LMT - Moog: Major Catalyst And Interesting Valuation Metrics

Summary

- Third quarter earnings were strong, with adjusted earnings per share 30% up and sales were up 9% compared to last year.

- The FLRAA program could be a major catalyst for Moog.

- High Buyback Yield of 7.8%.

- Moog's EV/EBIT of 14.6 is one of the lowest in the aerospace and defense sector.

Introduction

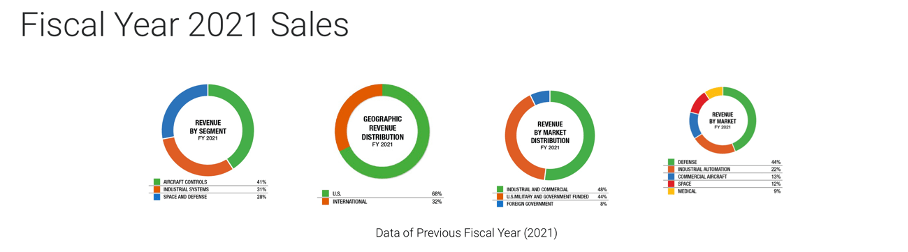

Moog Inc. ( MOG.A , MOG.B ) is a relatively small company operating in the aerospace and defense sector. The company's business segments include Aircraft Controls (41% of 2021 sales), Space and Defense Controls (28% of 2021 sales), and Industrial Systems (31% of 2021 sales).

Fiscal Year 2021 Sales (Moog Investor Relations)

{kind=link}

Moog's total return over 20 years is in line with that of the S&P500 Index (SP500), and over this period the stock averaged an annualized return of 10.6%. Since the fall in 2020, however, the share price has lagged. Still, it remains an interesting stock to watch because defense stocks are in demand in times of war. The war between Russia and Ukraine is a strong catalyst for those companies.

Third quarter results show a very positive picture for Moog's future, with the FLRAA (Future Long-Range Assault Aircraft) program being a key catalyst. Adjusted earnings were 30% higher than the same period last year. The high buyback yield of 7.8% and dividend payments make the stock attractive. The stock's valuation metrics show an attractive picture. Therefore, I believe Moog Inc. stock is a buy.

Strong Quarterly Results And Positive Outlook

Third quarter earnings were strong, with adjusted earnings per share 30% higher than last year (excluding the benefit of some tax specials). Moog Inc. sales were 9% higher than the same period last year. The company's outlook is favorable due to increased demand as a result of the war between Russia and Ukraine.

Moog does continue to experience problems in the supply chain, rising interest rates, and COVID. Free cash flow came in moderately, but that was not surprising due to ongoing supply chain issues. Reduced supply of natural gas is the new tactic as a threat to Europe, causing Europe to face an energy crisis during the winter as a result. Higher energy prices will lead to higher inflation because many businesses depend on natural gas. The government is trying to curb high inflation by raising interest rates, and rising interest rates are a headwind for Moog because total debt is about 5x FCF and their debt maturities are spread over the next few years.

Moog remains strongly optimistic about their future. CEO John Scannell describes the following during 3Q22 earnings transcript:

We have multiyear tailwinds in our defense, space, and commercial aircraft markets. Our medical market is robust and our concerns about future industrial softness is balanced by our record backlog giving us time to react to any downturn in the business. Finally, we're pleased with the results of our third quarter, our underlying operations are right on plan, and the fourth quarter is looking solid.

The aircraft business is performing strongly, demand for aircraft is no longer a problem, but staff shortages are hampering future growth. Sentiment in the defense segment is also strong due to the war in Ukraine, but this has yet to translate into new contracts. The FLRAA program, in which Moog is partnering with Textron, is expected to start in October, and this could be a major catalyst for Moog. CEO John Scannell expects this program could be as big as their F-35 production for the next decade.

High Buyback Yield of 7.8%

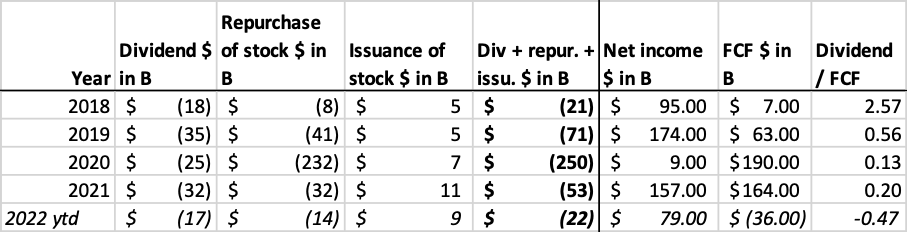

Moog pays a moderate dividend of $1.04 (dividend yield of 1.23%). In addition to the dividends, Moog buys back its own shares. Net income and free cash flow have fluctuated quite a bit in recent years, so paying a high dividend is not preferred. The dividend payments are less than free cash flow for the past 3 years. In 2020, Moog bought back a huge amount of its own shares after the share price took a big hit early that year. The stock's valuation became attractive, and Moog rewarded its shareholders well. The stock rose from $35 to $80 by the end of 2020.

Moog's cash flow highlights (SEC and Author's Own Calculations)

{kind=link}

The Board of Directors announced in 2020 a share repurchase program authorized to buy up to 3 million Class A and Class B shares.

Through the third quarter of this year, Moog has repurchased 532,000 shares for $40 million. That leaves about 2.5 million shares left to repurchase (a high buyback yield of 7.8%). However, the share repurchase program has been running since the end of FY2020, so the Board is slowly buying back shares. At this rate, there will be no aggressive price action, which will reduce the volatility of the stock.

EV/EBIT Ratio Lowest In Peer Group

Moog's EV/EBIT ratio is in line with the 10-year median. The EV/EBIT ratio takes enterprise value versus EBIT. Both market capitalization, debt and cash on the balance sheet are included in the ratio. The chart shows a large spike in 2021 due to lower EBIT.

In 2020, the EV/EBIT ratio was historically low. Right after the stock market crash, it turned out to be a good buying opportunity. A 143% gain could then be generated.

We compare Moog to other companies in the defense sector, such as Raytheon Technologies ( RTX ), Lockheed Martin ( LMT ) and General Dynamics ( GD ). These companies are larger in size. The stock valuation of larger companies is generally lower than a smaller growing company. In the chart below, we see that this is not the case. Moog's EV/EBIT of 14.6 is one of the lowest in the aerospace and defense sector. The strong growth prospects and low stock valuation make Moog an interesting buy.

Conclusion

Moog expects good prospects in their defense segment due to the war in Ukraine, and this has made the stock an interesting play. Third quarter numbers were strong, with adjusted EPS growth of 30% over last year and revenue growth of 9%. However, Moog continued to struggle with supply chain issues, higher interest rates and COVID. Free cash flow came out moderate. Still, due to the war in Ukraine, Moog remains strongly optimistic about the company's future. CEO John Scannell sees the FLRAA program as a major catalyst that could be as big as their F-35 program for the next decade. The high buyback yield of 7.8% and the dividend make the stock attractive to invest in. Valuation metrics such as EV/EBIT ratio are attractive compared to the aerospace and defense sectors. Moog stands out with an EV/EBIT ratio of 15, while Raytheon trades at an EV/EBIT ratio of 26. The favorable outlook, high buyback yield and attractive valuation metrics make Moog stock a buy.

For further details see:

Moog: Major Catalyst And Interesting Valuation Metrics