S - Navigating Cybersecurity: CrowdStrike Vs. Palo Alto Networks Vs. SentinelOne

2024-01-15 01:35:19 ET

Summary

- The article compares three cybersecurity stocks: CrowdStrike, Palo Alto Networks, and SentinelOne.

- I recommend buying shares of Palo Alto Networks and SentinelOne due to their attractive prospects and market positions.

- CrowdStrike is not recommended as aggressively even though its growing intrinsic value at a rapid rate.

Investment Thesis

In this in-depth analysis, I compare and contrast three cybersecurity stocks, CrowdStrike ( CRWD ), Palo Alto Networks ( PANW ), and SentinelOne ( S ).

The two stocks out of these three that I recommend buying more feverishly are Palo Alto Networks and SentinelOne. Why didn't I recommend CrowdStrike as aggressively? Simply because I run a very concentrated portfolio. And having two cybersecurity stocks is more than enough exposure to this sector.

That being said, as you'll soon read, I'm very openly bullish on this sector as a whole. Ultimately, it boils down to investors' preference.

Palo Alto is more of a stalwart, while CrowdStrike is delivering an all-around stellar performance, and SentinelOne is still unproven to a large if its underlying profitability can be reached in the near term.

On the other hand, SentinelOne's stock is very attractively priced if it reaches my assumptions. Also, relative to its market cap, I believe that SentinelOne's debt-free balance sheet is the most attractive relative to its peers.

We have much to go through, so let's get to it.

Rapid Recap,

Back in August, I concluded my bullish coverage of CrowdStrike by saying,

CrowdStrike is an attractive investment even if there's some lingering uncertainty about whether it can truly shine against these towering expectations.

I believed at the time that CRWD was an attractive investment, but that it needed to prove itself too. And prove itself it has, by becoming a highly profitable enterprise. In fact, I had a suspicion that CRWD could become a highly profitable enterprise and that's why I upgraded my call from neutral to bullish earlier in 2023. Here's the performance since I turned bullish on this name.

Author's work on CRWD

Why CrowdStrike? Why Now?

CrowdStrike's main product is the Falcon platform, which uses advanced technologies like artificial intelligence to detect and stop cyber threats in real time.

CrowdStrike helps organizations secure their computer systems, networks, and data by providing a comprehensive suite of cybersecurity solutions. This includes safeguarding against various attacks such as malware, ransomware, and other malicious activities that could compromise the security of digital information. Essentially, CrowdStrike's goal is to prevent breaches from cyber threats.

In the near term, CrowdStrike demonstrates robust prospects fueled by its impressive fiscal Q3 2024 performance. The company has surpassed the $3 billion ARR milestone, marking a 35% y/y growth, the only pure-play cybersecurity software vendor to achieve this milestone.

With an accelerating net new ARR of $223 million and a focus on innovation, including the introduction of the Falcon Platform Raptor release and strategic acquisitions like Bionic, CrowdStrike is well-positioned for continued growth. The market validation through industry awards and accolades, coupled with the successful expansion of cloud security, identity threat protection, and next-gen SIEM offerings, underscores CrowdStrike's dominance in the cybersecurity space. The company's commitment to a single-built-by-design platform, instills confidence in its ability to reach its outlined goal of $10 billion in ARR over the next 5 to 7 years.

{kind=link}

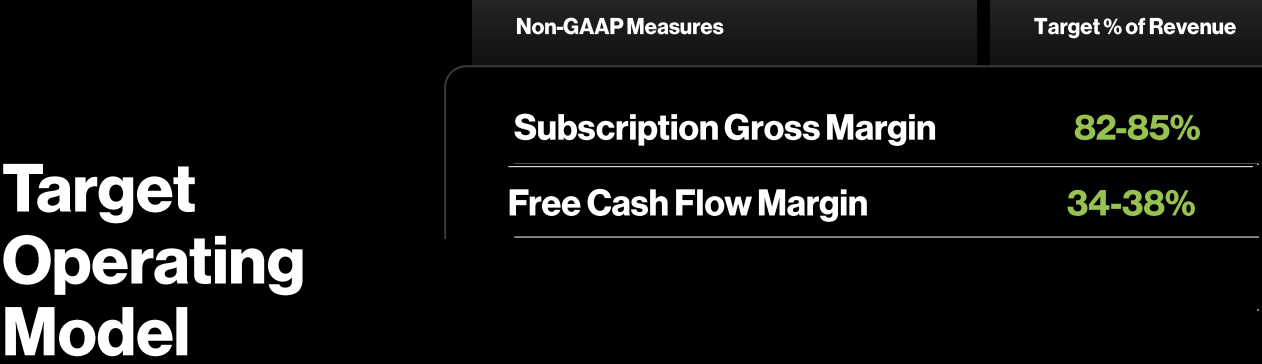

The one key challenge facing CrowdStrike is how it will balance its aggressive investments in innovation driving topline growth while at the same time maximizing free cash flow. More specifically, CrowdStrike aims to reach about 36% free cash flow margins over the next 3 to 5 years. It practically goes without saying that to grow at +30% CAGR, with mid-30% free cash flow margins is the holy grail of tech companies, that very few companies achieve.

