CA - Nano One: North America's Answer To China

2023-10-04 08:15:22 ET

Summary

- Nano One is a battery technology company focused on cathode production, with a technical innovation that improves the durability and performance of cathodes while reducing production costs.

- Nano One is targeting the growing market for lithium iron phosphate batteries, especially in North America where its process innovation enables a supply chain independent of China.

- In a recent test Nano One proved the commercial viability of its cathode technology, creating an asymmetric risk/reward proposition for investors.

- The company's vast partner network should enable rapid commercial scaling through licensing and joint-venture agreements.

Nano One ( OTCPK:NNOMF ) has been one of the most exciting names in battery technology for the past few years, but doesn’t seem to get the attention it deserves. Its highly technical focus on cathode production makes its story a bit difficult to penetrate mainstream EV interest. This article will offer a deep dive into the company’s LFP opportunity, fresh off the heels of its recent success in commercial-scale LFP production tests and a discussion of its new partner , Sumitomo Metal Mining ( OTCPK:SMMYY ).

Technical Innovation

Nano One seeks to deliver process innovations to the cathode manufacturing process (for those that need a refresher on cathodes, please see this article ). The two proprietary processes under development from Nano One are its One-Pot process and metal direct to cathode (“ M2CAM ”).

Nano One was founded on its One-Pot process , which seeks to improve the durability and performance of cathodes while reigning in production costs. The process takes a novel approach to cathode crystal coating, enabled by the unique precursor CAM (cathode active material) formation.

To be clear, the idea of cathode coating isn’t really anything new in of itself, it’s been adopted by cathode manufacturers as a way to limit side reactions in the battery, thus improving longevity. Where Nano One differs is that this coating is applied while the materials are all being added together. This reduces the number of steps required (hence “One-Pot”) and yields single-coated nanocrystals.

It’s important to understand that cathodes are a powder, not some foil alloy, bound together. In a standard cathode, the protective coating forms around clumps of CAM crystals. However, these protective layers break down as the crystals within continuously expand and contrast over the course of various charge cycles. As cracks form, side reactions begin to occur and battery longevity is limited.

Nano One’s process forms a protective coating around each individual crystal, rather than clustering them together. The One-Pot process achieves this by combining all of the metal feedstocks (lithium, nickel, cobalt, manganese, etc.) with the coating material in the One-Pot reactor. This allows the CAM to crystalize and form its protective coating simultaneously, rather than applying the protective coating to groups of CAM crystals.

While it is possible to individually coat much larger crystals (which are formed by fusing clusters of nanocrystals together), it requires significantly more time in the kiln, raising costs and emissions. Nano One’s process requires just several hours in the kiln, while large single-coated CAM crystals require days.

Nano One estimates that its single-coated nanocrystals may achieve up to a 4x improvement in longevity over uncoated cathode crystals. While the delta would likely be less significant when compared to a regularly coated cathode, the single-coated cathode still demonstrated impressive durability.

Nano One

Still, the positive impact on the chemistry does provide a demonstrable advantage of utilizing Nano One’s One-Pot process. While this study is now outdated, completed over three years ago, Nano One’s various partnerships make it difficult for it to provide public updates given the sensitivity of the information. However, the consistent advancement of these various partnerships have allowed investors to track Nano One’s technical growth (more on that later).

While a powerful process in its own right, the One-Pot process also gave birth to the company’s M2CAM process, which has since become the backbone of its North American LFP efforts (more on that later).

Traditionally, in nickel-based CAMs, metals like nickel and cobalt are transformed into sulfates (i.e. nickel sulfate, cobalt sulfate, manganese sulfate) and lithium carbonate is converted into lithium hydroxide. In an LFP battery, iron phosphate is formed as a separate precursor material prior to the LFP formation.

As the name suggests, M2CAM allows cathode manufacturers to bypass these steps by transforming raw metals directly into the CAM material. Along with some supply chain benefits, this process significantly reduces waste production and carbon emissions associated with CAM manufacturing.

Take nickel sulfate as an example, which contains one nickel atom per six water molecules. As a result, nickel sulfate is 5x heavier than pure nickel, contributing to greater expenses, and carbon emissions, throughout the supply chain.

In a study led by Hatch, Nano One found that its process reduced water consumption by 60% and completely eliminated sodium sulfate waste. In traditional CAM manufacturing, sodium sulfate (a waste product) output is 1.8x greater than CAM output. On the shipping side of things, this is estimated to reduce emissions and costs by 4-5x.

Crystallizing nickel, and other CAM metals, is also a rather expensive and energy-intensive process itself. Through bypassing this step, Nano One expects to create additional efficiencies, and emissions reductions, throughout the supply chain.

In a previous article, I noted that Nano One expects its One-Pot and M2CAM processes to reduce overall costs by 13% - 20%. While the company has completed more in-depth studies , and is currently undertaking additional studies, it’s likely that Nano One will continue to limit the availability of its findings to internal stakeholders and partners. This will also change from project to project, especially with different chemistries.

