NKLA - Nikola: Dismal 2023 Guidance And Going Concern Warning Spook Investors - Sell

Summary

- Zero-emission transportation start-up reported unimpressive fourth quarter results and provided 2023 guidance well below consensus expectations.

- Cash usage for this year likely to be well above $600 million.

- Elevated liquidity needs and limited funding availability required Nikola to warn investors of its ability to continue as a going concern in its annual report on Form 10-K.

- Nikola's pitiful shareholders appear to be caught between a rock and a hard place. Even if the company somehow manages to raise the capital required to make it into 2024, they will be saddled with outsized dilution.

- Given the obvious lose-lose situation, investors should consider selling existing positions and moving on.

Note: I have covered Nikola Corporation ( NKLA ) previously, so investors should view this as an update to my earlier articles on the company.

Shortly before the start of Thursday's regular session, zero-emission transportation start-up Nikola Corporation ("Nikola") reported unimpressive fourth quarter and full-year 2022 results.

On the subsequent conference call , management provided disappointing 2023 guidance with projected revenues of $140 million to $200 million missing the $300 million analyst consensus by a mile. In addition, gross margins are expected to remain deeply in the red with a projected range of negative 75% to negative 95%.

Company Presentation / Conference Call Transcript

Adjusted for $95 million in anticipated stock-based compensation, Nikola's projected cash usage for this year calculates to a range of $580 million to $705 million.

At the mid-point of the range, Nikola would use almost $650 million in cash in 2023, almost three times the amount of unrestricted cash left on the balance sheet at the end of December.

On the call, management was quick to point to its various sources of capital for this year:

Conference Call Transcript / Company Press Release

Please note that all funding sources available to the company appear to be outright equity sales or equity-linked debt instruments like the convertible notes issued in December.

In addition, access to the Tumim Stone equity line of credit ("ELOC") is currently limited as outlined in the company's annual report on Form 10-K:

(...) Although the Second Tumim Purchase Agreement provides that we may sell up to an aggregate of $300.0 million of our common stock to Tumim, only 29,042,827 shares of our common stock under the Second Tumim Purchase Agreement have been registered for resale by Tumim.

If it becomes necessary for us to issue and sell to Tumim under the Second Tumim Purchase Agreement more than the shares that were registered for resale under the respective registration statements in order to receive aggregate gross proceeds equal to the total commitment of aggregate of $300.0 million under the Second Tumim Purchase Agreement, we must file with the SEC one or more additional registration statements to register under the Securities Act the resale by Tumim of any such additional shares of our common stock we wish to sell from time to time under the Tumim Purchase Agreements, which the SEC must declare effective and we may need to obtain stockholder approval to issue shares of common stock in excess of the exchange cap under the Second Tumim Purchase Agreement in accordance with applicable Nasdaq rules.

Over the past year, Nikola managed to raise more than $600 million in cash from financing activities, thus causing outstanding shares to increase by almost 25% to 512.9 million:

Annual Report on Form 10-K

That said, with NKLA stock down by more than 70% over the past twelve months, dilution in 2023 is likely to be much higher.

Even when generously assuming the share price to hold up at current levels, fully utilizing both the Citigroup ATM agreement and Tumim Stone ELOC would result in the issuance of almost 250 million new shares thus increasing outstanding common shares by close to 50%.

Subsequent to quarter end, the company continued to dilute common shareholders by issuing an aggregate 21.8 million shares under the ATM agreement (3.9 million) and Tumim Stone ELOC (17.9 million) for gross proceeds of $53.2 million.

Given the toxic combination of elevated liquidity needs and limited funding availability, Nikola was required to warn investors of its ability to continue as a going concern in its annual report on Form 10-K (emphasis added by author):

(...) The Company has secured and intends to employ various strategies to obtain the required funding for future operations such as continuing to access capital through the equity distribution agreement with Citi Global Markets, Inc., as sales agent, (...), the second common stock purchase agreement with Tumim Stone Capital LLC (...), and the securities purchase agreement with investors for the sale of an additional principal amount of unsecured senior convertible notes (...).

