WFC - NCZ: Bursting Convertibles Bubble Still Weighs On This Fund

2023-12-18 14:58:06 ET

Summary

- The Virtus Convertible & Income Fund II aims to provide income-focused investors with the potential for capital appreciation through a combination of convertible securities and junk bonds.

- The fund has underperformed the S&P 500 Index over the past three years, but taking distributions into account improves its performance.

- The fund's portfolio consists of convertible securities and junk bonds, with a focus on companies that have resolved past financial issues. However, the fund's distribution has been declining over time.

- Convertibles underperformed bonds in 2022, which explains the fund's terrible recent performance. This fund underperformed the convertible index due to leverage.

- The fund failed to cover its distribution during the first half of this year, despite the euphoria and optimism surrounding AI technology.

The Virtus Convertible & Income Fund II ( NCZ ) is a closed-end fund, or CEF, that allows income-focused investors to pursue their goals without being forced to sacrifice the upside potential of a common equity investment. As we have discussed in numerous recent articles, in today’s market environment, fixed-income funds typically have much higher yields than can be obtained via any sort of equity investment. This is partly because bonds have a better risk-reward profile than common stocks right now given the challenges facing the American economy and the uncertainty surrounding monetary policy.

Unfortunately, fixed-income products have limited potential appreciation compared to common equities so purchasing such products today does involve some opportunity risk as an investor will miss out if the market enters another wild bull period, such as what we saw over the ten-year period that ended in 2021. The Virtus Convertible & Income Fund II invests in some rather unique assets in an attempt to provide investors with the best of both worlds and avoid the problem of needing to sacrifice potential returns in order to get income.

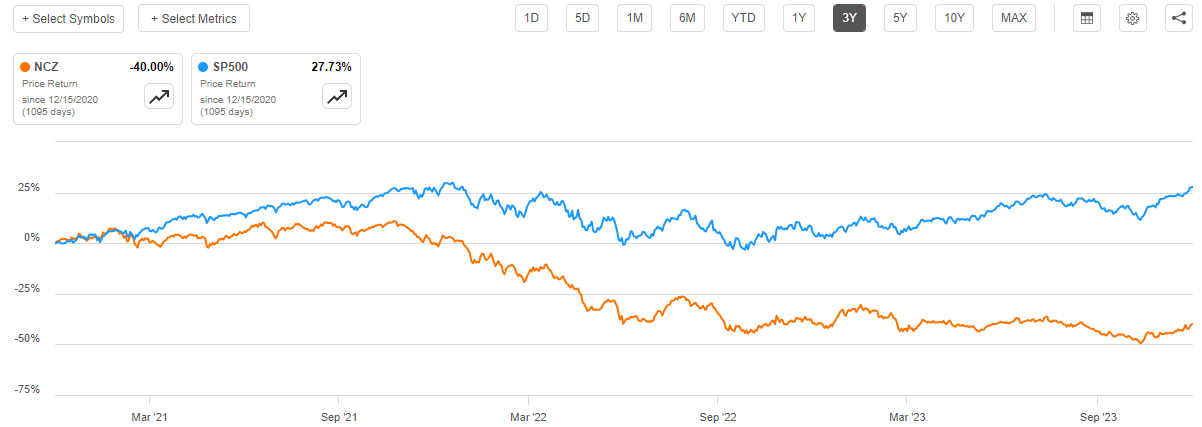

Unfortunately, the fund has not delivered a particularly attractive return in recent years. Over the past three years, the Virtus Convertible & Income Fund II is down 40% compared to a 27.73% gain in the S&P 500 Index ( SP500 ):

