UNP - Norfolk Southern: All Aboard This Buy-And-Hold Freight Train

2023-11-23 00:46:27 ET

Summary

- Norfolk Southern is a Class I railroad operator in the U.S. with a wide range of revenue streams in the transport of intermodal freight and other cargo.

- The company has a wide economic moat due to its large rail network and established market position in the Eastern United States.

- Norfolk Southern has historically shown strong financial performance along with a newfound desire for operational excellence.

- Recent short-term headwinds have led to a souring in investor sentiment and a potential 14% undervaluation in shares.

- Strong Buy rating issued.

Investment Thesis

Norfolk Southern ( NSC ) is one of the largest Class I railroads in North America. The firm has an excellent history of earning outsized returns on their invested capital with the last decade being characterized by solid growth and great asset management.

This high-quality railroad has had a difficult FY23 so far with falling revenues compounded by a derailment in East Palestine, Ohio souring investor sentiment in the firm.

However, Norfolk Southern remains a fundamentally profitable railroad that is managed excellently. When combined with the potential for a 14% undervaluation in shares to be present, I believe now may be a great opportunity to enter into a position in the railroad.

I have built a 16% stake in Norfolk Southern relative to my total real portfolio value as of present.

Strong Buy rating issued.

Company Background

Norfolk Southern is one of seven Class I railroad operators in the U.S. with their key business operations revolving around the transport of freight and cargo.

Norfolk has a wide set of different revenue streams within their core railroad business with the firm hauling both intermodals, automobiles, coal, chemicals, forestry products and even agricultural produce.

The firm has had a successful past with Norfolk Southern emerging as the one of the very few key players within the industry with Warren Buffett’s BNSF Railway, Union Pacific ( UNP ) and CSX ( CSX ) being the firm’s key competitors.

While Norfolk has historically tended to slightly lag peers such as Union Pacific on both returns and margins, the firm has committed in recent years to significant cost control through technology driven railroad solutions and smartly timed infrastructural improvements.

I believe the firm’s overarching business strategy to modernize their rail operations should prove beneficial in the long run placing Norfolk in a prime position to expand margins moving forwards.

Alan Shaw is Norfolk’s current President and CEO having taken over the helm of the metaphorical train from predecessor James Squires . Alan Shaw came as a natural succession choice thanks to his extensive experience at Norfolk Southern both as Vice President and through his role as Chief Marketing Officer.

While the merits of his strategic overhaul at Norfolk will require time to be properly evaluated, Shaw has also had to deal with the significant derailment accident in East Palestine, Ohio.

Nonetheless, I do believe his conscientious attitude and belief that the future for Norfolk entails becoming an even higher-quality organization suggests he is acutely in tune with what the railroad needs to succeed.

Economic Moat -In Depth Analysis

Norfolk Southern enjoys a wide and hugely robust economic moat that is fundamentally underpinned by massive barriers to entry along with a tangible set of economies of scale advantages.

Fundamentally, the construction and operation of class I railroads is an incredibly capital intensive and complex business. The established industry players such as Norfolk, BNSF and Union Pacific all enjoy massive economies of scale thanks to the thousands of miles of railroads already present within their networks.

