NAVI - Navient Corporation - Need To See Growth

2023-08-03 10:57:20 ET

Summary

- Navient Corporation's revenue has declined by 18% YoY, raising concerns about the impact of the new CEO's leadership.

- Investing in educational loan offerings like Navient is risky due to the uncertain market environment and loan forgiveness discussions.

- Navient generates substantial cash flows from educational financing and aims to focus on lending for potential growth in the future.

Introduction

Navient Corporation ( NAVI ) has had a shift in leadership as the new CEO David Yowan took over. I think we are still having to wait a bit until we see the impacts of his reign over the company, and I don’t think it could come any later as the last report showed a worrisome revenue shift YoY of -18%. The company has a broad set of markets that they serve and is projecting this will help them generate strong cash flows still.

Right now it seems rather risky to be investing in companies like NAVI engaging in educational loan offerings, especially as the hot topic right now seems to be about loan forgiveness. This is creating quite an uncertain market environment, and this seems to have pushed the share price downwards for NAVI. Trading at a p/e of just 5 and a yield of over 3% might look appealing to some, but I think we need to see a strong trend appearing for loan growth. Right now I am not quite seeing that, but given what seems like quite limited downside risk seeing as the valuation is so low I am rating NAVI a hold.

Company Structure

Founded back in 1973 NAVI has focused on providing educational financing and handling education loans and repayments for it. This is where the company has been generating a substantial amount of FCF which has been used to pay out a decent dividend for investors.

NAVI provides technology-based educational financing but also business processing solutions aimed at education, health care, and also government clients. Operations are in the United States.

The company has divided its operations into three various segments, those being: Federal Education Loans, Consumer Lending, and Business Processing. Within the first segment, the focus is on are of curse on education loans as NAVI owns FFELP that are insured or guaranteed by state or not-for-profit agencies. NAVI is generating a large amount of cash flows from these and in 2024 they estimate it will be generating $682 million in total. The payout ratio is still quite low for NAVI at just 19% which has been incredibly sustainable over the last several years. The company hasn't raised the dividend since 2015 and I don’t necessarily see any reason for them to do so in the short term. I say this because there is a lot of turmoil in the educational loan “market” as pushes for loan forgiveness are stronger than ever.