{kind=link}

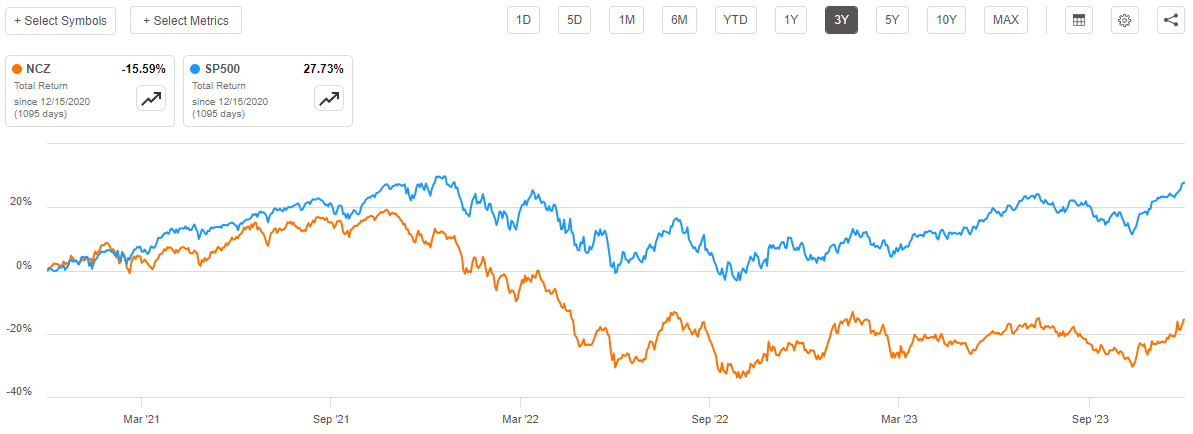

As I have pointed out in the past though, closed-end funds tend to deliver the majority of their total investment return in the form of direct payments to their shareholders. This is because the basic business model of these entities is to pay out all of the returns produced by their portfolios, rather than relying on the fund’s share price to appreciate over time. As such, any discussion of the fund’s performance should take the distributions that it paid out to the shareholders over the given period into account. After all, these distributions can sometimes offset share price declines.

In this case, taking the distributions into account does improve the fund’s performance portfolio dramatically, although it still underperformed the broader market. Over the past three years, the Virtus Convertible & Income Fund II handed its investors a 15.59% loss:

{kind=link}

This is partly due to the nature of the assets that this fund invests in, as convertible bonds generally imploded in value once the post-pandemic bubble burst. As such, this poor performance cannot solely be laid at the feet of the fund’s management team. It is understandable that investors would be hesitant to invest in this fund given the recent performance history, though.

Fortunately, at this point, the worst of the damage is already behind us as it seems very unlikely that the Federal Reserve will tighten monetary policy further, and even if it does, the fund has generally been range-bound since late 2022 so it seems unlikely that another interest rate hike will hurt it much. As such, there may be an opportunity for investors to obtain an attractive 12.12% yield along with significant upside potential today.

About The Fund

According to the fund’s website , the Virtus Convertible & Income Fund II has the primary objective of providing its investors with a high level of total return through a combination of current income and capital appreciation. As regular readers can likely recall, I frequently criticize funds that invest in debt securities and have capital appreciation as one of their goals. This is because bonds are incapable of delivering long-term capital appreciation due a few factors:

- Bonds have no connection to the growth and prosperity of the issuing entity,

- Bonds have a finite life due to the fact that they mature,

- Bonds are issued and redeemed at the same price,

- Interest rates cannot go below a certain level.

Thus, in most cases, the only real way to grow a bond portfolio indefinitely is to retain some of the coupon payments to use to buy more bonds. That is not the way most closed-end funds operate.

This fund is somewhat different though, due to the nature of the assets that it purchases. As the website explains,

The Fund seeks total return through a combination of capital appreciation and current income.

Invests in a diversified portfolio of domestic convertible securities and high-yield bonds rated below investment grade.

Under normal circumstances, the Fund will invest at least 80% of its total assets in a diversified portfolio of convertible securities and non-convertible income-producing securities and also seeks to invest at least 50% of its total assets in convertible securities, but determines its allocation based on changes in equity prices, changes in interest rates, and other economic and market factors. For the convertible portion, Voya Investment Management seeks to capture the upside potential of equities with potentially less volatility than a pure stock investment.

The fund therefore invests in a combination of convertible securities and junk bonds, which are both fixed-income vehicles. The junk bonds have the same problem as other bonds in that they cannot produce capital appreciation indefinitely. However, the convertibles are capable of this task due to the fact that these entities can be converted into common equities. These securities therefore do have the potential to deliver potentially infinite capital gains, as common stocks theoretically have no upper limit to their price. Thus, in this case, the fund might really be able to deliver on its objective of delivering long-term capital appreciation even though it did fail to accomplish that task over the past three years.

