ET - Near 10% Yield Plus Exciting Growth: Plains Vs. Energy Transfer

2023-06-17 05:55:29 ET

Summary

- Plains and Energy Transfer are both investment-grade midstream infrastructure businesses, offering high single-digit yields and potential for strong payout growth.

- Energy Transfer has a more diversified business model and greater exposure to natural gas.

- Plains, however, offers an exciting combination of current yield and distribution growth.

- We compare them side by side and offer our take on which is the better buy at the moment.

Both Plains ( PAA )( PAGP ) and Energy Transfer ( ET ) - both investment grade midstream infrastructure businesses - are among the most attractively priced high yielding securities that also promise attractive payout growth in the coming years. It is rare to find recession-resistant, inflation-resistant, investment grade, stable cash flowing businesses that have well-covered high single digit yields that also offer the potential for strong payout growth in the years to come. Yet, with both PAA/PAGP and ET, that is exactly what you get. In this article, we will compare them side by side and offer our take on which is a better buy at the moment.

Plains Vs. Energy Transfer: Business Model

Both businesses generate pretty stable cash flows thanks to the long-term fixed-fee commodity price resistant nature of the contracts on the vast majority of their assets. That said, ET's business model is both much larger and much more diversified than Plains' is.

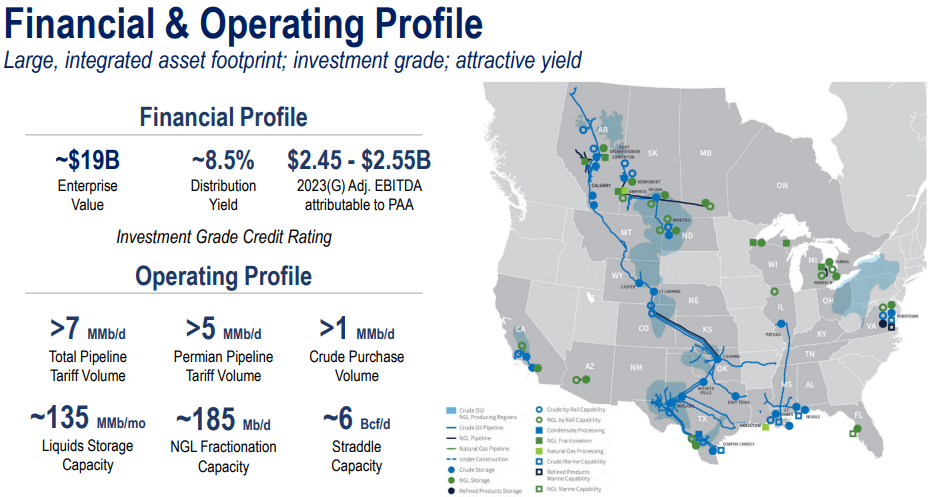

Plains is heavily concentrated in servicing oil production (83% of expected 2023 adjusted EBITDA) primarily from the Permian Basin, with some diversification into NGLs (~17% of expected 2023 adjusted EBITDA) from Canada:

Plains Portfolio (Investor Presentation)

{kind=link}

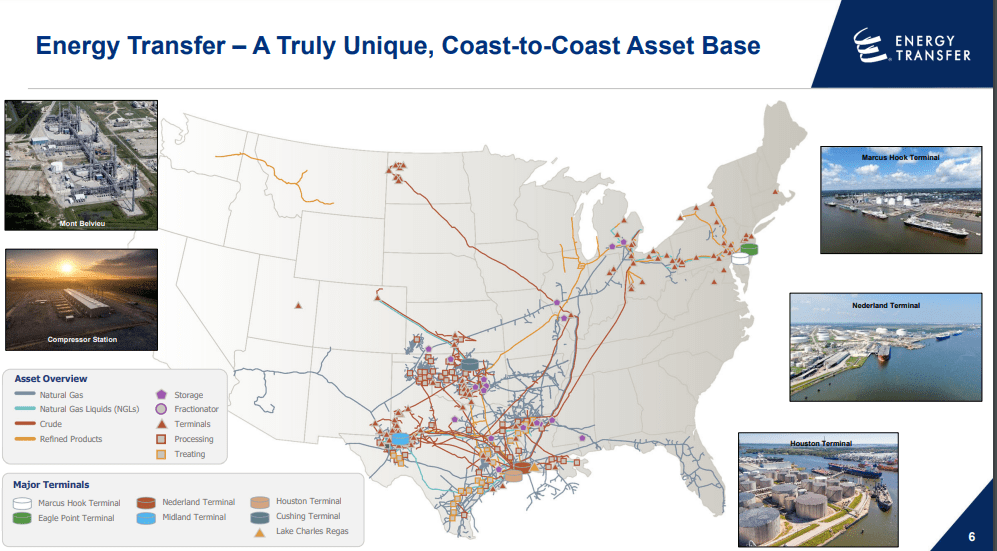

In contrast, ET has a much larger asset portfolio that is over 4.5x larger than Plains' is on an enterprise value basis. Moreover, it generates at least 11% and no more than 28% of its adjusted EBITDA from each of its five business segments (crude oil, NGL & refined products, natural gas interstate transport & storage, midstream, and natural gas intrastate transport & storage).

