CA - Nexus Industrial REIT: The 6.5% Yield Should Be Safe As The AFFO Will Increase

2023-03-21 11:31:00 ET

Summary

- Nexus Industrial REIT is a Canadian REIT with a very strong focus on industrial properties.

- The company has grown through acquisitions, but I expect the pace to slow down as debt is becoming more expensive.

- Unlike so many other REITs, I expect Nexus to actually increase its AFFO per share in both 2023 and 2024 as some recently announced acquisitions still have to start contributing.

- I expect the payout ratio to drop to 85% based on my assumptions for 2024.

Introduction

I have always had a weak spot for industrial REITs and I liked Nexus Industrial REIT ( EFRTF ) ( NXR.UN:CA ), a Canadian REIT focusing on industrial properties. The last time I discussed this company was in October 2020 (paywalled article) where I argued the 10% yield back in the day was safe while the stock was trading at a 25%-35% discount to its NAV. Since that article, Nexus completed a 4:1 share consolidation which means the C$1.68 the stock was trading at in Q4 2020 is now the equivalent of C$6.72 on a post consolidation basis. The share price chart below shows the stock had a good run but recently lost much of its strength so I figured this is a good moment for an update to see if I should re-establish a position.

As its US listing is pretty illiquid with an average daily volume of just 1,000 shares per day, investors should turn to Nexus's Canadian listing where it's trading with NXR (or NXR.UN) on the Toronto Stock Exchange. The average volume in Canada exceeds the 150,000 shares per day, offering better liquidity. The current market capitalization is approximately C$840M (including the pro forma conversion of Class B units into common units), making it substantially larger than the sub-C$200M market cap it was valued at when I discussed the company in Q4 2020.

I will use the Canadian Dollar as base currency throughout this article.

Q4 looked promising as the new acquisitions are now contributing

While Q4 is not a perfect "look under the hood" as the company closed an additional C$175M acquisition during the last quarter, it does provide us with a better understanding of what we can expect in 2023. In December 2022, Nexus announced a C$173.3M acquisition of three properties which will partially be funded by issuing 2.5M Class B units (with a deemed value of approximately C$25M) while Nexus also issued 8.22 million new units at C$10.30 to raise about C$81M before costs. This means the vast majority of the new acquisition was funded through equity and that is a solid move given how the credit markets were evolving.

As mentioned, the timing of this acquisitions means we should take the Q4 results with a grain of salt as the closing date for the acquisition of these new assets is only occurring this year. This means Nexus is feeling the negative impact of the acquisitions (the capital raise and increased share count) before realizing the positive contribution (the assets will only start to contribute to the top and bottom line later this year).