As the description above states, the fund will typically invest at least 50% of its total assets into convertible securities. The fund currently has a much larger weighting to these securities though, as we can see here:

CEF Connect

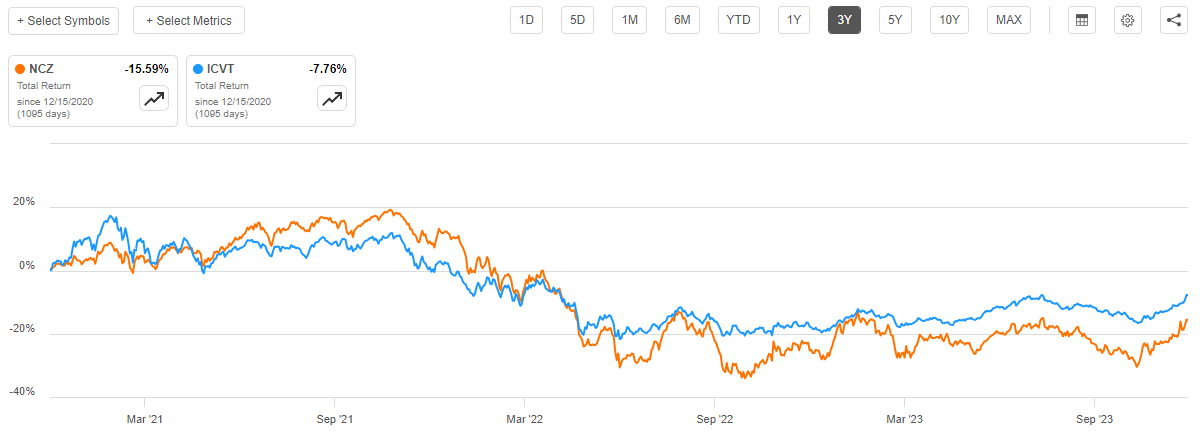

It is this high weighting to convertible securities that has been behind the fund’s incredibly poor performance over the past three years. As we can see here, the fund’s total returns have actually performed very similarly to the Bloomberg U.S. Convertible Cash Pay Bond > $250MM Index ( ICVT ):

{kind=link}

While this fund did underperform the index, that was partially driven by the fund’s use of leverage. We can see this in the asset allocation chart above which shows that the fund has a negative 56.65% weighting to cash. This leverage amplifies losses, so it makes sense that this will cause the fund to underperform the index during a period of poor performance for convertible securities in general.

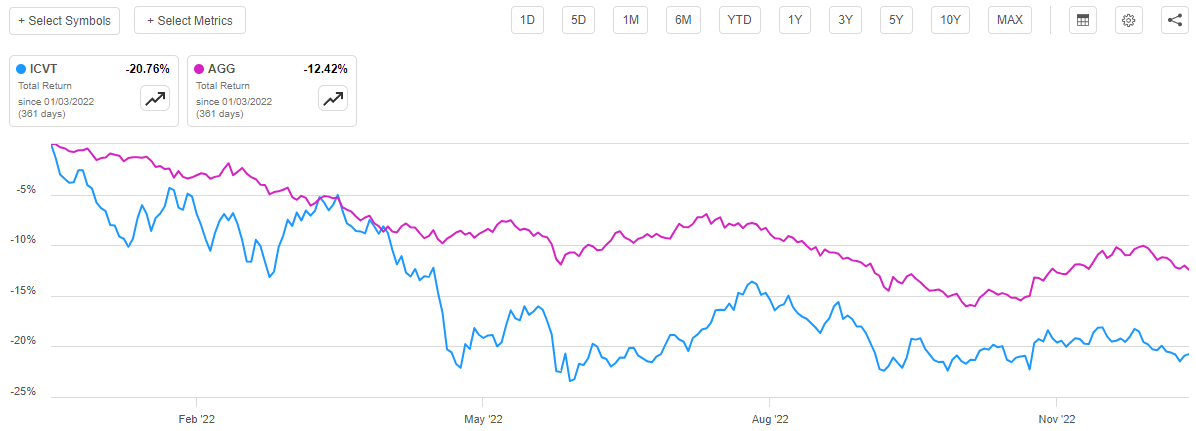

In the introduction to this article, I mentioned that some of this poor performance for convertibles, in general, was caused by a bubble bursting in 2022. We can see evidence of this in the fact that convertible securities substantially underperformed the Bloomberg U.S. Aggregate Bond Index ( AGG ) over the course of that year:

