DLA - Movado Group: Not Time To Get Out Just Yet

Summary

- Movado Group has had a great time as of late from a return perspective, even though recent financial data has been discouraging.

- The company's problems seem to be largely one-time in nature and shares still look quite cheap at this time.

- This is true on both an absolute basis and relative to similar firms and, as such, the company probably has further upside potential from here.

Whether it's great to admit or not, the fact of the matter is that it's not all that easy to beat the market, especially over an extended period of time. That's why even a modest level of outperformance should be appreciated. And one company that has achieved just that since I first wrote about it last year is Movado Group ( MOV ), a firm that's focused on the production and sale of various watch brands, some of which are owned by the business, while others are licensed from other leading consumer brands. From a share price perspective, performance achieved by the company has been impressive. Having said that, we have started seeing some weakness on both its top and bottom lines. Many investors may view this as a good opportunity to sell their stake in the firm. However, given how cheap the stock is, I would make the case that further upside is still on the table. Because of that, I have decided to keep the ‘buy’ rating I had on the stock previously.

Not time to sell just yet

In the middle of June of 2022, I stumbled across Movado Group and found myself instantly interested in the business. I like unique companies that operate in peculiar segments that you don't see often. A producer of watches fits that bill entirely. In that article, I talked about how well the company had done to recover from the COVID-19 pandemic. Both top and bottom line results were improving and shares of the business looked quite cheap. All combined, this led me to feel comfortable enough to rate the business a ‘buy’, a rating that reflected my belief that shares should outperform the broader market for the foreseeable future. Fast forward to today, and the firm has done just that. While the S&P 500 is up 8.7%, shares of Movado Group have generated upside for investors of 13%.

