XOM - Murphy Oil: Raising That Batting Average

2023-03-06 08:22:21 ET

Summary

- Big projects result in growth spurts and write-offs that make quarterly comparisons challenging.

- Murphy Oil Corporation was able to complete a large project that resulted in significant production growth.

- Offshore, particularly the Gulf of Mexico is a major focus area and profit center for the company.

- There are a lot of distant future growth possibilities in Brazil.

- The large growth in fiscal year 2022 necessitates a relatively large budget in the current fiscal year to maintain production levels and grow less rapidly.

Murphy Oil ( MUR ) is a company that frequently flies under the radar. Management does not do the "road shows" that many do to promote the stock. Management also has an unusual focus on the long-term for a publicly traded stock. Last but not least tends to be a focus on large projects. All of this makes for a very unusual company that does not have that quarterly focus while maintaining an exceptional long-term focus that few rivals can match.

A few years ago, management had decided that times had changed, and the portfolio needed an overhaul. What was amazing to me was that they took a couple of years and overhauled the portfolio. Now management has exactly what it wants to have. Some of the future results of that portfolio shifting should become apparent over the next few years if it is not apparent already.

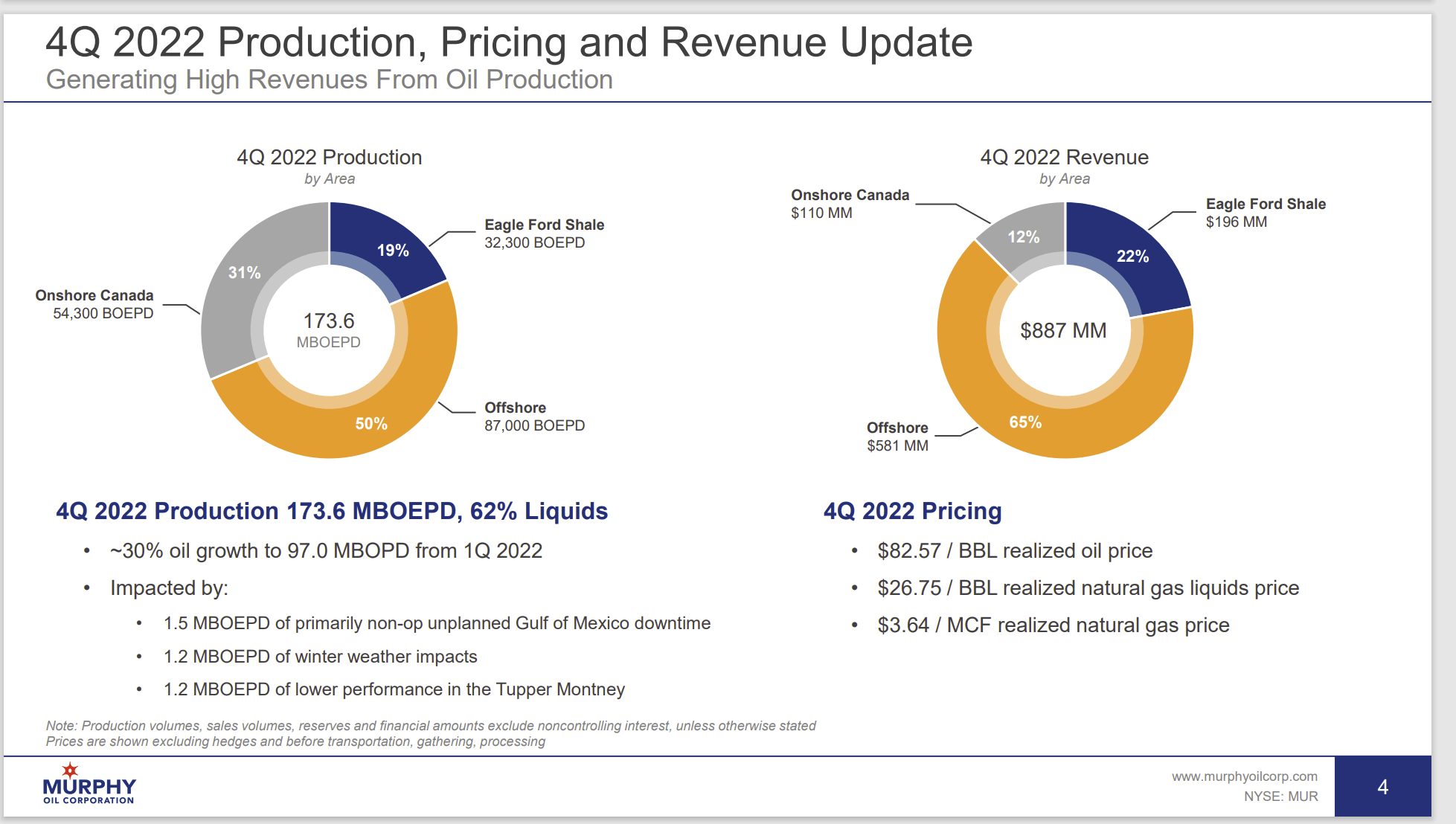

Murphy Oil Summary Of Fourth Quarter Oil Production Growth And Revenue Effects (Murphy Oil Fourth Quarter 2022, Earnings Conference Call Slides January 26, 2023)

{kind=link}

In a year when it has become popular to note that many companies did not grow production, this is one company with the balance sheet strength to very much grow production . More importantly, this is a management that is unlikely to join the rush to the most popular basins like the Permian. Instead, this management does what shareholders pay for. The management finds as profitable or more profitable opportunities at bargain prices elsewhere in the industry while avoiding capacity takeaway issues like the Permian.

Long-time followers of the company may remember that the Gulf of Mexico operations were sold around the time of the big oil spill. The company was absent from this major producing area for a couple of years that followed. Then in typical management style, there were some bargains in the Gulf of Mexico a few years later (most likely from operators upset with the aftermath of the oil spill) and Murphy management opportunistically re-entered this important operating market.