{kind=link}

This is due to the basic characteristics of the companies that usually issue convertible securities. In general, convertible debt is issued by companies that have strained cash flow, high levels of already existing debt, or some other problem that makes it very difficult for them to obtain financing at a reasonable cost. For example, a start-up company with limited revenue might choose to issue these securities. The ability to convert the debt into common stock may induce investors to accept a lower interest rate in the hopes that they can turn a huge capital gains profit when the start-up company becomes successful, or the company fixes whatever problem was causing it to struggle with obtaining affordable financing.

Once interest rates started rising in November 2021 and especially into 2022, investors in general became less willing to finance speculative investments. For example, we do not hear too much about non-fungible tokens, special-purpose acquisition companies, and other things that people were buying as investments during the height of the post-pandemic bubble. As such, the stocks of start-ups and similarly speculative companies fell from their heights and when we combine this with the fall in bond prices that accompanied the Federal Reserve’s policy shift, we can see how convertible securities would deliver a very disappointing return relative to the rest of the market.

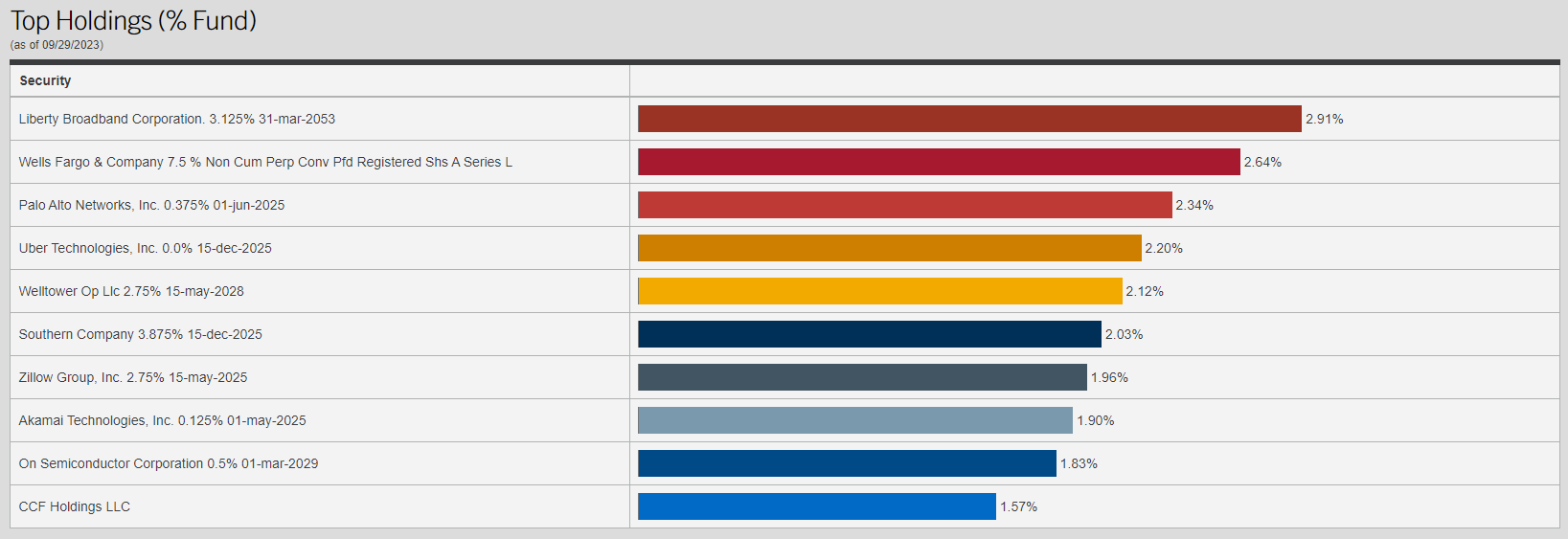

The fact that convertible securities are frequently issued by struggling companies is something that might be concerning for risk-averse investors who are simply seeking a high level of income. After all, companies with strained finances could have issues with making their debt payments during an economic downturn or similar event. Fortunately, the largest positions list of this fund does not show much in the way of greatly troubled companies:

{kind=link}

Many of the convertible securities that are held by this fund were issued during periods when a given company was experiencing financial issues that have since been resolved. For example, the Wells Fargo & Company ( WFC ) convertibles shown above were issued in order to raise cash during the subprime mortgage crisis more than ten years ago. Nobody would argue that Wells Fargo is not able to make good on its payments on those securities today. The same is true of many of the other companies on this list.

