LAC - NACCO: Potential Growth Catalysts In 2023 But Hold For Now

Summary

- Analysts expect price increases for coal and energy minerals and a favorable outlook for lithium mining and exploration activities.

- NACCO should benefit from higher energy minerals and metals, a well-diversified portfolio and investments in further portfolio diversification.

- NACCO receives a hold rating despite the catalysts in place, as the stock price could be on the way to becoming more attractive.

Investors Should Consider NACCO Industries Given a Favorable Outlook for Energy Commodities

For the future weights of investors in US-listed equities, analysts expect a favorable outlook for energy minerals and global lithium mining and exploration activity.

As such, investors should consider the stock in NACCO Industries, Inc. (NC) as the company is positioned to benefit from higher prices of energy minerals and metals, a well-diversified portfolio, and investments in further portfolio diversification.

Shares do not appear expensive and could trigger a buy, but there is a good chance they could form cheaper entry points in the short term. Therefore, a hold rating seems more appropriate for the time being.

Analysts Expect Higher Energy Minerals and Energy Transition Metals Prices

Coal, which is trading at $400.65 per ton at the time of writing, should hit a price target of $488.71 per ton before the end of 2023, up over 20% from current levels.

Analysts expect coal demand to remain resilient while supply tightens. Demand will be impacted by above-average European demand as the loss of Russian natural gas supplies has to be replaced with coal for power generation. In addition, the increase in electricity demand due to heat waves in the southern hemisphere and harsher-than-expected winters in the northern hemisphere will require the commissioning of additional coal-fired power plants. On the supply side, analysts are weighing the damage to Australian coal production from the La Niña weather phenomenon, which should result in lower coal exports from Australia.

With regard to other energy minerals, analysts project a 9% jump in Crude oil to $86.78 per barrel [/bbl] and a 67% soar in US natural gas to $8.51 per Metric Million British Thermal Unit [MMBtu] before the end of 2023.

Analysts expect lower crude oil shipments from Russia due to sanctions of the European Union and G7 and weigh the introduction of a price cap on the Russian commodity. Crude oil demand could suffer from potential disruptions to Chinese economic activity amid rising Covid-19 cases and a lower global economic outlook due to monetary tightening. However, upward pressure on prices from supply cuts will outweigh demand concerns.

The natural gas price will benefit from extreme cold spells in the US and storage below market expectations and well below historical averages, triggering the need to replenish reserves of the commodity. In addition, European fears about the availability of sufficient natural gas remain as long as the war in Ukraine continues.

Lithium, used in electric vehicle batteries, is trading at CNY547,500 per ton as of this writing and will reach CNY589,500 per ton by the end of 2023, up 7.7%, according to analysts. However, the target price could be revised downwards due to the expected surplus in the lithium market in 2023 as the worrying resurgence of COVID-19 cases could lead to a slowdown in the Chinese economy with a drop in electric vehicle sales.

On the supply side, according to top producers, global lithium production is expected to rise sharply next year as the mining industry continues to win contracts to produce the metal, helping to make up for shortfalls in China.

NACCO Industries, Inc. in the Energy Sector

NACCO Industries, Inc., headquartered in Cleveland, Ohio, is a resource company operating in the industry through three segments: coal mining, North American mining and mineral management.

Approximately 45% of corporate profit is attributable to the Coal Mining segment, 5% to North American Mining and 55% to the Minerals Management segment.

The Coal Mining segment includes the operation of open pit coal mines from which NACCO supplies the mineral to power generation companies and activated carbon producers under long-term contracts.

Activated carbon is needed while performing a variety of techniques, including the purification of liquids such as municipal drinking water and others. To name a few, it is also used in metallurgy for gangue processing during the extraction of precious metals and to control pollutants during industrial processes. The technology is also used to eliminate odors or purify ingredients in the processed food and beverage industry.

NACCO's customers are located across North Dakota, Texas, Mississippi, and Louisiana, and within the Navajo Nation Indian Reservation of northwestern New Mexico.

The segment shipped 7.96 million tons of coal in the third quarter of 2022 , down 11.3% year-on-year, with the negative trend expected to continue into 2023 due to the closure of supply activities from a Texas branch.

Adjusted EBITDA, which decreased 35.2% year-on-year to $10.35 million in the third quarter of 2022, is expected to decrease further in 2023. NACCO believes that inflationary pressures on input costs and higher depreciation costs will further drive up the cost per tonne of coal to be shipped from the Mississippi dark brown coal mine. Reductions in management fees at Falkirk's North Dakota coal production for 2023 and lower coal shipments following the aforementioned Texas facility closure won't help the Adjusted EBITDA either.