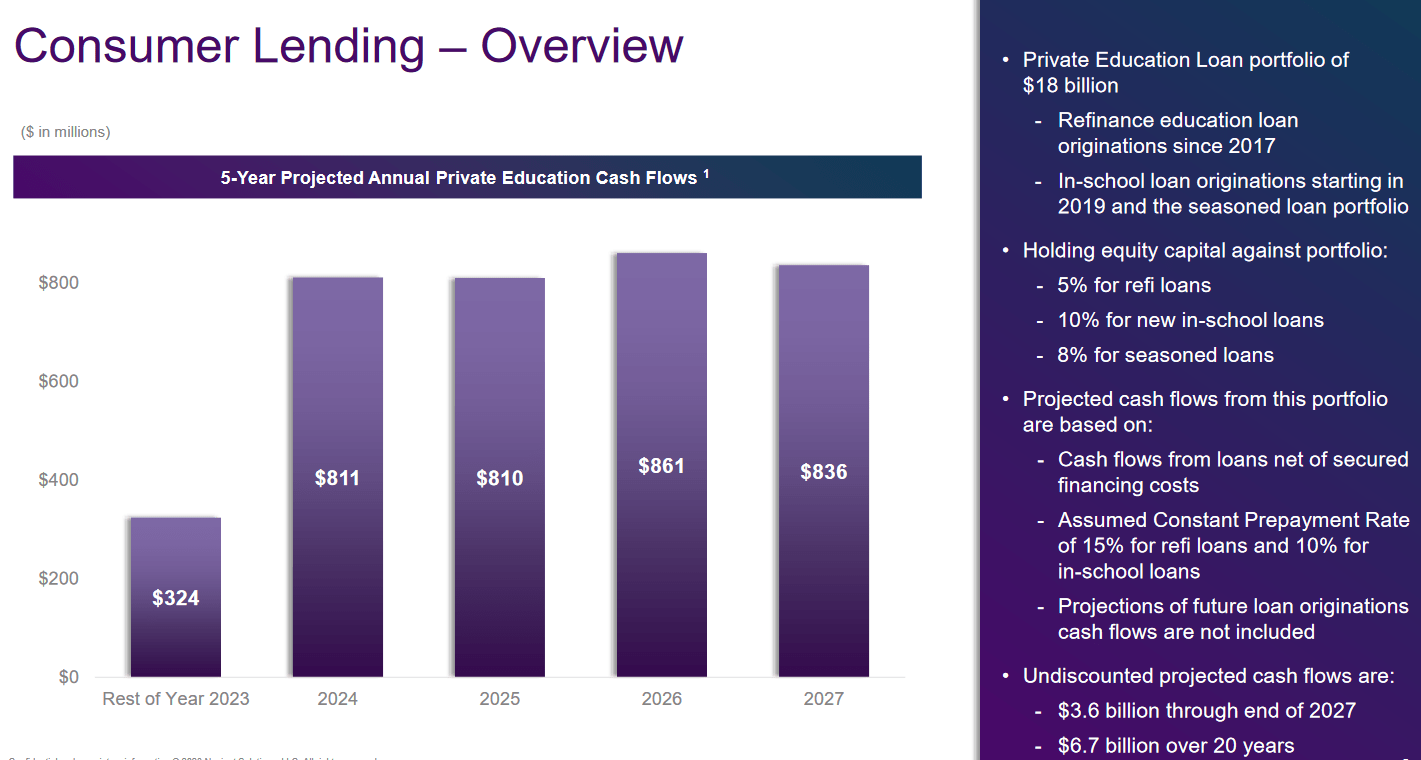

Consumer Lending (Investor Presentation)

{kind=link}

Where NAVI needs to place focus going forward I think is in consumer lending. A market they could tap in more heavily to grow sustainable cash flows. The projected cash flows that NAVI would be generating here comes from a constant repayment rate of 15% for refi loans and 10% for in-school loans. Seeing growth in this department for NAVI I think is where we might realize most of the potential growth of the business.

Earnings Transcript

From the last earnings call on July 26, there are some comments from the new CEO Dave Yowan that I think are with highlighting. The progress of the company in the coming quarters will be largely impacted by the initiatives that the CEO and other leading management members put in, but seeing a clear divergence to more consumer lending I think would make NAVI more appealing. Nonetheless, here is a comment from the CEO that I found quite interesting.

-

"Our strategy is underpinned by the four imperatives, you see on Slide 3, maximize the cash flows from our loan portfolio; enhance the value of our growth businesses; maintain a strong balance sheet and distribute excess capital, and continuously simplify the business and increase efficiency. While executing these imperatives, we continue to help customers meet their financial needs, continuously strengthen our control environment, and be good citizens in the communities in which we operate".

Maintaining strong FCF from their portfolios is a critical priority to keep the dividend yield and make room for potential raises to it in the future. In terms of assessing NAVI, I think looking at the cash flows is a crucial point. Besides that, looking at how the operating costs decrease is also a critical point. YoY NAVI has been able to achieve a 4.3% decrease YoY.

Operational Performance

Net income margin for NAVI sits quite high at 29% and the ROE is beating out the sector too at 13.2%. What is perhaps a little concerning regarding the ROE is the fact that it sits far below the 5-year average of 19% that NAVI has otherwise had.

Over the years the equity of the company has decreased and now sits at a TTM value of $2.9 billion. A steady decline like this is quite worrying and I think gives cause to the lower valuation. The topic of student debt has been on many people's minds and I think it might be posing some challenges for NAVI. In terms of going forward, I think investors will want to keep an eye out for NAVI being able to raise the equity levels to where it was before the pandemic at $3.4 - $3.5 billion. But as we have discussed above here is the fact that NAVI is leaning more toward consumer lending which seems right now to be an easier market to maneuver in and eventually grow ROE from.

Valuation

The valuation of the company is quite low but this seems to be justified given some of the uncertainties of the market. I think however a hold rating can benefit from some upside potential here on out. The p/e is just under 6, and even with the risk I think a 7x earnings multiple is fair given the sheer size and market position that NAVI has.

The p/b of the company is also quite low at 0.77 which is also below the 5-year average of 0.84. This leads me to believe that you aren't necessarily overpaying for NAVI right now, but the risks around it do justify the lower valuation and until that clears up then I fear it will trade at a discount to the sector.

Risk Associated

NAVl, being considered an income generator, would typically be a favorable option during uncertain times. However, it faces significant headwinds that undermine its business model. Investors seeking income may be better off exploring companies with a more robust revenue outlook, less vulnerability to economic fluctuations, and potential protection against inflation and higher interest rates. Additionally, the looming possibility of student loan debt forgiveness poses an overhanging risk for the company.

