VZ - My Dividend Growth Portfolio August Update - Waving Goodbye To Walgreens

2023-09-10 00:23:20 ET

Summary

- Walgreens has had better earnings promised for years that never materialize.

- Walgreens has more upside to the price than down, and the dividend is safe for now, so there is no rush to sell.

- September kicks off the busy fall season for dividend increases with expected increases from Honeywell, Texas Instruments, Microsoft, Starbucks, Philip Morris, and Lockheed Martin.

One of the most important things I have learned over many years of dividend growth investing is the value of patience. Patience in waiting for the right price to buy. Patience with dividend growth. Even patience when a company is down.

Right now, Walgreens ( WBA ) is down. The forever-promised turnaround is still just over the horizon. Dividend growth is nonexistent. How many CEOs have they gone through now? And I am out of patience.

I have yet to sell, however. My initial plan was to sell the company after the last ex-dividend date. However, I felt a better price would come in the next month or so. At the time, I wanted to replace my WBA income with more Enterprise Products Partners ( EPD ) and hopefully have some proceeds left over to add a share or two of something a little faster growing. Wow, did I ever miss the boat on that!

Now, I am playing a game of chicken. On the one hand, I am comfortable holding WBA for the time being as long as the dividend stays intact. The longer I keep it, the more chance the price has room to recover. Of course, if they cut the distribution, I may be forced to sell at an inopportune time. As I am focused on the income, there is a lot of timing with selling as I consider ex-dividend dates on both WBA and any replacement purchases.

I see more potential for upside in the stock price than downside currently.

- An announcement of a new CEO who is viewed with optimism. (Of course, they may have trouble finding anyone interested in the role!)

- The slightest bit of positive news right now could lead to a jump. This stock is nearly contrarian as can be.

- A kitchen sink quarter that is viewed as such by the investing world and leads to optimism that the worst is over, and not just considered as another typical bad quarter.

- A dividend cut. While a dividend cut may cause an initial drop in price, it will likely lead to increased optimism. Of course, this can play out over more months than I will be holding the company after a cut.

From the dividend side of the equation, there are a few things I am considering:

- The odds of a dividend cut in the next two quarters are small. The dividend is still covered with operating cash flow, and companies with long dividend growth histories often bridge a year where the distribution isn't well covered. Stanley Black & Decker ( SWK ) is a recent example of a company with awful earnings and cash flow but appears to have a safe dividend going forward.

- Once a new CEO is appointed, I expect them not to push too hard to change the dividend for a few quarters. Then, a visionary may ask for the cash to be put to better use, while if we get someone more of a fixer, we may see the dividend chug along indefinitely.

- While the company can likely sustain the dividend at its current earnings, its continued degradation is a genuine concern.

