ET - My Top 2023 Pick: Genesis Energy

Summary

- Genesis Energy had a positive year featuring multiple "beat and raise" quarters and issuing healthy guidance for 2023, yet units are down 20% from earlier this year.

- While debt levels are a concern, they are rapidly coming under control as EBITDA grows.

- Genesis is roughly 4 quarters away from generating significant FCF after expansion projects are completed which can be used to repay debt and rapidly delever.

- Genesis's two major business units are recession resistant and own nearly irreplaceable assets.

- Genesis units could offer investors a total return triple in 2 years.

Tell me if you're heard this story before: a Master Limited Partnership that has been paying out far more in distributions than prudent gets itself into trouble when a Black Swan event (COVID) happens and has to drastically cut distributions and sell a portion of its assets. As a result, the unit price is decimated, leaving current unitholders hopelessly underwater and swearing they'll never touch this or any other MLP again. Sound familiar?

Genesis Energy ( GEL ) certainly fits this description, and its unit price is significantly below where it was pre-COVID despite EBITDA fully recovering and the company issuing bullish guidance for 2023. This is providing a compelling opportunity as the company owns extremely valuable assets and is in the middle of a turnaround that the market is not yet giving it credit for.

Genesis Energy At a Glance

As is normal with my writing, I'm not going to spend pages repeating what is in the investor deck . There are many articles that dive deeper into the company's background and history, and I encourage you to read both them and the investor deck, which is very detailed, before considering an investment.

{kind=link}

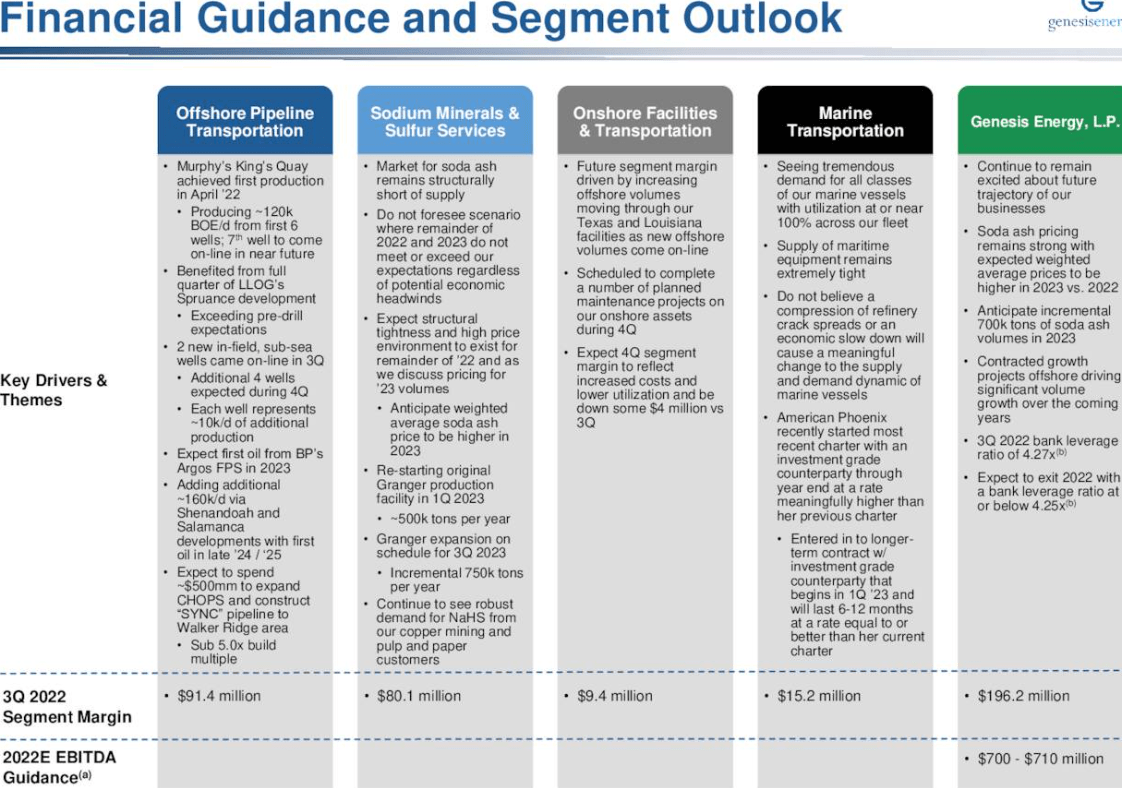

Genesis Segment EBITDA (Genesis Investor Presentation)

I'm going to focus on Genesis' two main business that will drive the valuation

- Offshore Pipeline segment, which owns nearly irreplaceable pipelines in the Gulf of Mexico.

