IIPR - NewLake Capital: Get A 12.7% Yield In A Growing Industry

2023-06-08 12:13:47 ET

Summary

- NewLake Capital is a REIT providing real estate capital to state-licensed cannabis operators in the US.

- NLCP's financials show a strong balance sheet, low debt, and a growing dividend.

- My analysis leads me to a buy rating.

NewLake Capital (NLCP) is a REIT that provides real estate capital to state-licensed cannabis operators in the US. The company was founded in 2019 and IPO'd in 2021 so it is very new. The future of this firm seems bright as the industry is expected to grow in the following years. Here are a few facts to back this up:

59% of Americans think that marijuana should be legalized on a federal level in the US for medical AND recreational purposes, 30% believe it should be legal for medical purposes, and only 10% do not think it should be legalized at all. The map of the states where cannabis is legal right now is below. It's easy to imagine the expansion prospects when more states join.

NLCP

Furthermore, the industry is supposed to grow from $26.1 million to $44.5 million by 2027, which represent an annual CAGR (cumulative average growth rate) of 11.2% per year, which would of course work in favor of NLCP which operates in the space. This major tailwind is key to my thesis for the company.

NLCP

Now for the company itself. They own 32 properties in 12 states totaling 1.7 million square feet of space. The properties are primarily leased to limited-license jurisdictions and it is 100% leased with a very long 14.6 weighted average remaining lease term.

64% of the tenants are public companies and 36% private. The biggest tenant is Curaleaf (CURLF) accounting for 22.4%. Cresco Labs (CRLBF), Revolutionary Clinics, and Trulieve (TCNNF) all take up around 10%. This definitely presents a concentration risk even though it seems that the company is trying to diversify the tenant portfolio as well as stick with some of the strongest players. While the tactic seems to be working so far it is something to take into account. Moreover the fact that a large percentage of companies are private, makes it much harder to evaluate the credit worthiness of these tenants as private companies don't have to report their earnings and aren't under as much scrutiny as their publicly traded peers.

NLPC

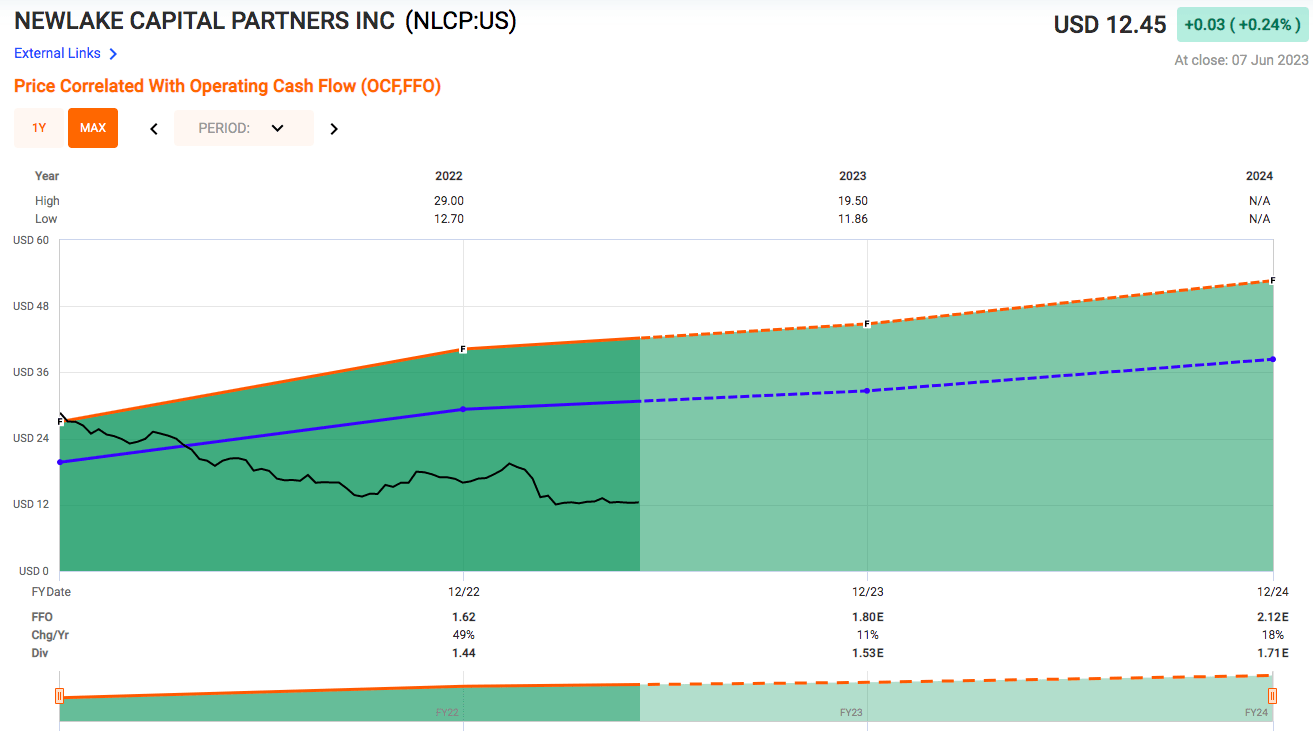

The FFO for the 1st quarter was $9.5 million ($0.44 per share) which is a 9.4% decrease from the last quarter. However, YoY the FFO increased by 21.1% and revenue by 12.3%.

Their balance sheet looks great as well. Their debt is only $2 million with a debt/EBITDA of 0.2x which is extremely low. The weighted average interest rate is 4%. Half of the debt matures in January 2024 which the company should have no problem with considering they have $41 million in cash and $89 million available on their credit line and half of the debt is only $1 million.

The dividend is $0.39 per share per quarter, so $1.56 per year. This translates to a very nice 12.7% yield and is well covered with an 86% payout ratio. The dividend has also seen growth since last year from $0.33 per share which is an 18% increase.

A risk I would like to mention is that the company can have issues with potential regulations in the United States. The states themselves can legalize cannabis and there is a distinction between medical and recreational use. However, on the federal level it is highly regulated and there is no distinction at all. Therefore, any new federal laws regarding the use of cannabis established by the US that would limit the business operations of NLCP's tenants would negatively influence NewLake Capital. However, with more states legalizing cannabis on state levels, I do not see this as a huge risk.

The P/FFO is at 7.32x trading way below the historical average of 18.1x. The analysts on FastGraphs expect the FFO to grow by 11% by the end of the year and by 18% in 2024. For reference, Innovative Industrial Properties ( IIPR ) trade at 9.12x. This leads me to believe that NLCP is a bit undervalued in comparison.

To sum up, the company has a really high dividend yield that is well covered, a strong balance sheet that presents no threat, and is in a growing industry. This leads me to a BUY rating for NLCP here at $12.45 per share. Considering the expected growth for the industry and the estimates on FastGraphs I expect an average annual growth of 18% over the next two to three years. This should translate into per share FFO of $2.12 by 2024/2025. Assuming a multiple expansion to 12x, which is still conservative considering that it's only half the gap to the long term average, yields a price target of $25 per share. That's over 100% of upside potential from today's level.

{kind=link}

For further details see:

NewLake Capital: Get A 12.7% Yield In A Growing Industry