NAVI - Navient Q3: A Contrarian Buy Despite Litigation And Rate Fears

2023-10-31 05:13:27 ET

Summary

- Navient's Q3 earnings missed expectations, but a deeper look shows financial stability and a healthy balance sheet.

- The regulatory cloud hanging over Navient is dissipating, with settlements reached to resolve litigation.

- Navient's discounted valuation and reasonable growth prospects make it a compelling investment.

Editor's note: Seeking Alpha is proud to welcome Thomas Potter as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

The Investment Thesis: Navient Is Undervalued Given Its Strengths

Navient Corporation ( NAVI ) reported third quarter 2023 earnings that missed analyst expectations, sending shares down. However, in my opinion, a deeper look shows Navient remains financially steady with an under the hood healthy balance sheet. Recent regulatory cloud hanging over Navient is dissipating. Settlements were reached to resolve litigation by several states regarding loan servicing practices. The remaining Consumer Protection Financial Bureau ((CFPB)) lawsuit is a risk, but Navient believes allegations are false and will vigorously defend its position. Any potential settlement or judgment appears manageable given Navient's financial strength. From my view, the company has solid financials and is shareholder-friendly.

Yet shares trade at just a reasonable 2x current sales and 2.5x forward sales. This discounted valuation seems compelling, especially given Navient's reasonable growth prospects. The forward P/E is just 5.27, on the lower end of P/E ratios over the last 8-10 years. Given that student loans in the US cannot be forgiven in bankruptcy, unless in special circumstances , these loans have a high probability of being serviced, meaning profits could be more stable than the market expects going forward.

Overall, I believe shares trade at an attractive valuation amidst likely overdone pessimism about rising interest rates, making Navient a compelling contrarian buy.

Business Breakdown (As Of The Most Recent 10Q):

Navient operates its business in three primary segments: Federal Education Loans, Consumer Lending, and Business Processing. The Federal Education Loans segment owns and services a $39.6 billion portfolio of federally guaranteed Federal Family Education Loan Program (FFELP) loans, representing 70% of total assets as of September 30, 2023 (10-Q pgs. 13, 20). Navient also services $46 billion in total federal loans for other institutions, generating revenue through net interest income on its FFELP portfolio and servicing fees (10-Q pg. 13). The Consumer Lending segment owns a $17.3 billion portfolio of Private Education Loans, comprising 30% of assets (10-Q pg. 20). These loans include "in-school" loans made while a student is in school and "refinance" loans taken post-graduation. As of September 30, 2023, $8.9 billion were refinance and $8.4 billion were non-refinance loans (10-Q pg. 17). Consumer Lending generates revenue primarily through net interest income on its Private Education Loans. Finally, the Business Processing segment provides revenue cycle management, contact center, and loan servicing solutions to healthcare, education, and government clients. Major service offerings include healthcare revenue cycle management and contact centers for federal, state, and local agencies (10-Q pgs. 5).

Navient relies heavily on net interest income from its student loan portfolios supplemented by fee income from servicing and business processing clients as it focuses on growing its private loan origination and business processing units. While this could be seen as a risk, I believe interest rates could remain higher for longer, supporting this business model.

Q3 Recap & US Supreme Court Lawsuit Status

On October 25th, Navient reported Q3 2023 EPS of $0.47, below expectations of $0.81. However, excluding one-time items, EPS was $0.84, exceeding estimates (Q3 earnings transcript). Revenue rose in the company's business processing segment, demonstrating organic growth potential.

The adjusted tangible equity ratio stands at a healthy 8.7%, allowing generous capital returns. Over $94 million was returned to shareholders through buybacks and dividends last quarter (Q3 earnings transcript). While concerns over the lawsuit with the CFPB could result in $250 million in liabilities/write offs for Navient, management has been proactive (Wack - American Banker):“We’ve taken a $45 million accrual, or $0.28 per share, in connection with the CFPB litigation. We accrued for legal matters as required based on developments over the quarter. We remain confident about the strength of our case. At the same time, we’re open to finding a solution that’s acceptable to all parties to put this matter behind us.” -Q3 Earnings Call

In addition, a recent lawsuit now at the US Supreme Court may result in the CFPB being unconstitutional altogether. I think this could have asymmetric upside if the government body suing Navient dissipates.

Financial Steadiness And Healthy Balance Sheet

Navient possesses financial stability and a solid balance sheet to weather rising rates. The company maintains an 84% term funding ratio for its education loan portfolio, limiting exposure to market interest rate swings (Q3 earnings transcript).

Meanwhile, net interest income increased by 13.4% year-over-year in the quarter for both the FFELP and private education loan segments due to slower expected prepayment speeds. With higher rates, borrowers have less incentive to refinance loans. This dynamic extends durations, benefiting Navient's income.

Credit metrics remain healthy, too. Total delinquencies and forbearances for FFELP and private loans improved or were stable year-over-year. Provisioning rose in Q3, but Navient believes reserves adequately cover expected losses. Charge-offs tracked in line with historical norms (Q3 earnings transcript).

