CA - Newmont: Margins Improve But Production Below Plan

2023-10-27 03:22:22 ET

Summary

- Newmont's Q3 production declined by 13% because of disruptions at its Penasquito and Ahafo mines, as well as lower production from joint-venture assets.

- Meanwhile, all-in sustaining costs increased by 12% year-over-year to $1,426/oz, with full-year AISC expected to be around $1,400/oz (related to higher than planned sustaining capital spending).

- In this update, we'll dig into the Q3 results & why it's worth ignoring the softer performance, given that the NCM deal will transform NEM into a larger/lower-cost miner.

The Q3 Earnings Season for the Gold Miners Index ( GDX ) began this week and one of the first companies to report its results was Newmont ( NEM ). Unfortunately, the results were a little below my expectations given that while I was anticipating no contribution from Penasquito, its larger Ahafo Mine was also disrupted with much lower throughput, resulting in lower output year-over-year despite a significantly improved grade profile. Meanwhile, production at its joint-venture assets also came in below plan (~352,000 ounces combined from NGM and Pueblo Viejo), further affecting production. Finally, all-in sustaining costs [AISC] were up 12% year-over-year to $1,426/oz, with full-year AISC now expected to come in closer to $1,400/oz, well above prior guidance ($1,200/oz), albeit impacted by higher planned sustaining capital spend. Let's take a closer look at the quarter below:

{kind=link}

Q3 Production & Sales

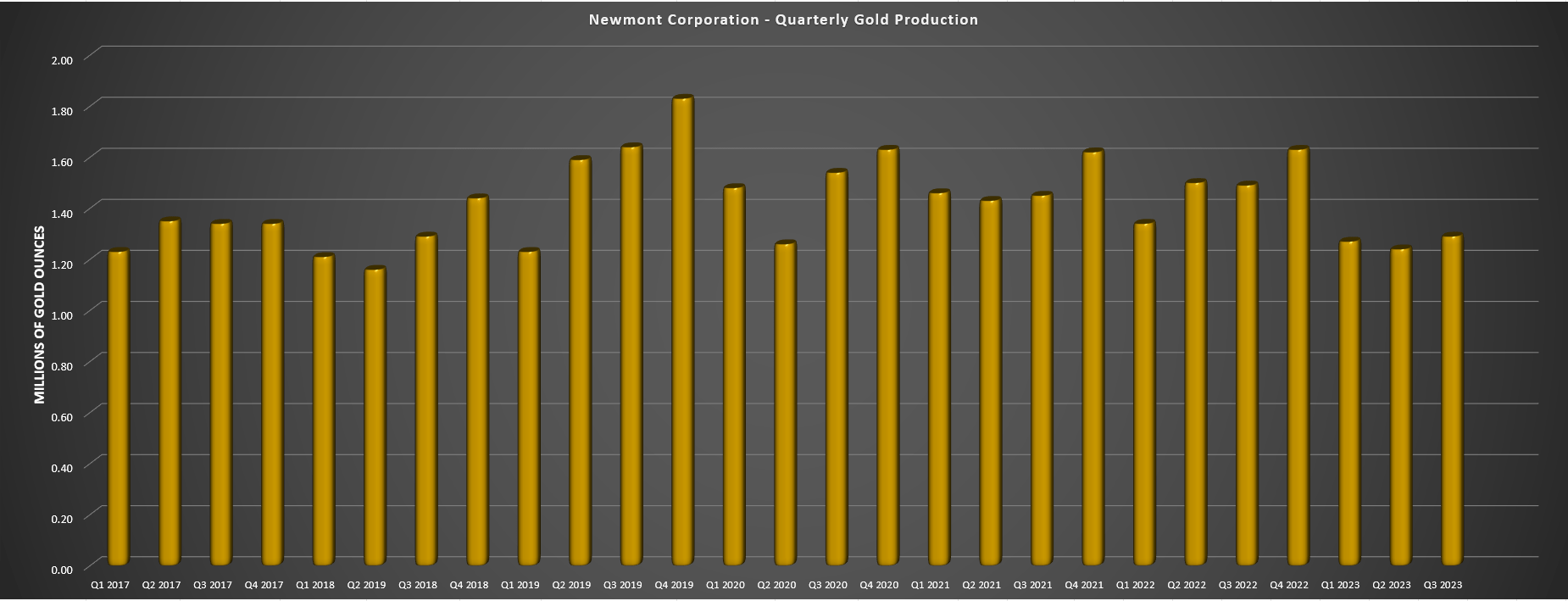

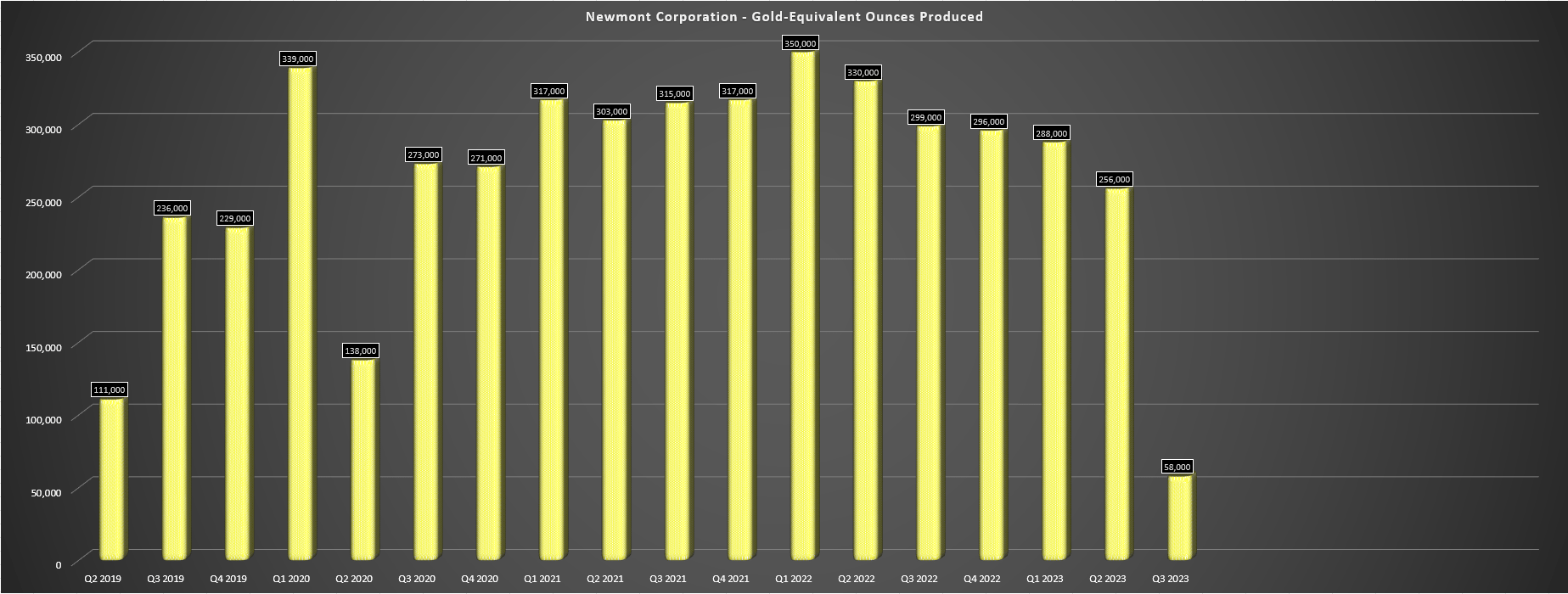

Newmont released its Q3 results this week, reporting attributable production of ~1.29 million ounces of gold, a 13% decline from the year-ago period. The sharp dip in production was primarily related to the company's massive Penasquito Mine being offline, but also to a softer than planned quarter at Ahafo despite the guided up-tick in grades (2.75 grams per tonne of gold processed vs. 1.89 grams per tonne of gold in Q3 2022), and lower production from its joint-venture partner at Pueblo Viejo (delayed ramp-up of PV Expansion). And while this was mostly related to one-time headwinds (Ahafo, Penasquito), the lower output at these mines combined with slightly fewer ounce sold vs. produced resulted in Newmont reporting a 5% decline in sales year-over-year with Q3 revenue of ~$2.49 billion.