- Sodium Minerals and Sulfur Services segment, of which natural Soda Ash production is the major product.

Both of these businesses are performing well and growing, and have a significant number of catalysts over the next 18-24 months which I believe will result in Genesis rerating.

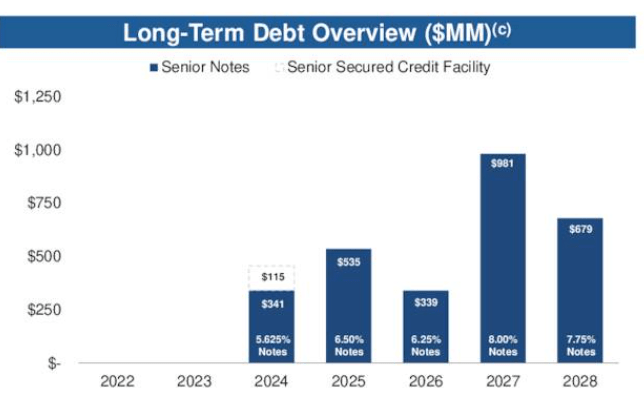

Genesis Capital Structure

Genesis Energy has an Enterprise Valuation of roughly $5 billion, of which $4 billion is made up of debt and preferred equity.

Genesis Capital Structure (Genesis Investor Presentation)

The level of debt is what adds risk to this investment, but is also part of the reason the unit price is so low. The company is deleveraging quickly by growing EBITDA and has called out deleveraging as a corporate priority. Insiders, which own a significant amount of units, likely also realize this is a big factor in the current low valuation, along with the much smaller distribution compared to historic levels.

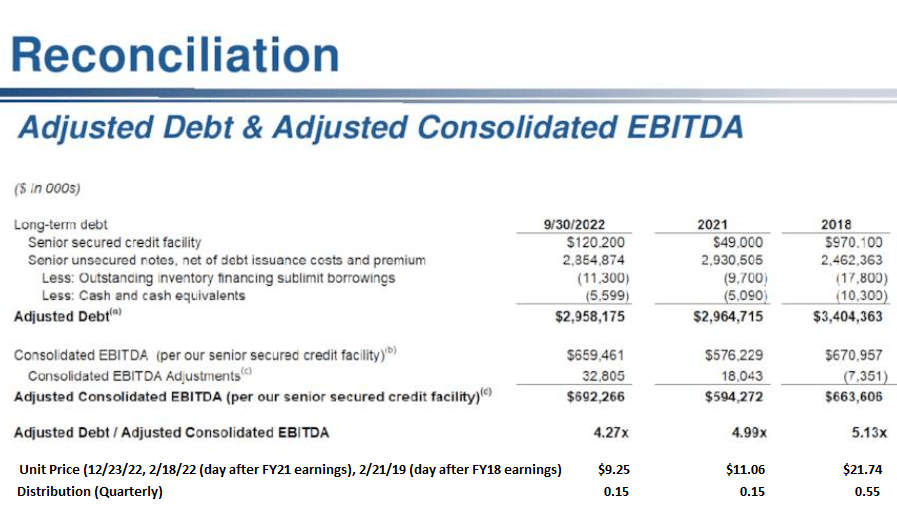

EBITDA has grown rapidly this year, and as a result leverage ratios have improved and are down from over 5x to 4.2x in the last quarter.

{kind=link}

Genesis Debt Schedule (Genesis Investor Presentation)

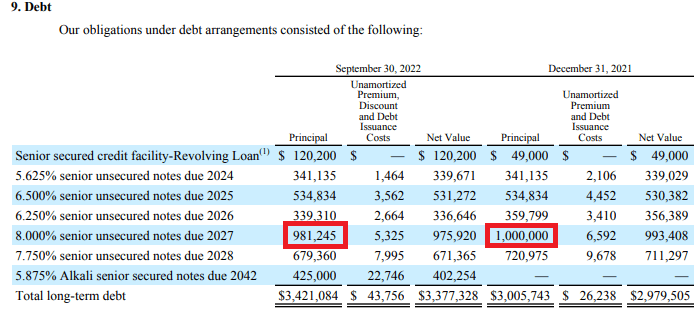

Showing a focus on debt levels, Genesis has even been quietly repurchasing some of its 2027 Senior Notes in the open market when these issues have traded at a discount.