{kind=link}

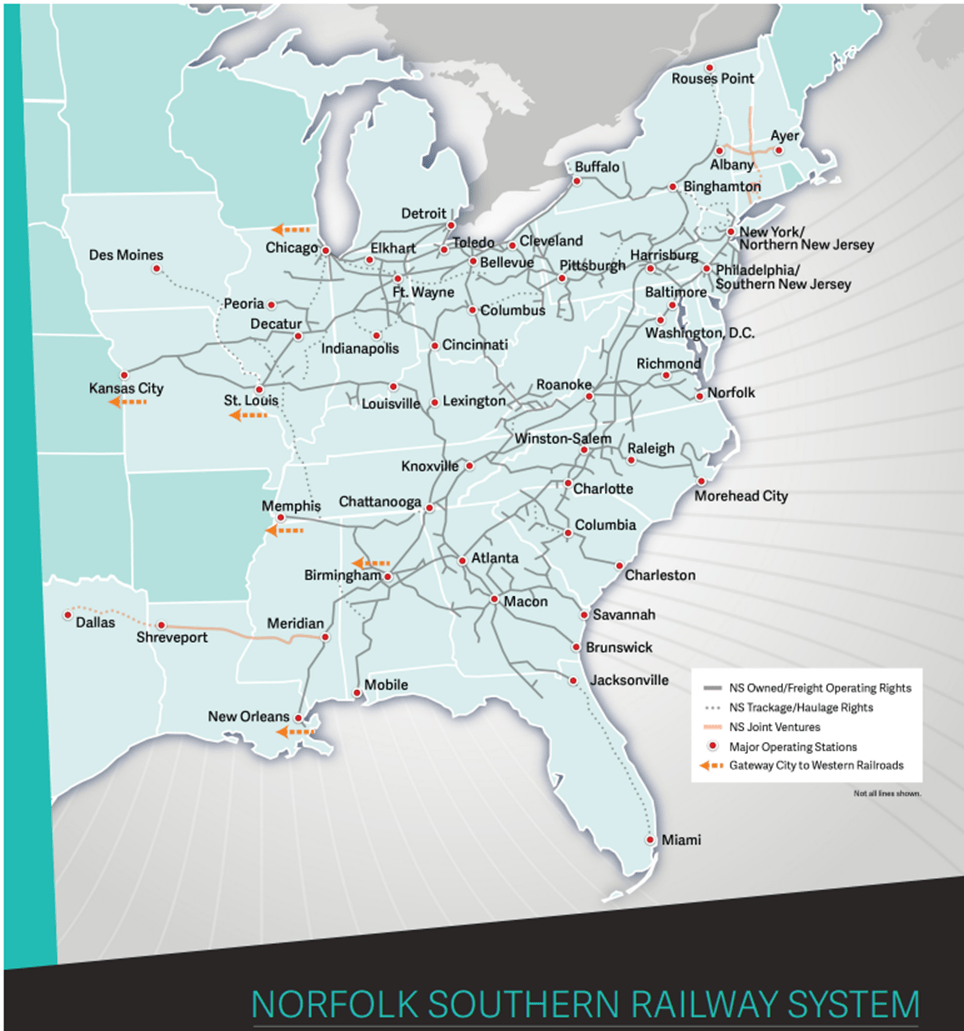

Norfolk alone operates around 20,000 route miles of track that service 22 states, the District of Columbia, every major container port in the easter U.S. and a majority of U.S. population and manufacturing bases.

The firm has also established multiple joint venture routes with competitors along with owning significant amounts of trackage/haulage rights that enable the firm to exploit pre-existing track owned by one of their competitors.

Quite simply, Norfolk has become an underpinning component of the United States economy without which the entire Eastern half of the nation would essentially grind to a halt.

Norfolk Southern FY23 Q1 Report

The massive amount of chemicals, forestry products, agricultural produce, automobiles, intermodal traffic and coal transported by Norfolk could simply not be covered by any other company alone.

Norfolk generates around 30% of their revenues from intermodal transport with the "merchandise" category consisting of agricultural, forestry and consumer products, chemicals, metals and automotive goods. Merchandise is responsible for around 50% of the firm's revenues.

The railroad also transports a large amount of coal which generates around 14% of total revenues.

Given the mature nature of the railroad industry combined with the massive barriers to entry created by the capital costs required to establish a class-I railroad, Norfolk Southern enjoys a tangible economic moat simply from the presence of their pre-existing railroad infrastructure and assets.

Furthermore, the firm’s specialization as a key eastern United States railroad has allowed the firm to develop a very strong foothold in the market with the variety and scale of produce transported by the company supporting this hypothesis.

This leading position within the market has allowed Norfolk to generate outsized returns on their invested capital for multiple years despite being smaller in size than some of their competitors such as BNSF and Union Pacific. While the firm has lagged these two competitors both in terms of returns on invested capital and margins, Norfolk Southern is still a very financially healthy operation.

Considering the massive barriers to entry into the railroad business and Norfolk’s excellent positioning within the market, I believe the firm clearly enjoys a wide and robust economic moat that will continue to allow Norfolk to generate outsized returns on their invested capital for at least the next 35 years.

While traditionally believe wide economic moats provide firms with competitive advantages ranging from 15 to 25 years, I confidently can add an extra 10 years in the case of Norfolk Southern. This primarily stems from the absolute inability for a new entrant into the market to build a comprehensive and competitive network similar to that of Norfolk in anything under 35 years.

Financial Situation

From an operating performance perspective, Norfolk Southern is a very healthy and financially successful enterprise.

