alone, there are nearly as many vehicles as there are people, with their number totaling around 290 million in all. It should come as no surprise then that there would be a large number of companies dedicated to providing various goods and services to keep our vehicles running. One firm that we could point to as an example of this is Monro ( MNRO ), an enterprise that owns a large number of tire and service shops spread across a large swath of the country. Recently, financial performance by the company has been a bit disappointing. Sales, profits, and cash flows have shown some signs of weakness. This has also made the firm's stock look a bit more expensive than it did previously. Add on top of this the fact that the stock has risen as of late, as well as broader economic uncertainty moving forward, and I feel as though a slight revision in my own thoughts for the company is in order. While I had previously rated the company a 'buy', I do think a more appropriate rating at this time is a 'hold' to reflect my view that shares should generate upside or downside that more or less matches the market for the foreseeable future.

A revision in expectations

Back in the middle of July of 2022, I revisited Monro to see whether or not the company still made sense for investors to consider buying into. Leading up to that point, the company had done exceptionally well over the prior few months. Even though financial performance had been mixed, it was still mostly favorable and shares of the company were trading at multiples that I considered low. This led me to keep the 'buy' rating I had on the stock. Since then, the company has gone up, but not by as much as I would have anticipated. While the S&P 500 is up 4.7% since the publication of the article, shares of Monro have generated upside of 4.4%.