In short, the fund does not appear to be too heavily invested in financially struggling start-ups or highly risky companies today, but it does hold securities that were issued when one of those descriptions applied to the issuer. This should provide a certain level of comfort to potential investors in this fund, as income-focused investors may not want to take on an exceptionally high level of risk.

However, as we also saw earlier, the fund invests its assets that are not in convertible securities into junk bonds. These securities are generally considered to carry a fairly high risk of default, which is the reason why the yield is much higher than investment-grade corporate securities. As of the time of writing, the Bloomberg High Yield Very Liquid Index ( JNK ) has a yield of 7.92% compared to 5.26% for the Markit iBoxx USD Liquid Investment Grade Index ( LQD ). The fact that this fund is investing in these securities may therefore be somewhat concerning for risk-averse investors.

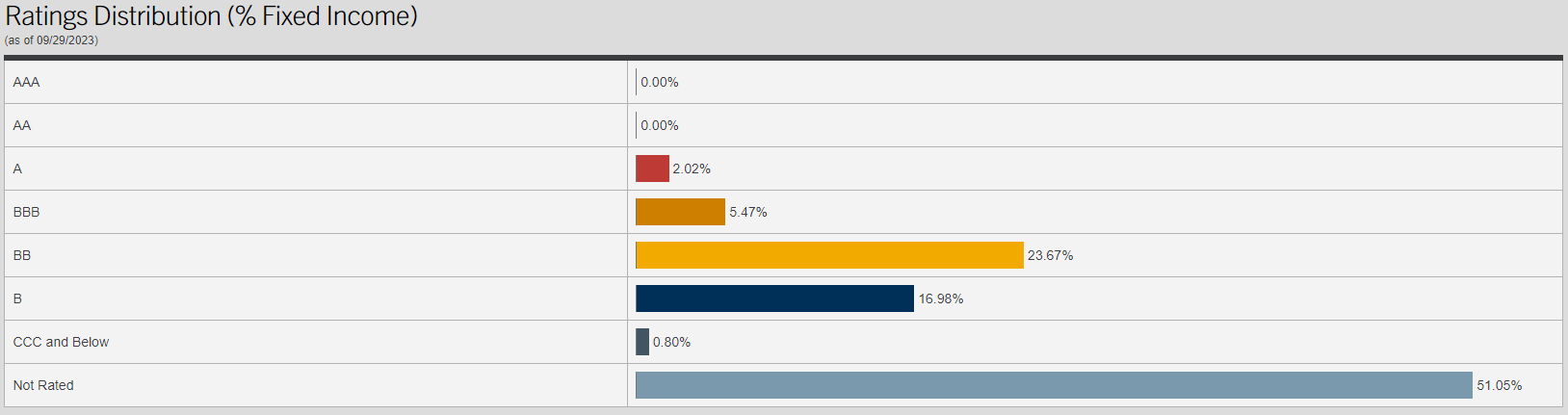

However, we can assuage these concerns somewhat by looking at the credit ratings that have been assigned to the securities in the portfolio. Here is a summary:

{kind=link}

An investment-grade security is anything that is rated BBB or higher. As we can see, that describes 7.49% of the portfolio. However, we can see that a much larger 40.65% of the portfolio is rated BB or B by one of the major rating agencies. These are the two highest possible ratings that can be assigned to speculative-grade bonds. According to the official bond ratings scale , securities that have been assigned one of these two ratings are issued by companies that have the financial capacity to carry their existing debt obligations even through a short-term economic shock or a recession. As such, while these firms do have weaker balance sheets than investment-grade companies, there should not be a reason to excessively worry about the safety of their debt. We probably do not need to worry too much about default-related losses here, especially since the fund’s portfolio contains 221 positions so each position represents a relatively small percentage of the overall portfolio.