Given this background, let's discuss it's financials and its key drivers.

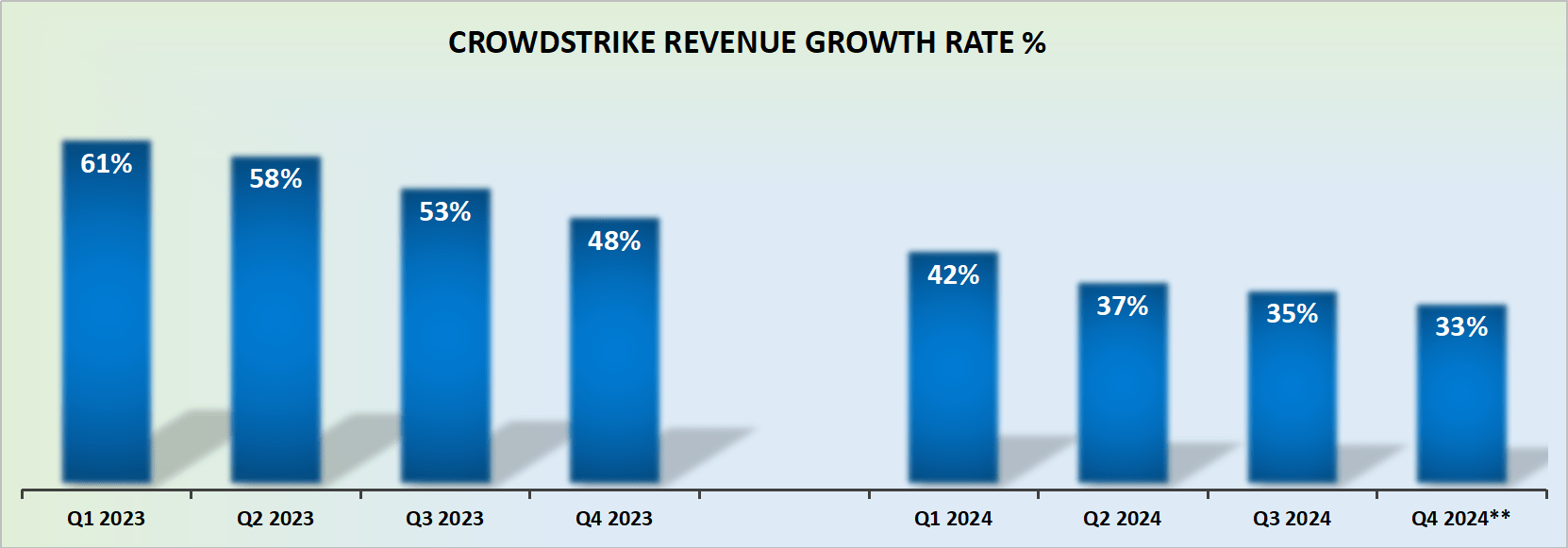

Revenue Growth Rates Above 30% CAGR

{kind=link}

CRWD's fiscal year finishes in January 2024, meaning that when I refer to fiscal 2025, it's essentially this calendar year, but skewed by 1 month.

CrowdStrike is expected to finish fiscal Q4 2024 with somewhere around 33% y/y growth rates, or perhaps slightly higher. Nevertheless, the takeaway here is that there's a very high likelihood that in fiscal 2025 CrowdStrike will be able to deliver yet another +30% CAGR year.

As a point of reference, consider what the Street expects:

SA Premium

The Street practically expects to see around 30% CAGR too. Naturally, these figures start off low, with the expectation that in the coming quarters these estimates and raised slightly as the company continues to make progress. After all, the sell side typically leaves some room to then upwards revise their estimates closer to the quarter.

Altogether, CrowdStrike is expected to see close to $4 billion of revenues next year, which is not small change, particularly for a company that's growing by 30% CAGR.

