CA - New Gold: A Tough First Half For This Mid-Tier Producer

Summary

- New Gold released its Q2 results earlier this month, reporting quarterly production of ~70,500 gold-equivalent ounces, a 33% decline from the year-ago period.

- This sharp drop in sales volume combined with higher sustaining capital led to a massive increase in costs, pushing New Gold's margins deep into negative territory in Q2.

- While this is quite disappointing, this was the definition of a kitchen sink quarter, and NGD should look completely different in 2024, more than doubling cash flow from FY2022 levels.

- So, while I continue to see more attractive bets elsewhere in the sector, I see New Gold as a Speculative Buy below US$0.61.

While most gold producers had a disappointing Q2 from a cost standpoint due to labor tightness and inflationary pressures, few companies fared as poorly as New Gold ( NGD ). Not only did New Gold see costs increase at a double-digit rate year-over-year, but costs soared to their highest levels in more than two years, coming in at $2,373/oz. While this pushed margins deep into negative territory, this was the definition of a kitchen sink quarter, and New Gold will look entirely different by H2 2023. So, while I continue to see more attractive bets elsewhere in the sector, I see New Gold as a Speculative Buy below US$0.61.

New Gold - Operations (Company Presentation)

{kind=link}

Q2 Production & Sales

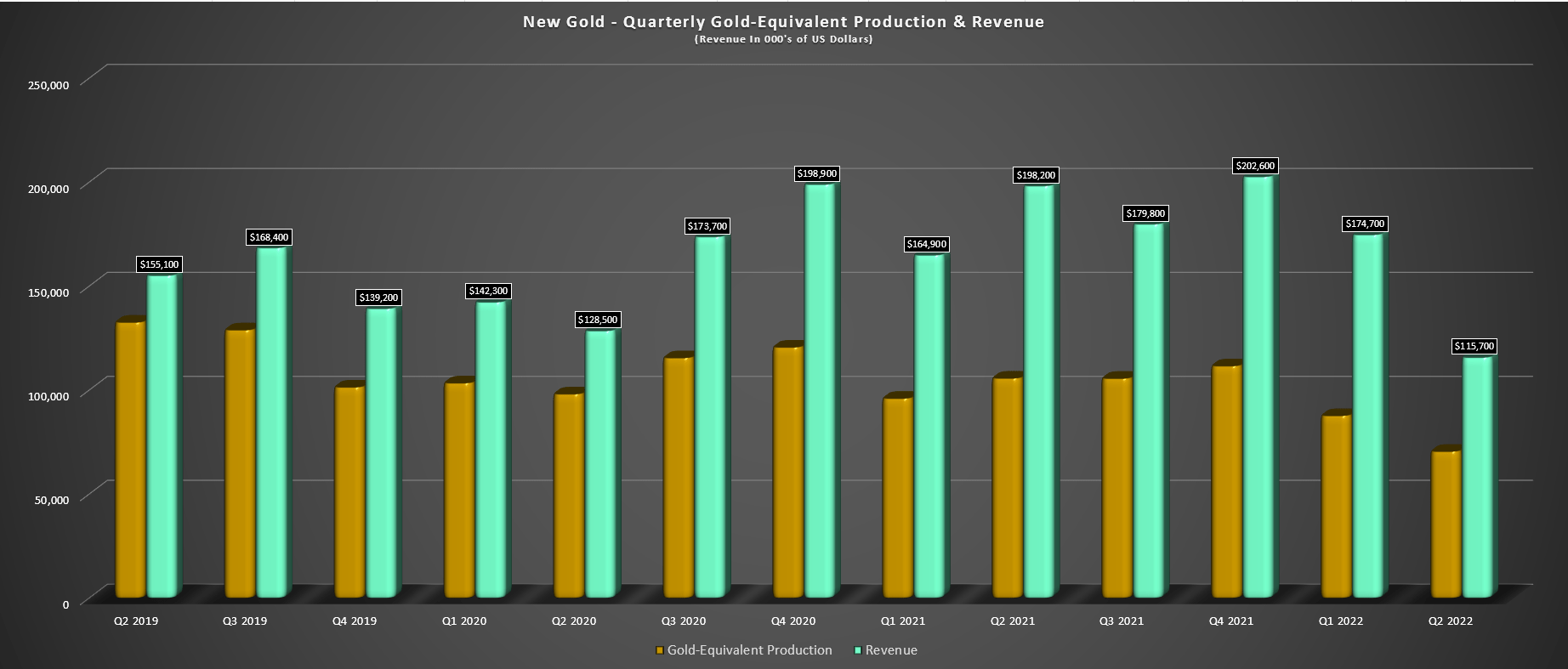

New Gold released its Q2 results earlier this month, reporting quarterly production of ~70,500 gold-equivalent ounces [GEOs], a 33% decline from the year-ago period. This was related to a sharp decline in grades at both of its operations, with Rainy River relying on stockpiles due to heavy rainfall and flooding in Fort Frances and New Afton processing much lower copper grades in the period with a reliance on stockpiles as well. The result was that the company is now well behind its planned FY2022 production levels of 390,000 GEOs (guidance mid-point), sitting at just ~158,200 GEOs year-to-date, more than 20% behind FY2021 levels in the same period (~201,700 GEOs).