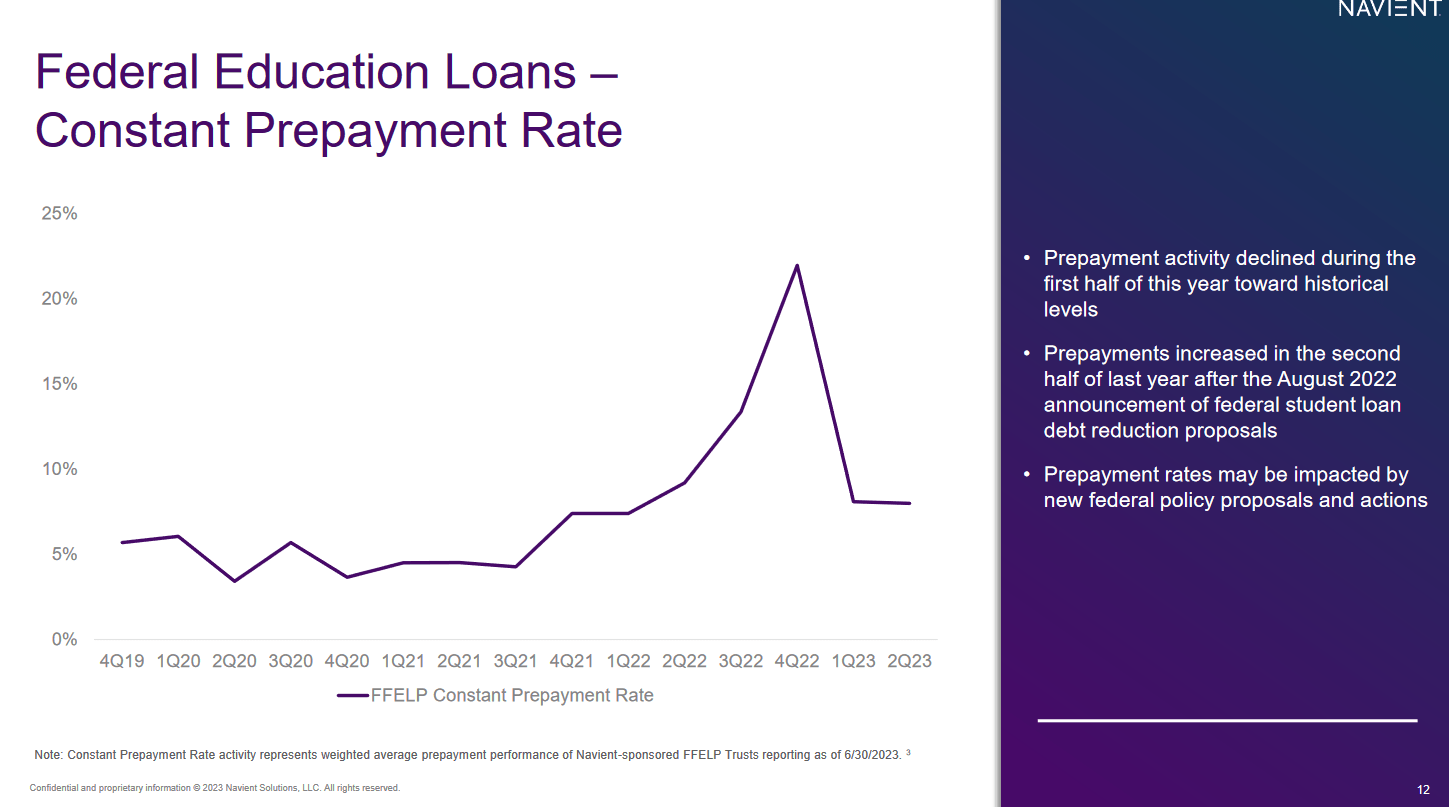

Prepayment Rate (Investor Presentation)

{kind=link}

I think the current economic landscape is marked by several challenges, which makes NAVl's business model less attractive for income-seeking investors. As the economy grapples with the uncertainties of a potential recession and inflationary pressures, companies with more stable revenue streams may offer a safer haven for investors seeking consistent income.

Investor Takeaway

Investors that seek a stable dividend-paying company might consider NAVI right now. The company has maintained the dividend for a very long time, but the buy case for the company I think quite quickly deteriorates as we look at the future ahead for the company. There are challenges amounting to the education loan market and that could negatively impact the top and bottom line for NAVI.

I think the headwinds and the fact that NAVI is making a significant portion of its revenues from this market are placing some risk on the side of investors. There is a chance for a further share price drop if we get more student loan pauses I think. As a result of these concerns, I am rating the company hold right now.

For further details see:

Navient Corporation - Need To See Growth