ET Portfolio (Investor Presentation)

{kind=link}

While Plains' assets are quite high quality - especially after their fairly aggressive non-core asset pruning program in recent years - we favor ET's portfolio overall given its greater size and diversification. We especially like its greater exposure to natural gas.

Plains Vs. Energy Transfer: Balance Sheet

When it comes to balance sheet, both businesses are in a similar spot. Both saw their leverage ratios rise to levels that threatened their investment grade credit ratings in the wake of the COVID-19 outbreak and the collapse in energy prices of 2020. As a result, both management teams slashed their distributions and began aggressive deleveraging programs.

Today, they are both in much stronger financial position, with their leverage ratios well within their long-term leverage targets and continuing to deleverage thanks to their large amounts of retained free cash flow. Moreover, both management teams are optimistic that they can get credit rating upgrades in the not-too-distant future.

Back in February, Plains' CEO stated :

We believe the path that we plan to manage our financial capital structure at is commensurate with mid triple BBB ratings, and it'll just take time and us executing against what we've laid out to get there. So, we're pleased with the progress so far. We did get one positive outlook recently and we're hopeful. Again, we just got to continue to execute and deliver like we think we will.

Meanwhile, ET's CEO stated on their latest earnings call:

Our goal is to get to that BBB flat...We think that BBB is a good place to be and that's what we're going to continue to target.

Neither business faces significant refinance risk, either, thanks to fairly well laddered debt maturities and plenty of liquidity and free cash flow generation. As a result, we consider both balance sheets to be equally strong at the moment with fair low risk and likely to earn credit rating upgrades in the near future.

Plains Vs. Energy Transfer: Distribution Outlook

ET has been growing its distribution at an incredibly brisk pace since late summer of 2021:

Moving forward, growth will likely slow substantially, but management still expects to be able to grow the distribution at a 3-5% annualized rate for the foreseeable future. When combined with the near 10% current yield, this makes for a very attractive current yield plus growth combination.

Meanwhile, Plains' distribution growth has been less impressive than ET's over that same period, though it has still been very strong:

Moving forward, however, Plains' distribution growth outlook appears to be much stronger than ET's, with Wells Fargo research forecasting a 12.4% distribution per share CAGR over the next three years. Management itself has stated that it plans to grow the distribution by $0.15 per unit per year until distributable cash flow coverage of the distribution falls to a still conservative 1.6x level. For 2024, that means that the distribution will likely grow at a 14% annualized rate.

In 2023, Plains is expected to cover its distribution by 2.3x with distributable cash flow, whereas ET is expected to cover its distribution by 1.96x with distributable cash flow. In addition to its superior distribution coverage ratio, the reason why Plains has a much stronger near-term distribution growth profile relative to ET is that ET is wanting to retain more of its cash flow to fund a fairly aggressive growth investment pipeline. In contrast, Plains is operating a smaller and leaner business model with unitholder capital returns and deleveraging as its primary goals.

Plains Vs. Energy Transfer: Valuation

Both businesses look to be among the cheapest in the midstream sector, with low P/DCF and EV/EBITDA multiples and sky-high distribution yields:

| EV/EBITDA |

| P/DCF |

| NTM Yield |

| ET |

| 7.62x |

| 5.3x |

| 9.8% |

| PAA |

| 8.85x |

| 5.4x |

| 8.5% |

While ET looks a bit cheaper than PAA at the moment, it is important to keep in mind that Plains' near-term distribution growth profile is considerably stronger than ET's.

Plains Vs. Energy Transfer: Investor Takeaway

At the end of the day, if we could only own one of these two midstream businesses, our choice would be ET given its superior diversification, greater exposure to natural gas/NGLs, its higher current distribution yield, and lower EV/EBITDA valuation.

However, Plains still has a quality asset portfolio and offers an extremely exciting combination of current yield plus distribution growth. As a result, for investors look to round out their energy exposure with an exciting combination of current yield and growth, Plains is an excellent choice. At High Yield Investor, we are long both of these businesses, along with five other midstream businesses .

For further details see:

Near 10% Yield Plus Exciting Growth: Plains Vs. Energy Transfer