With a solid balance sheet, increased net interest income, and credit outlook, Navient appears well-prepared to withstand rising interest rates or macroeconomic challenges. I consider these aspects highly important as it provides an encouraging backdrop for long-term investors.

Forward Outlook Points To Earnings Growth

Management issued an updated timeline of 2023 guidance that was confident in calling for core EPS of $2.92-3.02 (Q3 earnings transcript). While reduced from previous estimates, from my perspective, it still suggests reasonable earnings power.

Beyond 2023, Navient has levers to drive higher profits over time. The company is evaluating alternatives to deliver greater shareholder value after undergoing an extensive business review (Q3 earnings transcript). Efforts are underway to reduce expenses and capital intensity in certain operations.

As the regulatory overhang of past litigation wanes, Navient may consider deploying its strong capital base toward accretive acquisitions. Management could also opt to sell non-core assets and return more capital to shareholders. Given the low valuation, I believe returning capital to shareholders here may unlock some value.

Finally, Navient's growth businesses like healthcare revenue cycle management and tolling/parking authority services offer upside. In my opinion, these capital-light, recurring revenue streams deserve higher valuations.

Risks Appear Manageable

Of course, risks to this thesis still exist. Some FFELP loans still carry exposure to LIBOR rates, although the recent adoption of legislation to transition contracts to SOFR indexes reduces this risk (10Q). Additionally, college enrollment and the demand for education financing remains uncertain. However, even with a shrinking addressable market (the number of college students in the US is declining ), in my judgment, Navient maintains a solid competitive position.

The largest risk is potential cash outlays from remaining litigation and regulatory actions. However, Navient has accrued legal reserves and maintains adequate capital and liquidity to manage any potential settlements. And, like we mentioned before, some of these lawsuits could go away. In my opinion risks appear contained (and baked into the stock). The risk/reward favors long-term investors at current valuations.

Valuation

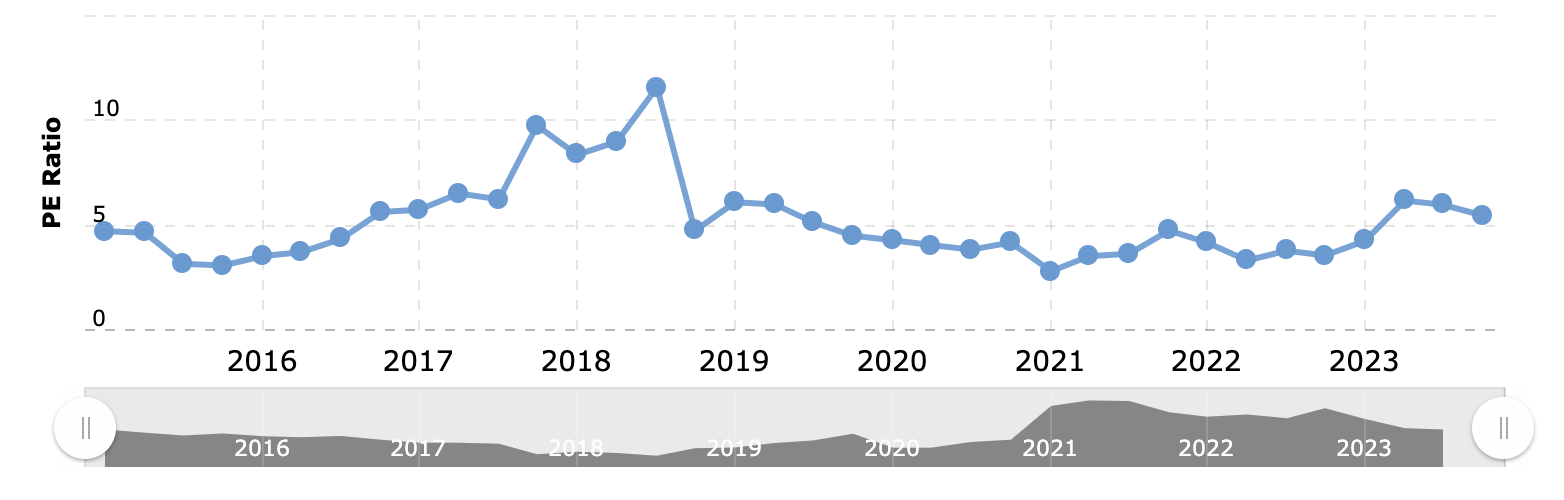

Navient trades near the bottom quartile of P/E ratios the firm has witnessed in the last 10 years. The current forward P/E ratio is 5.27, down from a high of 11.60 in 2018 (Macrotrends).