The durability of Nano One’s single-coated nanocrystals has also enabled it to pursue an NMC battery chemistry without cobalt. LMN, or high-voltage spinel (“HVS”), is a majority manganese blend (about 75/25 manganese to nickel) that seeks to retain some of the advantages of nickel-based cathodes without needing to rely upon the abhorrent , and unreliable, cobalt industry.

The HVS nomenclature is rather indicative of how the cathode behaves, which is rather similar to a basic LMO cathode. The addition of nickel helps add some energy density to the high-voltage chemistry, which is well-positioned to handle rapid charge/discharge cycles (good for acceleration or fast-charging without inducing strain).

However, as I noted in my cathode overview , LMO cathodes are particularly susceptible to side reactions, limiting their lifespan. This weakness is carried over to LMN cathodes, but suppressing side reactions is the primary issue that Nano One seeks to solve with its One-Pot process.

Nano One unveiled the chemistry in 2020, comparing an untreated cathode to its One-Pot coated LMN CAM. In the untreated cathode, capacity loss was ~80% while degradation in the treated cathode was >10%. Remember, the rudimentary NMC cell recorded ~16% capacity loss after 100 cycles.

Nano One

In a follow-up report a few months later, Nano One tested the cathode in full pouch cells with a standard graphite anode. In these cells, degradation for its One-Pot cathode was ~25% over the course of just under 1,000 cycles (comparable to ~300,000 miles).

Nano One

Nano One’s LMN cathode operates at a voltage of 4.7, a 25% improvement over commercial lithium ion batteries, though its energy density does leave room for improvement. The company hasn’t released many specifics about the cathode since its initial debut, but there does seem to be solid commercial interest.

Unfortunately, without an existing commercial presence and especially as a small player in the cathode space, it may be more difficult to grow this chemistry. With more turbulent financial markets too, many cathode producers may be less inclined to take somewhat of a chance on a new chemistry. Instead, LMN adoption may be limited until there are significant alterations in battery architecture, such as solid state batteries .