However, the ability to access the equity distribution agreement and second common stock purchase agreement are dependent on the Company’s common stock trading volumes and the market price of the Company’s common stock , which cannot be assured, and as a result cannot be included as sources of liquidity for the Company’s ASC 205-40 analysis.

(...) The result of the Company’s ASC 205-40 analysis, due to uncertainties discussed above, is that there is substantial doubt about the Company’s ability to continue as a going concern through the next twelve months from the date of issuance of these consolidated financial statements .

With the company's Nikola Tre BEV truck offering performing well below expectations, the company is now focusing on the launch of its FCEV truck in the second half of the year with a target to deliver up to 150 FCEV units in Q4 with sales expected to scale to up to 6,000 units in 2026.

On the margin front, Nikola is planning to achieve positive gross margins in 2024 while reaching breakeven EBITDA in the following year.

Suffice it to say, these are aggressive forecasts, particularly when considering the disappointing sales performance of the company's Nikola Tre BEV truck and the ongoing lack of hydrogen infrastructure.

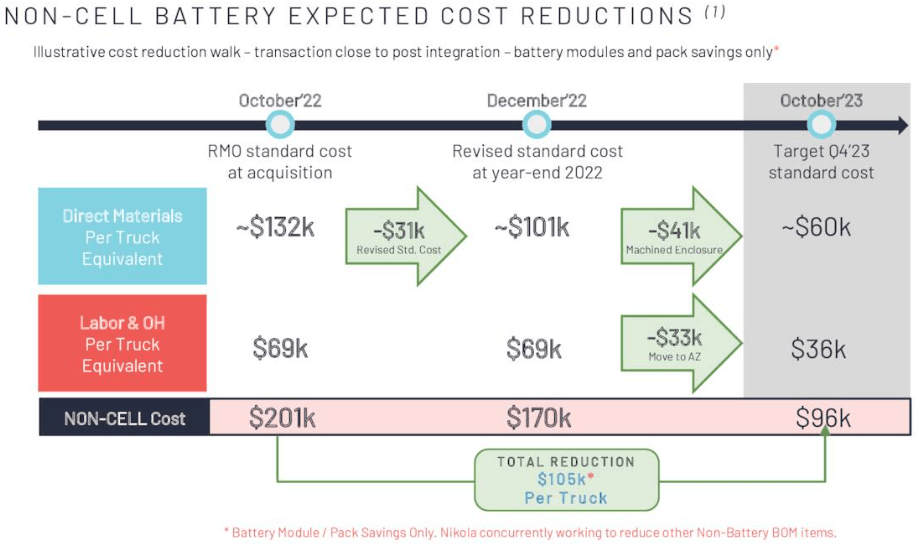

As already discussed by me three months ago, the recent acquisition of ailing battery supplier Romeo Power has resulted in a massive drag on BEV truck margins which the company expects to have largely reversed by the end of the year:

{kind=link}

Adding insult to injury, Romeo Power customer Lion Electric (LEV) recently initiated arbitration proceedings after not receiving contracted battery pack volumes subsequent to the close of the acquisition by Nikola.

Even worse, customer Lightning eMotors (ZEV) also claimed to have lost substantial sales volumes due to Romeo Power not honoring its contractual commitments:

Lightning lost significant sales volume during the fourth quarter because Romeo Power Systems, Inc. (a subsidiary of Nikola Corporation) unexpectedly notified Lightning that it would not honor its commitments to supply battery packs, or to provide further service or support, under its long-term supply agreement with Lightning.

On the conference call, management tried to water down the issue but considering the fact that the contract with Lion Electric was supposed to generate $234 million in revenue over a five-year period, Nikola might very well be facing a substantial impact from an unfavorable arbitration outcome.

Bottom Line:

Nikola's pitiful shareholders appear to be caught between a rock and a hard place. Even if the company somehow manages to raise the capital required to make it into 2024, they will be saddled with outsized dilution.

At some point, Nikola won't be able to cover its capital needs from additional equity sales anymore and with very limited funding alternatives, at least in my opinion, bankruptcy appears to be the most likely scenario for the ailing company.

Given the obvious lose-lose situation, investors should consider selling existing positions and moving on.

For further details see:

Nikola: Dismal 2023 Guidance And Going Concern Warning Spook Investors - Sell