CA - New Found Gold Corp.: A Sell Until There Are Revenues

2024-01-04 17:50:14 ET

Summary

- NFGC is a mineral exploration company with no revenues and negative cash flows.

- The company has been raising capital through share dilution and is dependent on additional financing to continue operations.

- NFGC has potential for future revenue generation through the development and production of its gold deposits, but this process has not yet started.

As I comb through gold miners, I came across the mineral exploration company New Found Gold Corp. (NFGC). Of the four analyses written on it in 2023 here on Seeking Alpha, two were Buys, and two were Holds. I, however, think the company is a SELL.

The reasons for that are simple, so I'll also spend this article giving ideas on when shares of NFGC might become a Buy.

History Since IPO

Exploration

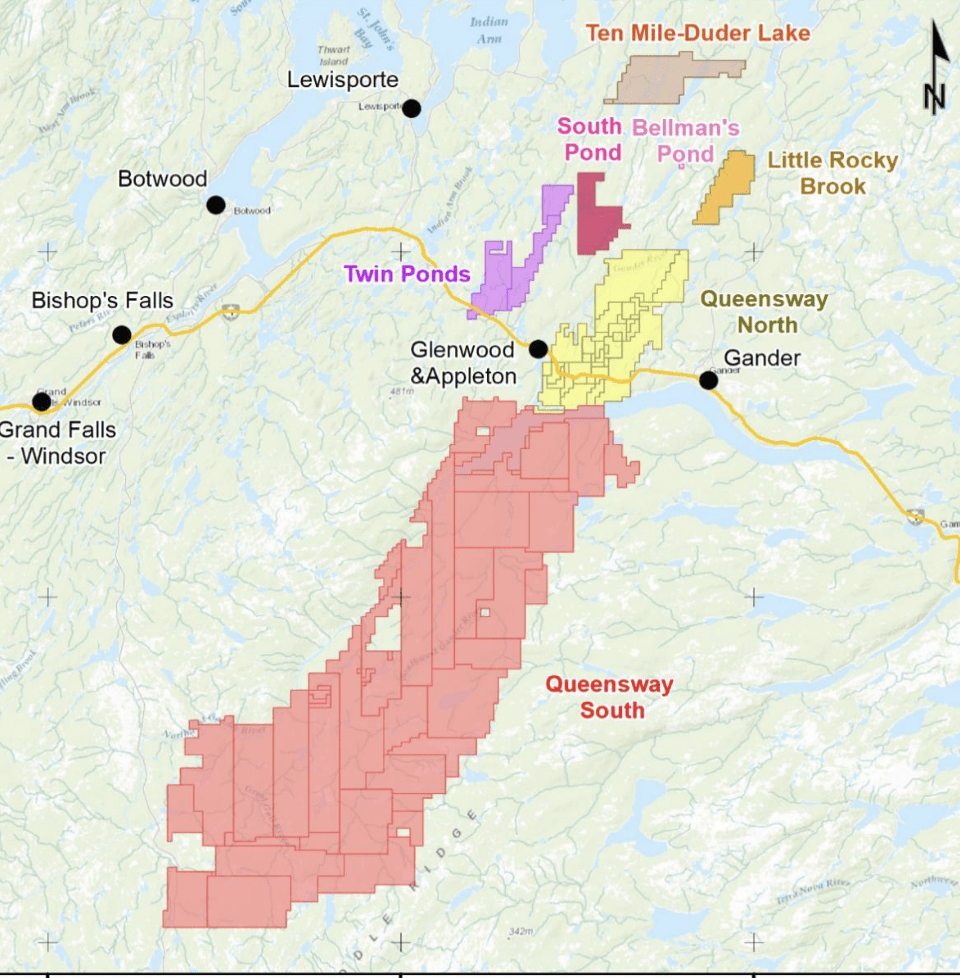

The company only recently had its IPO in 2020 on the Toronto Stock Exchange. It later became available on NYSE in 2021. Its only significant asset is the mineral licenses for the Queensway site, located in northern Newfoundland, Canada. It is a large area, covering 1,662 sq. km.

Over the last three years, the northern portion of the property has undergone numerous drilling and exploration projects of the area. The Q3 2023 MD&A release shows how the site is broken down.