In-House LFP Progress

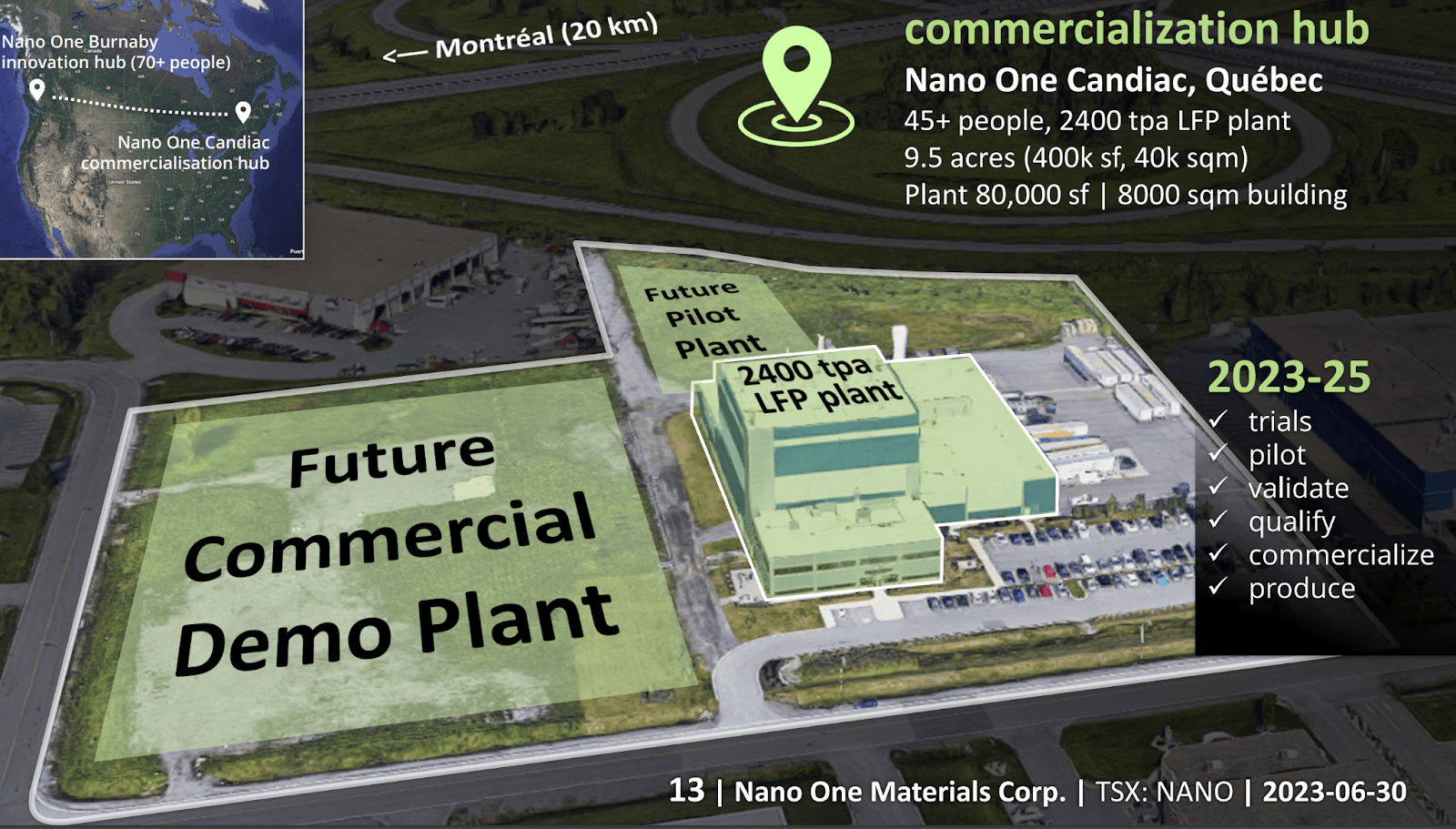

In May, 2022, Nano One announced that it would be acquiring Johnson Matthey’s LFP manufacturing site in Candiac, Québec at the end of 2022. The acquisition will allow Nano One to accelerate its development timeline by years, as the company took on over 50 employees with a combined experience of 360+ years of experience in LFP manufacturing and a fully-functional LFP facility.

While Nano One will be altering the manufacturing process, it will be able to retain ~80% of the existing equipment at the facility. For more information about this acquisition, see this article . The company began One-Pot trials in January , after fulfilling all of JM’s prior contract obligations.

In April, Nano One outlined its plans to retrofit the Candiac facility with its specialized One-Pot reactors, starting with 200 tpa LFP in 3Q and scaling up to 2,000 tpa in 2024. This marks a massive increase over the company’s 10kg batches, which were produced under the second SDTC program.

As Nano One continues to work on retrofitting the Candiac facility with its specialized One-Pot reactors, it has been conducting One-Pot trials with the existing 2,000 tpa commercial reactors. These tests yielded LFP “at commercial scale with performance results consistent to lab scale.”

Moving from lab scale to commercial scale always introduces some challenges, as it’s much more difficult to control all of the reaction parameters as scale increases (especially heat and general uniformity). By producing high-quality LFP samples in commercial scale batches, without its specialized reactors, Nano One has proven the viability of its One-Pot process at scale .

The company plans to ship tonne samples, produced from the existing 2,000 tpa reactors, to strategic partners in Q4. This is well ahead of schedule, which the company expects to accelerate the transition of the existing commercial scale reactors to One-Pot. Nano One expects to achieve a continuous production run rate of 2,000 tpa by the end of 2024.

While tests in the existing commercial reactors were advancing, Nano One was also in the process of installing its 200 tpa One-Pot reactors. These will allow the company to trial automated, continuous, production of its One-Pot process prior to its 2,000 tpa continuous run rate targeted for next year.

The smaller scale reactors may also be used to serve initial commercial offtake agreements, following customer validation. The reactors had all been received, and installed, as of this September update and the company is now working on optimization design before trials begin.

As a reminder, the primary competitive advantage that is enabled by Nano One’s One-Pot and M2CAM processes is the ability to remove the preliminary step of manufacturing iron phosphate. Iron phosphate is manufactured exclusively in China, with little viability of being produced elsewhere. As a result, Nano One offers the only opportunity to completely cut China out of the LFP supply chain.

{kind=link}

While production at Candiac will remain an independent endeavor, Nano One remains open to pursuing JVs and licensing opportunities with interested parties on LFP as well.

Sumitomo Partnership

Earlier this week, Nano One announced a collaboration agreement with Sumitomo Metals Mining (“SMM”), which includes a C$16.9 million investment from the Japanese company as well. The agreement comes off the heels of Nano One’s LFP update, in which it successfully demonstrated the commercial validity of its One-Pot process.

As Katsuya Tanaka, Managing Executive Officer, General Manager of Battery Material Division of SMM stated, “Nano One has proven LFP production experience and has demonstrated that their latest technology works at scale, their materials perform, and their costs are competitive.”

The collaboration agreement will be focused on accelerating Nano One’s commercialization of LFP and nickel-rich cathodes. Sumitomo Metals has been a pioneer in the high-nickel cathode industry, remaining the largest producer of NCA cathodes since Tesla’s ( TSLA ) introduction of the Model S.

Avicenne Energy

In 2021, SMM announced a $424 million plan to increase its cathode output to 10,000 tonnes per month, doubling its current output. The company expects to reach this output by 2027, splitting output 60/40 in favor of NCA over NMC. For these high-nickel chemistries, the company’s annual output of 120,000 tonnes would service approximately 92 GWh of batteries annually.

However, LFP is a focus for this partnership as well. Early last year, SMM announced that it had reached an agreement with Sumitomo Osaka Cement to receive the latter’s LFP battery materials business. Sumitomo Cement has been developing LFP materials since the 1980s, first opening a production site for LFP material in December 2012.