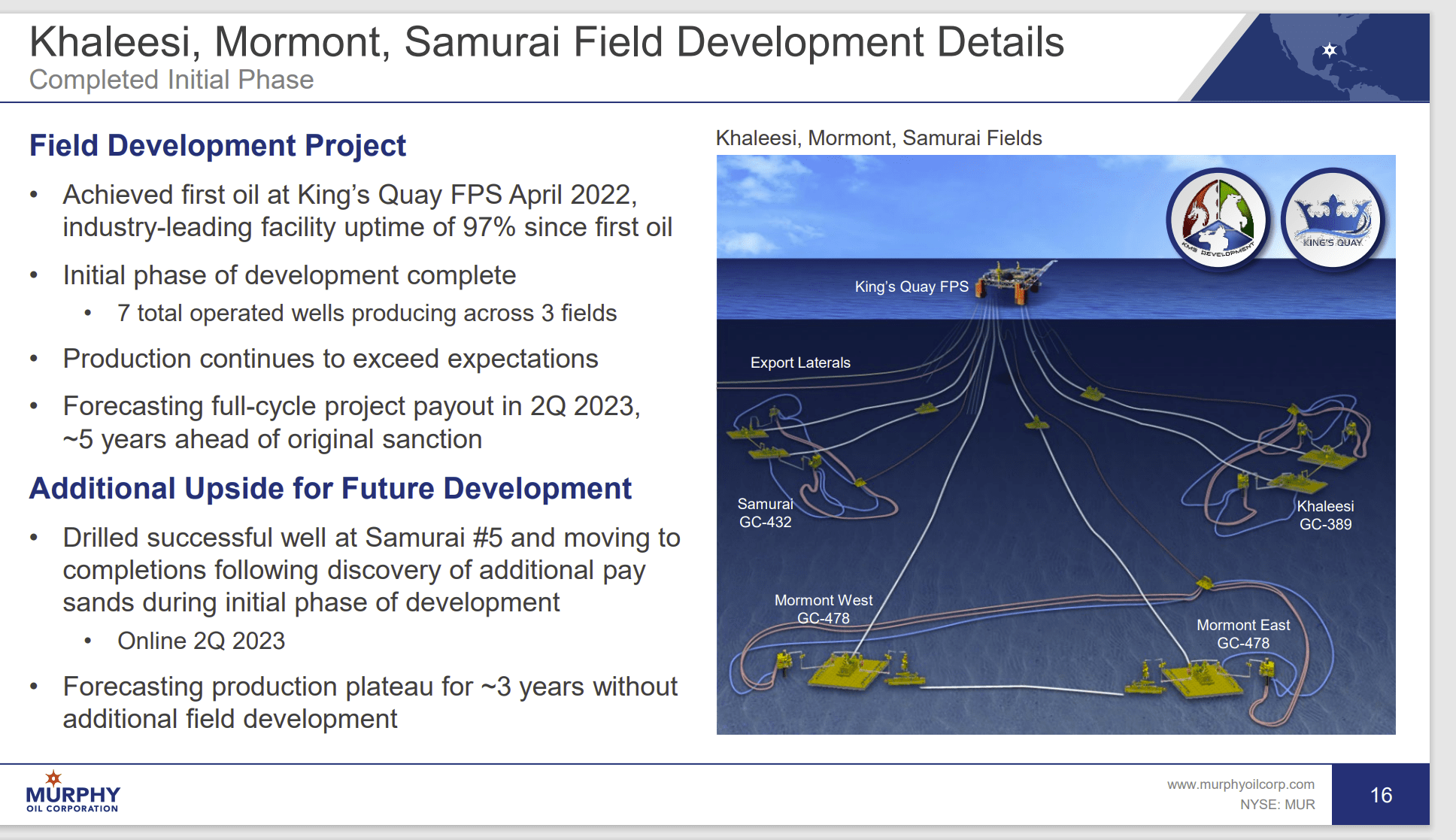

Murphy Oil Gulf Of Mexico Growth Production Initial Results (Murphy Oil Fourth Quarter 2022 Earnings Conference Call Slides January 2023)

{kind=link}

Much of the company production growth can be attributed to this project. The offshore wells tend to be significant to production individually because they tend to be large producers that are long-lived with low decline rates. Any project like this will take years to produce and the work to bring it online likely continued right through fiscal year 2020 when much of the industry shut-down due to all the coronavirus challenges.

Management got lucky in that the oil price recovery is far stronger than many anticipated by then. But a project like this one does not get built without a very low breakeven point because these large projects tend to produce in good and bad times. Then again it takes good management to be in a position to get lucky with commodity prices.

As so many companies amply demonstrated, fiscal year 2020 was devastating to a lot of company finances. Rarely do companies have the balance and diversification to get through a challenging situation like that to be able to grow production in a fantastic year like the current one. Of course, it goes without saying that the production also had very low breakeven points to provide relatively decent cash flow in fiscal year 2020.

As management noted above, the timing of initial production could not be better. The payback accelerated tremendously due to the sky-high commodity prices no one expected. That puts this project in the "catbird seat" to expand almost at will with paid off assets. Usually this kind of project is expected to payback in five or more years. So the future profitability of this project is likely to be unmatched easily because it paid back so fast. That is known as a competitive moat.

Future Potential Large Projects

This company has an unusually plentiful supply of potential large profitable projects on its plate. To some, that slows down current growth. But it also means that there could be some rapid growth in the future like the production growth this year if management chose well.

