IIPR - NewLake Capital Partners: Short-Term Volatility Creates Buying Opportunity

2023-03-17 12:56:19 ET

Summary

- Since February 10, NLCP shares have lost approximately 1/3 of their value.

- On March 9, the company presented Q4 and FY22 results. While the actual results were stellar, the forward outlook for FY23 was far from great.

- The long-term risk/reward on the investment seems favorable, as long as investors are willing to stomach the likely high volatility ahead.

After taking a long hiatus from contributing, I have decided to return and share some of my investment ideas with the community. Although it has been a while since my last piece, and even if my employer might prevent me from making regular contributions, I will do my best to upload more content in the coming weeks. As we experience a period of heightened market volatility, I find it too exciting not to write about these market gyrations. The increased volatility in the stock market is creating great opportunities for profit, for both long-term investors and traders alike.

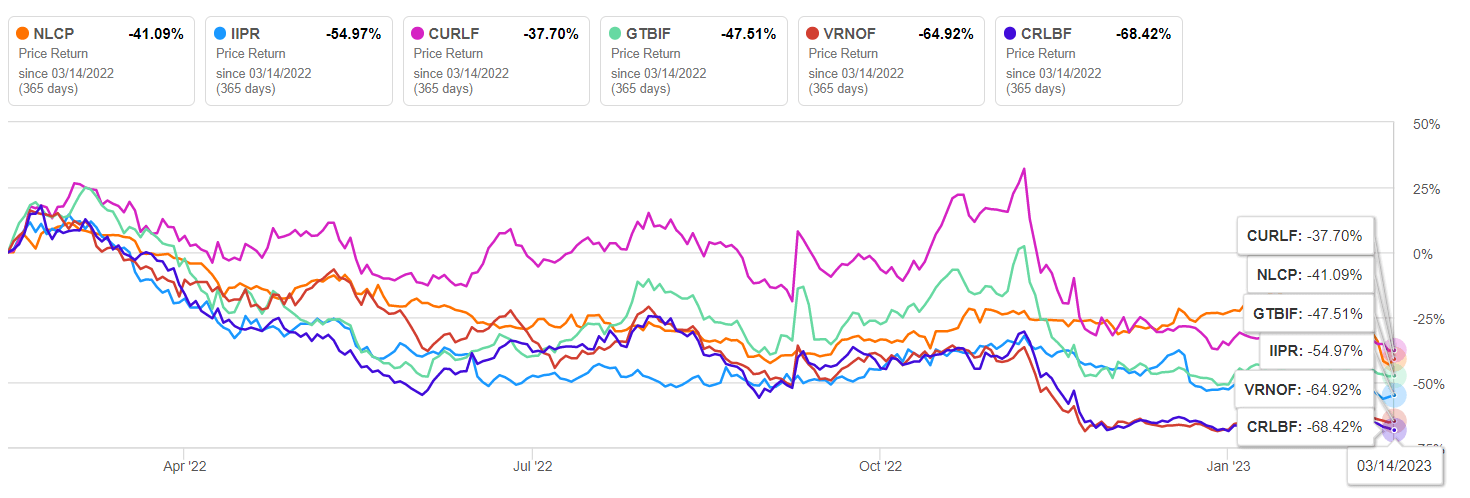

The first investment idea I am presenting is cannabis REIT NewLake Capital Partners Inc ( OTCQX:NLCP ). Headquartered in Connecticut, the company only began an OTC listing in August 2021 and has since lost 50% of its initial offer price. While some may assume this is another busted IPO, it is important to note that the drop was not due to company-specific issues but rather reflects the deflating valuations in the entire cannabis sector. Large players, including MSOs (whether NCLP tenants or not) and peer REIT Innovative Industrial Properties ( IIPR ), have all shared similar one-year market performance, and a tight correlation is expected to continue going forward

{kind=link}

The cannabis industry has undoubtedly entered a new and more challenging stage, and traders who foresaw the upcoming issues back in 2021/2022 made the right call. Previously, cannabis businesses in the US grew like a weed (pun intended), but management decisions are no longer focused solely on top-line growth. In a challenging macro-environment where inflation is driving up costs and interest rates are rising, access to capital has become more difficult, and cash-flow preservation and operations streamlining have become the new priorities. Additionally, producers continue to face price competition from illegal suppliers .