Newmont - Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

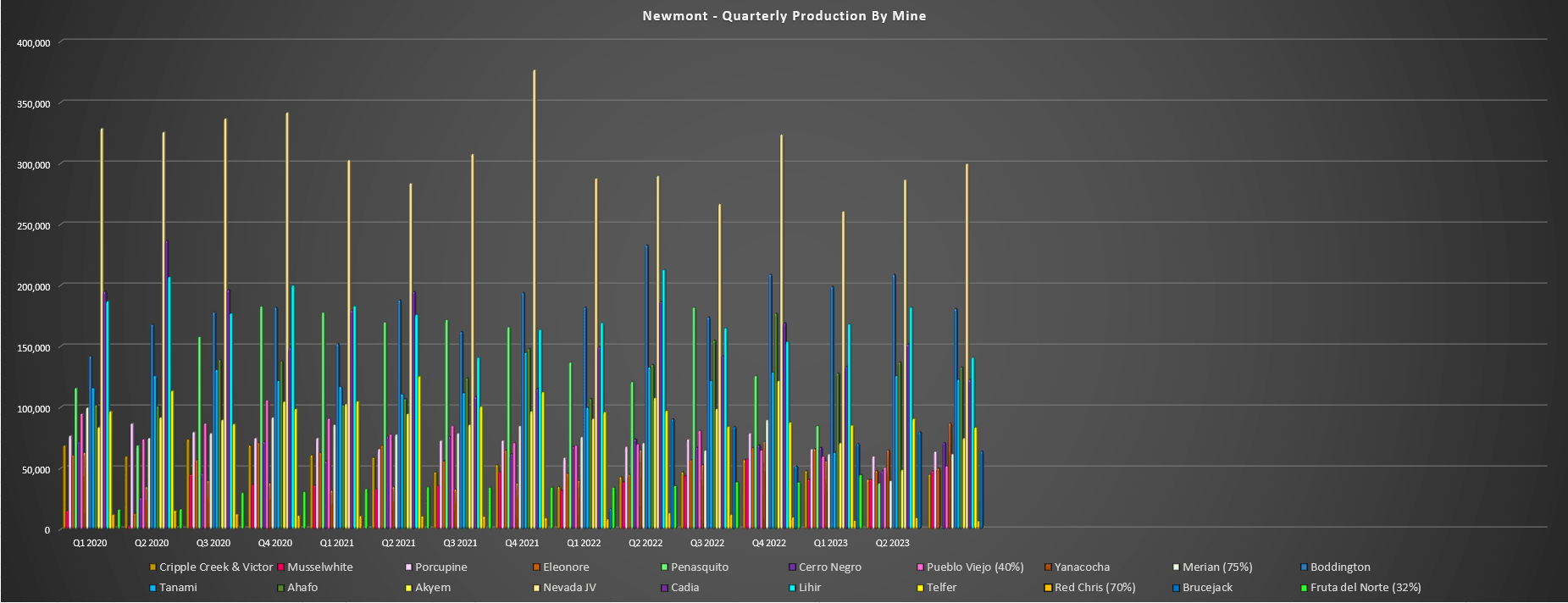

Digging into the results a little closer, investors will be pleased to know that aside from the 8% wage increase agreed upon between Newmont and the National Union of Mine and Metal Workers of the Mexican Republic, things are back to normal at its Penasquito Mine with a return to full operating capacity expected by year-end (resolution announced in mid-October). Unfortunately, the up-tick in production here will be partially offset by lower output at another of Newmont's massive assets, Ahafo, where the company noted that it identified damage to in the SAG mill girth gear that resulted in the mine operating below full capacity in Q3, which is why production was down year-over-year to ~133,000 ounces despite what would have otherwise been a 200,000 ounce plus quarter assuming a ~2.5 million tonne throughput rate. And while this did severely impact Q3 production and Newmont has optimized the circuit to operate at ~80%, full processing won't be reached until Q2 2024 when the damaged gear is replaced.

Newmont Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

Moving to Australia at two of the company's other largest operations, production was up year-over-year at Boddington (~181,000 ounces vs. ~174,000 ounces) on the back of marginally lower grades but higher throughput of ~9.1 million tonnes per annum. Meanwhile, at Tanami, production increased marginally to ~123,000 ounces at industry-leading costs of $890/oz after a slow start to the year (rainfall event), and this is a mine that will enjoy even lower costs once the Tanami 2 Expansion is complete, adding a shaft to the operation to a vertical depth of 1,460 meters. And as investors familiar with Newcrest will know, Newmont is expected to see a significant increase in its Australian production to 1.8+ million ounces per annum next year assuming Telfer is not divested. And these ounces will come at a lower-cost overall, with Tanami 2 set to improve costs and Cadia being a much lower-cost operation, with AISC at Cadia of $45/oz.