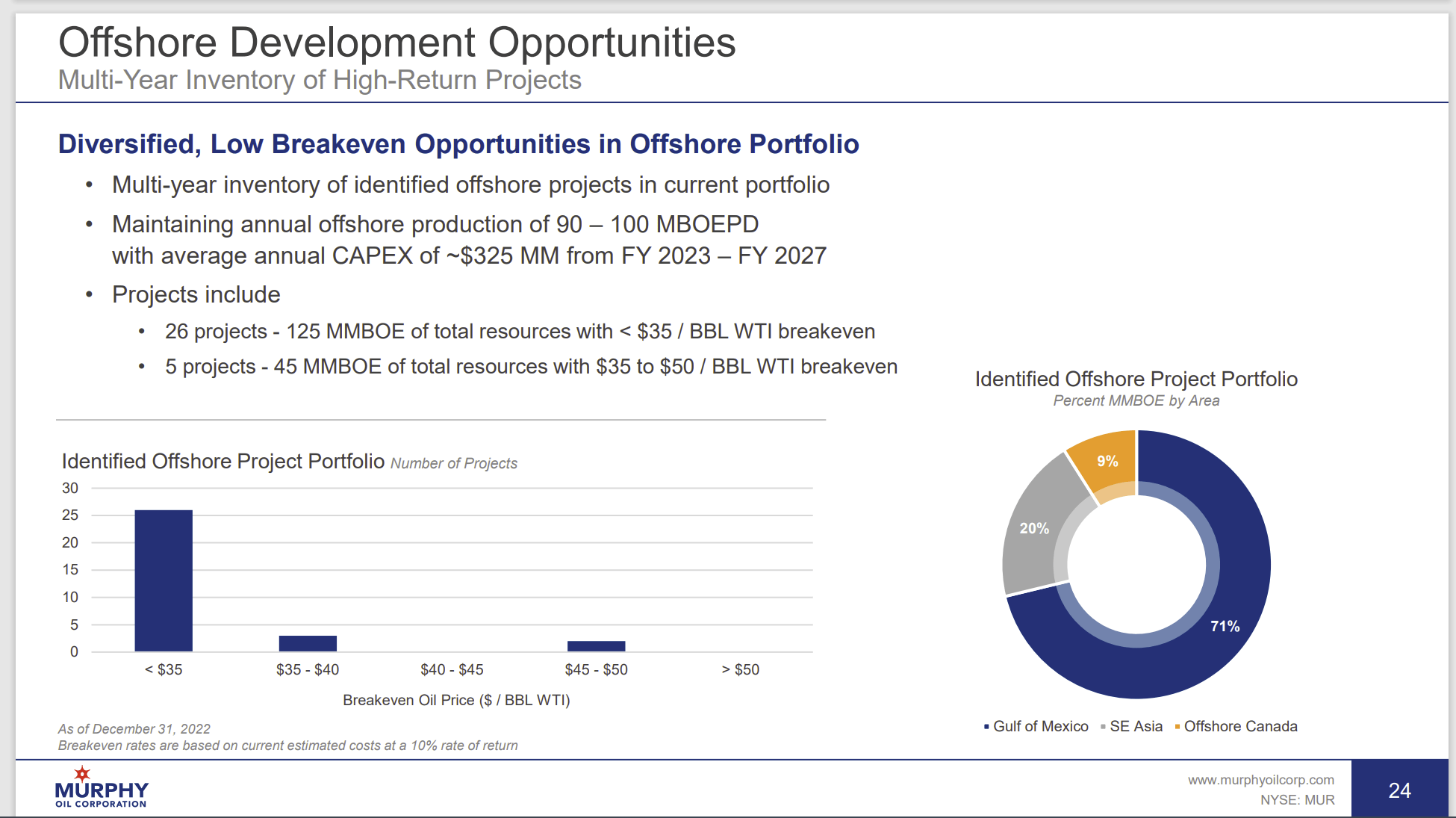

Murphy Oil Breakdown Of Offshore Breakeven Potential (Murphy Oil February 2023, Corporate Presentation)

{kind=link}

It is hard for the company to find lower breakeven projects than is the case offshore. Those projects are often large and Murphy is a relatively small player offshore. But management has adeptly handled the challenges of offshore to achieve a relatively high level of success.

The result of this is a fair number of offshore projects that are lower risk than one would expect to provide significant upside potential for a company of this size. Make no mistake, there will be some dry holes along the way. But the sheer number of development projects available (as well as exploration in areas that are relatively explored is phenomenal for any management).