{kind=link}

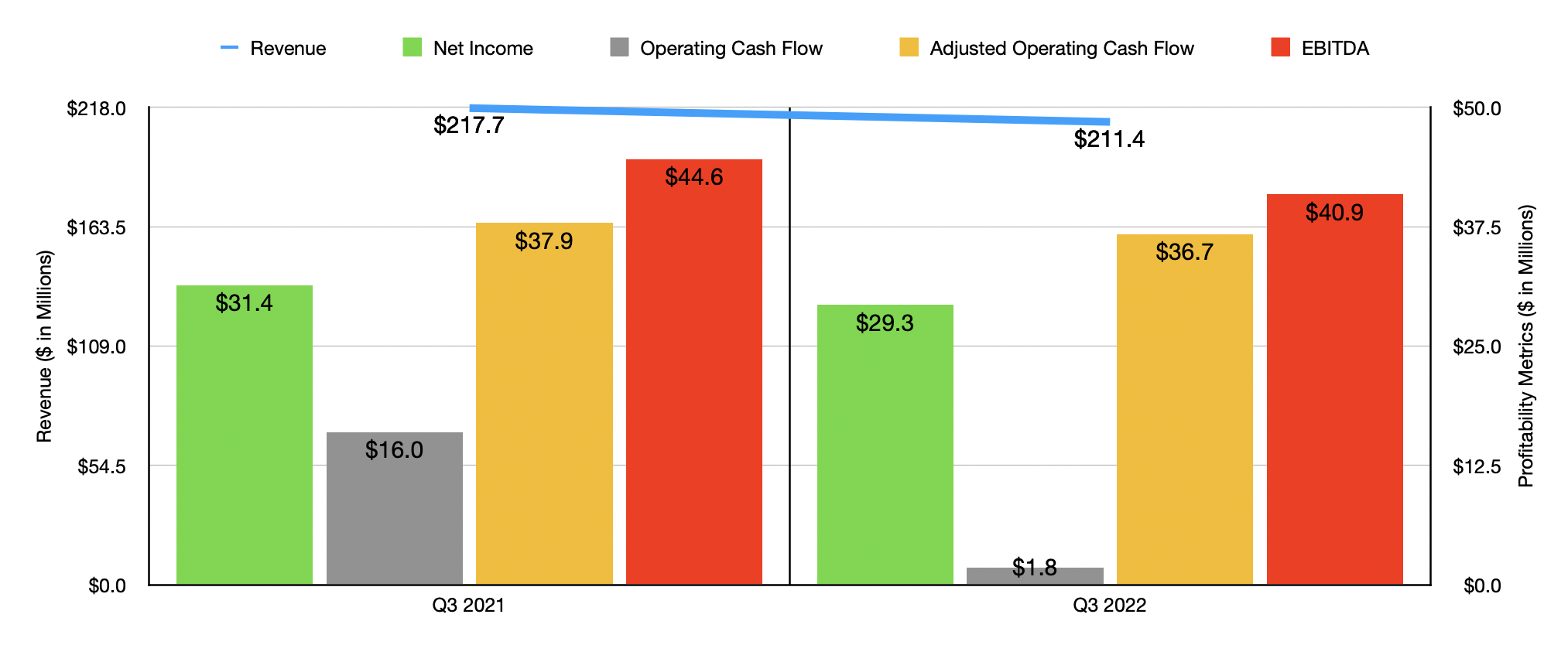

Interestingly, this outperformance has come at a time when fundamental performance reported by the company has shown signs of weakness. Take, as an example, data covering the third quarter of the firm's 2022 fiscal year. This is the most recent quarter for which data is available that was not available when I last wrote about the business. According to management, revenue during that quarter came in at $211.4 million. That's actually down from the $217.7 million reported one year earlier. Across its company stores, sales actually increased year over year. For instance, revenue associated with stores in the US inched up from $22 million to $24 million. It is true that international sales dropped from $1.4 million down to $1.3 million. But as a whole, company store revenue rose from $23.4 million to $25.2 million.

The company did experience pain elsewhere. Under the watch and accessory brands operations that it has, sales in the international market dipped from $123.6 million to $122.8 million. But the real pain came from the same watch and accessory brands sales in the UU market. Revenue here fell from $70.8 million to $63.4 million. This decline was driven by a plunge in its after-sales service and all other operations revenue, with sales falling from $2.8 million to $1.8 million. It also was the product of the owned brands category of sales falling from $69.4 million to $61.6 million. This, management said, was driven largely by the negative impact of foreign exchange rates, lower demand from the firm's wholesale customers, and a decrease in online retail sales. Specific to the US, the pain was mostly associated with decreased volumes resulting from lower demand from the company's wholesale customers in the owned brand category, and a decrease in online retail sales. When it comes to the international watch and accessory brands category, sales would have been meaningfully higher had it not been for foreign currency fluctuations. These impacted revenue by $13.7 million. In a way, this is a positive since it should be a one-time fluctuation, and considering that, without this, overall revenue for the quarter would have been higher than it was one year earlier.

Profitability, unfortunately, followed sales lower. Net income went from $31.4 million in the third quarter of 2021 to $29.3 million at the same time of the 2022 fiscal year. Operating cash flow plunged from $16 million to $1.8 million. But if we adjust for changes in working capital, it would have dipped more modestly from $37.9 million to $36.7 million. And finally, EBITDA for the company shrank from $44.6 million to $40.9 million.