Looking out across some of the smaller assets in the portfolio, Newmont's Canadian production declined year-over-year to ~162,000 ounces (Q3 2022: ~175,000 ounces), with the higher production at Musselwhite and Eleonore offset by lower output at Porcupine. And while Newmont's output from Canada will also increase materially in Q4, with the addition of Red Chris (70% of a copper/gold mine), and Brucejack (high-grade underground gold mine), costs for its Canadian operations will remain elevated with costs at these operations continuing to be well above the sector average, with year-to-date AISC of $1,869/oz, $1,545/oz, and $1,855/oz at Musselwhite, Porcupine, and Eleonore, respectively. And while this is partially because of higher sustaining capital, these assets continue to be a drag on the company's overall cost performance.

{kind=link}

Finally, as for Yanacocha, Cerro Negro, Merian and Akyem, production was higher at Cerro Negro (higher grades and throughput) and Yanacocha (increased leach pad production because of injection leaching), offset by lower output at Akyem, where lower grades and throughput resulted in a nearly 25% decline in production (~75,000 ounces vs. ~99,000 ounces). And although Merian reported much higher throughput in the period at ~3.7 million tonnes, production was lower here as well by ~4% due to lower grades and recoveries. Lastly, from a gold-equivalent ounce [GEO] standpoint, the drop-off was even more severe (down 82% year-over-year) given that the only co-product output came from Boddington with Penasquito temporarily offline. The result is that Newmont has reeled in its previous production guidance of 6.0 million ounces to ~5.3 million ounces of gold, with all-in sustaining cost guidance increased to $1,400/oz due to a much higher sustaining capital budget.