{kind=link}

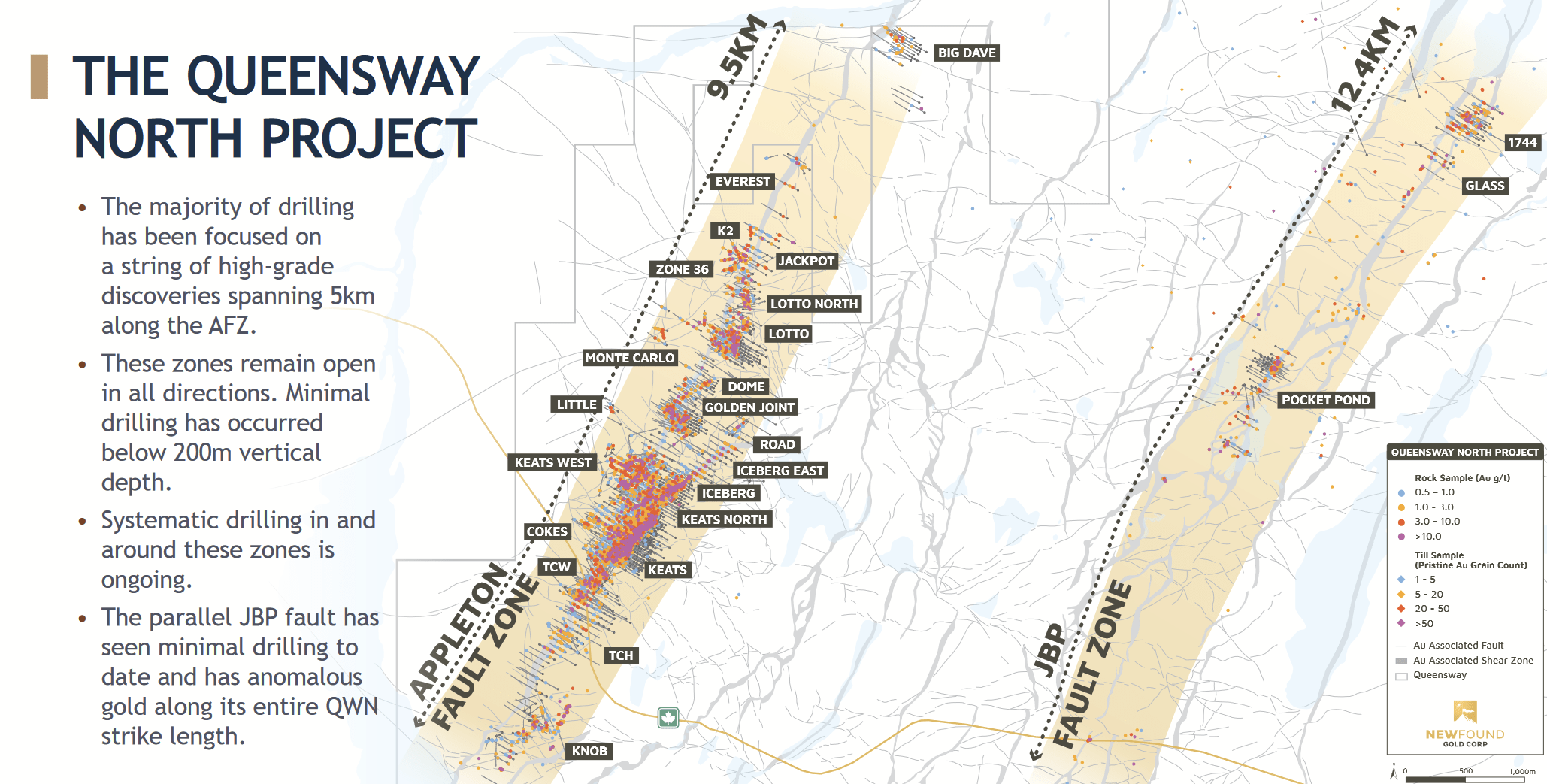

As this shows, most of the land is yet to be explored. Let's look at the various sites that have been drilled and assessed.

{kind=link}

Based on these samples that they have used to map out the area, the company believes several deposits of high-grade gold exist along the Appleton and JBP fault zones in the northern portion.