We can see that above as well, as there is no individual position that accounts for more than 3% of the portfolio. As such, any company that does default on its obligations should only have such a small impact on the overall portfolio that we will not even notice it.

Leverage

As is the case with most closed-end funds, the Virtus Convertible & Income Fund II employs leverage as a method of boosting the effective yield and total returns of its portfolio well beyond that of any of the underlying assets. I explained how this works in a variety of previous articles on other closed-end funds. To paraphrase myself:

Basically, the fund borrows money and then uses that borrowed money to purchase convertible securities, junk bonds, and similar income-producing assets. As long as the total return that the fund receives from the purchased assets is higher than the interest rate that it needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will normally be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for that reason.

As of the time of writing, the Virtus Convertible & Income Fund II has leveraged assets comprising 37.64% of the portfolio. That is, unfortunately, a bit more than we really like to see. However, as I have pointed out in various articles, funds that invest in fixed-income and debt securities can generally carry a higher level of leverage than a common equity fund. This is due to the fact that these securities are less volatile than common equity and ultimately it is asset volatility that gets a fund in trouble with leverage.

Overall, investors probably do not have to worry too much about the fund’s leverage as it is not substantially above that one-third level and the aforementioned ability of fixed-income funds to carry higher levels of leverage than common equity closed-end funds. We do still want to keep an eye on things though, as we do not want the fund’s leverage to increase much beyond today’s level.

Distribution Analysis

As mentioned in the introduction to this article, the primary objective of the Virtus Convertible & Income Fund II is to provide its investors with a high level of total return that consists of a combination of capital appreciation and current income. In order to achieve this objective, the fund invests in a portfolio that consists primarily of convertible securities and junk bonds. Convertible securities and junk bonds both deliver the bulk of their returns in the form of direct payments to their investors, however, convertibles can also deliver capital gains via the conversion to common stock. The fund collects all of the payments that it receives from these securities, and then borrows money to allow it to collect payments from more securities than it could purchase solely with its equity capital. It combines this money with any profits that it manages to realize from trading bonds and the sale of common stock and then pays it out to its investors, net of the fund’s own expenses. We can expect that this would result in the fund having a very high distribution yield.

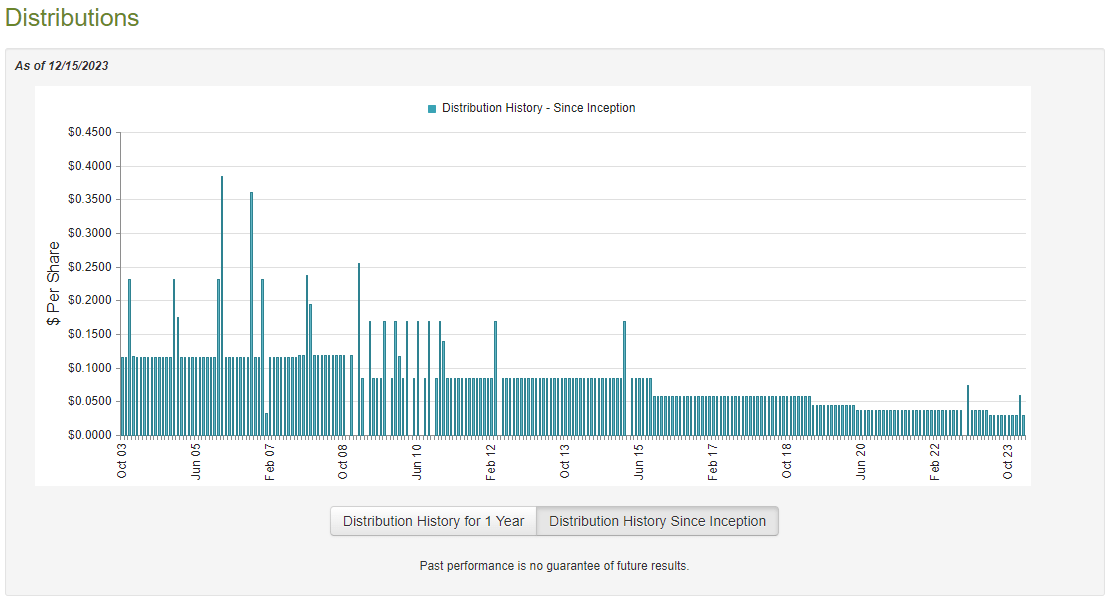

This is indeed the case, as the Virtus Convertible & Income Fund II currently pays a monthly distribution of $0.03 per share ($0.36 per share annually), which gives it a 12.12% yield at the current share price. This is certainly an attractive yield for any income investor, even in today’s high-interest rate environment. Unfortunately, the fund has not been particularly consistent with respect to its distribution over the years. In fact, it has repeatedly cut its payout and has overall delivered investors a steadily declining payout over its history:

{kind=link}

This seems highly likely to be a turn-off for any investor who is seeking to earn a safe and secure income from the assets in their portfolios. The fact that inflation has been steadily reducing the number of goods and services that can be purchased with even a stable distribution amplifies this irritation, as any investor who has been dependent on this fund’s distributions to pay their bills or finance their lifestyles has seen a steady erosion of purchasing power over time. This is a category that would include many retirees.

However, anyone who is purchasing the fund today is not affected by the fund’s past history. After all, today’s buyer will receive the current distribution at the current yield and will not suffer any adverse effects from the fund’s past distribution cuts. The most important thing for a buyer today is ensuring that the fund is able to sustain its current distribution going forward. Let us investigate this and attempt to determine if that is the case.

Fortunately, we do have a somewhat recent document to consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on July 31, 2023. As such, this report will not include any information about the fund’s performance over the past four months. This is somewhat disappointing given the market volatility that has occurred since the end of July in both directions, as that could have had an impact on the fund’s financial condition. However, the first half of this year was characterized by a generally friendly market that caused the price of many assets to increase. This almost certainly benefited this fund considering that the Information Technology sector, which was the biggest beneficiary of the strength in the stock market, accounts for 20.45% of the fund’s total assets. This report should give us a good idea of how well the fund managed to take advantage of that situation.

During the six-month period, the Virtus Convertible & Income Fund II received $8.047 million in interest and $1.059 million in dividends from the investments in its portfolio. This gives the fund a total investment income of $9.106 million during the period. The fund paid its expenses out of this amount, which left it with $5.185 million available for stockholders. That was, unfortunately, nowhere near enough to cover the distributions that the fund actually paid out. Over the six-month period, the fund distributed $14.843 million to its shareholders. At first glance, this is something that could be quite concerning as the fund is clearly failing to cover its distributions.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distributions. For example, it might have been able to make money by selling appreciated bonds as prices rose during the first half of this year. It also could have had some capital gains from common stock that it obtained along the way. Realized capital gains are not considered to be investment income for accounting or tax purposes, but they clearly represent money coming into the fund that can be distributed to the investors.

Fortunately, the fund did have some success in this area. It reported net realized losses of $19.804 million during the period, but this was offset by $25.499 million net unrealized gains. The fact that the fund did manage to get some capital gains is certainly nice, but it was still not enough to fully cover the distribution. Overall, the fund’s net assets declined by $6.956 million after accounting for all inflows and outflows during the period. This is certainly worrying, as the fund overdistributed and was unable to fully cover its distribution.

Valuation

As of December 15, 2023 (the most recent date for which data is currently available), the Virtus Convertible & Income Fund II has a net asset value of $3.39 per share but the shares currently trade for $2.98 per share each. This gives the fund’s shares a 12.09% discount on net asset value at the current price. That is a more expensive valuation than the 13.89% discount that the shares have had on average over the past month. As I have pointed out in numerous previous articles though, a double-digit discount generally represents a reasonable price to pay for any decent fund. As such, the price today is reasonable if you want this fund.

Conclusion

In conclusion, the Virtus Convertible & Income Fund II has almost certainly disappointed many investors over the past few years as convertible securities got punished severely when the post-pandemic bubble burst and monetary conditions began to tighten up. Fortunately, the high distribution did offset some of the share price declines, and investors as a whole did not do too badly.

The Virtus Convertible & Income Fund II failed to cover its distribution in the first half of this year, which is likewise concerning and adds an additional risk. While the current price is nice, I will admit that I cannot come up with a good reason to buy the fund today.

For further details see:

NCZ: Bursting Convertibles Bubble Still Weighs On This Fund