Newmont - Quarterly GEOs Produced - Company Filings, Author's Chart

{kind=link}

Costs & Margins

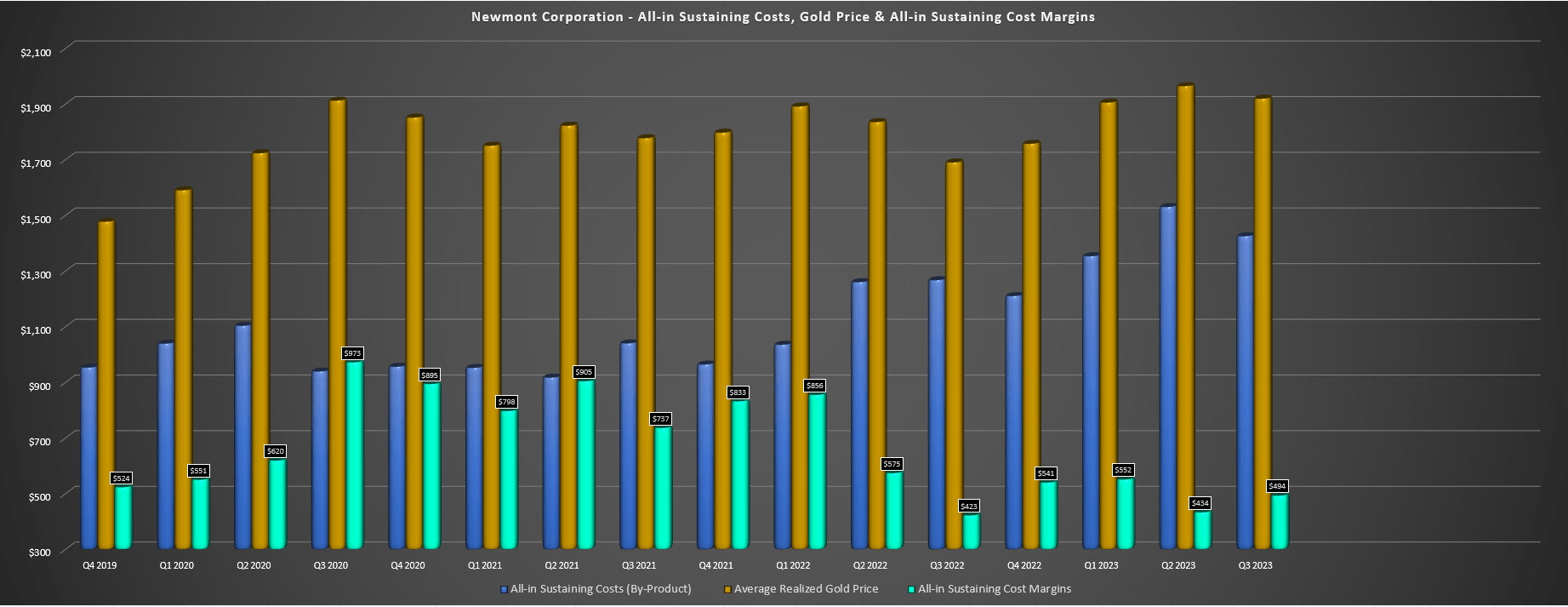

Moving over to costs and margins, it was another high cost quarter for Newmont, with all-in sustaining costs of $1,426/oz (+12% year-over-year), which can partially be explained by a weaker than planned quarter at Ahafo, no contribution from Penasquito which is one of its lower-cost mines (FY2022 costs of ~$1,000/oz), and higher sustaining capital spend in the period ($336 million vs. $258 million). Fortunately, these higher costs were offset by a stronger average realized gold price and Newmont was able to report a 17% increase in AISC margins to $494/oz. That said, the company was up against its easiest comparisons in years with this being the weakest quarter for margins since Q4 2019. Hence, while the margin was recovery was positive, it was less of a recovery than I had hoped and costs at Penasquito won't be any cheaper going forward with a further wage increase for union workers.

Newmont - Quarterly AISC & AISC Margins - Company Filings, Author's Chart

{kind=link}

If we dig into the bigger picture, costs are sitting at $1,425/oz year-to-date ($1,209/oz in same period of 2022), and Newmont is now guiding for ~$200/oz higher AISC than its previous outlook of ~$1,200/oz. However, while this might seem alarming, it's worth noting that this is due to an increase in its sustaining capital budget for 2023 to $1.4 billion (previously $1.0 billion to $1.2 billion), with five new autonomous haul tracks purchased at Boddington, camp upgrades at Musselwhite, and a replacement conveyor at Ahafo. This has been offset by lower than planned growth capital due to less spending on Yanacocha Sulfides and delayed timing of spending at Tanami due to the rainfall event, with full-year capex still expected to come in near ~$2.5 billion. So, while the full-year AISC might appear disappointing, I would expect a meaningful improvement in costs with this largely a function of higher sustaining capital, and one-time headwinds, and with the benefit of Newcrest's lower-cost assets that will contribute a full year of production in 2024.