Given this context, let's now delve into CRWD's valuation

CRWD Stock Valuation -- 57x non-GAAP Operating Income

The graphic above is a reminder that CRWD has seen its multiple double in the past 12 months. Incidentally, keep in mind what I previously said about CRWD's fiscal year finishing later this month. This means that on a forward-looking multiple, CRWD is priced slightly cheaper than this figure and closer to 17x forward sales, rather than 24x forward sales shown above, meaning that it's not quite as exaggerated as it appears at first glance.

Furthermore, what I like about CRWD is that it's able to grow at around 30% CAGR, even as it's working hard to improve its underlying profitability. Case in point, for this upcoming year (fiscal 2025) CRWD is already on a run-rate of $1.2 billion of non-GAAP operating income

Moreover, I believe that this time next year, as investors look out to the following year, it's more than likely that CRWD will be able to deliver more than $1.5 billion of non-GAAP operating income. Needless to say if CRWD matches my estimates, which I believe it should, it will become a formidable free cash flow machine.

In the next section we'll discuss SentinelOne.

Rapid Recap

Asides from paying members, very few readers would know that I recommended going long SentinelOne subsequent to its latest quarterly results.

Indeed, I had previously been bearish on this name. Although I did make change of stance clear in the comments section at the bottom of my previous article.

So, allow me to explain why I went from bearish this stock, to uber bullish on SentinelOne.

Why SentinelOne? Why Now?

Demonstrating its prowess in the cybersecurity arena, SentinelOne shines with a robust performance in fiscal Q3 2024 (more details on its financials to come lower).

SentinelOne's CEO Tomer Weingarten outlined the company's impressive financial achievements, boasting a remarkable 42% year-over-year revenue growth and a substantial 43% increase in Annual Recurring Revenue.

Weingarten highlighted the success of the Singularity platform in modernizing endpoint security, positioning SentinelOne as a go-to choice for enterprises seeking innovative solutions. The triple-digit growth in Cloud Security and Data Lake solutions adds another dimension to its triumph. Weingarten's assertion that the company's innovation and technology leadership fuel growth reflects its commitment to staying ahead in the dynamic cybersecurity landscape. With a customer base exceeding 11,500 and a notable 15% year-over-year growth in ARR per customer, SentinelOne demonstrates strength in large enterprises and platform adoption.

However, despite its evident strengths, SentinelOne faces challenges inherent in the cybersecurity domain. Weingarten's comments to a large extent echo many of CrowdStrike's, as you'd expect.

He pointed out the persistent and evolving threat landscape, emphasizing the escalating velocity and complexity of attacks. Real-time protection becomes crucial in addressing shorter dwell times and increasingly sophisticated cyber threats. Traditional, disjointed security solutions are acknowledged as insufficient by Weingarten, with challenges extending beyond technical aspects to include geopolitical tensions impacting the cybersecurity space.

Against this backdrop, a closer look at the company's financials becomes pertinent.

Revenue Growth Rates Into Next Year at 40% CAGR

S revenue growth rates

Looking back to SentinelOne's fiscal Q2 2024 results, at the time, SentinelOne, had guided for 35% y/y growth for fiscal Q3 2024. However, SentinelOne pleasantly surprised with a substantial 42% y/y increase in its revenue line.

Moreover, as SentinelOne now guides for a 34% y/y increase in revenue growth in fiscal Q4 2024, I am anticipating SentinelOne to potentially surpass its own guidance by 5% to 7%.

In an optimistic scenario, the company might achieve a remarkable 41% y/y revenue growth into fiscal Q4 2024.

Even if growth rates fall slightly short of the 41% mark, a close-to-40% CAGR seems plausible. This sets the stage for insights into fiscal 2025, commencing in February 2024.

While industry analysts anticipate approximately 32% y/y revenue growth rates, I find this estimate rather conservative.

SA Premium

My expectation is that SentinelOne is likely to achieve revenue growth rates closer to a 40% CAGR. The rationale behind this optimistic projection stems from the company facing a challenging comparable period in the previous fiscal year, with triple-digit revenue growth rates. Considering this lower hurdle and the current momentum, a near 40% CAGR appears achievable, potentially surpassing analysts' present estimations by around 8%.

To summarise how SentinelOne's financials compares with CrowdStrike, I believe that SentinelOne is about 3-4 years behind CrowdStrike in terms of scale. That being said, the corollary of this statement is that SentinelOne is growing at the pace that CrowdStrike was growing at 3-4 years ago.