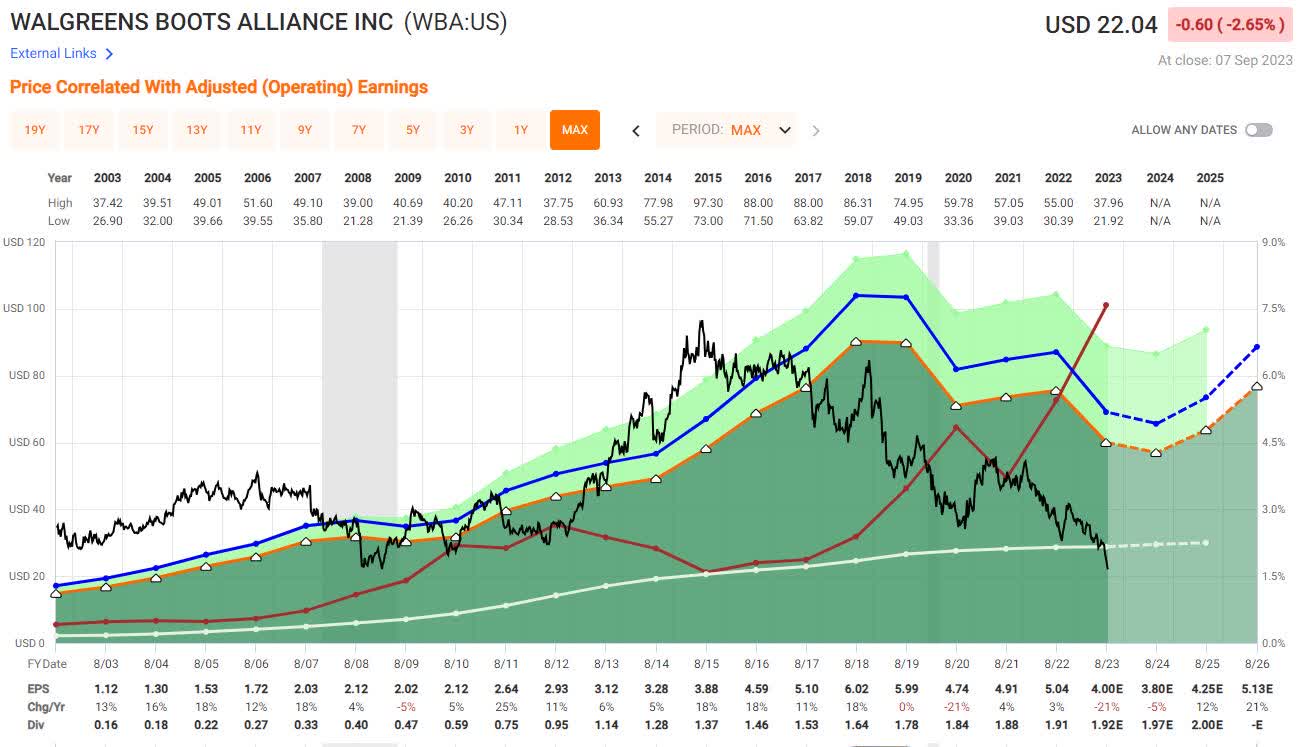

The non-stop reduction in earnings has led me to give up on the company. A turnaround in earnings is always right around the corner. For fun, I pulled some FAST Graphs from past articles showing the projected earnings. These should serve as a warning on trusting analyst projections too much!

Here is how the FAST Graph looks today: analysts projecting EPS growth in 2024 of -5 %, 2025 of 12%, and 2026 of 21%. Seems like today might be a good time to jump in before the growth takes off, right?

{kind=link}

Here is one from an article written in June of 2023, just a few months ago. At the time, the expected EPS in 2023 was $4.49, and 2024 was $4.78. Today, analysts are projecting $4.00 and $4.25, respectively.