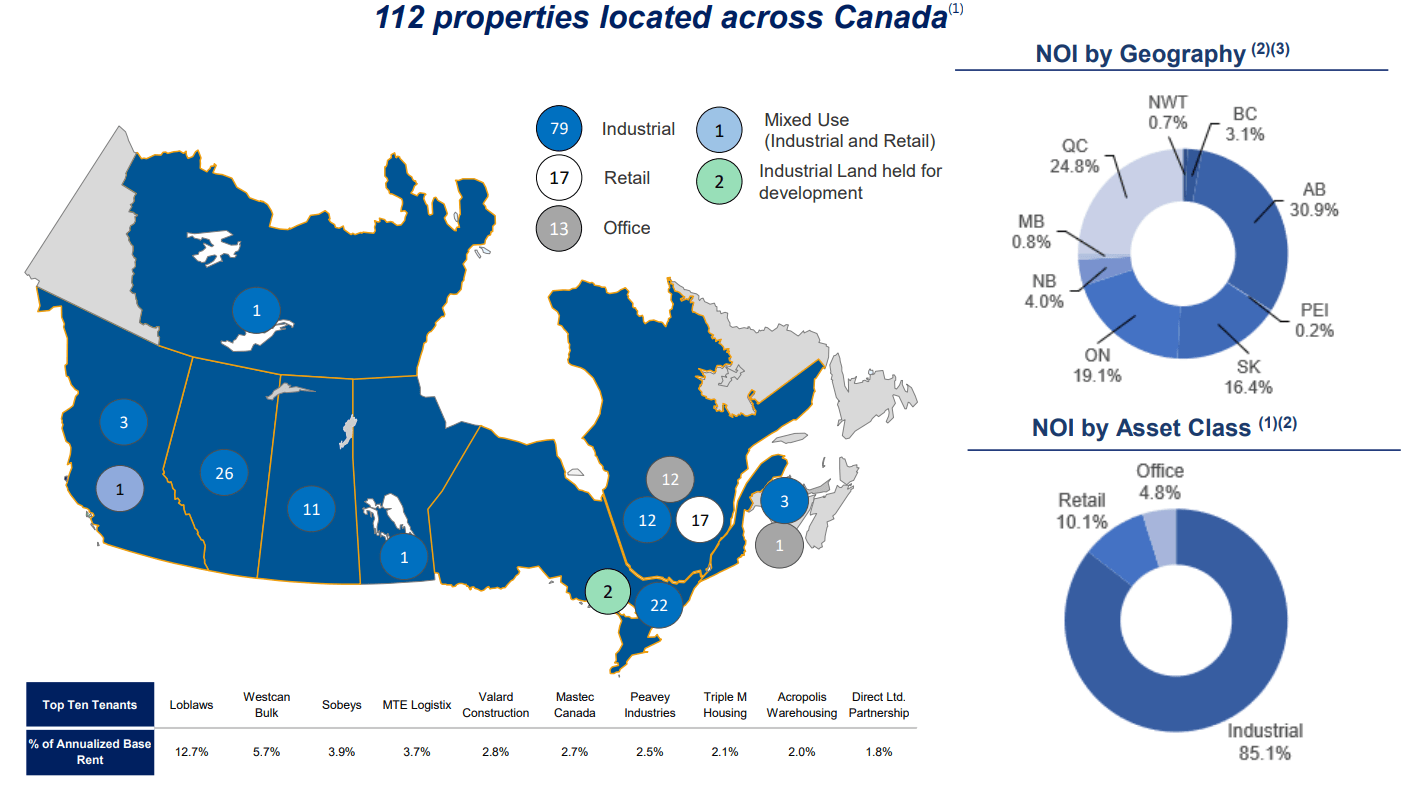

Nexus is now solely focusing on industrial properties with a relatively long lease term as about 85% of the NOI is now related to the industrial assets with just a few retail and office assets contributing to the Net Operating Income.

{kind=link}

The assets are all over Canada with Alberta as most important market as it contributes in excess of 30% of the total consolidated NOI.