The Vietnamese production facility is one of the only operational LFP facilities outside of China. By partnering with Nano One, SMM hopes to accelerate the production ramp of its newer LFP business, which wasn’t initially included in the company’s 10,000 tpa cathode production forecast.

As a vertically-integrated cathode producer, SMM is also in a uniquely strong position to utilize Nano One’s M2CAM process as it has significantly more control over its raw material supply. Regarding the future of the two companies’ collaboration, the press release went on say:

“In the future, the Companies intend to evaluate and negotiate a longer-term partnership in the form of a joint-venture and/or a licensing agreement for large scale production of LFP, NMC and other CAM formulations using Nano One’s One-Pot process in Asia (excluding China) and other global jurisdictions such as Europe, North America and the Indo-Pacific region.”

It’s also worth noting that this collaboration announcement came just three days after Canada and Japan signed a memorandum of cooperation “to strengthen supply chains for storage batteries used in electric vehicles.” The agreement seeks to reduce China’s strength in the global EV supply chain and increase production of batteries, and battery materials, in Japan and Canada.

As CBC wrote , “While no contracts or specific funding will be finalized on this trip, the Japanese business representatives are expected to sign memoranda of understanding with Canadian companies with whom they intend to share technology and business intelligence.” It appears that Nano One has become one such company, opening Nano One and SMM to now receive support from both Canada and Japan on their developmental, and commercial, endeavors.

The memorandum also includes a commitment from both countries to provide financial support for lithium projects in Canada.

LFP Market Opportunity

With cathode-agnostic technology, Nano One’s platform can address the entire EV battery market, albeit within quite a tight niche of that massive market. However, for the purposes of this article, I will be focusing on its LFP opportunity (see the full article on Green Growth Giants).

Still, given the market’s massive scale, Nano One doesn’t plan to go at this alone. Instead, it plans to pursue licensing arrangements and joint ventures, in addition to its Candiac facility.

A JV would follow a shared-cost structure, resulting in far greater top-line sales for Nano One. Assuming a sales price of ~$23/kg ( 80% of CAM cost is raw material) for LFP cathodes and a gross margin of ~15%, the JV structure would generate gross profit of $3.75/kg, or $1.88/kg for Nano One.

Forecasting licensing revenue, and profitability, is a bit more difficult as Nano One doesn’t provide any guidance on what its licensing arrangements may look like due to its commercial sensitivity. However, I would expect the company to charge around $1 per kg for its LFP cathodes.

In the LFP market, Nano One will likely debut as a standalone producer. While the company has no plans to expand its in-house manufacturing efforts beyond the Candiac facility, there is significant room for expansion at the site. Nano One also remains open to licensing and JVs to expand the scale of its LFP product.

From its 2,000 tpa pilot facility, Nano One plans to move to a commercial facility with an initial 10,000 tpa production line. Nano One is currently undertaking a detailed engineering study to evaluate the actual size of their future commercial lines, as well as how many lines they plan to invest in.

While it isn’t yet clear what the individual production lines will look like, the company expects to eventually reach an output of “hundreds of thousands of tonnes per year” at the facility as the LFP market continues to develop, especially in North America. Assuming a sales price of $23/kg for LFP and a gross margin of 15%, Nano One stands to generate gross profit of ~$34.5 million at a rate of 10,000 tpa.