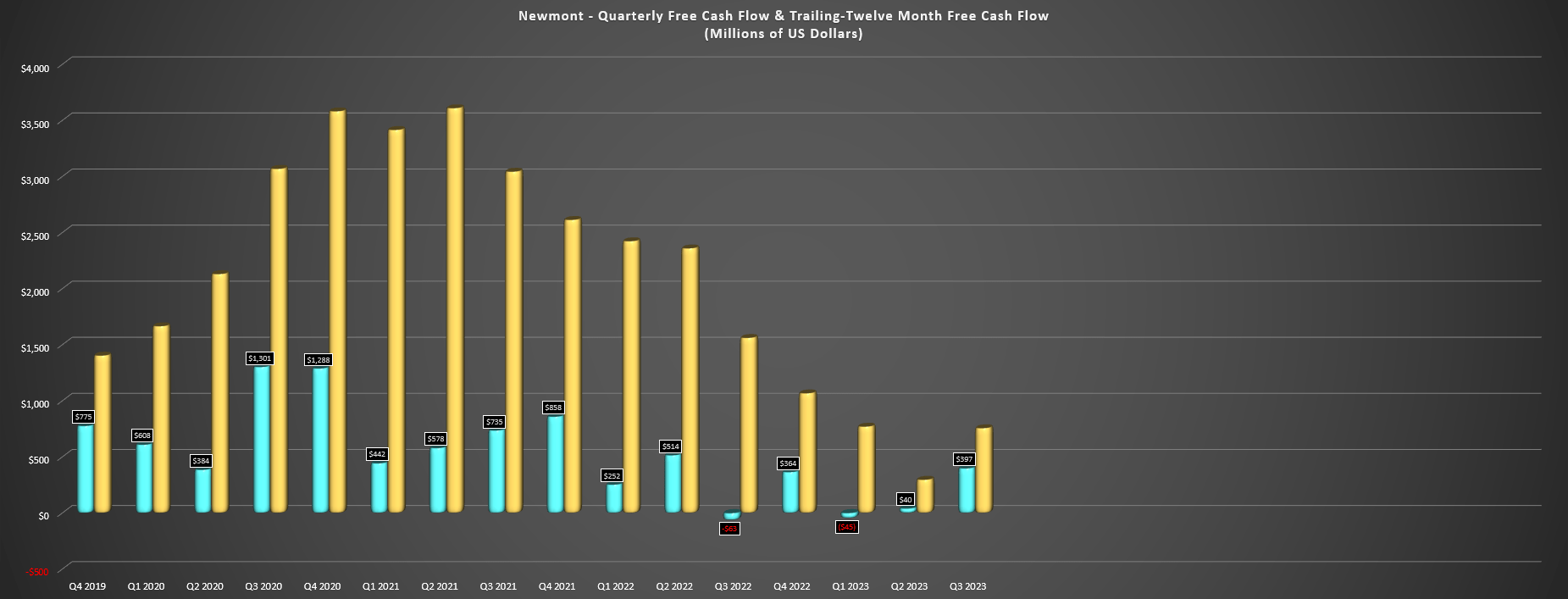

Newmont - Quarterly Free Cash Flow & Trailing Twelve Month Free Cash Flow - Company Filings, Author's Chart

{kind=link}

Finally, looking at Newmont's financial results, the company generated ~$1.01 billion in operating cash flow helped by favorable working capital changes and generated ~$397 million in free cash flow despite higher capital expenditures in the period (~$604 million). This was a meaningful improvement from limited free cash flow generation in H1 and a free cash outflow of $63 million in Q3 2022. That said, the quarter was mediocre overall in my view and while the company will look very different with the addition of lower-cost assets added to the portfolio once the Newcrest deal closes in early November, the meaningful wage increase to turn Penasquito back online is not ideal especially with headwinds from a stronger Mexican Peso, nor is the softer production over the next couple of quarters from Ahafo vs. my previous expectations, with this asset now likely to produce closer to ~700,000 ounces vs. what should have been a ~800,000 ounce year previously.

{kind=link}

Recent Developments & Updated Outlook

Although Newmont's year-to-date results have been disappointing, investors certainly have reason to be excited about the approval of the Newcrest merger by shareholders which will transform the company and add ~2.15 million ounces of attributable gold production per annum with the bulk of this coming from Tier-1 ranked jurisdictions and lower cost assets. In addition, Newmont will also add significant copper production (FY2024 production of ~130,000 tonnes based on Newcrest's guidance) assuming none of Newcrest's assets are divested. That said, Newmont did note that there will be re-sequencing of projects in the portfolio and that portfolio optimization proceeds from the divestment of assets will go to strengthening the balance sheet, suggesting that some portfolio optimization within the first 18 months post-closing looks likely.