The reader should be aware that Mississippi lignite production facilities sell ore at contract prices, but these are subject to changes in indices reflecting inflation trends over time. However, the increase in the lignite production cost could not yet be compensated by higher contract prices and thus higher revenues, as it will take some time for the market to adjust the selling price of coal to the increased inflation.

But it must be said that since September 21, 2022 (a few days before the end of the third quarter of 2022), the Fed has made three rate hikes to curb aggressive inflation, while many traders on the US stock market were already eyeing the possibility of a change in the US FED stance. There were increases of 75 basis points [bps] with the first two decisions and a further increase of 50 basis points with the most recent decision of December 14, 2022.

Thus, if inflation affects coal sales prices later, at least on production costs, the rapid rise in interest rates could have a calming effect, especially if the economy is expected to slip into recession in 2023. Thus, an operating result that already exceeds the company's expectations in 2023 can therefore not be ruled out. Most likely, the combined positive effect on sales prices and production costs should result in impressive growth in this segment's profit in 2024.

The North American Mining segment includes the provision of value-added contract mining and other related services to miners of aggregate for the construction industry, and to miners of lithium and other minerals. This segment also provides contract mining services to independent mine and quarry operators in Florida, Texas, Arkansas, and Indiana.

North American Mining Results shipped 13.421 million tonnes of minerals in the third quarter of 2023 , down 5.6% year over year.

The segment's Adjusted EBITDA fell 44.5% year over year to $1.38 million due to lower shipments and higher labor costs despite higher selling prices.

In 2023, the North American mining segment should see an improvement in Adjusted EBITDA from 2022. This will be possible thanks to the ongoing fall in labor costs and the ramping up of mining activities in the US to make up for the portion of China's metals and minerals production that will be lost due to COVID-19.

Also, North American Mining engages in growth initiatives to increase future profits.

Under an agreement signed in 2019, NACCO will act as the exclusive contract miner for a northern Nevada lithium project owned by Lithium Americas Corp. ( LAC ), a Canadian explorer for lithium prospects in the US and Argentina. Lithium Americas will process and sell the metal.

NACCO Q3 2022 notes that Lithium Americas announced in October 2022 that this lithium project, dubbed the Thacker Pass Project, will begin construction in 2023 based on a feasibility study scheduled for Q1 2023. This asset should generate fee income in line with that of a medium-sized coal mine management fee.

Furthermore, NACCO is committed to transforming the North American mining segment into a market leader in providing contract mining services aimed at producers of a broad range of minerals and materials.

The Minerals Management segment leases its royalties and mineral interests to third-party exploration, production and mining companies, which can then explore, develop, produce and sell energy minerals.

The Minerals Management business segment reported a tremendous 54% year-over-year increase in Adjusted EBITDA to $15.215 million in the third quarter of 2022, thanks to higher fossil fuel prices and increased income from leases and mineral holdings.

Obviously, any change in the price of natural gas and oil affects Minerals Management's results.

The company said Adjusted EBITDA for the segment could decrease in 2023 compared to 2022 based on market expectations for fossil fuel prices as of September 30, 2022, and because miners should produce fewer tons.

In terms of future production, the company's expectations are not likely to be proven wrong if miners' existing wells are in the declining phase of production. However, NACCO took precautionary measures and during the third quarter of 2022 acquired certain mineral interests in the Permian Basin and Powder River Basin with the aim of increasing production levels. Further investments in mineral interests and royalties are planned for 2023.

But in terms of expectations for oil and gas, the company may have misjudged the situation. Even assuming weaker demand for fossil fuels in the event of a 2023 recession and a slowdown in China due to the coronavirus, sanctions against Russia combined with OPEC's unwillingness to ship more barrels will create strong upward pressure exerting on fossil fuel prices. It is roughly for these reasons that analysts are forecasting a surge in oil and gas prices in 2023, as outlined at the beginning of this analysis.