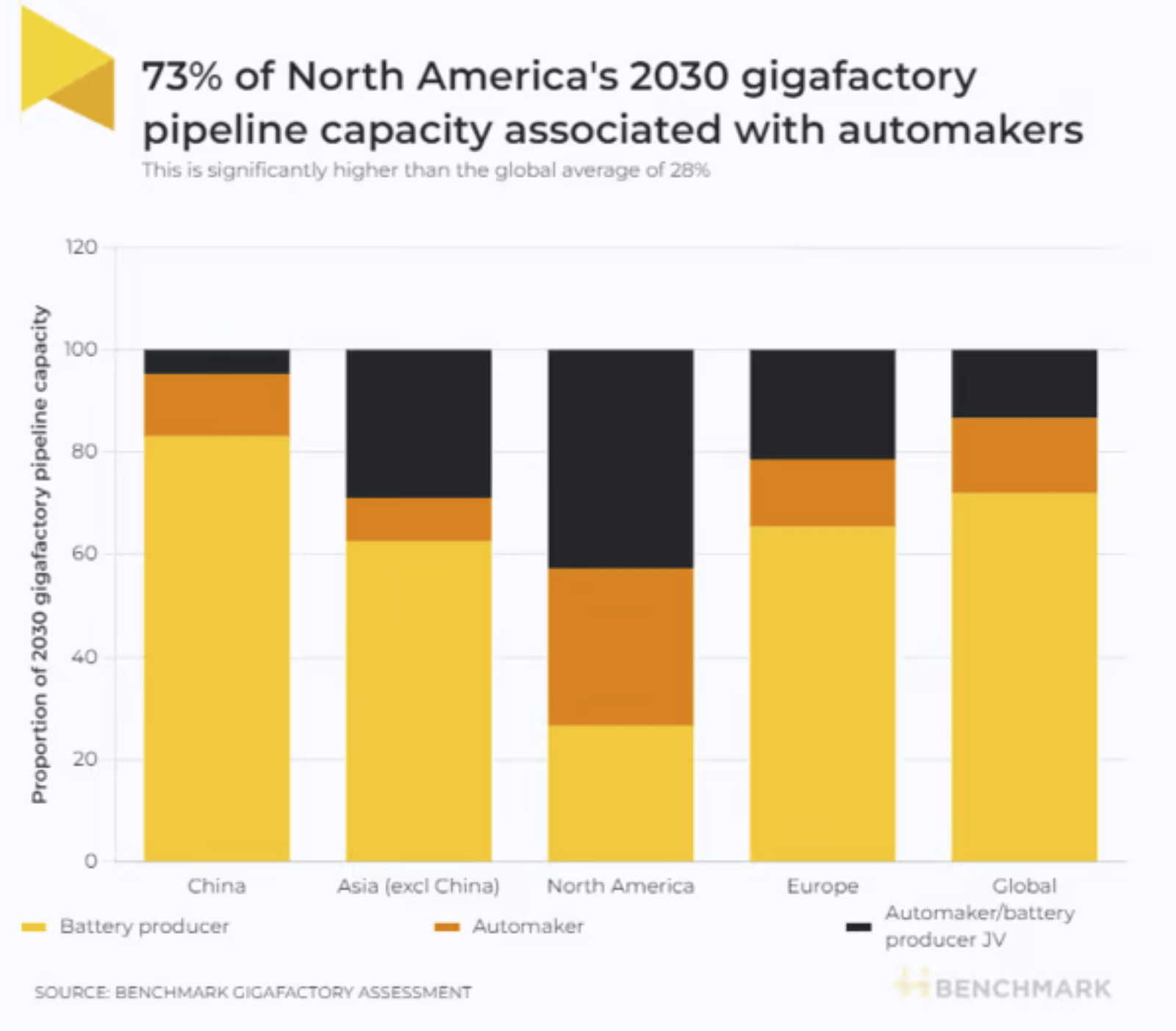

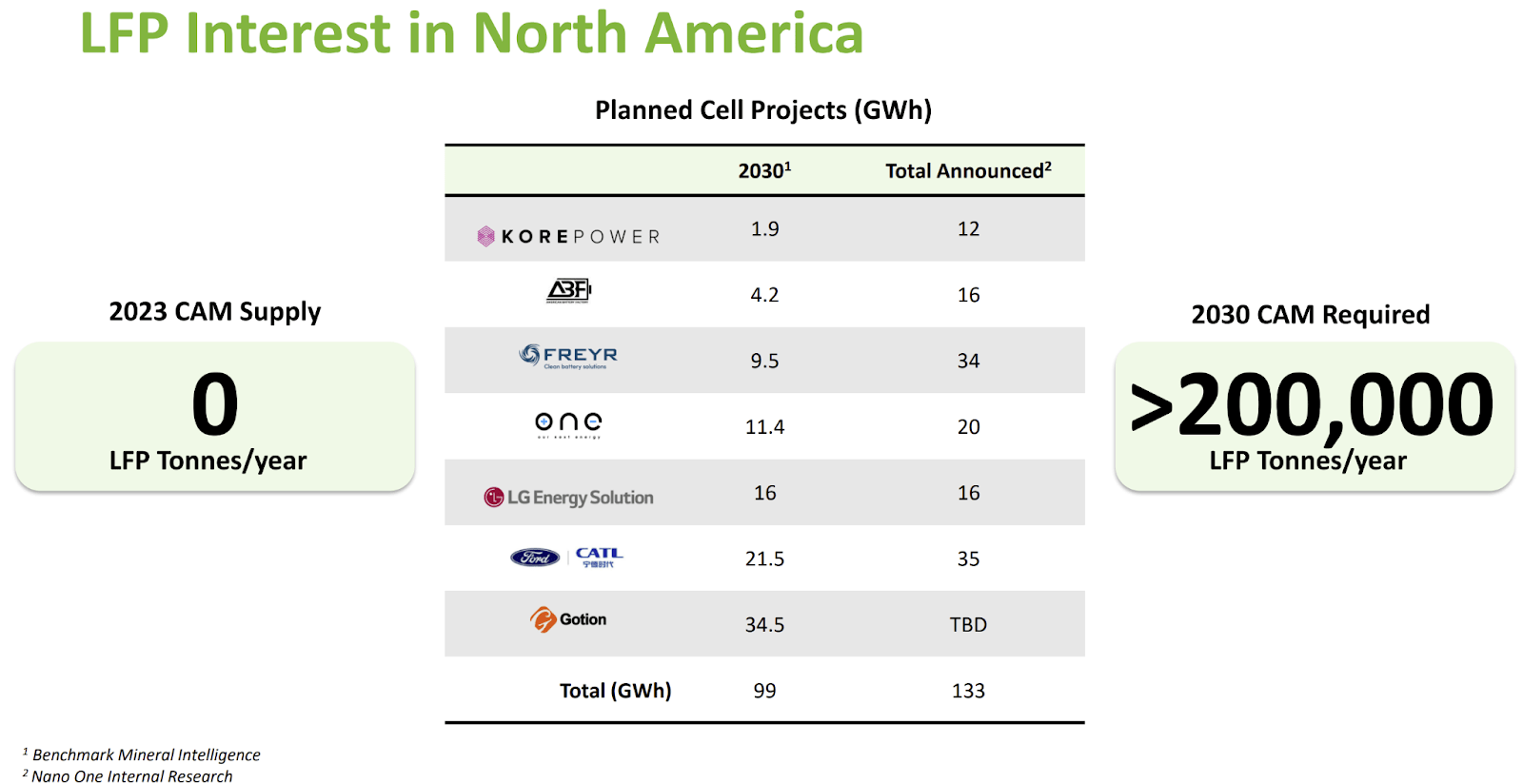

This facility is currently the only LFP manufacturing site in North America, which makes it extraordinarily important to US automotive OEMs. In order to qualify for the EV tax credits, a significant portion of a vehicle’s battery components need to be manufactured in North America (more on that in this article ).

Currently, automakers are responsible for nearly three quarters of America’s gigafactory pipeline, far greater than the 29% global average. This is indicative of how critical OEMs view these tax credits to be for their market success.

Benchmark Mineral Intelligence

{kind=link}

As automakers like Ford ( F ), Tesla ( TSLA ), and General Motors ( GM ) all strive to introduce more LFP-based EVs to the American market, they will need to source LFP cathodes from North America in order to receive the full benefit of the low-cost battery chemistry. As such, Nano One’s Canadian facility should generate incredibly high interest amongst US automotive OEMs.