Financial Situation

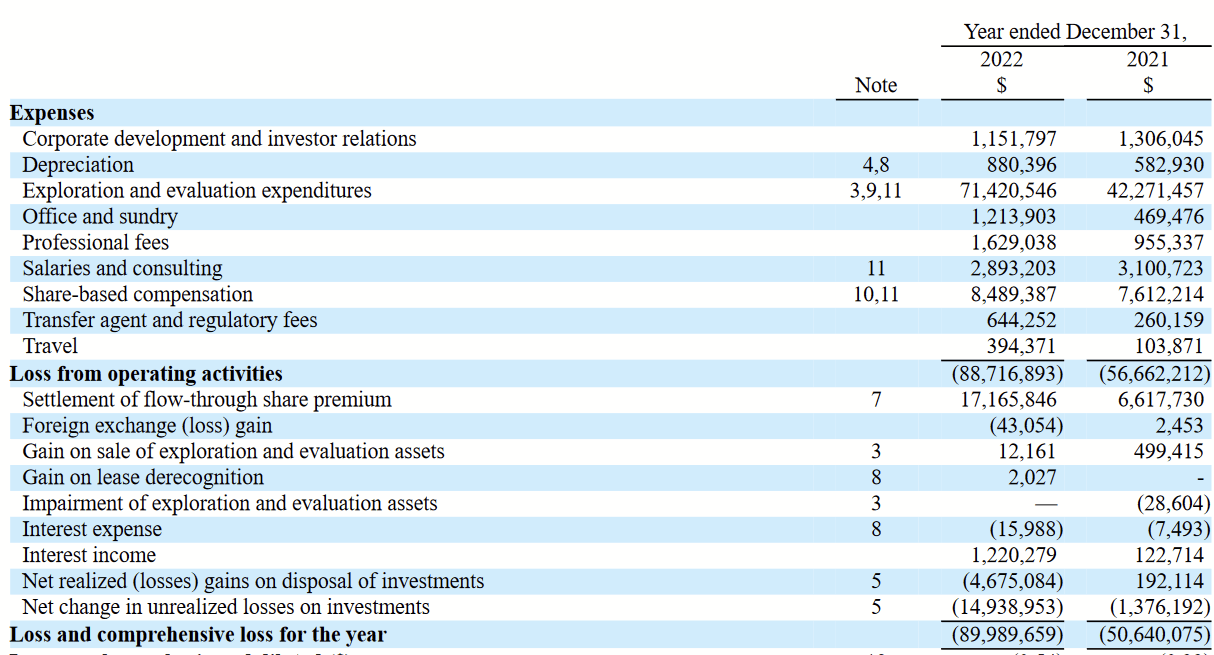

As the income statement shows (and as its exploration projects imply), the company has no revenues, only operating expenses.

{kind=link}

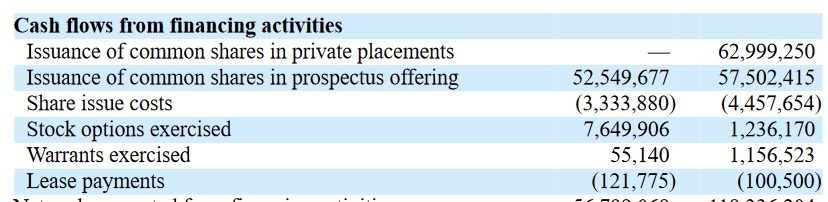

In 2022, they reported a loss of almost $90m in CAD. In order to fund operations without any revenues to support them, the company has been raising capital by selling shares.