New Gold - Quarterly Gold-Equivalent Production (Company Filings, Author's Chart)

{kind=link}

Looking at the chart above, we can see that this was the worst quarter for production in more than three years, and despite the higher gold price ($1,879/oz vs. $1,817/oz), revenue fell off a cliff, declining 42% to $115.7 million. This was related to the much lower production volumes in the period, exacerbated by a large discrepancy in ounces sold vs. produced due to ~7,500 GEOs, which were delayed into July at New Afton (timing of concentrate shipments). These lagging sales pushed into Q3 will boost the next quarter's revenue, but certainly didn't help in what was already a rough Q2. In fact, the delayed sales tacked ~$700/oz onto New Afton's already industry-lagging all-in-sustaining costs in the period.

New Gold - Quarterly GEO Production & Revenue (Company Filings, Author's Chart)

{kind=link}

Costs & Margins

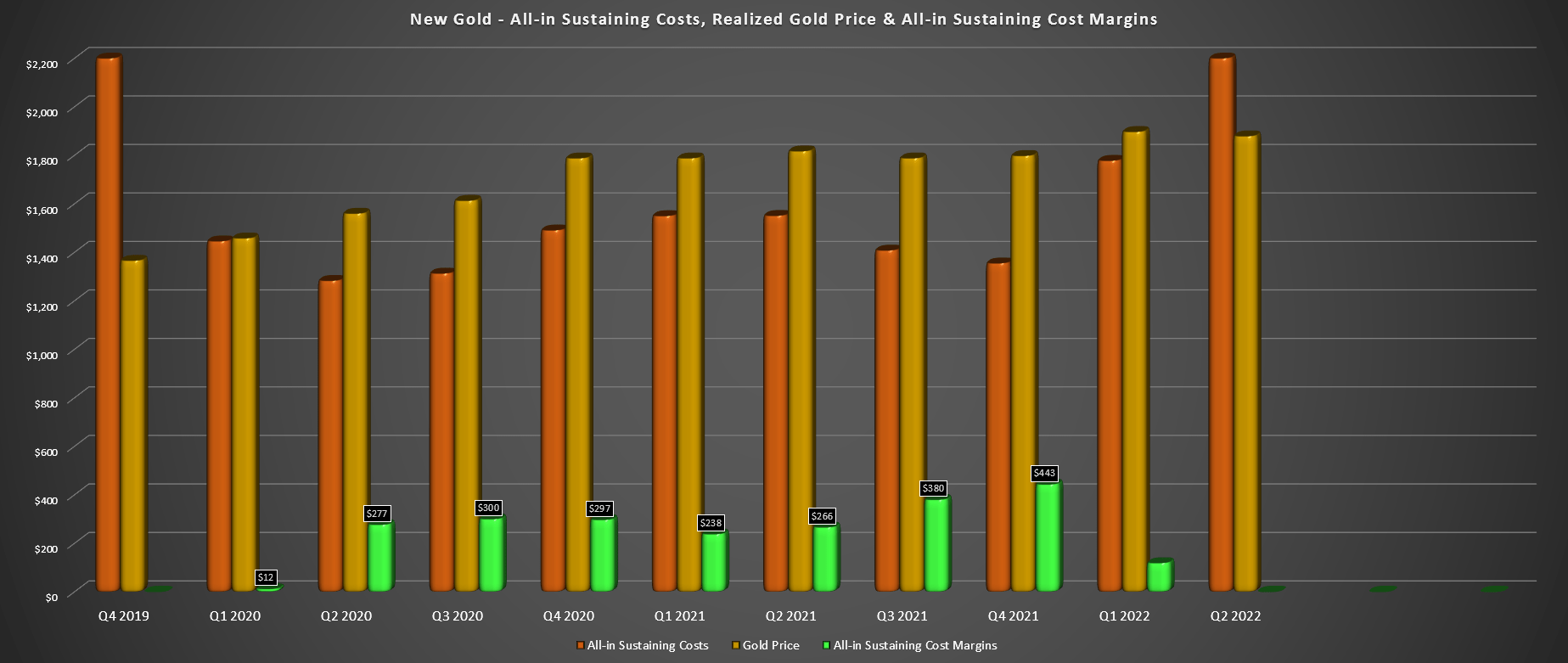

Moving over to costs, New Gold reported all-in-sustaining costs [AISC] of $2,373/oz in Q2, nearly taking the cake for the highest costs sector-wide in the period. The result was that AISC margins dipped to negative $494/oz despite a tailwind from a higher gold price in the period ($62/oz higher than last year's levels). This compared unfavorably to AISC margins of $266/oz in Q2 2021, which already left much to be desired, being more than 50% below the FY2021 industry average. That said, a couple of impacts in the quarter that are worth noting did distort the results.