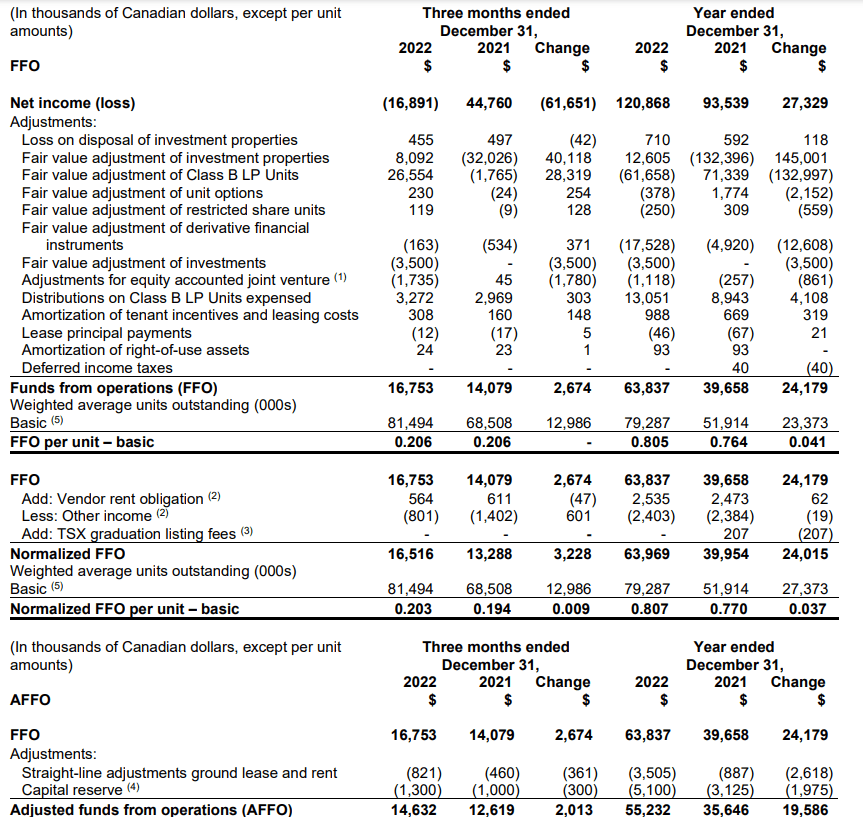

During the final quarter of 2022, Nexus reported a total FFO of C$16.75M resulting in an FFO of C$0.206 per share and approximately C$0.203 per share on a normalized basis. The AFFO calculation comes in at C$14.6M of C$0.18 per share.

{kind=link}

As you can see in the image above, these per-share calculations are based on the average share count of 81.5M shares. However, subsequent to the capital raise completed in December, the total share count increased to 87.6M shares which means the per-share FFO and AFFO results would have come in lower compared to the reported results.

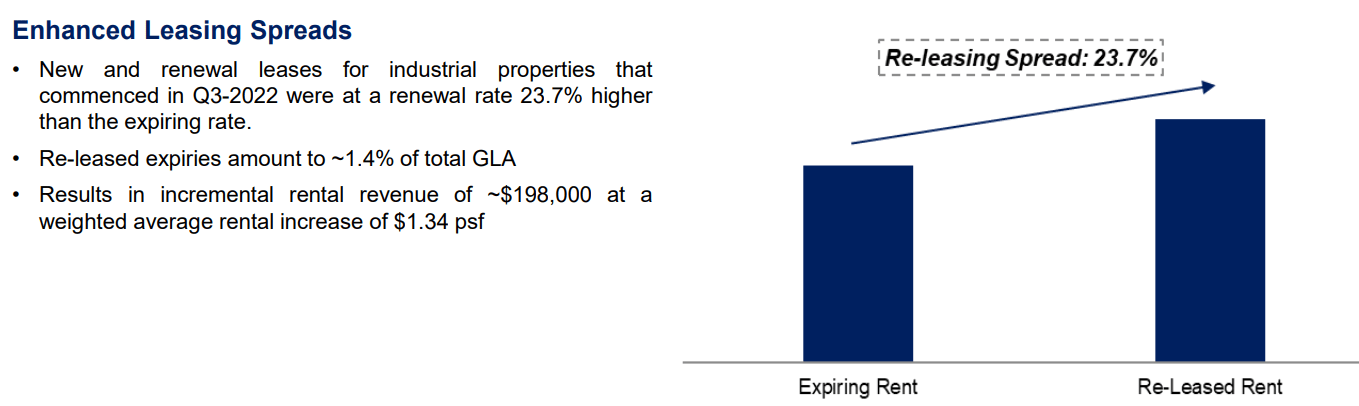

Of course it's not just black and white. During 2023, several of the already announced acquisitions will finally start to contribute while the REIT has a good chance at hiking some of the contractual rent on existing properties. And some of these lease spreads could be pretty impressive. Nexus mentioned it released an admittedly small asset at a 71% spread while a 31,375 square foot asset in Quebec enjoyed a leasing spread of 63%. Of course in some areas there may be some markdowns but with about 15% of the leases expiring in the next two years I think the potential for a strong uplift in rent is real.