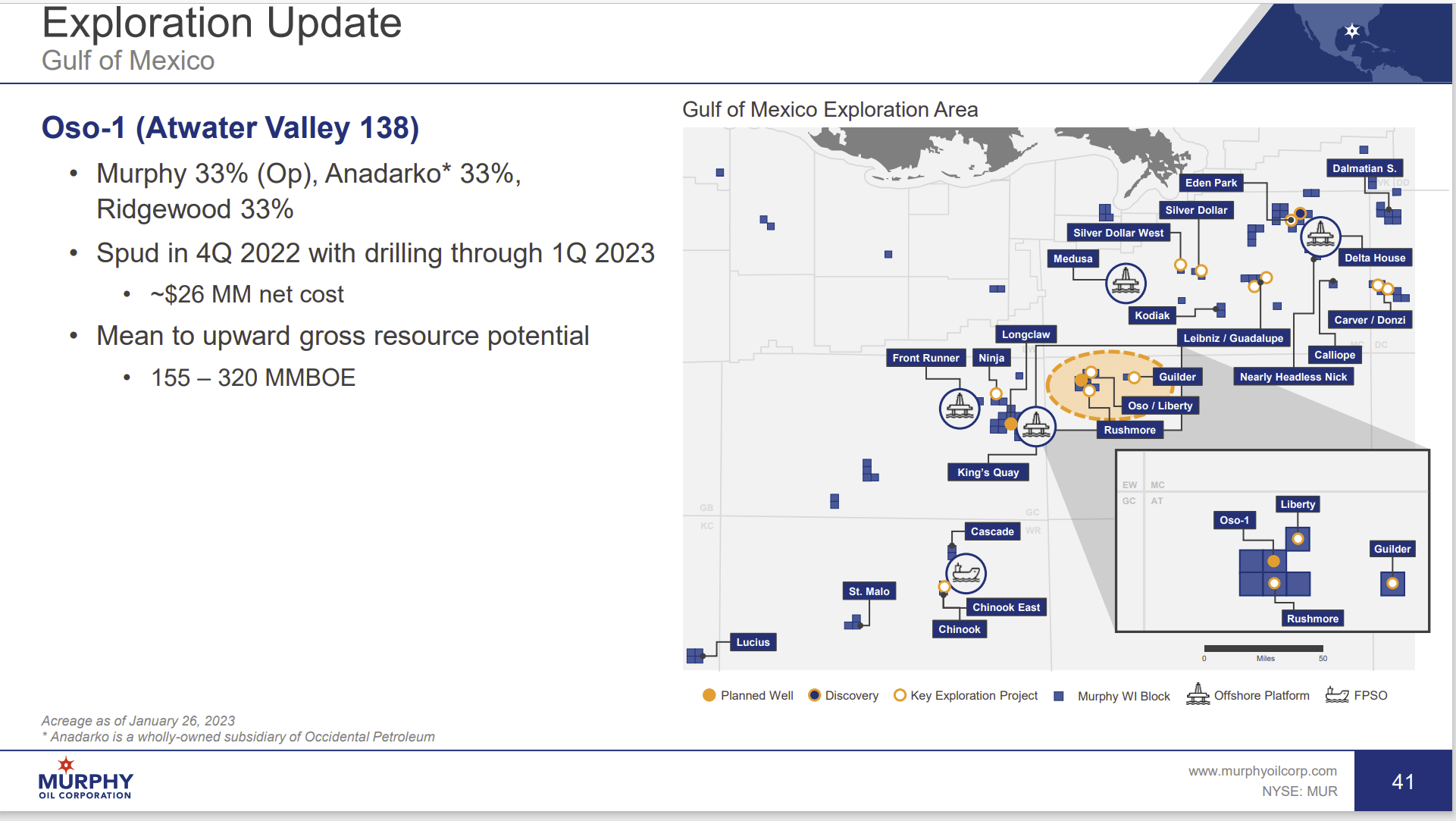

Murphy Oil Joint Venture Gulf Of Mexico (Murphy Oil February 2023, Corporate Presentation)

{kind=link}

Since Murphy has a lot of these projects, there are frequent expensing of dry wells because those offshore attempts are expensive. That makes quarterly comparisons nerve wracking for any investor that wants smooth comparisons. On the other hand, the growth shown earlier tends to be quite significant to the company when one of these exploration wells succeeds. Things will smooth out as the company grows. But for the time being, lumpy and erratic comparisons are the order of the day as this is a relatively small company in the offshore world. It is also a relatively successful company though.