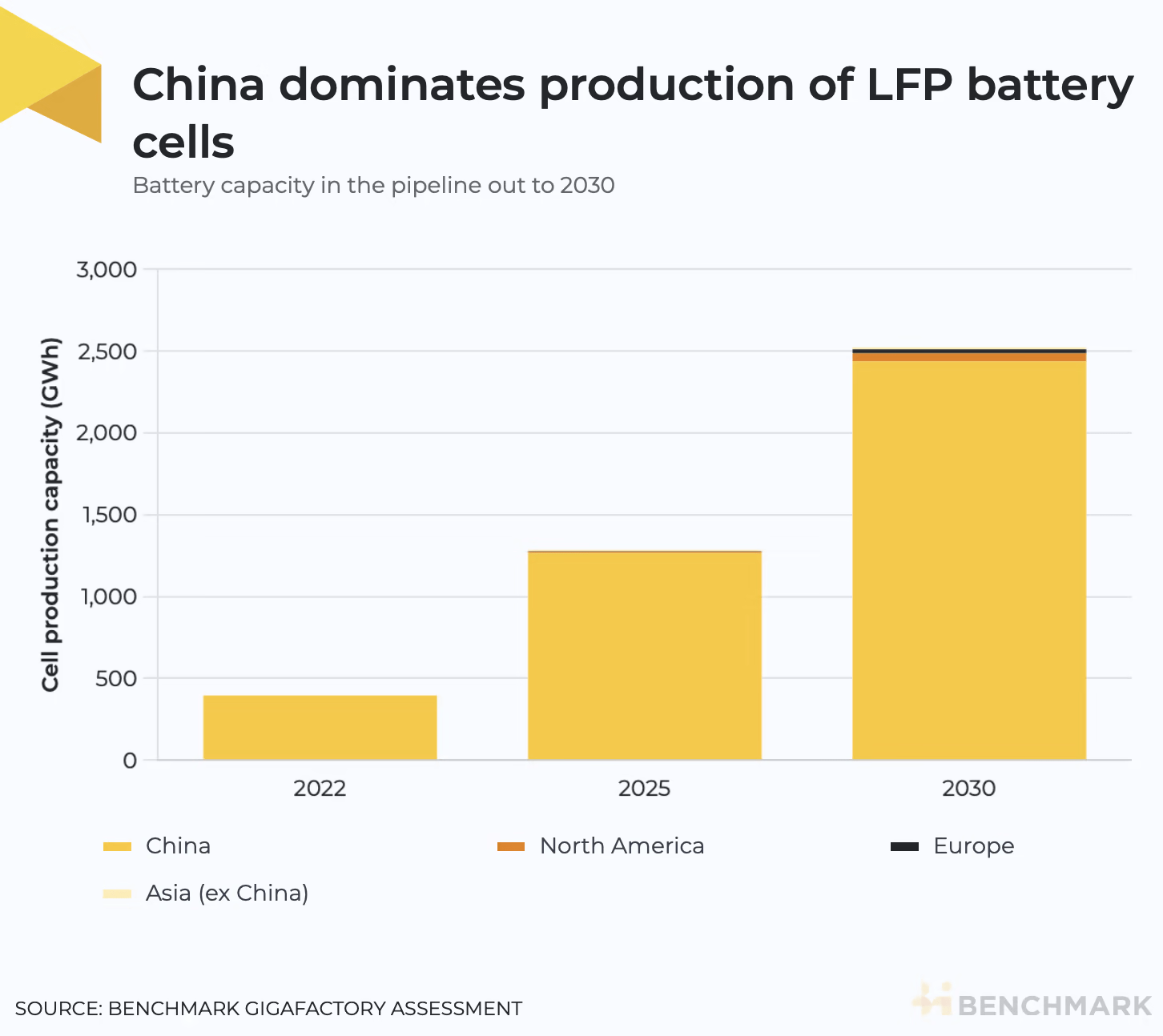

As of February, Benchmark Mineral Intelligence (“BMI”), estimated that the announced US gigafactory pipeline implied LFP battery manufacturing capacity of 8 GWh by 2025 and 49 GWh by 2030.

Benchmark Mineral Intelligence

{kind=link}

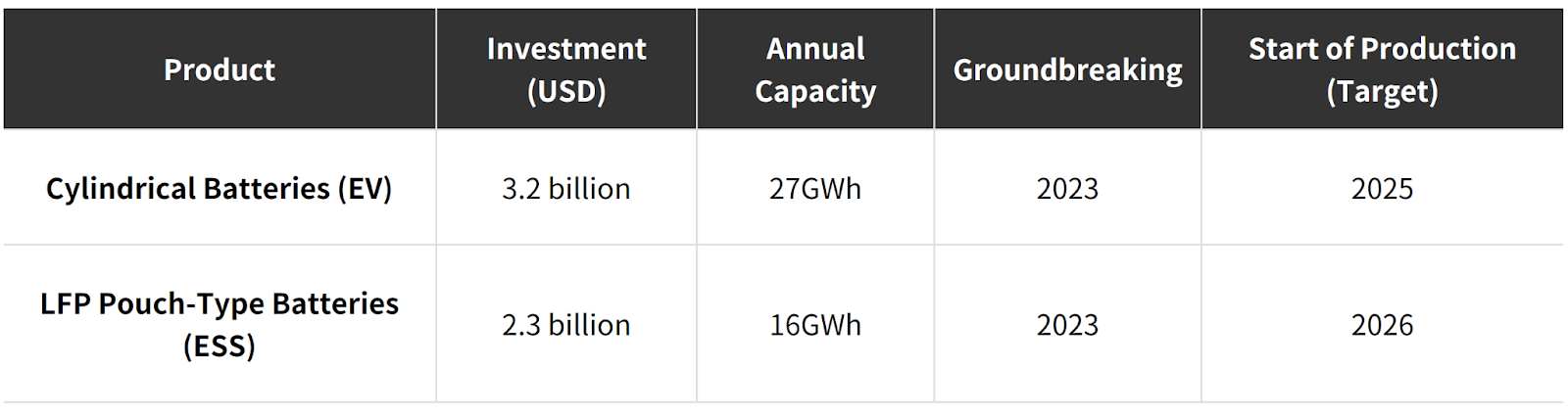

Just a month later, LG Energy Solution announced a $5.4 billion investment in a 43 GWh LFP battery facility. Capacity will be divided between EVs and grid storage, with 27 GWh going toward EVs and 16 GWh for energy storage. In the announcement, LG specifically called out “customers’ needs for locally manufactured batteries in response to IRA tax credits and surge in market demands.”

{kind=link}

LG plans to start producing its EV cells in 2025 and its energy storage cells in 2026. This announcement nearly doubled BMI’s 2030 estimate of announced LFP capacity in North America, up to a total of 92 GWh. Prior to LG’s announcement, BMI estimated LFP capacity for 2025 at 8 GWh. These figures (8 GWh in 2025 and 92 GWh in 2030) imply demand of 16,000 tonnes in 2025 and 184,000 tonnes in 2030.

{kind=link}

With Ford still the only automotive OEM to have announced LFP production capacity, I feel rather strongly that this figure will continue to grow as more automakers seek to bring LFP in-house. As of January, planned battery capacity for 2030 in North America was 998 GWh . Keep in mind, this was before either announcement from Ford or LG about their planned LFP capacity, bringing the total planned capacity above 1,000 GWh.

US Department of Energy

Given this context, even 184 GWh, double the currently announced 92 GWh, seems like an awfully conservative estimate for North American LFP capacity in 2030. 184 GWh would necessitate 368,000 tonnes of LFP CAM production.

My expectation is that the US will require at least 1,250 GWh of battery production by 2030 (with ~1,000 GWh going toward EVs). I expect at least 30% of this to be dedicated to LFP, as the low-cost chemistry is best positioned to serve energy storage manufacturers and mass-market EVs. This scale would require 750,000 tonnes of LFP CAM.