My Bull Case For SentinelOne: Profitability in Sight

S Fiscal Q3 2024

The main blemish in the bull case here has always been that the business is dramatically unprofitable. That's what had kept me away from this stock in the past. It very easy to grow rapidly if you are growing while running at a loss.

Certainly, the strides made by the company in streamlining its cost structure are truly commendable, leaving no room for doubt. Impressive, when compared to the same period a year ago, both on the EBIT line and the non-GAAP operating line, the company exhibited a remarkable improvement of 3,200 basis points year-over-year, showcasing significant progress.

Additionally, it's noteworthy that the outlook for fiscal Q4 2024 indicates a negative 14% non-GAAP operating margin, as detailed below.

SentinelOne fiscal Q3 2024

Given the management team's track record of maintaining a conservative approach in their guidance, I am inclined to believe that they will surpass the projected margin profile.

SentinelOne fiscal Q3 2024

To provide context, let's review the situation. In the preceding quarter, fiscal Q2 2024, SentinelOne initially anticipated negative 22% operating margins. However, when the quarter's results were disclosed, the actual margin profile revealed a more favorable negative 11%.

Similarly, their earlier projection for the fiscal year's end foresaw negative 25%, which has now been revised to an expected negative 20%. Considering these adjustments collectively, there is a possibility that fiscal Q4 2024 might conclude with approximately negative 10% operating margins, or even potentially as low as negative 8%. Consequently, there's a chance that SentinelOne could approach breakeven as it enters the next fiscal year.

It's essential to acknowledge the counterargument, wherein it's suggested that SentinelOne is presently implementing more straightforward cost-cutting measures, targeting the "low-hanging fruit."

This implies that the company is focusing on easily achievable reductions or optimizations. While this doesn't diminish the earlier assumptions, it's evident that sustaining this rapid pace of improvement may pose challenges. The nature of the cost-cutting measures becomes a critical factor. As SentinelOne strives to enhance its operating margins further, it will likely encounter diminishing returns, transitioning from easily attainable adjustments to more intricate, complex changes. This shift could be met with resistance or present challenges that are harder to address without affecting core business functions or customer satisfaction. Additionally, the acknowledgment of potential trade-offs with top-line growth implies that prolonged cost-cutting may eventually impact the company's ability to invest in innovation.

Stock Valuation -- 8x Forward Sales

According to my estimates, if I assume that my 40% CAGR for next year is vaguely correct, this means that next year, SentinelOne will make about $860 million in revenues. Might even make slightly more than this. But not a lot more.

This leaves this stock priced at about 8x forward sales. Note, this figure is different from the graphic above, because as explained previously, its fiscal year is about to start next month, therefore readers should adjusts for this element.

Depending on how familiar with high growth stocks you are, this may sound cheap or expensive.

In my experience, any company that's growing at about 40% CAGR in high tech is getting a 12x to 14x multiple. Of course, this depends on how close the business is to becoming profitable.

My point is, that if by next December I see that the business is becoming profitable, or at least there's profitability within its grasp, this stock could get closer to 11x forward sales, or perhaps slightly more. Again, I believe that its current forward price to sales ratio is about 8x.

Therefore, I am hoping to see SentinelOne trading closer to a $11 billion market cap in the next 18 months.

Next, we'll discuss Palo Alto Networks.

Rapid Recap,

Back in November, I made a strong buy recommendation where I said,

I maintain that paying 43x forward EPS is a fair price for a high-quality company, with strong long-term tailwinds, that's growing its EPS by approximately 25% CAGR.

PANW is a stock that I've been recommending to readers since 30 August 2022.

With the benefit of hindsight, this was the clear winner since I've been actively recommending the stock.

Also, while it's not immediately obvious from the chart above, my recommendation had the least volatility of the peer group. While I know from experience that it's easy to talk in hindsight, the fact is that volatility is the killer for investors. It's easy to look back and talk. It's another thing to continue buying and holding over a two-year period when the world moved from inflation concerns to worries about the fed and layered with the regular theme of geopolitical tensions.

Why Palo Alto? Why Now?

Palo Alto Networks is one of my preferred cybersecurity companies (the other stock I recommend is SentinelOne).

Not because I believe it has the best product. Rather, because I believe that investors' expectations remain muted relative to its full potential, even though the stock has clearly been a strong performer since I've actively recommending it.

Investors in 2024 are likely to be aware of the surging demand for cybersecurity solutions. Even if readers weren't previously aware of this aspect, the readers that made it this far into my analysis (thank you), will by now be aware of this dynamic.