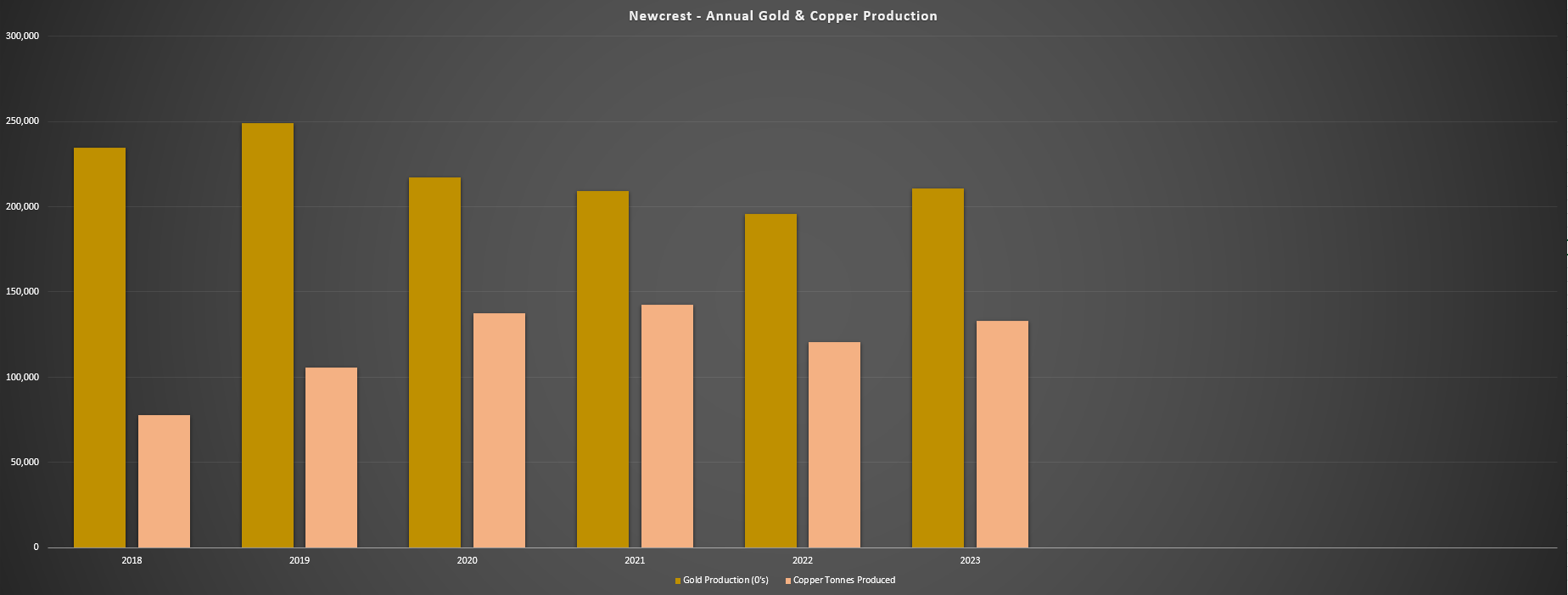

Newcrest Annual Gold & Copper Production - Company Filings, Author's Chart

{kind=link}

Overall, the amalgamation of Newmont and Newcrest will give Newmont a much larger leader on the #2 and #3 gold producers in the sector, with its total production set to be in line with its two closest peers production profiles combined at ~8.0 million ounces vs. ~7.8 million ounces. Meanwhile, Newmont will see improved diversification, enjoy a significant improvement in its margin profile with the addition of lower-cost assets like Cadia and Brucejack, and could ultimately see much lower all-in sustaining costs if it approves the Red Chris Block Cave which is expected to carry negative AISC. Finally, Newmont shared that it plans to put its Full Asset Potential program to work at Cadia and Lihir (similar to how it put its own mark on Penasquito and significantly improved the asset), suggesting that there could be better days for Lihir under Newmont if it can be optimized (currently a massive producer, but higher-cost). To summarize, while the year-to-date and Q3 results were nothing to write home about, patient investors should be rewarded here.