{kind=link}

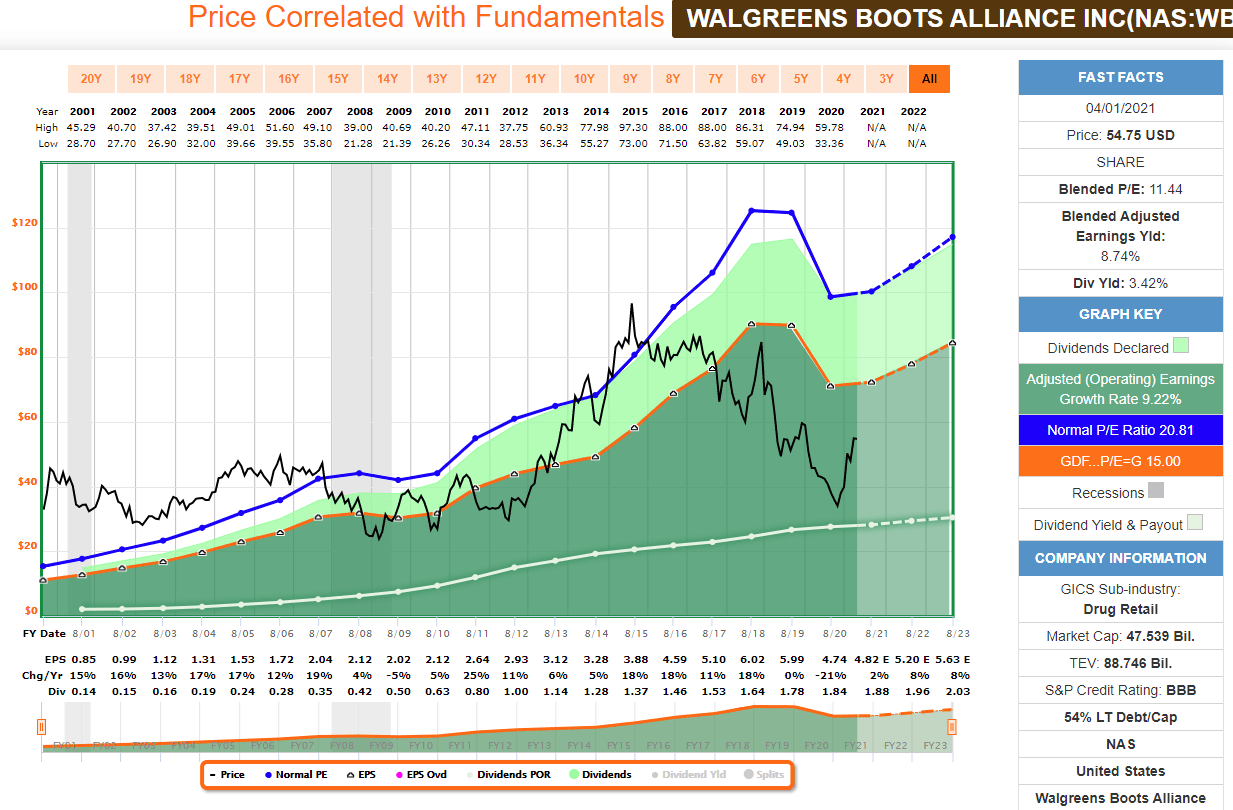

And finally, here is one from April of 2021. At this time, earnings per share were expected to be $4.82 in 2021, $5.20 in 2022, and $5.63 in 2023 . Remember, today's number is $4.00 for 2023!

{kind=link}

Walgreens is a company that, for several years, has had a brighter future right over the horizon. And given the rosy projections, it's easy to see why new investors jump in, and it always appears to be a bargain. I believe better opportunities lie elsewhere. I will continue to hold until the price rises to a point where I can replace the income or the dividend is cut, whichever happens first.