{kind=link}

Genesis Energy Debt Schedule (GEL Q3-22 10-Q)

In addition to the debt, there is a significant amount of convertible preferreds outstanding.

Genesis Preferred Equity (Genesis Energy Investor Presentation)

The amount of interest Genesis pays is certainly the most concerning part of this investment, but it is rapidly coming under control by two businesses that I believe have extremely bright futures.

Genesis CapEx Plans - When will we see the real Free Cash Flow?

2022 was a year where Genesis paid a small distribution while retaining most FCF to pursue two major growth projects

- The Granger soda ash plant reopening and expansion, a roughly $350 million expansion. The majority of this CapEx is due to be spent in 2022 per Grant Sims on the Q4-21 Conference Call . Granger is set to reopen in early 2023, and the expansion should be online by Q3.

- A $500 million expansion of its offshore pipeline system to connect two major new oil fields to be completed in late 2024.

I expect 2023 will be a year similar to 2022 in which FCF will be used to finish funding these projects.

In 2024 and beyond, Genesis will have ample FCF (I will cover in detail below) which I believe they will use to rapidly deleverage and increase the distribution, which could lead to a rerating of the units.

Offshore Pipeline Business and Valuation

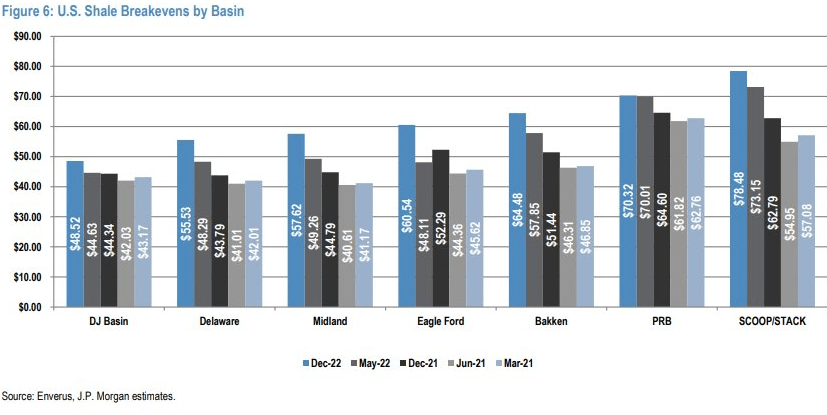

I'm bullish on the future of oil in general, and Gulf of Mexico offshore oil in particular, as the economics become increasingly compelling as compared to shale. While shale oil offers far faster time to production, breakeven prices continue to drift higher due to a combination of less well productivity and an increase in material and labor costs.

{kind=link}

Share Breakevens (JP Morgan estimates)

While Gulf of Mexico offshore production has lots of its own challenges, the breakeven oil prices offering compelling economics for new developments, especially projects that reuse existing infrastructure. In this article in the Journal of Petroleum Engineering, Shell estimated breakeven costs under $35/bbl for medium sized floaters, like the Independence Hub to be used in the Salamanca development project.

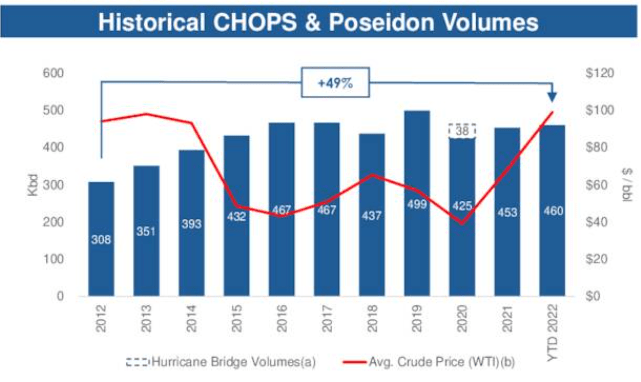

Volumes in Genesis's two major GoM pipelines, CHOPS and Poseidon, have grown decently when you consider there were two major oil crashes in this timeline.