Stock Valuation

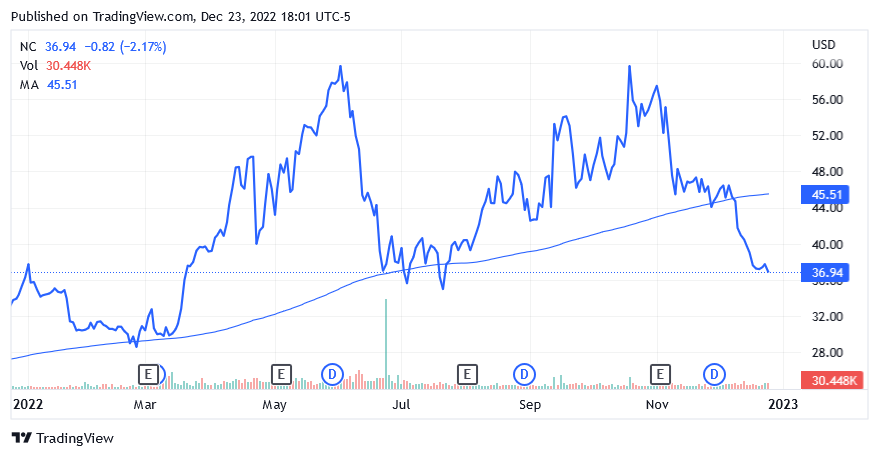

Shares of NACCO Industries, Inc. were trading at $36.94 apiece for a market cap of $277.24 million and a 52-week range of $28.42 to $63.19, as of this writing.

{kind=link}

Currently, the stock price is well below the long-term trend of the 200-day moving average of $45.51 and is also trading well below the midpoint of $45.805 of the 52-week range.

Based on these technical indicators, the share price looks cheap and would encourage an increase in the position. However, when the TTM EV/EBITDA of 10.99x is compared to the industry median of 6.78x, the stock price no longer looks as attractive.

Other comparisons such as TTM price/book of 0.67x versus sector median of 1.79x and TTM price/cash flow of 4.47x versus sector median of 4.60x paint a different story. The share price has been falling for the past two months (it is down 38% from the Oct. 19 high of $59.66) since it tracked the decline in crude oil and natural gas prices.

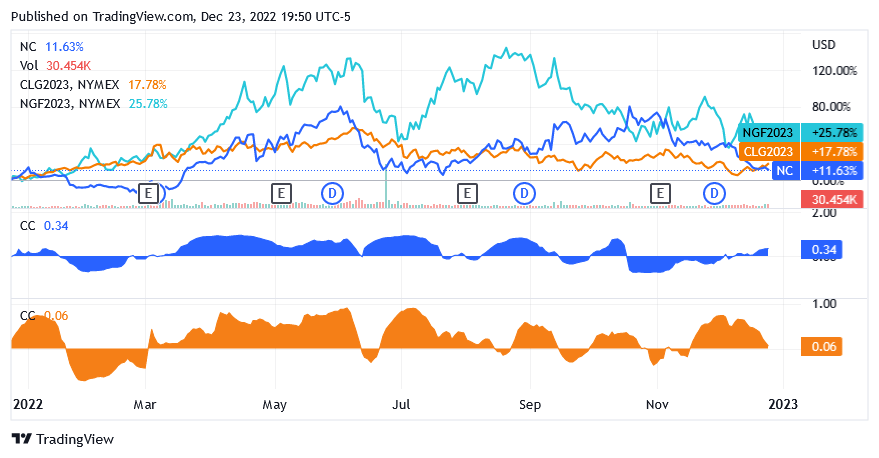

Because NACCO's performance is more similar to that of natural gas futures than crude oil, the stronger correlation between NACCO and natural gas will outweigh the correlation between NACCO and crude oil, based on trailing 12-month prices. This information will come in handy should the trends in fossil fuels have a mixed impact on NACCO's stock price in the near term. See the chart below.

{kind=link}

Given the stronger correlation with natural gas and the impact of the EU price cap agreement coupled with weather forecasts pointing to a largely mild climate in Europe through January, it is possible that NACCO could see further downside towards more attractive entry points. Therefore, NACCO gets a Hold rating for now.

Lastly, the stock offers a dividend yield of 2.20% (vs. the industry median of 3.10%) based on a quarterly cash dividend of $0.208 per share paid on December 15, 2022. NACCO has been paying dividends for about 36 years .

Conclusion

NACCO Industries shareholders are expected to benefit from higher energy mineral prices, cost catalysts and improvements in the North American mining segment.

NACCO is building an increasingly well-diversified portfolio that should allow the company to conquer many more commodity and mineral markets over the long term.

The stock price doesn't look expensive, which could trigger a buy. However, there is a good chance that the stock will become more attractive in the short term. So, investors might want to consider holding NACCO.

For further details see:

NACCO: Potential Growth Catalysts In 2023, But Hold For Now