That sort of scale can’t be served by Nano One alone, and the company plans to scale its LFP production through joint ventures and licensing agreements just as it does its nickel-based cathodes. While it’s impossible to reliably estimate exactly what Nano One’s market opportunity is here, given their various potential commercial routes, I do feel it’s safe to say that it exceeds $1 billion (pure licensing opportunity is $750 million assuming 375 GWh of North American LFP production).

It’s worth noting that Nano One could potentially serve as a catalyst to increase planned North American LFP capacity. There isn’t much use in manufacturing the LFP cells in the US if the LFP cathodes, or even precursors (i.e. iron phosphate), are still sourced from China. This does also support Ford’s decision to be the first automotive OEM to announce an LFP gigafactory, if it has the confidence that it will have access to a localized supply chain.

Thesis Risks

With cash reserves of C$34.403 million as of June 30 (prior to Sumitomo’s C$16.9 million investment ), and a quarterly burn rate of ~C$7.25 million, Nano One still has a solid 18 months before it will be forced to raise more capital. However, in order to scale its LFP factory, the company will need to raise more capital. It’s possible this comes with significant dilution, so investors should be aware of this, though the company has also seen significant support from the Canadian government thus far (and potentially Japan) making it eligible for future financing packages.

Receiving grants worth over C$20 million, it’s likely that Nano One will continue to receive support as it ramps its commercial efforts. The company has seen the value of its grants increase in line with its own growth, with the initial grant value doubling from its second SDTC program to its third. As Nano One’s SDTC projects become increasingly commercial-focused, it’s likely that the support it receives will continue growing significantly, perhaps in excess of C$20 million.

The company’s licensing business, on the other hand, should be far easier to scale as it wouldn’t require any initial capital investment from Nano One. Once the MCPH is operational, with financing support from SDTC, Nano One can begin to leverage that to expand partner discussions. Regardless, with no immediate financing concerns, the greatest risk for Nano One remains the commercial viability of its technology.

While I feel comfortable with this risk, due to the company’s partnership progression and LFP development, Nano One does offer little visibility into the validation work being completed due to the commercial sensitivity of the information. This creates inherent risk, especially for a company so reliant upon successful commercialization of its R&D efforts. As such, I view the more pertinent risk to be the timeline risk for Nano One.

It may take several years for Nano One to achieve commercially-relevant scale at its Candiac facility. While the company does still believe it is on track to complete major contract work by mid-2024 (both raw materials and offtake), there’s really no telling what the ramping process may look like. Potentially limited by financing and general ramping troubles, Nano One could still be over three years away from achieving commercially-relevant scale (10,000 tpa) at Candiac even if its R&D remains on track.

On the flip side, Nano One’s partners should help it achieve rapid commercial expansion for its One-Pot and M2CAM processes, assuming they demonstrate commercial viability. Furthermore, with the company able to utilize ~80% of the manufacturing equipment already in place at Candiac, it stands to reason that commercial partners would be able to re-tool their existing facilities relatively easily.

Still, it’s incredibly difficult for R&D projects to remain on track as any number of unforeseen complications may arise. If there is timeline drift due to difficulties with R&D, Nano One may be forced to raise more capital before truly demonstrating the commercial viability of its processes. This may create more dilution, diminishing the returns for investors.

Furthermore, simply because Nano One demonstrates it has a better process doesn’t mean it will be adopted immediately. Partners may be unwilling to shut-down a facility and re-tool, even if 80% of the equipment can be carried over, for a slight improvement in product quality and reduction in production costs.

This could limit adoption to only new facilities, or expansion lines at existing facilities. Still, the rate at which the battery market is growing should provide ample customer interest as partners consistently expand their production footprints.

Investor Takeaway

Despite the positive steps the company has been making recently, investors will need to remain patient as Nano One continues to progress toward commercialization. I don’t expect the Candiac facility to reach commercial scale (10,000 tpa) until the end of 2026 at the earliest. While this could be enough to get the ball rolling in the public markets, the company still has much to prove in terms of partner scalability.

As such, shares likely won’t fully respond until the company achieves significant scale by way of licensing and JVs. For that reason, I expect much of the company’s value to remain unrealized through the remainder of the decade.

This doesn’t mean there won’t be rewards for shareholders that hold on the path to commercialization. I expect shareholders to be rewarded with a CAGR of >30% up until commercialization, at which point growth would become somewhat parabolic.

Assuming the company is able to execute on its commercial vision, a multi billion dollar valuation by 2030 doesn’t seem out of reach for the company. Essentially, I believe that Nano One is a massive winner, so long as it is able to achieve successful commercialization.

This makes its real “fair value” less relevant, especially as this isn’t really something that’s possible to calculate at the company’s current stage. Instead, I think it’s important to focus on the perceived chances of success and timeline to significant scale.

Following its successful 2,000 tpa reactor tests , Nano One has significantly improved its odds of commercial success. Given the level of confidence this creates for Nano One’s commercial success, and its strong partner network, the company’s current value provides an asymmetric opportunity given the ample upside a successful implementation provides.

For further details see:

Nano One: North America's Answer To China