I want to begin by warning potential investors that as we navigate 2023 and beyond, there is likely to be additional headline risk that could impact the cannabis industry and hence short-term stock prices. Furthermore, it is difficult to ignore the possibility that some weaker MSO players might end up going bust or having to restructure. Such events could impact not only a few quarters of rent collection, but multi-year FFO projections for landlords like NCLP and IIPR.

Longer-term investment thesis for the cannabis industry

There are several factors that lead me to believe that the long-term outlook for the cannabis industry remains favorable, and hence, the investment case remains intact. In my opinion, investors with sufficiently long investment horizons should remain bullish due to the following reasons:

- A vast majority of Americans support legalizing cannabis for recreational use, and this percentage has continued to grow over time. This raises the question of when, rather than if, recreational cannabis will be legalized at the federal level. Despite lobbying efforts to maintain the status quo, the political cost of doing so will eventually become too great.

- The legal cannabis market is projected to triple by 2030. Various US cannabis market reports forecast that the industry will grow at a compounded annual growth rate [CAGR] of 14% through the end of the decade. This is a very bullish figure, which implies that the size of the legal market will increase from approximately $15 billion in 2022 (on top of an estimated $80 billion illegal market) to almost $45 billion in 2030.

- Efficient operators, such as Green Thumb Industries ( OTCQX:GTBIF ), have already scaled beyond the breakeven point and achieved a sustainable operating model, allowing for profits and positive operating cash flows. This is a critical consideration as it reminds investors that a viable business model can be achieved even in the current environment.

Longer-term investment thesis for NewLake Capital Partners

Above arguments are valid for most MSO operators and landlords alike and set my overall bullish outlook for the US cannabis industry. To be transparent, I anticipate that the best stock market returns will be for those choosing the "best" vertically integrated MSO rather than a REIT, but I see this as a personal risk/reward tradeoff choice. A “Cannabis REIT” could be an interesting investment vehicle, alternative (or in complement) to MSOs exposure to those seeking a lower-risk (and higher-yielding) name in this space. Publicly listed REITs IIPR and NLCP both fit the bill, and I have a moderately bullish view also of IIPR, but I favor NLCP between the two for a few reasons:

- Lower Debt. While leverage will likely play an important role in the future, I consider the course of action of NLCP to essentially remain debt free (Debt/EBITDA of 0.3x, as per latest report) the prudent one in the current business environment. As my former CFO used to say, "Remember, you can't go bankrupt if you don't owe anything to banks." While leverage will likely play an important role in the future, NLCP's lack of debt makes me confident in its viability and ability to recover from a possible industry slump. In addition, NewLake does not have any preferred shares (that, as rating agencies, I tend to view as a debt instrument) in its capital structure.

- NLCP's conservative underwriting practices include a focus on limited-license jurisdictions, where the market is expected to be less volatile. Additionally, licenses themselves have economic value, and NLCP has no exposure to potentially riskier markets like Oregon and Washington.

- NewLake has a strong management team with a track record of success. From my research on the people involved in the business I believe both the management team and board of directors, led by DuGan, bring valuable expertise to the company's success. Management has skin in the game. Also, while internally managing a REIT comes with structural costs, I do not usually consider externally managed REITs investable due to the substantial misalignment of interests between management and shareholders.

A rebuttal of bears’ arguments

In the past month, there has been a decrease in the overall sentiment towards NLCP among SA authors, coinciding with a decline in the company's share price. As an investor, I welcome this development as it provides exposure to a variety of viewpoints, allowing for better-informed decisions. It also challenges my long thesis, requiring me to reconsider whether my original assessment was correct. I hold a great deal of respect for authors who are willing to issue sell ratings, regardless of whether I agree with them or not. Like short sellers, they provide balance to the market and often work hard to present their cases. While some bearish points have been raised, I believe they can be refuted (at least in part), which should provide some reassurance for those who hold a long position. In the following sections, I will address some of these points.

Point 1: Federal legalization would provide an additional source of capital through banking, disproving the business model of companies like IIPR/NLCP.