Portfolio Goals

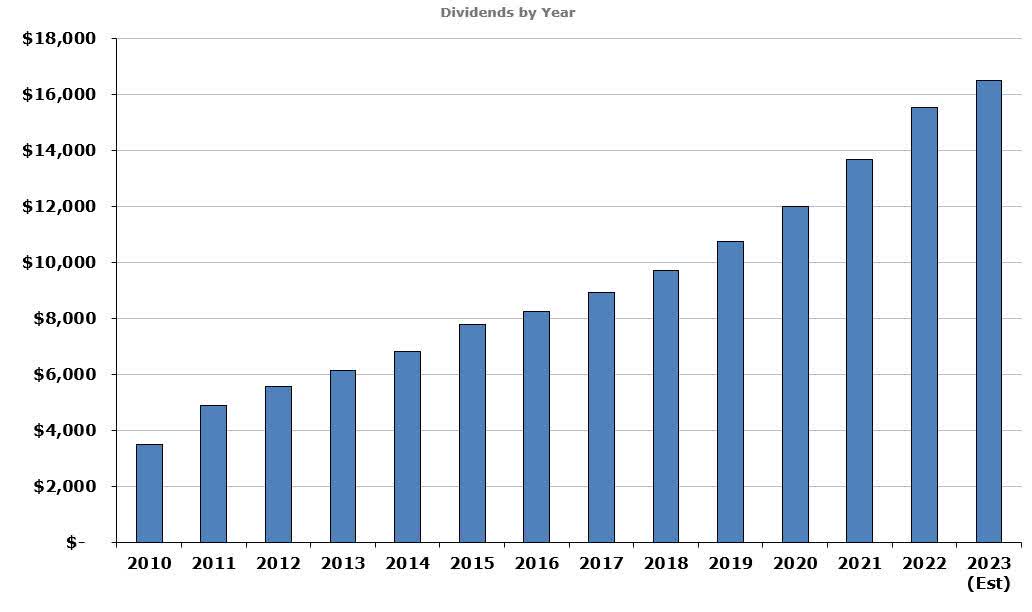

The portfolio goals are simple: Grow the income by 10% annually with dividends reinvested and 7% annually without reinvesting. This goal allows my income to double approximately every seven years while reinvesting and every ten years after I begin withdrawing the dividends. It's important to know that this portfolio has been closed to new capital since 2016. The graph below shows the steady progress of income growth.

{kind=link}

Portfolio Guidelines

I use guidelines to achieve my goals rather than rules. Rules imply something hard and fast, whereas guidelines are flexible but give a general direction to follow. I keep these simple, as I have found that complexity adds time without any real benefit. These have evolved over the years, the most recent being the addition of selling covered calls in certain circumstances.

- Invest in companies from the Champions and Contenders list with at least 15 years of dividend growth.

- Look for companies with a 3% starting yield and the potential to maintain a 7% dividend growth for decades. The growth is critical as it's impossible to continue growing income at 7% without reinvesting unless companies raise distributions by at least that amount.

- Replace (or sell covered calls against) significantly overvalued positions if the opportunity exists to reduce risk and increase income. In practice, this usually means higher quality at a higher yield.

- I want to see flat to mild payout ratio creep. A payout ratio growing from 30% to 35% over ten years is acceptable. One that has gone from 30% to 60% is not. I want companies to grow the dividend with earnings, not by increasing the payout ratio.

- Unless it is well-diversified across industries, no single sector should account for more than 20% of the income. This burned me in 2016 when several energy companies cut dividends.

Again, these are just guidelines and are flexible to accommodate what makes sense to achieve my overall goals. I follow a few other items but don't see them as integral to my investing. Instead, these tend to be more personal preferences. They include avoiding foreign companies because I don't enjoy accounting for the taxes and FX rates causing fluctuating dividends.

How am I doing so far in 2023?

As I wrote last month, I won't reach my 10% dividend growth this year. With a 5% yield on cash, I expect much better bargains to reinvest, and the companies I want to add (or buy more of) in this portfolio have yet to be at prices I want to pay. As a result, I currently hold over a year's worth of dividends as cash.

At present, I am projecting a final number of 7.9% dividend growth for the year. If I include interest earned on cash, it would be closer to 11%. However, I am still trying to figure out how or if I should include the return on cash.

While the total return isn't a goal of the portfolio or something I particularly watch, it is something readers are interested in, so I report it here. Through the end of August, the portfolio is up 10.1%, significantly trailing the S&P 500. On a 1-year basis, however, the portfolio is still slightly ahead of the S&P.

August's Dividend Increases

There was only one increase last month, Altria (MO), and they behaved as expected. The company announced a 4.3% increase, right in line with my projections. I believe raises like this will be the norm in the future. This raise is significant to my portfolio as MO contributes 11% of the total income.

September's expected increases

September kicks off the busy fall season for increases, a nice change from the slow summer months.

Honeywell ( HON )

Honeywell is a micro position in the portfolio at less than 1/2% of the value. The position was established in 2018, and the price just hasn't been right to increase it.

Honeywell has consistently raised in the 5% range for the past few years. While they could afford a more significant raise, they most likely stick to the 5% range.

