GS - Morgan Stanley: Wait For A Better Entry Point

Summary

- Morgan Stanley has sound fundamentals and its business strategy seems to be the right one.

- Its operating momentum is weakening due to cyclical headwinds, but profitability remains good and capital returns are attractive.

- Despite this backdrop, its current valuation of 1.6x book value is not cheap and some discount should be warranted due to the challenging economic environment.

Morgan Stanley ( MS ) has a sound business profile and its strategy to increase its exposure to asset and wealth management in recent years seems to be the right one, but its current valuation is not particularly cheap.

Company Overview

Morgan Stanley is a financial holding company, being one of the largest U.S. banks. It has a market value of about $145 billion and trades on the New York Stock Exchange. Its business is spread across three main business segments, namely institutional securities, wealth management, and investment management.

While the company remains as one of the largest players worldwide in the investment banking industry, its business strategy has been focused on growing in other segments over the past few years, especially in the wealth management business. Indeed, in Q3 2022, this segment was the largest one measured by revenue, which provides the bank with a more recurring and less volatile revenue stream than some years ago.

Even though Morgan Stanley has a global reach, it generates the vast majority of its revenue in Americas, given that 75% of its revenue was generated in this region during 2021. Its main competitors are other global banks, which have large investment banking and wealth management operations, including Goldman Sachs ( GS ), Citigroup ( C ), or Deutsche Bank ( DB ).

Morgan Stanley's strategy has been to grow its business through acquisitions, especially in the brokerage and wealth management segments. It has purchased E*TRADE in 2020 and Eaton Vance in 2021 , which increased its exposure to more stable segments over the economic cycle and increased the company's overall size, reaching close to $60 billion in revenue last year, compared to $41.5 billion in 2019.

Revenue (Morgan Stanley)

Despite these acquisitions, Morgan Stanley's revenue is still largely exposed to its institutional securities segment, which generated about half of its annual revenue over the past three years.

Within the institutional securities segment, Morgan Stanley's revenue comes mainly from Equities and Fixed Income, both from underwriting (new issues) and trading. Advisory also has a significant weight on revenue in this segment, both the majority of revenue is transaction-based, which means that it can be quite volatile from quarter to quarter, depending on activity in the capital markets. Its equities franchise is the most important segment within institutional securities, being a distinctive factor compared to other large U.S. investment banks.

While Morgan Stanley continues to be significantly exposed to investment banking, its strategy has been to shift its focus toward wealth management, both through organic initiatives and acquisitions. This segment has a more recurring revenue profile throughout the economic cycle, which is positive for the bank's earnings visibility over the long term.

Its smaller segment is asset management, which has generated around 10% of total revenue in recent years, being mainly focused on institutional customers. This is a segment where competition is quite fierce and the rise of passive investing is a structural headwind, thus this business should report lower growth than other segments in the next few years.

Financial Overview

Regarding its financial performance, Morgan Stanley has reported a positive operating momentum over the past few years, as the bank's operations benefited from higher activity in capital markets and acquisitions also increased the bank's revenue and earnings pool.

In 2021, Morgan Stanley reported revenue of close to $60 billion, an increase of 23% YoY, while its net income was around $15 billion (+37% YoY). By operating segment, wealth management increased revenue by 27% YoY, while asset management reported an increase of 67% YoY, due in large part by the integration of Eaton Vance.

Its efficiency ratio was 67% in 2021, which is somewhat high compared to Goldman Sachs (50% in 2021), thus Morgan Stanley may have some room to cut costs, especially from the integration of E*TRADE and Eaton Vance that have certainly significant synergies to be explored. Despite that, its profitability was quite good, considering that its return on equity ratio, a key measure of profitability in the banking sector, was 15% in 2021. This was the highest level since 2006, showing that operating momentum was quite impressive during 2021 across its business.

However, during the first nine months of 2022, the operating landscape has changed quite significantly, impacting especially its institutional securities segment. Indeed, in Q3 2022 , its revenues amounted to $13 billion (-12% YoY) due to weakness in investment banking and asset management, while on the other hand the wealth management segment reported a revenue increase of 3.1% YoY. This clearly shows that Morgan Stanley's strategy to increase its presence in this segment was the right one, providing a more resilient revenue profile during downturns.

Regarding costs and credit losses, they were quite stable compared to the same quarter of 2021, but due to lower revenue the bank's efficiency ratio increased to 74% in Q3 (a higher ratio is worse). Its net income was $2.6 billion and its ROE was 10.7%.

Going forward, Morgan Stanley is not expected to report a rapid rebound on revenue and earnings, as the macroeconomic environment remains quite uncertain and activity in M&A and underwriting should remain quite muted in the coming quarters. Nevertheless, according to analyst's estimates , its revenues should be around $53.4 billion in 2022 (-10.4% YoY), a recover slightly during 2023 to $55.8 billion, followed by growth to more than $61 billion by 2025. Its net income is also expected to improve from $10.7 billion related to 2022, to some $12.6 billion by 2025, which seems to be a reasonable expectation.

Capital Returns

Regarding its capitalization, Morgan Stanley has a very comfortable position that enables it to provide an attractive capital return policy to shareholders, as the bank does not need to retain much profits.

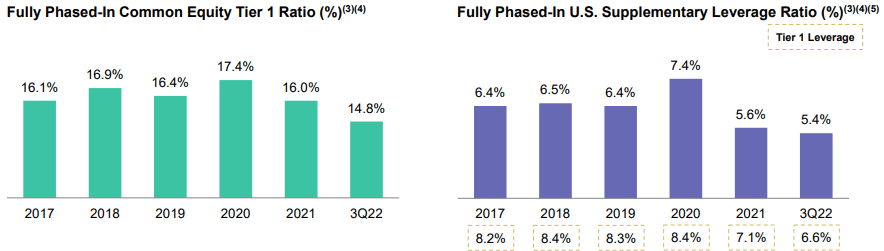

At the end of Q3 2022, its Fully Loaded Common Equity Tier 1 (FL CET1) ratio was 14.8% and its leverage ratio stood at 5.4%. This is significantly above the bank's capital requirements, providing it with an excess capital position that allows it to do share buybacks and distribute regular dividends.

{kind=link}

Its current quarterly dividend is $0.775 per share, or $3.10 annualized, which at its current share price leads to a dividend yield of about 3.6%. This is an interesting yield among U.S. large banks, given that only Citigroup offer a higher yield. Moreover, there is a high likelihood that Morgan Stanley's dividend will continue to gradually increase in the near future, as the dividend payout ratio is about 43% of its expected 2022 earnings per share, thus there is plenty of room for the bank to grow its dividend over the coming years.

Regarding its share buyback program, Morgan Stanley bought some $2.5 billion of its own shares in Q3, and is expected to continue to perform regular share repurchases in the next few quarters, as the bank's capitalization is strong and can return its profits to shareholders, both through dividends and share buybacks.

Conclusion

Morgan Stanley has strong fundamentals and its higher exposure to wealth and asset management than some years ago provides a more recurring revenue and earnings profile. Morgan Stanley is currently trading at around 1.6x book value, in-line with its historical average over the past two years, which seems fair considering the bank's good profitability and capital returns profile. However, considering the current challenging economic environment, I think investors should demand some discount compared to its historical valuation, and wait for a better entry point over the coming months.

For further details see:

Morgan Stanley: Wait For A Better Entry Point