{kind=link}

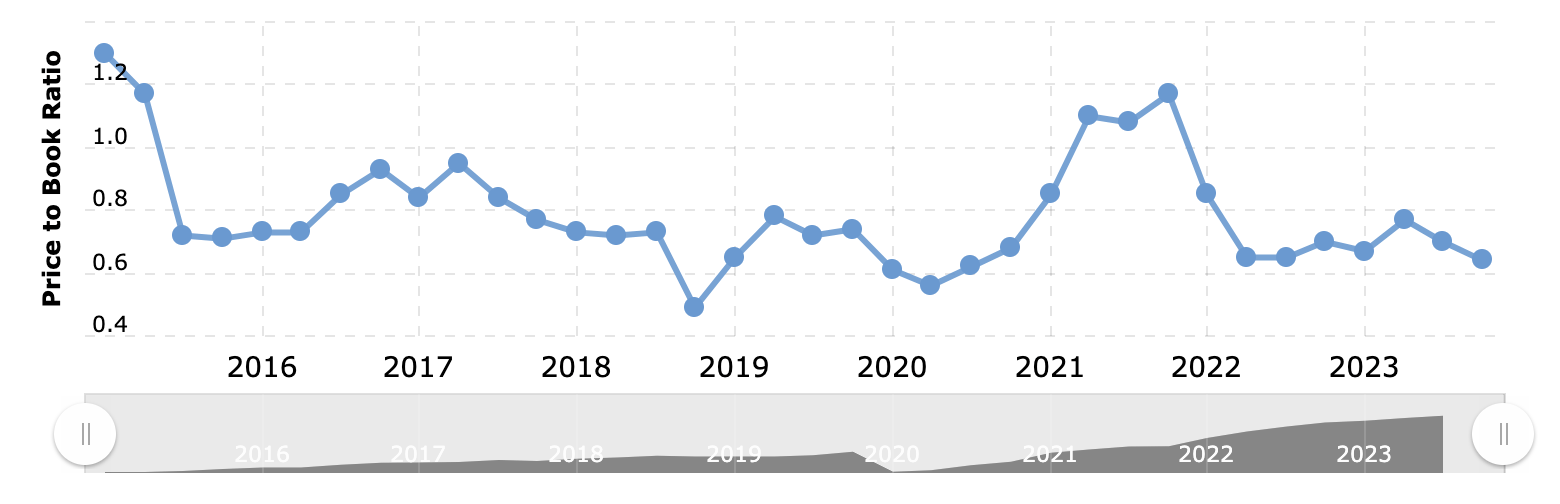

Navient also currently trades at a forward Price to book ratio of 0.62 . This is also on the low end of Price to Book ratios over the last 10 years. Current expectations are for charge offs to cause losses and a decrease in book value. If these charge offs are lower than expected, lawsuits fall apart, or the CFPB gets dismantled, there could be a quick snapback to a price to book ratio of closer to 1.

{kind=link}

Comparative Valuation

In addition, Navient trades at a discount both to the sector Median and peer Nelnet Inc . (NNI)’s PE and Price to Book ratio. Nelnet was recently caught up in a separate lawsuit .

| Company/Median |

| NAVI |

| NNI |

| Sector Median |

| GAAP P/E (fwd) *Fwd P/E is not available for NNI so trailing is used. No analysts covering it |

| 9.1 |

| Price/Book (fwd)*Fwd P/B not available for NNI so trailing is used |

| 0.62 |

| 0.95 |

| 0.95 |

What I Think Fair Value Is

I think the market is currently discounting Navient shares due to their exposure to a lawsuit from the CFPB. While this is a legitimate concern, as I mentioned before the firm is taking steps to put in place charge offs, and there is even a chance the Supreme Court nullifies the agency. Given this I think the shares should trade closer to what peers should trade at.

If we look at Price to Book, the forward sector median stands at 0.95. I believe shares in Navient should trade closer to this price to book ratio but not at it unless the CFPB lawsuit is officially removed. Given this, I think a price to book ratio of 0.79 (average between NAVI forward book and sector median forward book). The 0.16 price to book ratio difference amounts to a $352mm discount and more than fully accounts for the size of the CFPB lawsuit if Navient lost the lawsuit (penalties are anticipated to be about $250mm). This is based on the book value of $2.2 billion at the end of the third quarter 2023.

If Navient reached this price to book ratio of 0.79, this would represent an approximate 27% upside from today's prices, establishing a fair value around $20.33/share. These shares could be worth even more if the lawsuit is nullified, but even in this base case, I see 27% upside as a possibility.

The Bottom Line: Navient Is A Buy For Contrarian Investors

Navient's stock price disregards underlying financial strength. Lingering fears about interest rate exposure seem likely stretched. With a potentially improving regulatory outlook and multiple avenues for enhancing stock price, I believe Navient appears significantly undervalued.

For contrarian investors with longer time horizons, Navient offers substantial upside potential. I expect the stock to re-rate higher as the company delivers on growth initiatives and continues returning capital. There could be a more asymmetric appreciation as well if current lawsuits get dismissed or ruled favorability. Navient remains a compelling buy rating in my book.

For further details see:

Navient Q3: A Contrarian Buy Despite Litigation And Rate Fears