Within this environment, Palo Alto Networks is well-positioned to benefit from a resilient tech spending sector, where budgets remain intact, ensuring a sustained and robust demand for their cybersecurity solutions.

In the broader context of the cybersecurity sector, Palo Alto consistently emphasizes the ongoing trend of market consolidation. This observation aligns with discussions from other cybersecurity companies' earnings calls, indicating a widespread acknowledgment of this phenomenon pervades the industry. The increasing demand for cybersecurity solutions is part of a broader evolution in categories such as firewalls, endpoint protection, and systems-on-chip management, characterized by both volume and complexity.

Author's calculations on PANW

Over time, my investment thesis regarding Palo Alto has garnered increasing traction. It revolves around a straightforward concept, as I believe the most effective investment ideas are those that are easy to comprehend. While various distractions may vie for investors' attention, simplicity has proven to be effective in my experience.

Based on my calculations, which may have a slight margin of error but are nonetheless suitable for our analysis, approximately 39% of Palo Alto's revenue stems from its Next Generation Security portfolio.

PANW Q1 2024

As evident from the red arrow above, this segment of the business is experiencing rapid growth.

However, it's clear that there's a degree of customer cannibalization at play. This suggests that Palo Alto's "hardware customers" are likely transitioning to Palo Alto's next-generation security, resulting in a scenario where Palo Alto is essentially reallocating customers from one pocket to another. Despite this, the crucial aspect is the full adoption of Palo Alto's platform by these customers, who are, for the most part, unlikely to churn out.

Revenue Growth Rates Of A More Mature Business

PANW revenue growth rates

Palo Networks as a whole is not growing anywhere near as fast as CrowdStrike or SentinelOne. As noted already, Palo Alto's hardware business is holding back the company. That being said, on the flip side, its legacy hardware business is highly free cash flow generative.

For transparency, I'll persist in recommending Palo Alto as long as it consistently achieves a CAGR above 15%. This threshold is chosen based on my observation that tech businesses falling below 15% tend to lose significant market share to competitors, making it challenging for them to regain growth in intrinsic value.

While businesses can potentially accelerate once more, such occurrences are rare. Microsoft ( MSFT ) serves as a classic business study in this context, but instances of businesses successfully reaccelerating are infrequent (rarer than Silicon Valley unicorns), despite anyone's silver-tongued proclamations to the contrary.

PANW Stock Valuation -- 46x Forward EPS

PANW Q1 2024

Note, that Palo Alto's fiscal 2024 ends in July. Here, I've assumed that Palo Alto will end fiscal 2024 at around $5.60 of EPS and that next year PANW will grow its EPS by around 20% y/y. This implies that looking out to fiscal 2025, PANW is likely to see about $6.72 of EPS.

Consequently, PANW is priced at 42x forward fiscal 2025 EPS. Therefore, to think about halfway through fiscal 2025, meaning towards the end of 2024 to make it more comparable to CrowdStrike and SentinelOne, I estimate that PANW is priced at around 46x forward EPS.

Now, you'll obviously be aware that I've referred to CrowdStrike and SentinelOne on a P/Sales multiple, while I've referred to Palo Alto on a P/earnings multiple.

The reason for this is that Palo Alto is growing much slower, and I need to start thinking more about its underlying profitability than SentinelOne is more focused on getting to scale, rather than on maximizing profitability.

The Bottom Line

In wrapping up this comprehensive analysis of cybersecurity stocks, my investment lens converges on the financial intricacies and valuation metrics, casting Palo Alto Networks and SentinelOne as the more compelling choices compared to CrowdStrike in my strategic portfolio.

Palo Alto Networks, standing as a stalwart in the industry, touts a mature business model, particularly evident in its measured growth and resilient legacy hardware segment.

While its pace may not match the fervor of CrowdStrike, the consistent free cash flow generation and a forward EPS multiple of 46x in fiscal 2025 render it a steadfast player in the market.

Conversely, SentinelOne, though currently operating on a smaller scale compared to its peers, propels itself into the spotlight with an alluring growth trajectory, boasting a potential 40% CAGR. The current valuation, marked by an 8x forward sales multiple, positions SentinelOne as an intriguing high-tech contender, emphasizing its pivotal role in the evolving cybersecurity landscape.

As I meticulously evaluate these nuances, my prognostication leans towards SentinelOne attaining a market cap of $11 billion in the next 18 months, underscoring the significance of imminent profitability in shaping the trajectory of this cybersecurity stock.

For further details see:

Navigating Cybersecurity: CrowdStrike Vs. Palo Alto Networks Vs. SentinelOne