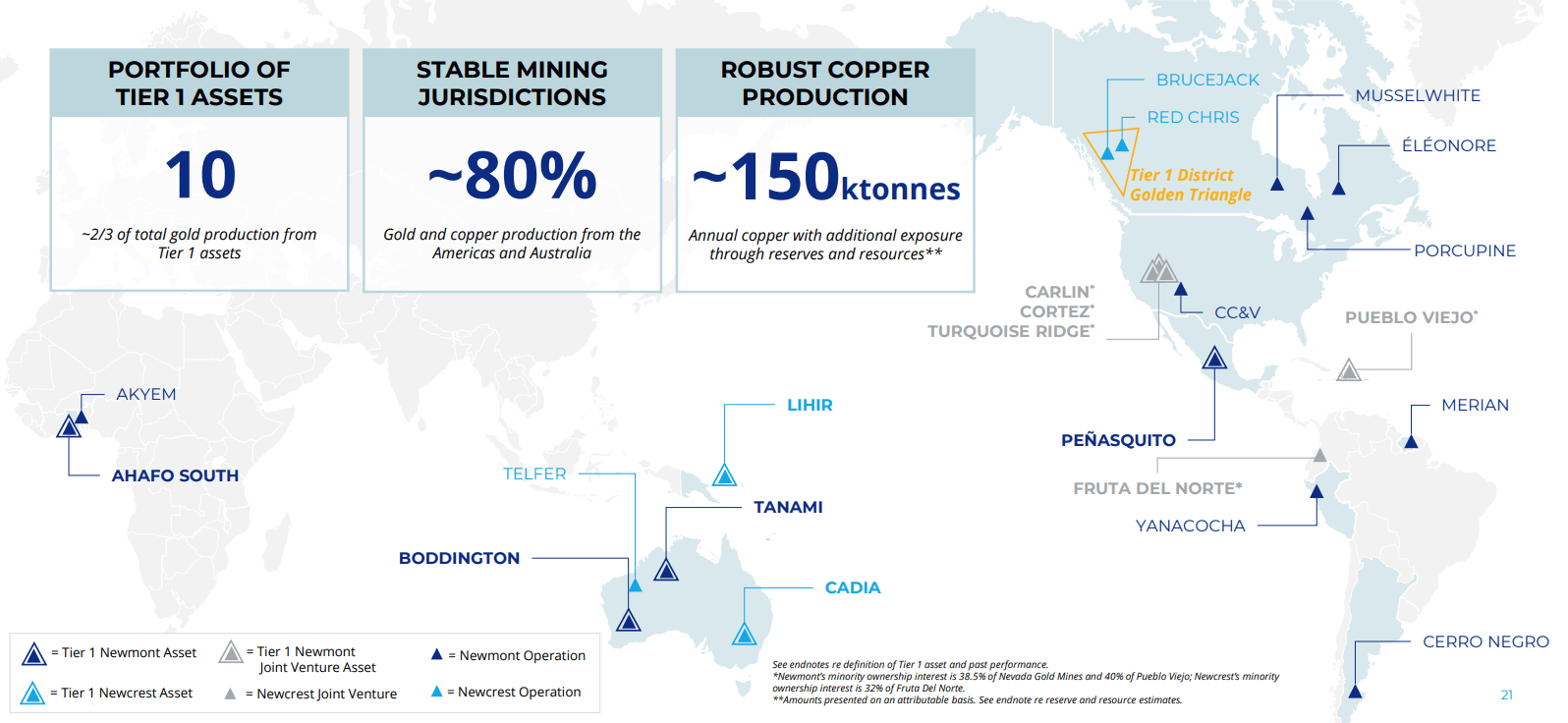

Newcrest/Newmont Portfolio Post-Closing - Company Presentation

{kind=link}

Finally, when it comes to capital allocation, Newmont shared that following potential portfolio optimization, it could look at buying back shares if its currency continues to be attractively valued and this would certainly help to claw back some of the expected dilution from the Newcrest deal. This is similar to what Newmont did following the Goldcorp deal and it was certainly received well by the market (~$500 million in share repurchases in 2019), with NEM outperforming the GDX massively following the deal and hitting a new multi-year high vs. the GDX from a relative strength standpoint. Plus, one could argue that the Goldcorp was more opportunistic vs. this deal being more strategic (higher-quality assets even if paying a higher price), so investors should be more comfy with the current deal and this contributing to a better portfolio overall vs. the Goldcorp deal where the best contributors were Penasquito, 40% of Pueblo Viejo and Cerro Negro, offset by some more marginal assets.

{kind=link}

Summary

Newmont had a softer Q3 year-over-year than I hoped even adjusting for the interruption to operations at Penasquito, but its financial results were helped by being up against easy year-over-year comps with a lower gold price in Q3 2022. And while Penasquito is back online, the wage increase isn't ideal when combined with a stronger Mexican Peso from a cost standpoint, though there certainly weren't many alternatives other than selling the asset and it at least drove a hard bargain to not cave to the initial demands. On a positive note, the company is just over a week away from closing its transformative Newcrest acquisition, and investors will get their first look at the new Newmont in the next quarterly report with seven weeks of operations from the combined portfolio expected in Q4. So, with Newmont 2.0 being much stronger and what I trust will be a much better portfolio post-2025 following portfolio optimization with much stronger free cash flow generation, I would view sharp pullbacks on NEM as buying opportunities.

For further details see:

Newmont: Margins Improve, But Production Below Plan