The firm has 5Y average (as measured from FY22-FY18) gross, operating and net margins of 39.71%, 38.70% and 23.51% respectively. The relatively high gross margin in particular illustrates that Norfolk’s fundamental business model is working for the firm.

While these margin metrics lag rival Union Pacific by around 5pp each, the larger scale of Union Pacific and a recent history of excellent execution by Norfolk’s competitor are the main reasons for this disparity.

Norfolk also has 5Y (FY22-FY18) average ROA, ROE and ROIC of 7.03%, 18.58% and 11.53% respectively. The firm’s relatively healthy ROIC is dragged down by a difficult FY20 which not with counting sees the firm have a 4Y average ROIC of around 13.54%.

Once again, Union Pacific leads Norfolk in these key fiscal return metrics by around 3pp each.

Nonetheless, these very healthy operational performance metrics from Norfolk illustrate that the firm is a fundamentally profitable and successful enterprise. While the firm is being narrowly outperformed by their larger competitors such as Union Pacific, I believe there is much more to be analyzed with regards to Norfolk’s business strategy.

For the last two decades, Norfolk has been a much more conservatively managed operating compared to Union Pacific with management electing to grow at a slightly slower pace instead focusing on increasing the robustness of the firm’s balance sheets and the quality of their core enterprise.

I believe this much more long-term focused management style which revolves around making Norfolk the highest quality business possible has set the company up for significant future growth which will outpace that of its more liberal competitors.

Considering Norfolk’s FY23 so far, a slightly mixed bag of results has been earned by the railroad.

{kind=link}

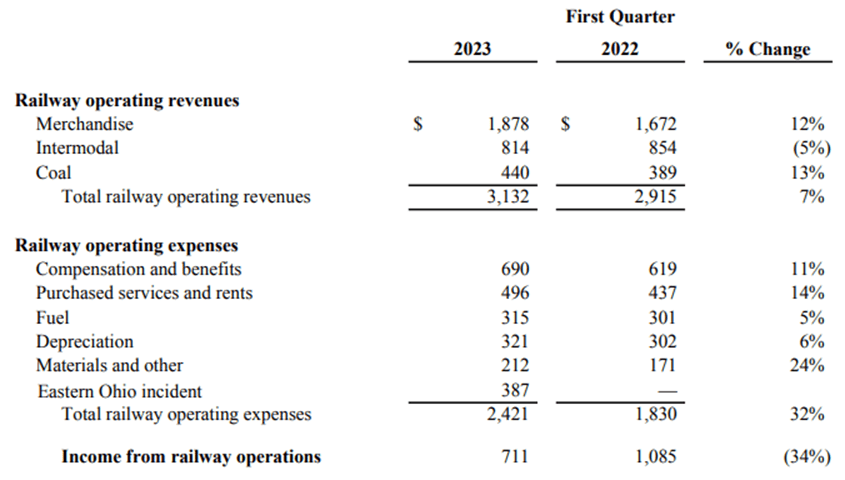

FY23 Q1 saw Norfolk grow their revenues YoY by 7% thanks to strong merchandise and coal operating revenues along with a smaller than expected decrease in intermodal demand.

While this overall growth in operating revenues was great to see and aligned mostly with the relatively robust demand across the U.S. both by consumers and business as witnessed in H1 of FY23, unfortunately did not translate to increased operating income.

Falling incomes due to a significant increase in essentially all of the firm’s operating expenses along with the significant impacts of the February 3 East Palestine derailment of one of Norfolk’s 150-car trains led to a massive 32% drop in income for the railroad.

Without the massive $387M impacts of the East Palestine derailment, income from railway operations still would have actually been essentially flatline YoY with increased revenues offsetting the relatively smaller increase in operating expenses.

Norfolk also utilized Q1 to repurchase and retire 0.6M and 2.2M shares of common stock respectively. Norfolk’s share repurchases are a large reason for the massive shareholder returns generated by the firm in recent years and once again illustrates the firm’s utmost desire to present a high-quality business to investors.

While the East Palestine derailment led to significant expenses in Q1, investors were largely able to overlook these troubles given the firm’s solid revenue growth. However, Q2 saw Norfolk struggle not only due to the costs associated with the derailment.

