NAVI - Navient: Staying Neutral Until Positive Loan Growth Acceleration

2023-05-09 17:05:25 ET

Summary

- Navient Corporation reported Q1 2023 adj. core EPS of $1.06, which beat consensus estimates of $0.82, but I have concerns about the sustainability of the earnings.

- Faster prepayments could lead to lower NIM, which could impact earnings growth and guidance.

- Navient Corporation is currently trading at a lower multiple (both P/E and P/B) than the average over the last ten years, which provides some margin of safety for current shareholders.

Thesis

Navient Corporation ( NAVI ) provides education loan portfolio management, servicing, and asset recovery. The Company acts as a servicer for Department of Education and Federal Family Education Loan Program ((FFELP)) loans as well as private student loans.

Navient Corporation reported Q1 2023 adj. core EPS of $1.06, which was a major surprise to consensus estimate of $0.82, and management reiterated their FY23 guidance. While the results were good, I am holding a neutral view on Navient Corporation stock as I have concerns about the sustainability of the earnings. The business is likely to perform well in the near term as it benefits term from reserve releases, which effectively pull forward earnings into FY23 from next year.

In my opinion, this might give off the illusion of things growing better than expected, and with expectations further raised for FY24 (which might be hard to meet, as some earnings are already pulled forward). The bull case, I believe, would be to see an acceleration in loan growth that will increase future earnings potential, and also other growth segments (such as Business Processing). As such, I am recommending a hold rating for Navient Corporation until I see evidence of whichever playing out, before considering a position.

Q1 2023 Results Review

The net effect of new accounting standards and the resolution of private legacy loans in bankruptcy drove NAVI's adj core EPS to $1.06, significantly higher than the consensus estimate of $0.82. Moving up the P&L, net interest income was reported at $233 million and operating expenses came in at $192 million. Overall, net income was reported at $111 million.

One thing to note for the quarter and coming quarters is that, to properly account for the restructuring of troubled debt, NAVI implemented a new accounting standard in 1Q23, which affected the financial results. NAVI had $77 million in associated reserves on the balance sheet, of which it released $52 million during the quarter in light of the new accounting standard's treatment of foregone interest. Half of the $25 million in reserves will be released in FY23, with the other half to follow in FY24, as per management.

Faster prepayments could lead to lower NIM

According to management, there has been a significant decline in prepayment activity since last November, and the situation has not changed for the better. This is in particular within the FFELP loan book, where rate of prepayment are now well below historical levels. The implicit result is the lifetime of such loans are now dragged further, which drives up amortization of premiums. I believe this is a result of the consolidation last year as FFELP borrowers consolidate into direct government loans to take advantage of the student loan forgiveness proposal .

While the lifetime of such loans is being dragged further, there was a net benefit from the interest rate mismatch within FFELP (1Q22 earnings call), which improved FFELP NIM to 112bps. For FY23, management is guided for FFELP NIM to be in the range of 100bps to 110bps, with the assumption that prepayment rates remain at current levels. In the event that prepayment rate increases (if rates fall, which provides incentives for borrowers to repay), this is likely to hurt NIM (1Q23 earnings call) and also impact guidance.

