CA - MTY Food Group: Increasing Growth But Income Hindered By Cost Of Sales

Summary

- Increasing revenues, recent acquisition and global outreach depicts potential in the company.

- The rising inflationary pressures are leading to heavy increase in cost of sales.

- I would rate MTYFF as Hold.

MTY Food Group, Inc. ( MTYFF ) has shown consistent revenue growth over the past decade, except for 2020. In 2022, the company's system sales were at an all-time high, with its Canadian segment experiencing a 27% organic normalized adjusted EBITDA growth. The company's digital sales also increased by 8% from the previous year. However, the rising interest rates and inflation are a cause for concern as they are increasing the cost of sales, which requires attention. The intrinsic valuation of the company is below the current market price, which makes me rate MTYFF stock as a Hold.

About the company

MTY Food Group, Inc. operates in the restaurant industry as a franchisor and also operates corporate-owned locations in the quick service restaurant, fast casual, and casual dining segments. The company sells retail products under several different brand names. MTYFF has three distribution centers and two food processing plants located in Quebec. The company's business model is designed to operate across a broad range of demographic, economic, and geographic sectors. The concepts operated by the company include a variety of brands within the restaurant industry.

{kind=link}

Recent performance

The company achieved a new milestone in 2022 by surpassing $500 million in revenue for the first time, making it a record-breaking year. The net income accounted for approximately 10% of the total revenue and there was a nearly 25% increase in revenue per share. The company has continued to expand its business by acquiring other companies, such as Barbecue Holdings, Wetzel's Pretzels, and Sauce Pizza and Wine, resulting in soon to be a network of more than 7,000 locations and establishing itself as one of North America's largest franchisors. In the fourth quarter of 2022, the company exceeded expectations by over $20 million in revenue, resulting in a positive surprise.

Strengths

MTYFF's greatest advantage is its potential for continuous expansion, which is evident from its performance over the past decade. With the exception of 2020, when the COVID pandemic negatively impacted the entire restaurant industry, the company has consistently generated incremental revenues over the last ten years. In 2022, MTYFF achieved a milestone by surpassing CAD 4MMM in system sales for the first time in its history. Despite being currently divided into two geographical segments, Canada and the United States, and international, the company has 488 locations operating in 39 countries outside of North America as of November 2022. This suggests that the company has significant opportunities to expand its operations in these countries and generate returns for its investors.

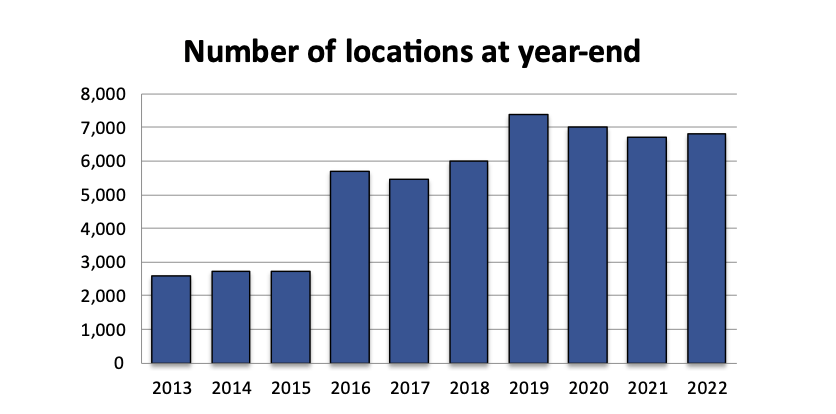

Another advantage of MTYFF is its successful record of acquisitions, which has the potential to generate greater returns for its investors. In the latter half of 2022, the company acquired three new businesses: BBQ Holdings, Wetzel's Pretzels, and Sauce Pizza and Wine. Prior to these acquisitions, the company had 6,788 locations in its network, as shown in the graph below. With the addition of 350 Wetzel's Pretzels locations and 13 Sauce Pizza and Wine locations, the company would have more than 7100 locations and there is the potential for increased profits for the company.

Number of locations at year end (Annual Information Form 2022 - MTYFF)