{kind=link}

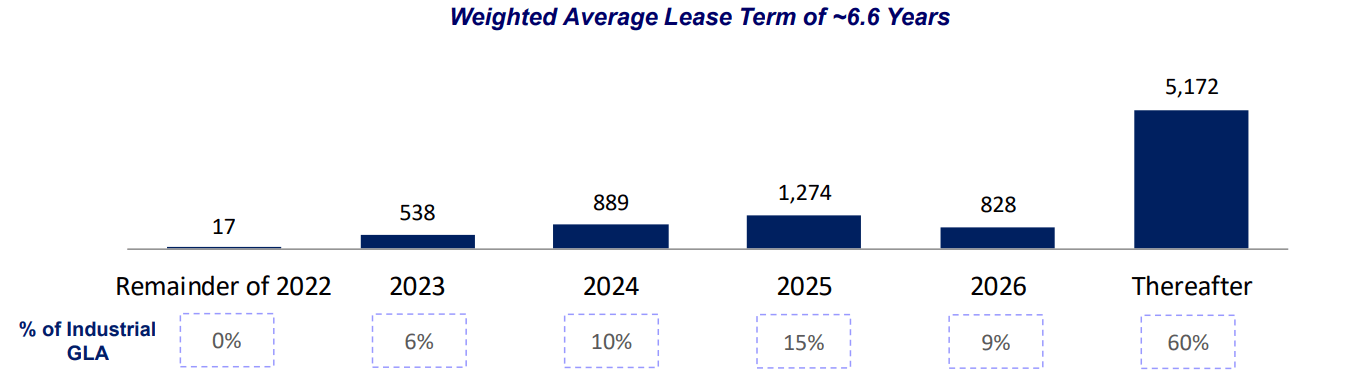

The WALT stands at 6.6 years as of the end of 2022.

{kind=link}

Nexus REIT is currently paying a monthly distribution of C$0.05333/unit which results in C$0.64 per unit per year for a dividend yield of in excess of 6.5%. This distribution rhythm should be reasonably well covered going forward and I expect a payout ratio of less than 90% for this calendar year, dropping to 85% in 2024. This would allow the REIT to 'hoard' about C$15M in cash in the 2023-2024 period.

A look at the balance sheet and the debt situation

So I think Nexus is looking good from a rental income and NOI perspective: Several new properties will start to contribute this year and this should more than offset the slightly higher share count versus the weighted average share count in the final quarter of last year.