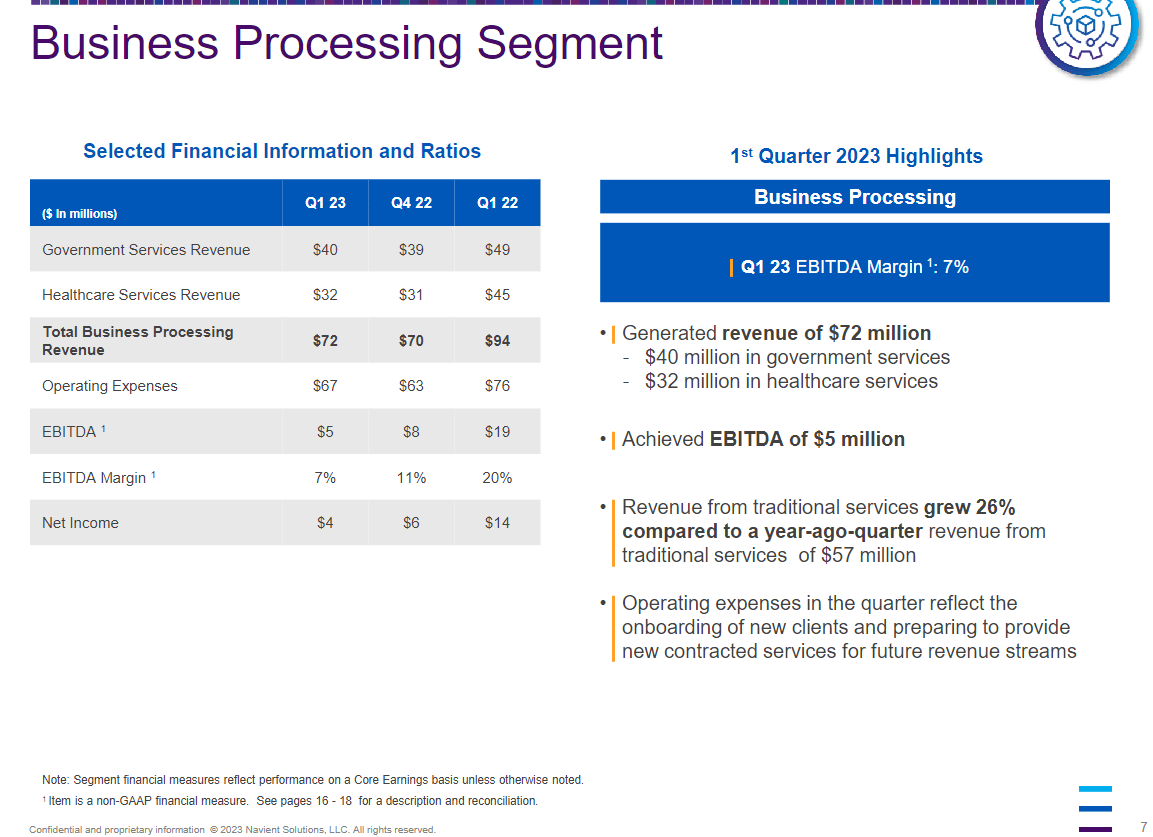

Business processing continues to be strong

While still a small part of the business profits, the Business Processing segment has been growing fast, with Q1 2023 growing at 26% as NAVI secures additional contracts. Management has guided the segment to grow more than 10% with a high-teens EBITDA margin. I have an optimistic view on this segment that earnings can accelerate, and that the 1Q23 depressed margin was merely a function of cost pulled forward (NAVI hired additional hundreds of employees). As such, any incremental growth will now carry a high incremental margin as it scales off the current start-up cost. While this segment is still in the phase of proving itself, if executed properly, it could reduce the cyclicality of the overall business.