Banks would not be an alternative source of capital, but rather a complementary one. Improved access to banking would immediately benefit IIPR/NLCP tenants, which would in turn be a bullish development for landlords. Furthermore, the business model of triple-net lease REITs such as W.P. Carey ( WPC ) has stood the test of time, despite their customers having access to bank loans. REITs are an attractive source of capital for modern consumer and service companies who prefer to operate asset-light models. And even if some hardcore bears argue that the rates offered by banks will be much lower, the truth is, not quite. REIT lenders are not loan sharks and are skilled at pricing risk. It's simply their job. This statement also leads me to the second bear argument.

Point 2: Rent is far above market rent for similar industrial space.

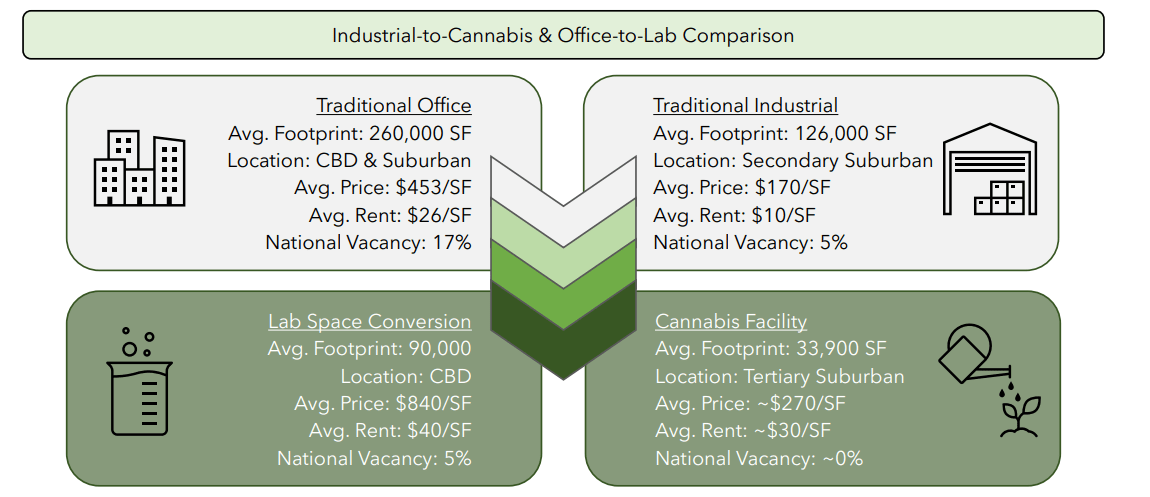

While it is true that the rent per square foot may be higher than that for warehouses, this does not necessarily mean that it is "far above" market rates. The rates must reflect two important factors: the tenant's risk and the actual costs of the landlord for the facility. Cannabis cultivation sites are not the same as warehousing facilities. For instance, they require permits that are not as easily granted as those for warehouses. In limited-license jurisdictions, these permits have an economic value themselves, which goes to the owner of the facility and not the operator. Additionally, if the facility is equipped, the equipment will have a cost that needs to be reflected in the rent. However, it's worth noting that the current overall capital investment cost of approximately $220 per square foot for NLCP is below the estimated industry average of $270 per square foot. In my view, a comparison with industrial REITs such as Rexford ( REXR ) is not apples to apples, and the same can be said of one with Americold ( COLD ), another niche industrial space REIT for which we do not know the overall per square foot acquisition price but we know it is no stranger to deals that value cold storage facilities at $300 per square foot.

While it is true that purpose-built cultivation facilities have a higher equipment component, this is not unique to NLCP. Other REITs, such as COLD, also have valuable equipment for which rent is paid. However, equipment does depreciate, and eventually, NLCP will need to allocate maintenance CAPEX for it, similar to how hotel REITs handle room refurbishments. Nevertheless, like hotel furniture, equipment can be moved in a worst-case scenario, albeit at a cost. The argument that re-leasing is impossible when current estimated vacancy rate is 0% (compared to traditional industrial, which is relatively low at 5%) is a tough sell. While there may be challenges in re-leasing a specialized cultivation facility, the lack of available space in the market suggests that demand is high.

{kind=link}

Point 3: Tenants are going to default.

This is, in my opinion, the only notable cause of concern. Yes, it is likely this will happen to some extent, though I would also add “as they do in every other economic sector”. The problem is that cannabis REITs operate in a nascent industry where concentration risk is real. There are no solutions other than stick with the perceived strongest players or seek tenant diversification. I think NLCP has put up its best effort to do a bit of both, though it is far from safe.