{kind=link}

Genesis Offshore Pipeline Volumes (Genesis Investor Presentation)

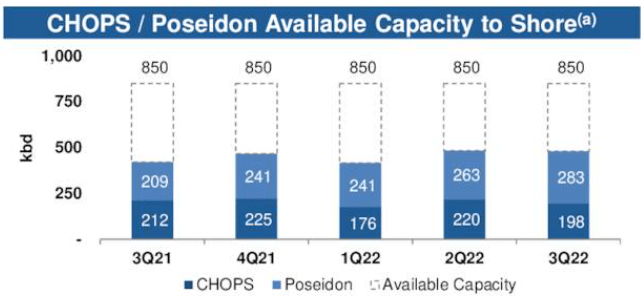

Both pipelines have significant spare capacity, which if/when is contracted, results in FCF for Genesis without having to spend much additional money.

{kind=link}

Genesis Offshore Pipeline Volumes (Genesis Investor Presentation)

The positive news is that a significant amount of this capacity is due to be filled over the next two years.

- Murphy Oil's ( MUR ) King's Quay FPS is already online and the project looks like a home run. According to Murphy's latest public disclosure, King's Quay is producing volumes in excess of 90,000 barrels of oil equivalent per day from only 5 of the 7 original wells, and are expected to bring the sixth and seventh wells online in the near future and are working to increase the capacity beyond the original design capacity of 85,000 bpd of oil and 100 mcf over the remainder of the year.

- BP's ( BP ) Mad Dog 2 field with 140kpd should be coming online sometime in mid-2023. BP has not publicly explained the delays, as this field was supposed to come online in late 2022. But the wells for this field are already drilled, and I expect the project to come online soon.

Genesis Offshore Pipeline Key Events (Genesis Investor Presentation)

- Beacon Offshore Energy's Shenandoah project and LLOG's Salamanca project, which represents another $100-150 in incremental EBITDA from Genesis $500 million investment to increase the capacity of the CHOPS pipeline and build a new lateral (the SYNC project) to reach these fields.

Beyond these already sanctioned projects, Genesis remains "in active discussions" with the operators of multiple infilled subsea and/or secondary recovery development opportunities, representing upwards of 200,000 barrels of oil per day in the aggregate that can turn to production over the next 2 to 4 years."

I believe in the next 3-4 years, these pipelines all become fully filled.

Soda Ash Business and Valuation

Soda Ash, generally viewed as a boring yet profitable business, is set to accelerate in the coming years partly as a result of green transition, as Lithium Carbonate requires significant amounts of Soda Ash. SA Author Michael Boyd wrote a compelling case for this 18 months which seems to be playing out judging by the strength in the price of Soda Ash.

There are some other markers to the value of this business. During the Q4-2021 Conference Call , CEO Grant Sims said

During the fourth quarter, we saw Sisecam, a multinational glass and chemicals manufacturer out of Europe, acquired a controlling stake in one of our neighbors in Green River, Wyoming. The consideration paid implied a transaction value of roughly $530 per ton of existing production capacity. This recent data point if applied to our fully expanded 4.8 million tons of production capacity would imply a valuation of over $2.5 billion for our soda ash business by itself .

Since then, Soda Ash prices have increased significantly. If this sale happened today, I would expect it to be closer to a $3-3.5 billion deal. At a $3 billion valuation for this business, Genesis could sell it and be nearly debt free.

2022 Soda Ash Pricing (Genesis Q3-22 10-Q)

Looking at this another way, this segment did $219 million in segment margin for the first 9 months of this year when manufacturing (namely auto, a major user of glass) was still constrained from the supply chain crisis. Annualizing this puts the business near $300 million, and the company has guided to 2023 pricing being above 2022.

The Westvaco facility produces 3.5 million tons of soda ash; Granger will add another 1.3 million tons. The Alkali business constitutes 75-80% of this segment's revenues. With Granger, this segment could do $350-400 million in futures years if pricing holds near current levels.

Taking the lower end of that number and assigning a conservative 10x EBITDA multiple, this segment alone could be valued at $3.5 billion.