{kind=link}

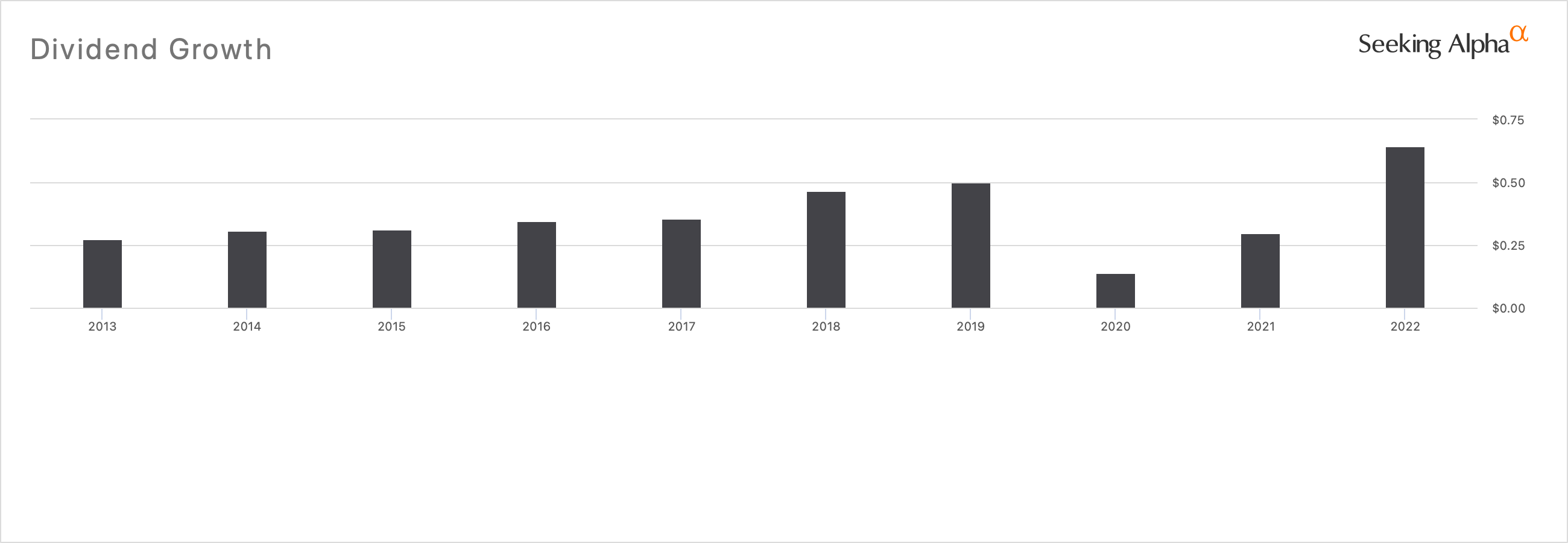

MTYFF also prioritizes returning value to its investors through dividends and share repurchases. In 2022, the annual payout to investors more than doubled, with annual dividends increasing from $0.29 to $0.65 . The dividends declared by the company were the highest in the last 10 years especially after seeing a huge dip in 2020. This suggests that the management expects positive and stable cash flows in the future. Additionally, the company implemented a share repurchase program, purchasing over a quarter million shares. This indicates that the management believes the company's stock is still undervalued and has confidence in MTYFF's potential for growth.

{kind=link}

Weaknesses

Upon closer examination of MTYFF's income statements, it appears that the cost of sales is rising at a faster rate than revenue. Although revenue increased by approximately 23%, the cost of sales surged by around 84%, resulting in a decrease in the company's gross profit margin. In 2021, the company had a gross profit margin of approximately 89%, but in the previous year, it decreased by 5%. This decline may be due to rising inflationary pressures, which the company will need to address in order to prevent further shrinking of the profit margin.

Furthermore, an examination of MTYFF's balance sheet indicates that the company has a weak liquidity position. With a current ratio of only 0.61x, the company's current assets are insufficient to meet its short-term obligations such as paying suppliers or fulfilling its payroll responsibilities. A weak liquidity position may lead to a negative impact on the company's reputation, which can make it difficult for the company to attract customers, suppliers, and investors.

Valuation

The analysis of MTYFF's value using both EV/EBITDA and P/E multiples suggests that the current stock price of $47.43 is higher than the estimated intrinsic value of $39.45, indicating that the stock is overvalued. The following assumptions were made for the valuation:

Peers - To evaluate and compare MTYFF's valuation techniques, a group of ten peer companies were selected based on their similarity in business and market capitalization. The selected peer companies include Portillo's Inc ( PTLO ), Arcos Dorados Holdings Inc. ( ARCO ), Brinker International, Inc. ( EAT ), Jack in the Box Inc. ( JACK ), Dine Brands Global, Inc. ( DIN ), Sweetgreen, Inc. ( SG ), First Watch Restaurant Group, Inc. ( FWRG ), BJ's Restaurants, Inc. ( BJRI ), Denny's Corporation ( DENN ), and Chuy's Holdings, Inc. ( CHUY ).

EV/EBITDA - A peer median multiple of 15.54x was utilized to compare with MTYFF's 15.38x.

P/E multiple - A peer median multiple of 14.57x was utilized to compare with MTYFF's 20.82x.

Intrinsic Valuation (Created by author using data from Seeking Alpha)

Conclusion

MTYFF is growing and 2022 was a year of accomplishments for the company. Its global outreach and recent acquisitions make it a company with huge potential. Recent dividends and the confidence of management impress me, and I would keep MTYFF in my watchlist.

Despite the positive aspects of MTYFF's growth and recent achievements, there are also some challenges that the company may face. One of these challenges is the declining sales in Q1 for the past two years, which could negatively impact the company's performance. Additionally, the increasing inflation rates and labor costs are putting pressure on the company's cost of sales. Furthermore, my intrinsic valuation analysis suggests that the company is currently overvalued and this stops me from rating MTYFF any higher than Hold for the time being.

For further details see:

MTY Food Group: Increasing Growth But Income Hindered By Cost Of Sales