{kind=link}

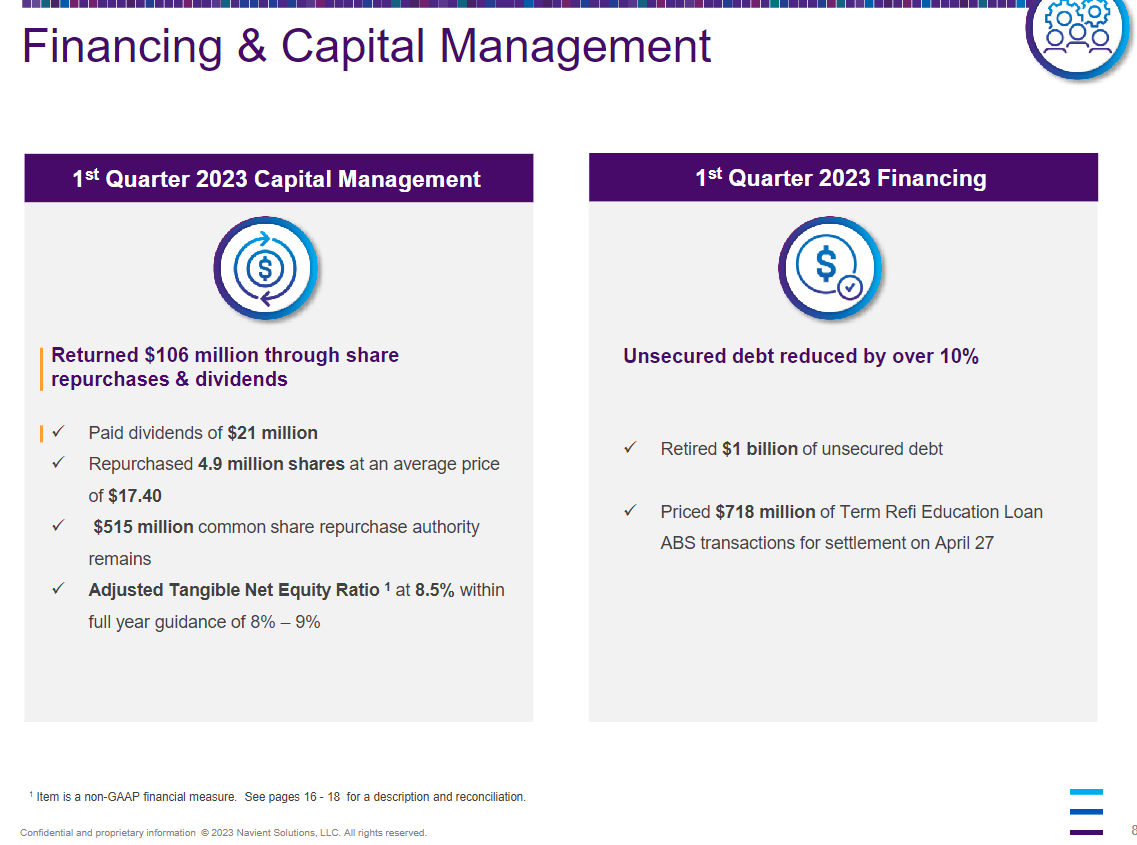

Capital allocation

Navient Corporation has a good capital allocation strategy, in my opinion, that is focused on increasing balance sheet strength and at the same time return capital to shareholders. In Q1 2023, the business retired $1 billion of notes, reducing its outstanding unsecured balances by 14%. They are also on track to repurchase $310 million of shares in FY23 (4Q22 earnings call), which has about ~$225 million (12% yield) left for this year.

{kind=link}

Valuation

For investors who already have a position, I believe the current valuation provides some protection if things go wrong. NAVI is currently trading at 5x earnings and 0.6x book value. Both of these metrics are 25% and 40% lower than the average multiple over the last ten years. As a result, the market is already anticipating a slowdown in earnings (consensus estimates for FY24 EPS at $3.02 vs LTM of $3.7). In this sense, unless NAVI really messes up and reports lower than an already low expectation, I don't think the stock will suffer too much.

Conclusion

Navient Corporation Q1 2023 results were strong, with adj. core EPS coming in at $1.06, beating consensus estimates. However, I have concerns about the sustainability of the earnings, as some earnings were pulled forward from future years due to reserve releases. Additionally, the increase in prepayment activity could lead to lower NIM, which may impact guidance.

On the positive side, the Business Processing segment continues to be strong and could reduce the cyclicality of the overall business. Overall, I recommend a hold rating for Navient Corporation until there is evidence of loan growth acceleration and other growth segments (such as the growth momentum in Business Processing) before considering a position.

For further details see:

Navient: Staying Neutral Until Positive Loan Growth Acceleration