New Gold - All-in Sustaining Costs, Realized Gold Price & AISC Margins (Company Filings, Author's Chart)

{kind=link}

For starters, New Gold saw a headwind from a lower realized copper price ($4.14/lb vs. $4.43/lb), and it had much higher sustaining capital in the period ($59.9 million vs. $49.2 million). In addition, production was impacted by the heavy rainfall and floods at Rainy River, leading to the company relying on lower-grade stockpiled ore. Finally, further exacerbating the cost increases was deferred sales of ~7,500 GEOs at New Afton that had a $140/oz impact on costs. So, while the Q2 cost figures were not easy on the eyes, this was a kitchen sink quarter, to say the least.

This weaker margin profile resulted in operating cash flow dipping to just $37.4 million from $110.2 million last year and prompted the company to revise its guidance to 345,000 GEOs at $1,925/oz at the mid-point, a massive downgrade from ~390,000 GEOs at $1,520/oz. The good news is that as mining heads underground at Rainy River [RR] and we prepare for mining the higher-grade C Zone in late 2023, New Gold will see a significant increase in margins, especially if the copper price can recover.

Valuation

Based on ~688 million fully diluted shares and a share price of US$0.65, NGD trades at a market cap of ~$572 million. This is a dirt-cheap valuation for a company with two Tier-2 jurisdiction operations and a portfolio. The problem is that with negative AISC margins in the most recent quarter and expected in FY2022, investor interest has waned considerably, which is to be expected. That said, the team certainly had a healthy dose of headwinds in H1 2022, and while the current margin profile leaves much to be desired, the future outlook for its mines is much more attractive. The reason is that C-Zone is a game-changer for New Afton, and higher grades from RR Underground, combined with lower open-pit strip ratios, will drive down costs considerably at its flagship operation.

New Gold - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

Previously, New Gold was looking very attractively valued on FY2022 cash flow estimates in June, trading at just 3x FY2022 estimates ($0.43) and ~2.5x FY2023 estimates. However, with the significant guidance cut and meaningful increase in cost guidance, FY2022 and FY2023 cash flow estimates have slid to $0.26 and $0.46, respectively, leaving NGD trading at a similar cash flow multiple even after a 50% decline in its share price. The good news is that this decline in cash flow is temporary due to the much weaker operational performance but will correct itself as production from the B Zone ramps up and commercial production begins at year-end from Intrepid (RR Underground). So, New Gold remains very attractively valued on a forward cash flow basis (~1.5x FY2023 estimates).

Under the previous New Gold of the last cycle, I would not give the company credit for any forward estimates. However, the leadership team has been strengthened here with a new CEO in 2018, Renaud Adams, and the appointment of a new COO, Patrick Godin (Q2 2022). For those unfamiliar, Godin has over 30 years of technical and operations experience and was Vice President and COO of Pretium (PVG) before its acquisition.

{kind=link}

The combination of stronger leadership and the best years of its assets finally ahead of the company with the heavy lifting done (underground development nearly complete at RR) de-risks the path to a much more attractive growth profile post-2022. Therefore, I would view NGD as a Speculative Buy on further weakness (below US$0.62). Finally, while insider buying is not always a great timing tool, it is worth noting that insiders have stepped up to the plate recently, with steady insider buying between C$0.84 and C$1.05 since August, or the equivalent of US$0.67 to US$0.84.

Summary

New Gold had one of the roughest first halves among its peer group, severely impacted by heavy rainfall and flooding at Rainy River and lower grades with delayed receipt of its B3 permits and work to close the recovery level zone in June. However, the company should have a better H2, and we should see a significant improvement in operations starting next year, benefiting from higher grades at both operations. So, while it's easy to be negative on NGD given the horrid Q2 results and negative guidance revisions, I see a much brighter future for the company.

New Gold Operations (Company Presentation)

{kind=link}

Having said that, I prefer to buy elite companies in any sector I'm investing in, which means looking for those businesses with industry-leading metrics. While New Gold is a clear turnaround story, I've had limited success with turnaround stories in this sector from experience, with them often underperforming the sector. This doesn't mean that NGD can't bottom out near US$0.60 and go much higher, but with companies like Agnico Eagle ( AEM ) also trading at a 60% discount to historical cash flow multiples. So, while I expect further weakness in NGD to present a speculative buying opportunity, I am currently focused elsewhere.

For further details see:

New Gold: A Tough First Half For This Mid-Tier Producer