{kind=link}

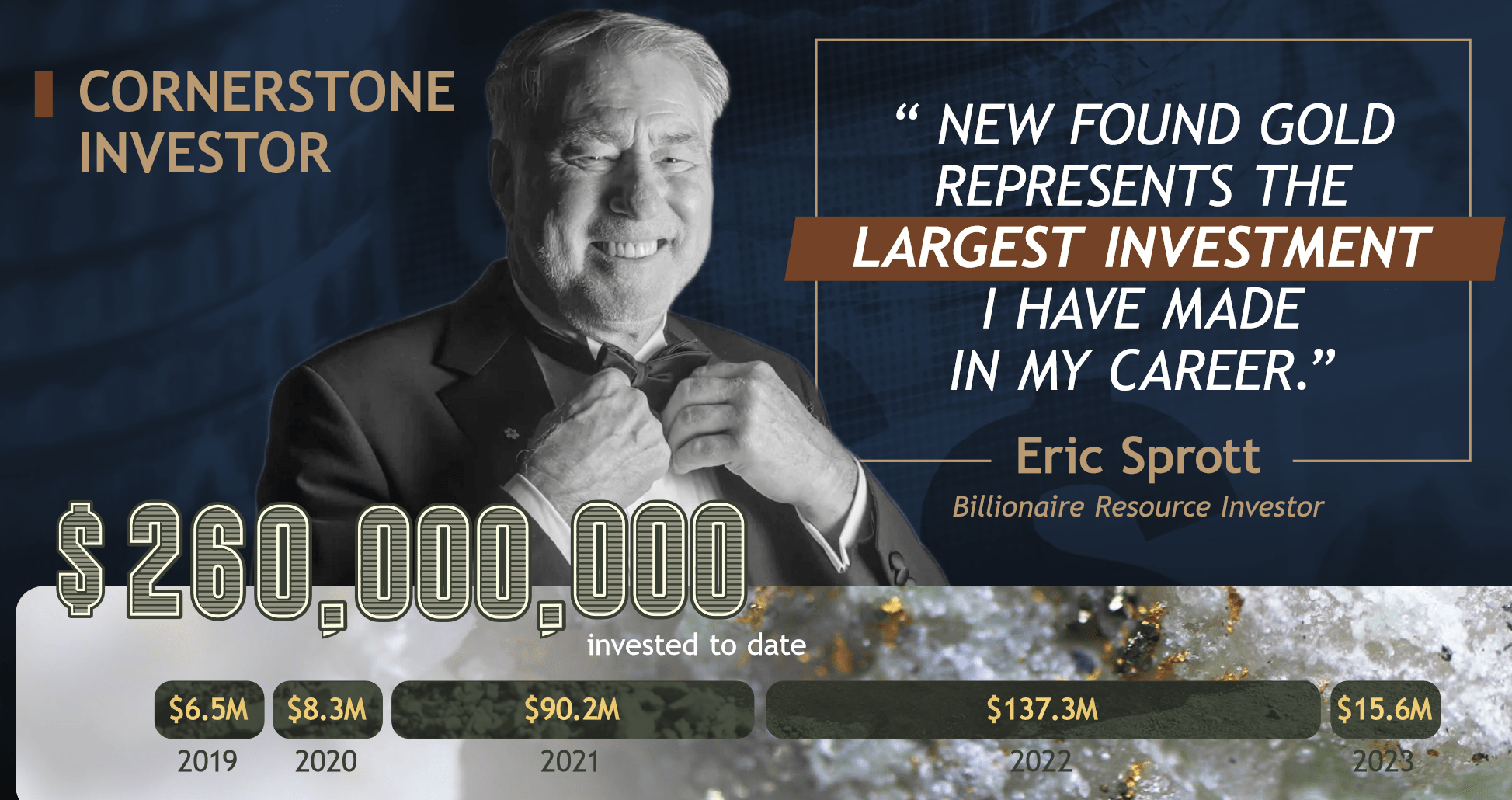

A significant amount of this has come from billionaire Eric Sprott, as the slide below shows.

{kind=link}

He stepped up his investments in 2022, with total contributions of almost $258m.