{kind=link}

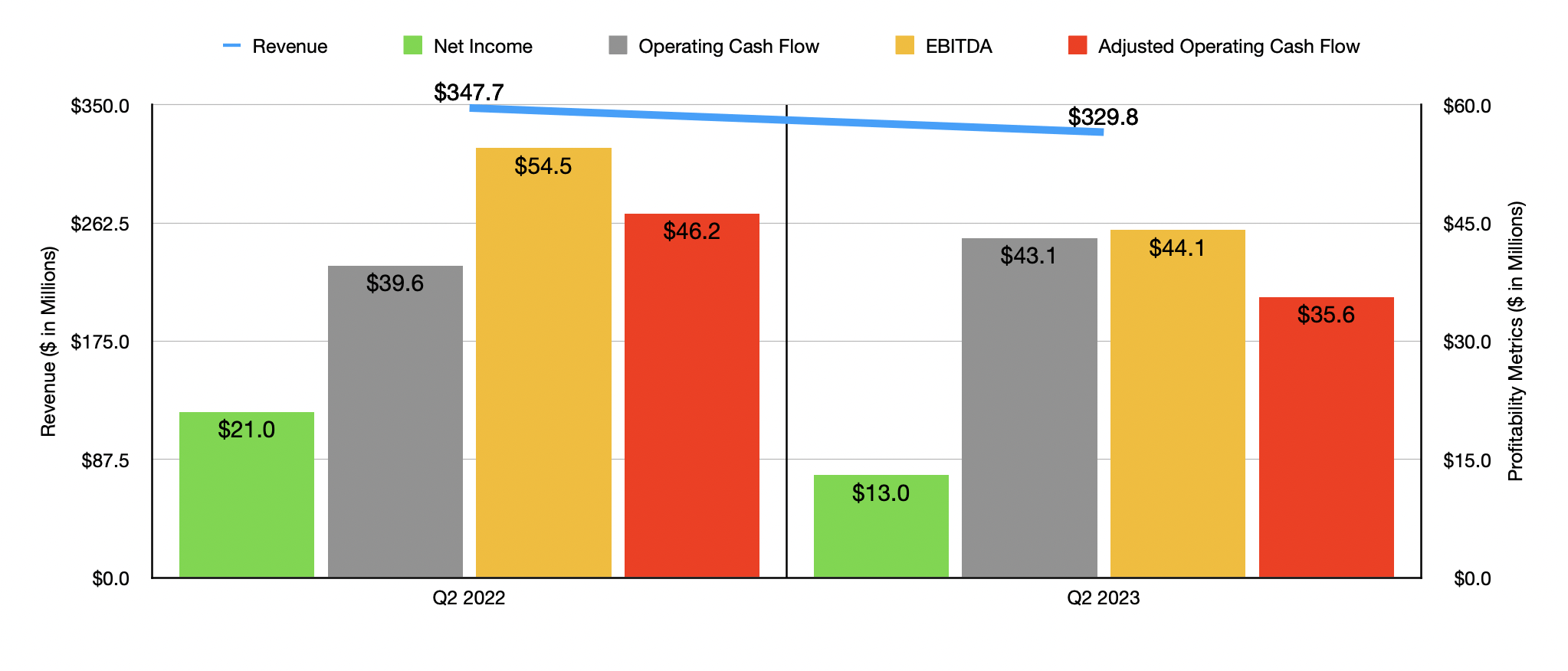

Personally, I think that the upside the company achieved could have been greater had it not been for the fact that fundamental data has been quite mixed. And that's saying it generously. For the most part, the data has actually been somewhat disappointing. Consider, for starters, results achieved during the second quarter of the company's 2023 fiscal year. During that time, sales came in at $329.8 million. That's down from the $347.7 million reported the same time one year earlier. According to management, this drop was driven entirely by a plunge in revenue associated with stores that the business ended up closing. But really, this drop was mostly associated with wholesale locations of some non-core operations that the company had divested of earlier in the year. New store sales, meanwhile, added 2.3% to the company's top line, while comparable store sales grew 1.3%.

Given the aforementioned divestiture, I could understand just the drop in revenue. But it also brought with it a decline in profits. Net income fell from $21 million in the second quarter of the 2022 fiscal year to only $13 million the same time of the 2023 fiscal year. In addition to being hit by a decline in revenue, the company also suffered from its gross profit margin contracting from 37.6% to 35.4%. This was driven largely by an increase in retail material costs, much of which was associated with a shift to a higher mix of tire sales at its retail locations and because the company chose not to pass all of its price increases onto its customers. Higher technician labor costs were also a problem cited by management. for the most part, other profitability metrics followed suit. Yes, operating cash flow did increase year over year, climbing from $39.6 million to $43.1 million. But if we adjust for changes in working capital, it would have fallen from $46.2 million to $35.6 million. Also on the decline was EBITDA, dropping from $54.5 million to $44.1 million.