Lockheed Martin ( LMT )

Since reaching the high end of its historical dividend yield range in the fall of 2021, Lockheed Martin has soared in price. The company has been giving 20 cent raises since 2018. Another 20-cent increase would equate to a 6.6% increase. I would like to see a bigger boost, but this is not the year. LMT is in one of the largest positions in the portfolio both by value and income and accounts for 3.5% of the dividends collected.

Philip Morris ( PM )

I initially received PM shares in the split from MO, although I have added several times over the years on the expectation of growth. But this company has disappointed as a dividend growth company, to say the least.

PM has a 5-year dividend growth rate of 3.7%, and last year's was an abysmal 1.6%. I'm optimistic that this year's will improve, but I expect it will still be sub-3 %. This is disappointing as the company is one of the most significant positions at 4.3% of the portfolio and accounts for 7.5% of the income.

Texas Instruments ( TXN )

Texas Instruments has been a dividend growth all-star with a 5-year dividend growth rate of 17% and a 10-year dividend growth rate of nearly 21%. Last year's increase was much smaller at only 7.8%, and I would like to say this was an aberration. However, given the company's upcoming capital commitments, investors should be happy with mid to high single-digit increases for the next few years.

Texas Instruments is another large position in the portfolio and is the 6th largest dividend contributor at over 3.6% of the total income.

Microsoft ( MSFT )

Microsoft was added to the portfolio when 3% seemed like a reasonable yield for the company. I couldn't see adding it to the portfolio today, but it continues to be a fantastic dividend grower. The company has provided highly consistent raises in the 10% range for over a decade, and I see no reason to expect anything different this year.

While Microsoft is the second largest position in the portfolio, behind only Ameriprise (AMP), it only contributes 1.7% of the total income.

Starbucks ( SBUX )

Starbucks has had a slowing dividend growth rate. While the 10-year dividend growth rate stands at over 18% and the 5-year at nearly 14%, the last couple have been below 10%. The dividend growth rate has fallen steadily for the previous ten years. This year's increase should be sub-10 % again, although the future looks promising for double-digit increases.

Sales and Purchases in August

None. I continue to accumulate cash. More on this in my closing thoughts.

What Else I am Watching

While I have quite a few companies showing up on my watch list as potential bargains based on historical dividend yields, I have concerns about many of them in the current environment. None of them would be on my list if I didn't think they had long-term potential; however, I'm not rushing into anything right now.

Many of the companies at the top of my list are banks or retailers, both of which I'm avoiding now. The exception is Tractor Supply Company ( TSCO ), which I like close to $210.

Medtronic ( MDT ) and CVS Health ( CVS ) are still high on the list. I'm not rushing to buy more MDT, as we may have seen a long-term reset in its valuation. CVS is a decent if uninspiring bargain.

Verizon ( VZ ) just raised its dividend and is high on my list. The company might be a good choice for someone looking for a high-yield position. Rarely has the company offered such an attractive yield.

The most attractive bargains right now are Kroger ( KR ) at close to $45 and Tractor Supply near $210. Nexstar ( NXST ) is yielding near 4% and is the highest rated on my tracking sheet, and I am considering starting a speculative position. Finally, Texas Instruments is moving up the list and is a solid bargain, although I would like to see it below $160.

Final Thoughts

As has been the case for much of the year, I continue to accumulate cash. At a 5% (nearly) risk-free yield, I will continue to insist that dividend growth investors should demand better bargains than over the last few years.

In 2021, when cash yielded zero, it made sense to accept sub-par bargains as the missed income and dividend growth would crush cash. At 5%, I estimate I can wait 2-3 years for the deal I want. This timeframe is on an income basis. Although, if you believe the market will be up considerably, the equation changes.

No one can know what the market will do over the next couple of years. However, I expect better buying opportunities and will continue to enjoy my worry-free 5% on cash. As I opened with, being a dividend growth investor has taught me a lot of patience!

For further details see:

My Dividend Growth Portfolio August Update - Waving Goodbye To Walgreens