{kind=link}

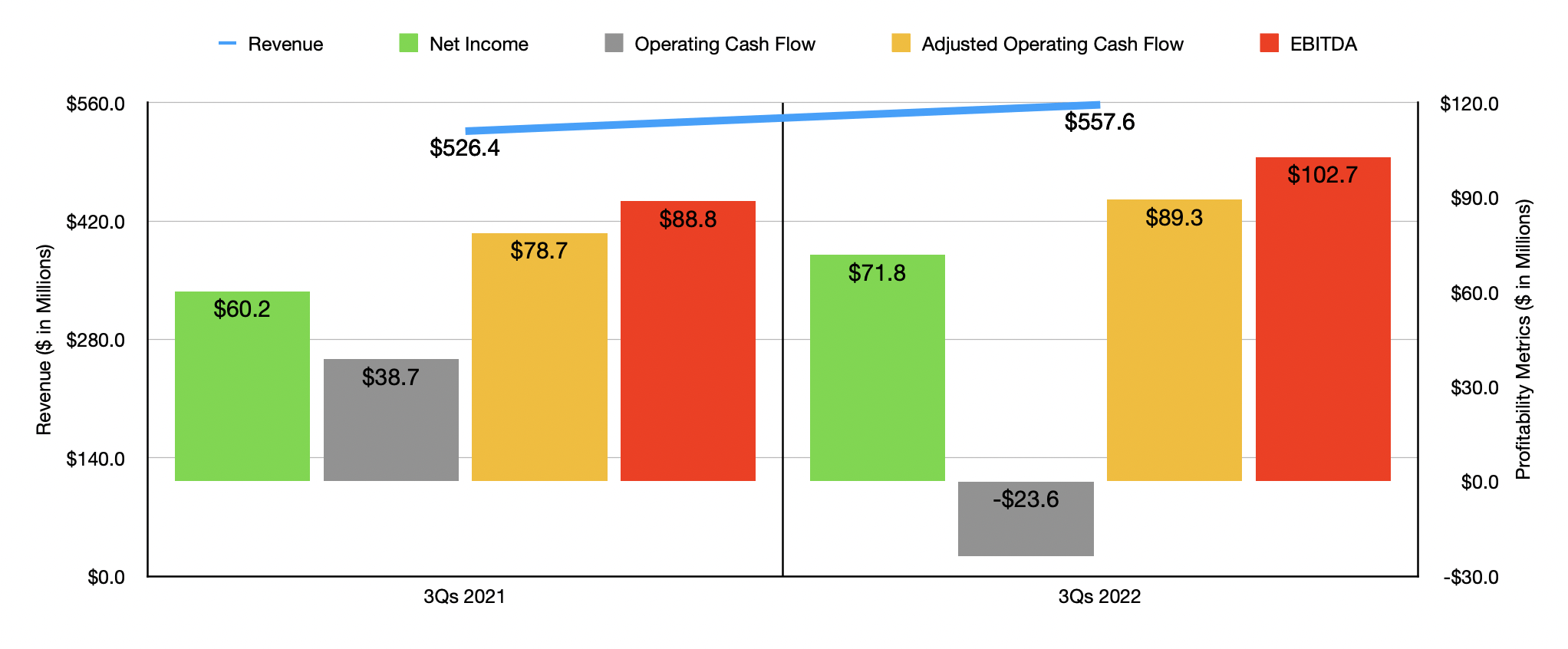

While the third quarter was bad for the company, the first nine months of 2022 as a whole were still positive. Revenue of $557.6 million beat out the $526.4 million reported one year earlier. Net income rose from $60.2 million to $71.8 million. It is true that operating cash flow worsened year over year, plunging from $38.7 million to negative $23.6 million. But on an adjusted basis, this metric still managed to rise from $78.7 million to $89.3 million. Also showing improvement was EBITDA. Year over year, this metric rose from $88.8 million to $102.7 million.

Because of the weakness experienced in the third quarter, as well as expectations for the rest of the year, management said that overall revenue for 2022 should come in at between $740 million and $750 million. This is down from the $780 million to $790 million range the company previously anticipated. Approximately $35 million of negative impact is expected from foreign currency fluctuations. The rest will likely be associated with decreased demand for its products. The company didn't come straight out with an estimate for earnings per share or net income. But they did give rough estimates for operating income and the percentage of pre-tax income that it will have to pay toward taxes. Using midpoint estimates here, we should anticipate net income for 2022 of around $91.8 million. If we annualize financial results for the other two metrics, we would anticipate adjusted operating cash flow of $128.7 million and EBITDA of roughly $147.6 million.