{kind=link}

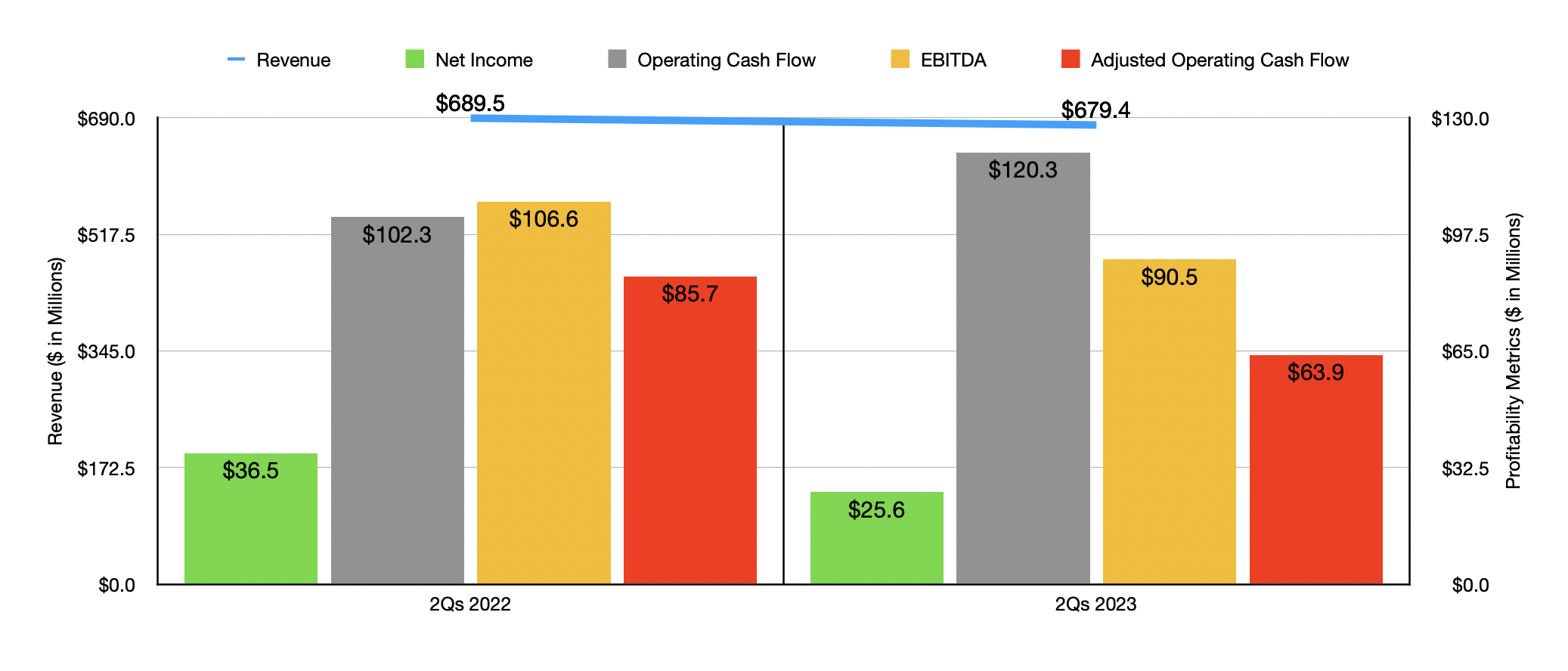

The results seen in the second quarter alone were reflective of results seen for the first half of the year in its entirety. Sales, for instance, dropped from $689.5 million to $679.4 million. Net income fell from $36.5 million to $25.6 million. Once again, operating cash flow was higher year over year, having risen from $102.3 million to $120.3 million. But if we adjust for changes in working capital, it would have plunged from $85.7 million to $63.9 million, while EBITDA for the company contracted from $106.6 million to $90.5 million. Despite these troubles, the company has not been afraid to buy back stock. In the first half of the year, it repurchased 1.6 million shares for a combined $71.2 million. 1.2 million of these shares were repurchased in the second quarter alone. This shows at least some confidence from management during what investors should consider to be uncertain times.