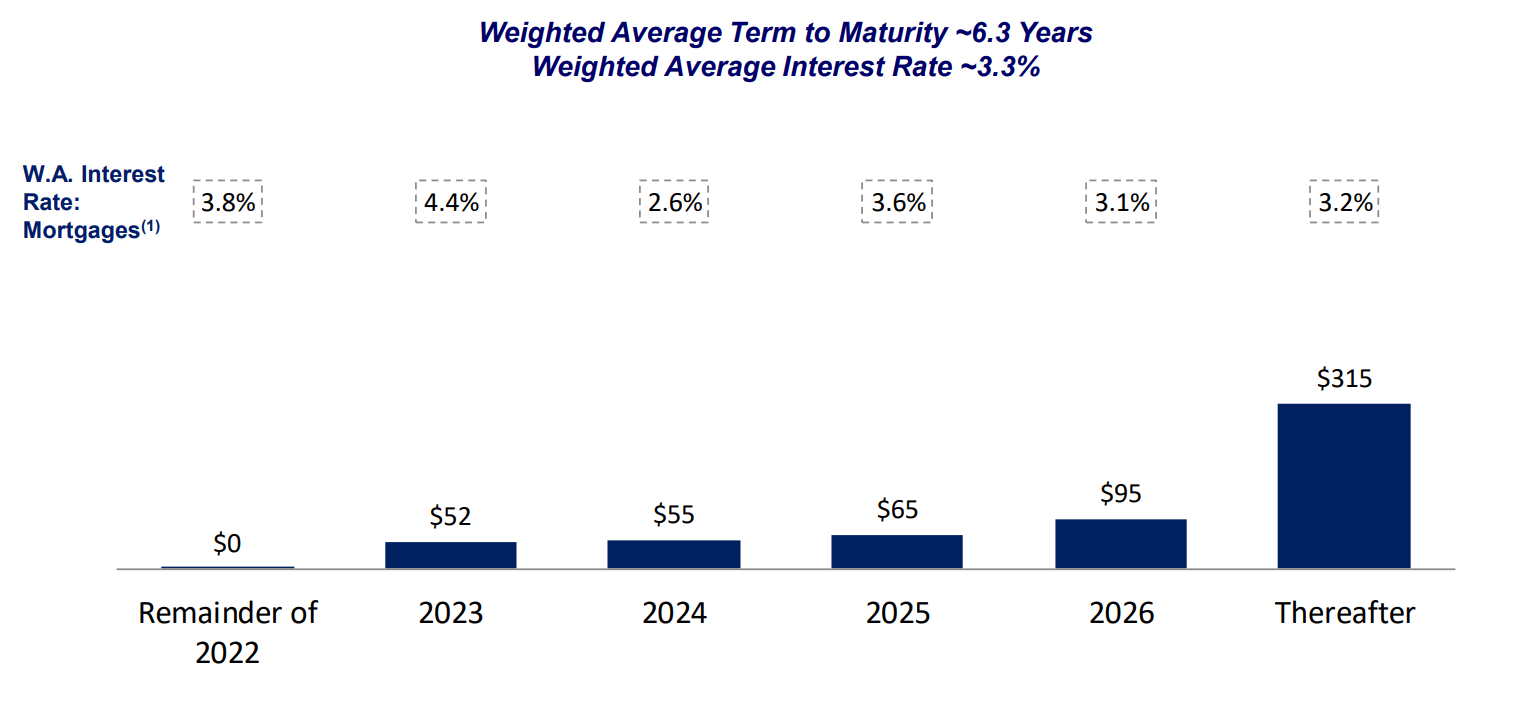

So the next question is whether or not Nexus may be caught in the vicious circle of increasing interest rates. I don't think so as the majority of Nexus' debt has fixed interest rates while it also hedged about 80% of the C$300M in floating rate debt. This means the interest expenses should remain pretty stable as less than C$100M of debt will be floating rate debt. This number will increase as Nexus acquired yet another property in March while securing a C$375M senior unsecured credit facility with a cost of debt of bankers' acceptance +170bp or prime +70bp.

{kind=link}

That being said, as mortgages mature, Nexus will have to refinance them at what very likely will be a higher rate. A total 200 bp increase in the cost of debt across the total indebtedness would increase by just C$16.3M (excluding the impact from the recent acquisitions). This would reduce the Q4 2022 annualized AFFO by just 28% (again, this excludes any rent hikes, releasing spreads and the impact from the recent acquisitions that will close later this year and excludes the net impact from the March acquisition). As I expect the NOI to increase by approximately C$15-20M by the end of 2024 (including the impact of the recent acquisitions), I think Nexus is in a good position to mitigate the impact of a higher average interest rate.

As of the end of 2022 the properties were valued at C$1.82B which means the net debt of approximately C$820M represented an LTV ratio of 45%. As of the end of 2022, the debt to total assets ratio was 43.7%. This of course this excludes all transactions that still have to be closed this year so you can expect the LTV ratio to fluctuate quite a bit this year depending on the closing of the acquisitions.

As of the end of 2022 the weighted average capitalization rate was 5.72% (using a stabilized NOI of C$102.5M). And a 0.25% increase in the capitalization rate would reduce the fair value of the assets by C$75M. An increase to a capitalization rate of 6.25% would thus knock off C$150M from the real estate value. But if the average NOI increases by 5% this year the negative impact would remain limited to just around C$100M.

Investment thesis

I don't expect Nexus to post a substantially higher AFFO per share this year, mainly due to the timing of the acquisitions announced in December 2022 which will only close in Q2 and Q3 of this year. There are four acquisitions "under firm contract" at an average capitalization rate of 5% based on the C$200M total price tag. This means we can expect an uplift in the rental income of C$10M as soon as the deals close and the tenants start to making their lease payments.

Nexus' NOI run rate is already C$3M per year higher than the performance in Q4 while we can expect additional rent hikes and lease spreads. I wouldn't be surprised to see the same-store NOI come in 6-7% above the Q4 2022 result which would already result in a NOI of C$107M excluding the net impact of the new acquisitions. And while it's not easy to guesstimate the AFFO performance due to the timing issue, I think a realistic target for the AFFO per share for this year would be C$0.72, increasing to C$0.75 in 2024 when the new properties are contributing for an entire financial year.

The official NAV/unit (including the impact of the capital raise) was C$12.19 as of the end of 2022. And even if I would apply a 6.25% capitalization rate, the NAV/share will likely still come in around C$11 which means the stock is currently trading at a discount of almost 15% to my more conservative NAV estimate.

For further details see:

Nexus Industrial REIT: The 6.5% Yield Should Be Safe As The AFFO Will Increase