{kind=link}

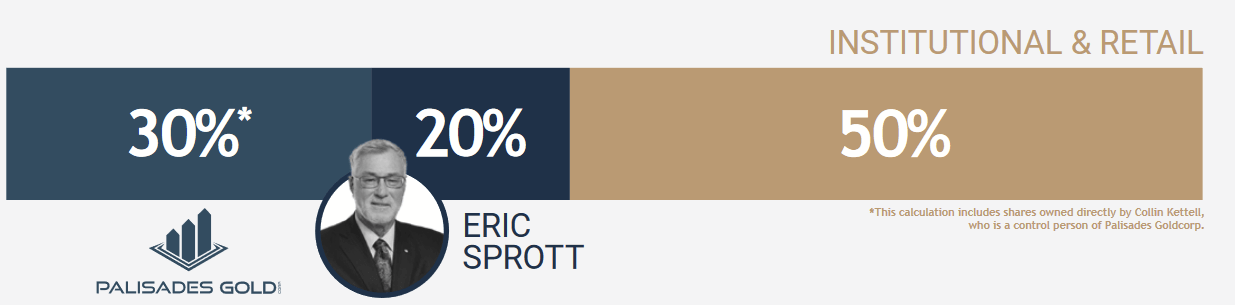

This gives him about 20% of the company and has made him the largest individual shareholder. Yet, the cash has been important to maintain the exploration of the property, which is consistently showing signs of gold deposits.

Management has not currently given indications of plans to develop the properties for mining. As such, it does not currently describe itself as a mining company but as a "mineral exploration company," per its last annual report.

A Look to the Future

Keeping the Business Going

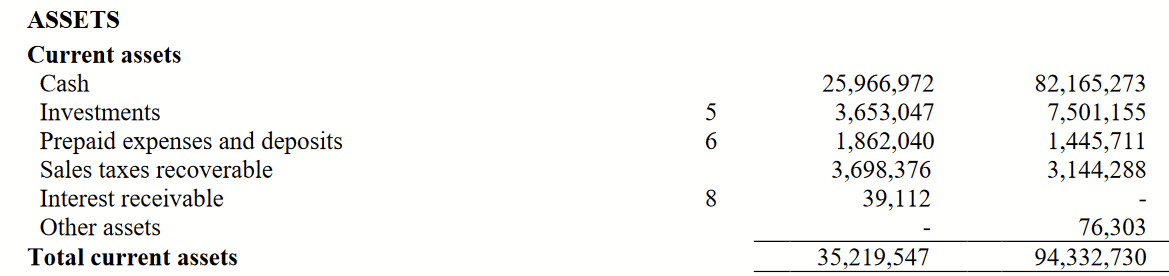

Currently, the company does not have adequate cash to maintain its operational needs.

{kind=link}

Cash declined from $82m to $26m from the end of 2022 to the end of Q3 2023. Given that expenses have been in excess of $70m each year, this will not be enough to continue each year. This means more capital will need to be raised. In its Q3 financial report , management even stated:

Management is actively targeting sources of additional financing through alliances with financial, exploration and mining entities, or other business and financial transactions which would assure continuation of the Company’s operations and exploration programs. In order for the Company to meet its liabilities as they come due and to continue its operations, the Company is solely dependent upon its ability to generate such financing. These items give rise to material uncertainties which may cast a significant doubt on the Company’s ability to continue as a going concern.

Historical data show just how major dilution of shareholders has been to keep this company going.

{kind=link}

I do believe that, with Eric Sprott's substantial, personal stake, the chances of the company lacking funds is lower than your average would-be miner. Yet, he will not be diluted by such a move; he will largely be the one diluting in my opinion.

Even if we can be reasonably sure that this company will grow into something that produces revenue, I think the dilution current owners would face will be greater than the improvement in financial results, even for long-term investors.

The Transition to Revenues

This company doesn't have revenue, and it's not clear at this moment when that will change. Given that it covers a fairly substantial swath of land with high grades of gold detected, there is a lot potential here.

At some point, the company will need to transition into development and production, generating cash from the sale of its ores. That process hasn't started yet. It does not have to be a lot either. The company can start with modest development at just one of the sites they have identified and use the cash from that to fund the development of newer mines and continue exploration with the larger, more southerly stretch of Queensway. Assuming the initial development generates positive cash flows, I think this should solve the dilution problem.