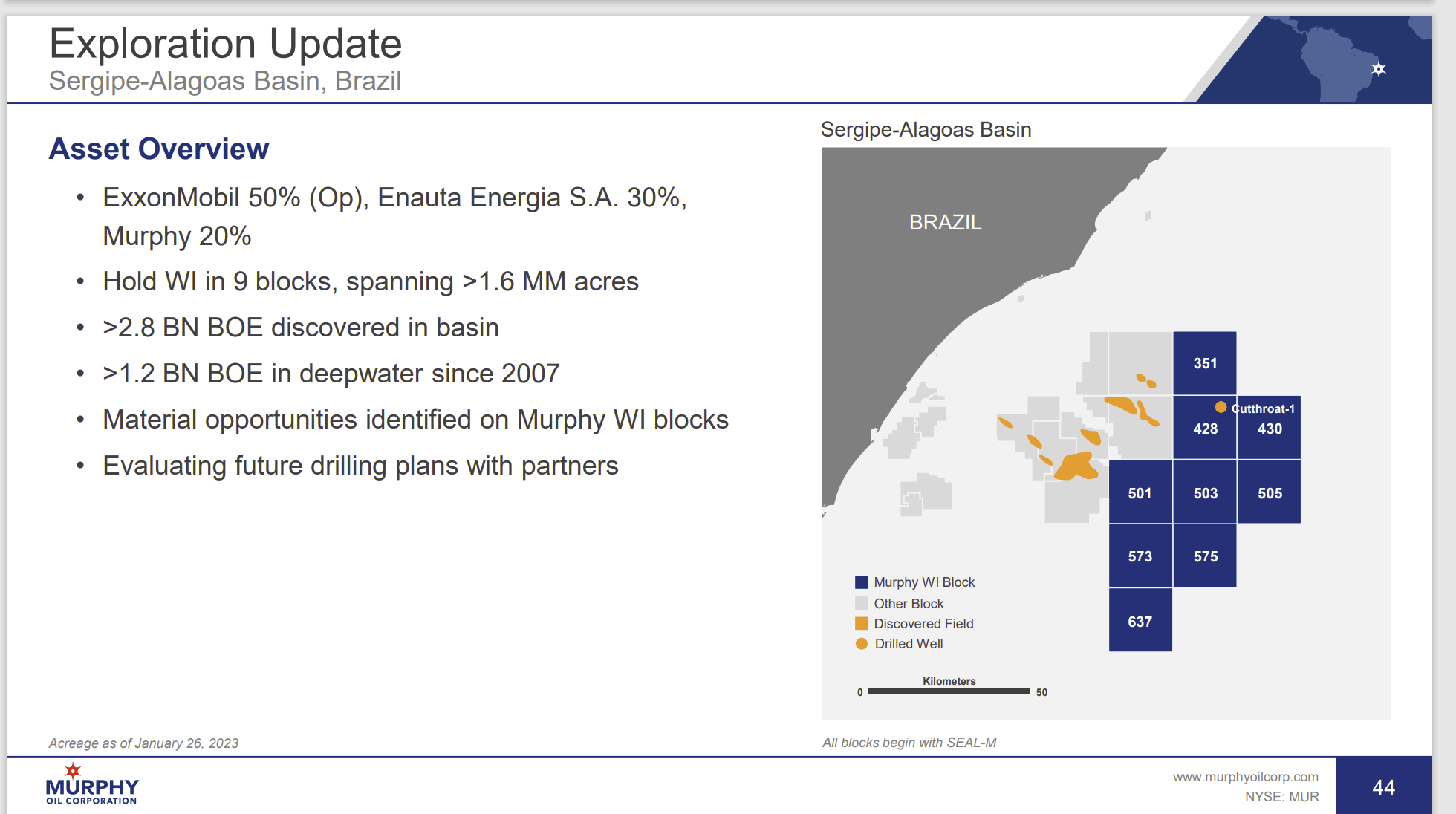

Murphy Oil Exxon Mobil Brazilian Project Joint Venture (Murphy Oil February 2023, Corporate Presentation)

{kind=link}

The Brazilian joint venture that is operated by Exxon Mobil ( XOM ) is not as far along as is the Gulf of Mexico. The first exploration well was not successful. So, the partners are evaluating the next steps on the leases owned. Murphy actually has other opportunities in Brazil that are also in the early exploration stages.

Ironically, Exxon Mobil has not had the success in Brazil that it has had in Guyana. But it is still one of the most reputable firms in the business to partner with. As shown above, Murphy tends to be involved in projects that are near known fields. This is thought to somewhat reduce the exploration risk.

Still, the timeline for a successful commercial find is about 5 to 7 years. But this is how the company keeps those large projects coming in the future for steady growth.

The Future

Murphy is going to have a "hang on to that growth" fiscal year. The rapid growth from last year will mean a relatively large budget dedicated to replacing the first-year decline of that rapid growth. Therefore, the production growth in the current fiscal year is likely to be in the low teens as management forecast.

But another offshore discovery can rapidly change future prospects as the fiscal year just ended demonstrated. In the meantime, investors need to realize that a dry offshore well will result in a material quarterly expense that can jade the market outlook on the company until the next quarter arrives.

Mr. Market is of course thrilled when a fantastic growth year like fiscal year 2022 arrives. But that generally takes a few dry wells and then some years of development to have that kind of fiscal year. Nonetheless, successful offshore projects are among the most profitable in many company portfolios.

Whether the erratic nature of the results suits a particular portfolio is up to the individual investor. Timing this investment is exceptionally hard because one never knows when a major discovery well happens. The offshore world is full of material surprises.

But this is probably one of the better companies to participate in the offshore business. Management generally uses much of the onshore business as a cash flow source to fund the "big projects". The balance sheet is always a priority. Sometimes the dividend is sacrificed temporarily as a result. But that strong balance sheet makes betting on an offshore discovery far less risky than is the case for some of the more speculative "market darlings" that literally "bet the company". Growth will be erratic due to the nature of the large projects. But it will also be reasonably assured because the company has a lot of chances for future material discoveries that are well thought out.

For further details see:

Murphy Oil: Raising That Batting Average