{kind=link}

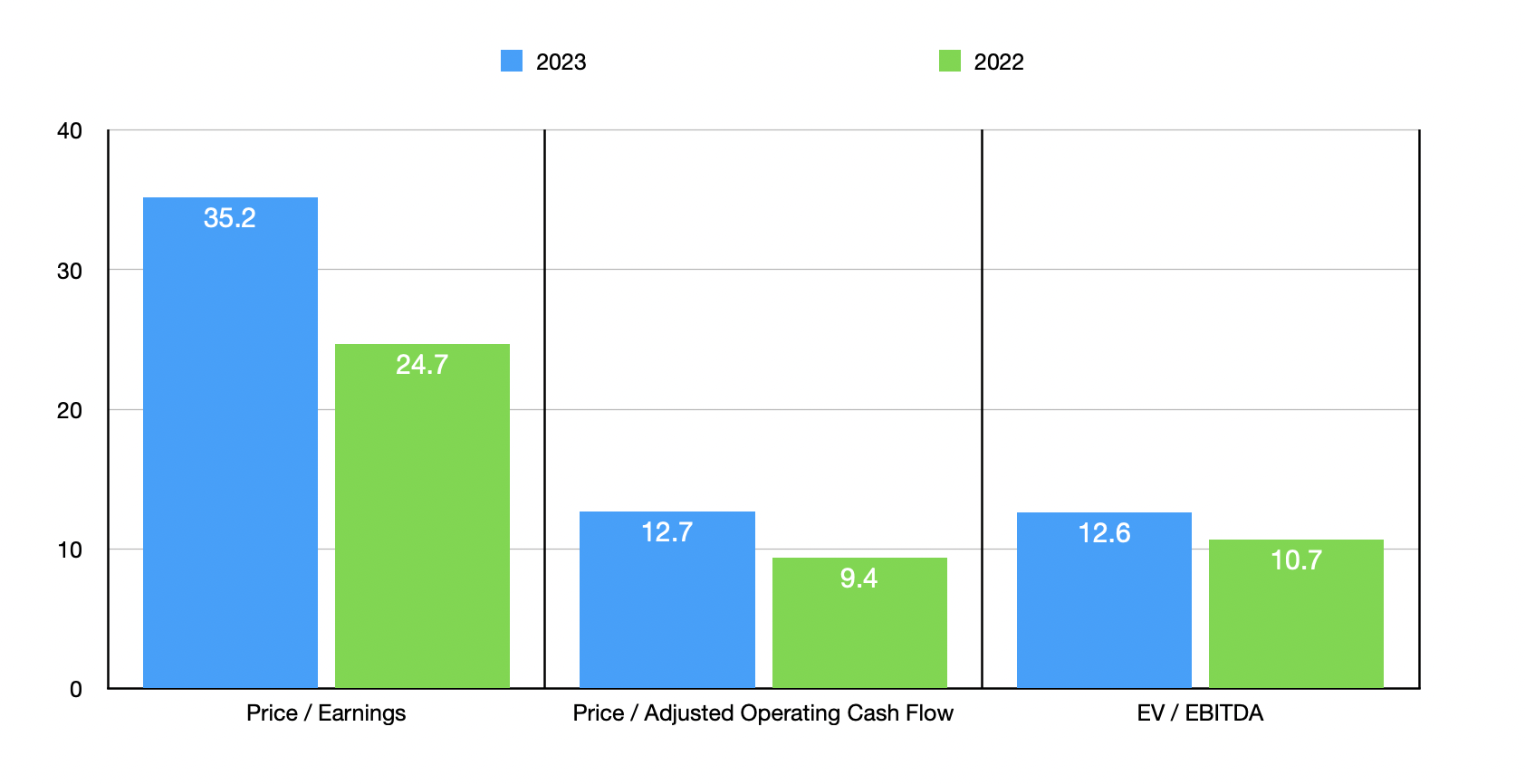

If we annualize results experienced so far for 2023, we would expect net income for the full fiscal year of $43.2 million. Adjusted operating cash flow would be $120 million, while EBITDA would come in at $158.6 million. These numbers would imply a forward price to earnings multiple of 35.2, a forward price to adjusted operating cash flow multiple of 12.7, and a forward EV to EBITDA multiple of 12.6. As you can see in the chart above, this pricing is worse than if we were to use data from 2021. Although not terribly expensive by any means, shares of the company are a bit lofty compared to similar firms. Using five other companies as comparables, I calculated that, on a price-to-earnings basis, a typical range for investors to look at would be from 5.4 to 19.9. But in this case, Monro was the most expensive of the group. Using the price to operating cash flow approach, the range was from 3 to 14.9, with three of the five companies being cheaper than our prospect. And finally, using the EV to EBITDA approach, the range was from 5.7 to 13.7. In this scenario, four of the five companies were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Monro |

| 35.2 |

| 12.7 |

| 12.6 |

| AutoZone ( AZO ) |

| 19.9 |

| 14.9 |

| 13.7 |

| Arko ( ARKO ) |

| 17.1 |

| 6.1 |

| 5.7 |

| Sonic Automotive ( SAH ) |

| 5.4 |

| 3.0 |

| 5.9 |

| Advance Auto Parts ( AAP ) |

| 19.4 |

| 13.9 |

| 10.7 |

| Murphy USA ( MUSA ) |

| 10.0 |

| 7.2 |

| 6.6 |

Takeaway

At this point in time, I do still count myself a fan of the business model that Monro employs. But this doesn't mean that I feel as strongly about the company as I did before. On an absolute basis, shares are still reasonably affordable. But relative to similar firms, the stock is a bit lofty. Add on top of this the fact that shares have risen in recent months and that its bottom line and top line results have both worsened, and I believe that a more appropriate rating for the company at this time would be a 'hold' compared to the 'buy' I had it at previously.

For further details see:

Monro Warrants A Revision