When To Buy

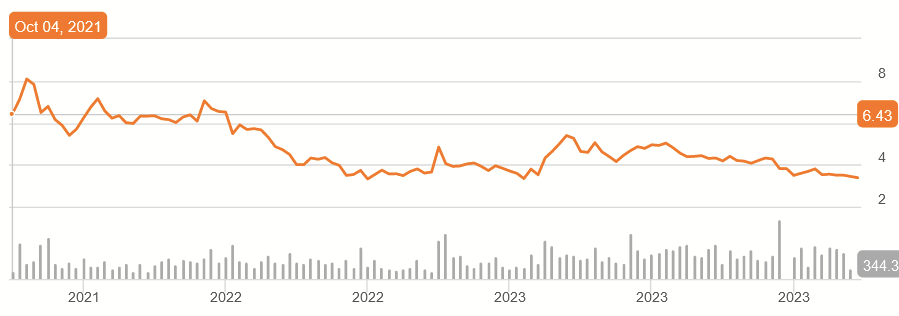

Folks who bought in during the IPO are likely disappointed. Take a look at the chart.

{kind=link}

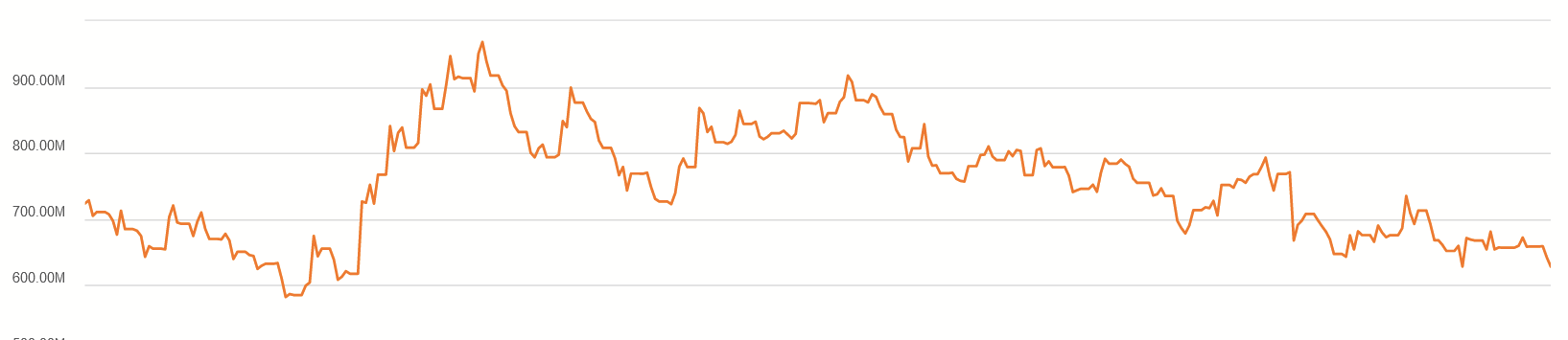

Yet, while the stock is currently about half of where it started, the market cap has not declined as much.

{kind=link}

It's a decline, yes, but we also saw a period where the value of the company as a whole was higher. The market seems to be orbiting around a belief that this company is worth somewhere between $600m and $800m. When I see a market cap for a company that has no earnings, I interpret that as a P/E of 10 for the possible earnings. Could a single mine produce $60m - $80m for the company each year? I believe so, as I've seen mines that do that and because there's a lot of ore over a large area here, but it's all a matter of A) when a mine is started and B) when that mine becomes profitable. In the meantime, I don't think NFGC is worth anything because there are simply no earnings to use as a basis for valuation.

Even if the market sticks to its general valuation, dilution will continue, and I believe the share price will decline accordingly. Holding this stock isn't helpful to the long-term investor until the fundamentals change to where the company is making money. At that moment, I think this company will be worth buying. I think it could easily be five years before something like that even happens.

Conclusion

Cash flow is king. This is a guiding principle when I invest. When I look at a company with consistently negative cash flows, I wait for things to change before I buy it. If any of us were to start our own businesses, whether it's a website or even a lemonade stand, we would do so only if we believe we will make more money than we put into it.

In this case, we have a company whose cash flows are negative, doesn't even have revenues, and whose operations are years away from reaching that point. It must continue to raise capital through share dilution. There's no gains to be made here, so it's not even worth holding in my view. If the company gives up, then I believe the shares could potentially be worth zero.

NFGC could prove to be a very lucrative investment, perhaps even a staple dividend stock. That's well into the future, and it's worth keeping our eyes peeled for that day to come. In the meantime, the risks of capital loss are too great, so NFGC is an easy SELL.

For further details see:

New Found Gold Corp.: A Sell Until There Are Revenues