Future Valuation from 2023-2025

Genesis has guided to a "mid $700 million" EBITDA guide for 2023 already. This likely includes half of normal run rate for BP's Argos, which is slated to come on "mid year", and half a year of Granger expansion. EBITDA in this range will yield free cash flow of ~$300 million, most of which will be used to internally fund the construction of SYNC pipeline and expand the CHOPS pipeline.

If we look ahead to 2024, adjusted EBITDA will likely be in the $825 million range with a full year's worth of Argos and Granger, with free cash flow nearer to $400 million. At this point, I expect growth capital needs to be around $100 million to finish SYNC and the CHOPS expansion, leaving $300 million over to reduce debt or increase the distribution. We'll likely see a combination of both.

In 2025, Genesis will add $100-125+ million from Shenandoah and Salamanca. Using the lower end to be conservative, we should see EBITDA of at least $925 million.

From the $925 million in EBITDA, we subtract

- $225 million in interest expense (this assumes none is paid down by then, which I find unlikely.)

- $100 million in preferred distributions.

- $100 million in maintenance capital. (It's worth nothing that maintenance capital for Genesis's business is relatively low.)

That leaves $500 million for common unit holders. With a current common unit market value of $1.1 billion, that's nearly a 50% DCF yield at today's price. Genesis could restore the distribution to $2/unit, and still have over $250 million left over to reduce debt, repurchase units or invest in high ROI projects.

In this scenario, I believe units will at least double to $20, and could go near $30 or higher if additional offshore projects are added at low cost.

Why I think we're at an inflection point

I've discussed seasonality with MLPs before. Many investors are hesitant to open a K-1 position late in the year, and prefer to open them early in the next tax year. Considering Genesis was well above $20/unit even in 2019, other investors likely have tax losses they can harvest, even considering the depreciation add-backs.

I think this year-end has been especially nasty for MLPs because of an IRS change that beginning in 2023 that will require brokers to withhold 10% of gross proceeds from sales of PTP securities and certain distributions by PTPs for any foreign holders. I even read one foreign investor complain that his brokerage/custodian is forcing him to transfer or sell the PTP he holds!

This could explain why MLP's like Genesis, Energy Transfer ( ET ) and Enterprise Products Partners ( EPD ) have underperformed pipeline C-Corps like Williams ( WMB ) and Kinder Morgan ( KMI ) over the past 2 months (especially in the case of KMI, which I think gave pretty weak guidance for 2023.)

Conclusion and Recommendations

Genesis has had a 2022 that has frustrate even the biggest bulls.

Back in 2018, Genesis unit price was more than double the current price despite having a full turn higher debt and lower EBITDA. Why? The higher distribution, of course!

{kind=link}

Genesis EBITDA (Genesis Investor Presentation, Authors Calculations)

This year has been mostly all good news, but the unit price has not reacted.

- FY21 Earnings Release: Provides FY22 EBITDA guidance of $565-$585 million, which is an apple-to-apples $50-70 million increase over FY21 (FY21 included $70 million in payments from a legacy CO2 business that is not present in FY22 and beyond.) Unit Price: $11

- Q1-22 Earnings Release: Guides towards higher end of previously announced range not including the gain from selling independence hub. Announces two major oil development takeaway agreements. Unit Price: $12.36

- Q2-22 Earnings Release: Excellent quarter, raises EBITDA guidance (after removing sale of Independence Hub and other one-time items) to $633-643 million. Kings Quay is coming online. Unit Price: $9.99

- Q3-22 Earnings Release: Raises EBITDA guidance again to $661-671 million (ex one-time items) guides to a "low-mid" $700's EBITDA in FY23. Unit Price: $11.62

Current Unit Price: $9.25!

So after 2 very significant EBITDA raises, a healthy guide for FY23, a significant value added takeaway project announced (albeit with a significant capital spend requirement), one of the two major GoM fields (Kings Quay) coming online with Agros/Mad Dog 2 coming soon, Granger about to reopen into a strong soda ash market, and the unit price is down 20% from the start of the year?

I think this is a mispricing which will correct itself early in 2023. I expect Genesis to report a strong Q4 and units re-rate back above $12 early next year and go higher from there. I believe a total return triple inside of 2 years of a very real possibility.

Best of luck to all in 2023 and thank you all for reading.

For further details see:

My Top 2023 Pick: Genesis Energy