{kind=link}

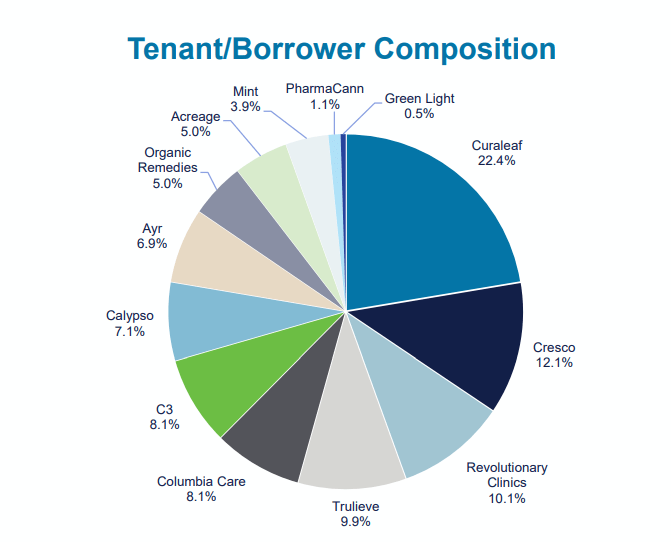

The top five tenants as of the latest report were Curaleaf ( OTCPK:CURLF ), Cresco Labs ( OTCQX:CRLBF ), Revolutionary Clinics, Trulieve ( OTCQX:TCNNF ), and Columbia Care ( OTCQX:CCHWF ), representing almost 2/3 of the total. However, Revolutionary Clinics has not paid rent in Q1 2023, and while I believe Curaleaf, Cresco, and Trulieve are safe, I am uncertain about Columbia. M&A consolidation in the space, which has been steadfast in recent years, could be a potential solution. Still, it would worsen the already high concentration risk.

Finally, it has come into question whether NewLake is an efficient operator due to high overhead costs (SG&A). While it's true that these costs are currently high, I believe they are a necessary evil of management internalization. Furthermore, I think the argument is overly punitive towards a REIT that has only been around for a couple of years. When you consider that low leverage is typically associated with a higher SG&A cost structure, it's unfair to use this as a criticism of NewLake. In fact, a REIT with a 50% LTV ratio has essentially double the capital to form its revenue base than one with zero leverage.

Headwinds to monitor

To conclude this extended review of risks associated with the investment, I want to highlight two key areas that I will monitor closely over the next few months:

- Tenants’ composition and concentration risk. In specific, I’ll be looking favorably at any further capital deployment that dilutes the percentage of revenue coming from the top five tenants. Few disclaimers: the exception of Trulieve (as I think they are the strongest in the group) and a further check on the relative strength of the new tenant brought onboard, to ensure diversification is not instead deworsification. A strong potential negative could be the signing of a new lease with Revolutionary Clinics (increased dependency on a weak tenant as part of a deal to recollect the missed payments on the current leases).

- I expect some delays in collections to become the new normal in the industry. 100% collection was a dream, while it lasted. However, if the collection rate drops below a certain point, it would indicate that a situation of deterioration has turned into acute distress. At that point, I would not want to hold onto the investment any longer and would consider selling it, even at a loss.

Valuation and conclusion

As a long-term investor, my target price for NLCP is intended only as a reference point and I do not plan to sell immediately if the target is hit. However, other investors may have a different approach. The target price serves as a guidepost in case the market becomes volatile in either direction.

With this in mind, I am valuing NewLake at about $20 per share here based on NAV value. This figure is almost in-line with NLCP tangible book value per share, and I think the approach makes sense considering the relatively young age of the assets. The target prices NLCP at less than 12x forward FFO, which is considerably lower than industrial REITs and, in my view, reflects correctly the higher risks involved in the cannabis space.

Considering NLCP as a high risk/high reward kind of investment, my recommendations are based on an arbitrary margin of safety placed at 30% for BUY, and 50% for STRONG BUY respectively.

Price at submission: $13.90

BUY - $14 or below / STRONG BUY - $10 or below

For further details see:

NewLake Capital Partners: Short-Term Volatility Creates Buying Opportunity