{kind=link}

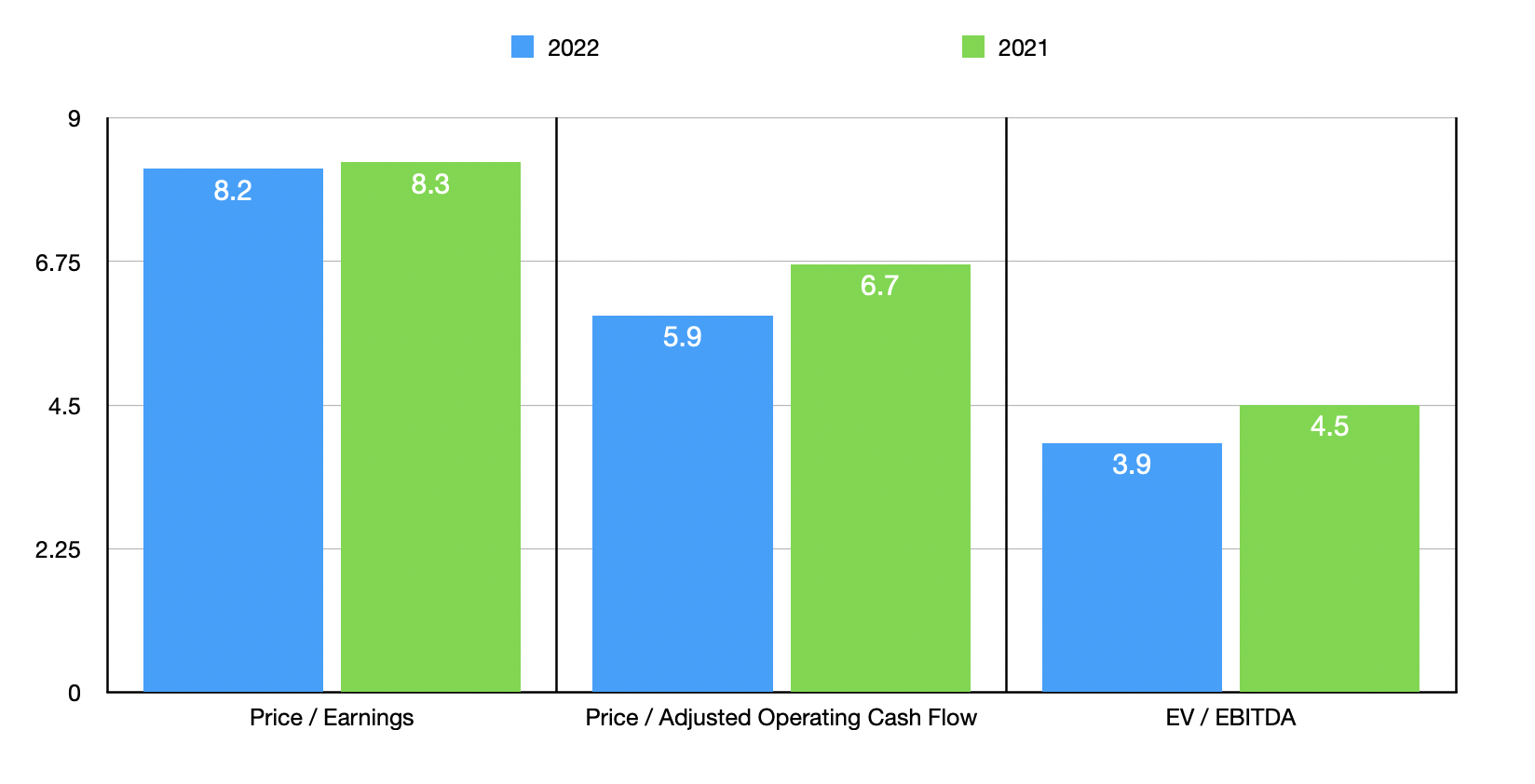

Based on these numbers, Movado Group is trading at a price-to-earnings multiple of 8.2. The price to adjusted operating cash flow multiple should be 5.9, while the EV to EBITDA multiple, benefiting from cash in excess of debt of $186.7 million, should come in at 3.9. By comparison, if we were to use the data from 2021, these multiples would be 8.3, 6.7, and 4.5, respectively. As part of my analysis, I also compared the business to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 4.2 to a high of 12.3. In this case, two of the five companies were cheaper than our prospect. Using the price to operating cash flow approach, the range was from 3.7 to 99.2. And when it comes to the EV to EBITDA approach, the range would be from 1.8 to 61.9. In both of these scenarios, only one of the five companies was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Movado Group |

| 8.2 |

| 5.9 |

| 3.9 |

| G-III Apparel Group ( GIII ) |

| 4.2 |

| 7.3 |

| 4.6 |

| Superior Group of Companies ( SGC ) |

| 11.8 |

| 11.8 |

| 61.9 |

| Delta Apparel ( DLA ) |

| 6.6 |

| 99.2 |

| 6.2 |

| Vera Bradley ( VRA ) |

| 11.3 |

| 3.7 |

| 1.8 |

| Signet Jewelers ( SIG ) |

| 12.3 |

| 6.7 |

| 6.1 |

Takeaway

Fundamentally speaking, Movado Group has experienced a bit of weakness as of late. However, most of that weakness seems to be associated with foreign currency fluctuations. This is mostly forgivable because it should be considered one-time in nature. Outside of that, the overall picture for the firm remains fairly solid and shares are trading on the cheap, both on an absolute basis and relative to similar firms. Given these factors, I do believe that further upside is on the table from here. As such, I've decided to keep the ‘buy’ rating I had on the stock previously.

For further details see:

Movado Group: Not Time To Get Out Just Yet