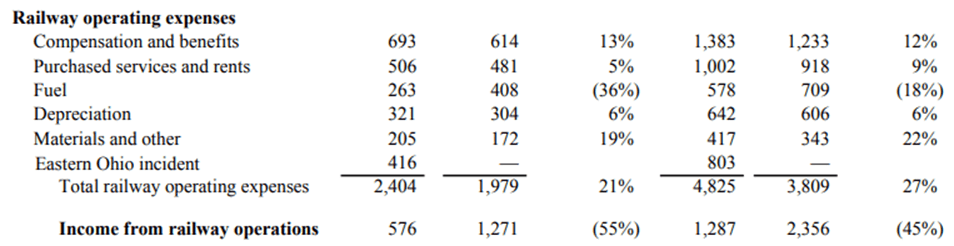

A drop in total operating revenues of 8% in Q2 to just $3.00B down from $3.25B in Q2 FY22 saw Norfolk suffer from decreasing industrial and business demand across the U.S. due to the higher interest rate environment and the effects inflation have had on end consumer demand.

{kind=link}

Railway operating expenses also continued to surge in Q2 which led to overall railway income dropping a whopping 55% YoY. The first two quarters saw Norfolk’s H1 income drop 45% to just $1.06B down roughly $1.0B YoY.

While Norfolk’s H1 of FY23 was disappointing, I believe the weak revenue growth and overall rise in operating expenses can mostly be considered out of Norfolk’s control. Fundamentally, Norfolk is continuing to operate their business through what are now significantly more dire macroeconomic conditions that are unfavorable to economic growth.

When combined with the costs associated with the East Palestine derailment, Norfolk has been hit with multiple challenges that the firm has had to deal with simultaneously.

{kind=link}

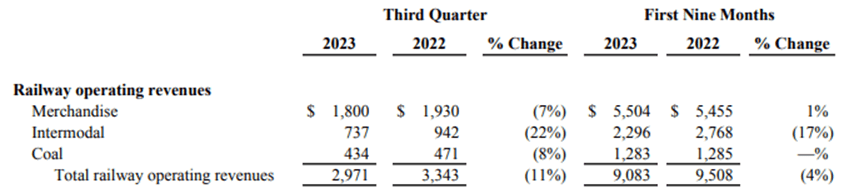

Still, Q3 has seen little improvement for Norfolk with regards to their overall revenues with quarterly figures dropping 11% YoY to $2.97B.

While Norfolk’s trend of decreased YoY revenues is regrettable, the difficult macroeconomic conditions facing the firm are still largely to blame. As the railroads are an unavoidable part of the greater macroeconomic scene, their returns will always at least somewhat be tied to the overall performance of the U.S. economy as a whole.

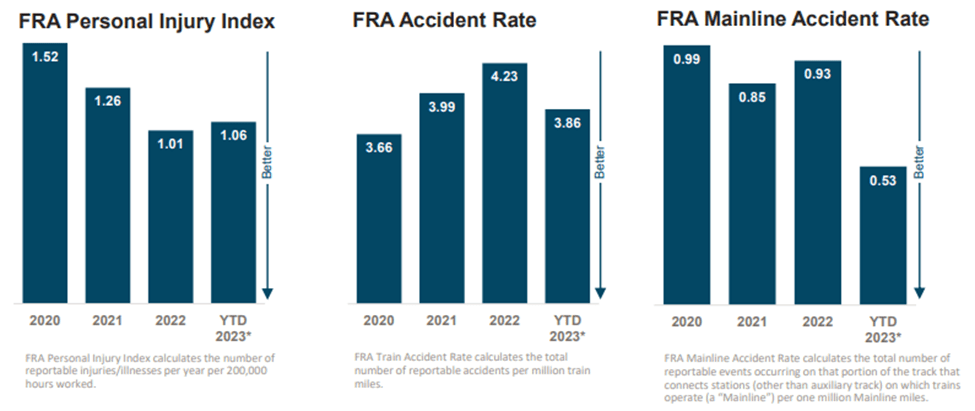

Furthermore, Q3 has seen Norfolk manage their costs well with decreases of 3% and 25% being achieved in compensation costs and fuel expenses respectively. Furthermore, the firm has managed to significantly increase the efficiency of their operations both from a service perspective and with regards to safety.

{kind=link}

Norfolk has reversed FRA accident rate figures with their YTD 2023 rate of 3.86x illustrating positive trends for the firm. The significant overall drop-in mainline accident rates and the continuously low personal injury index rates illustrate that Norfolk is committed to increasing the safety of their operations.

This strategy once again aligns with Shaw’s desire to increase the overall efficiency and quality of the business present at Norfolk.

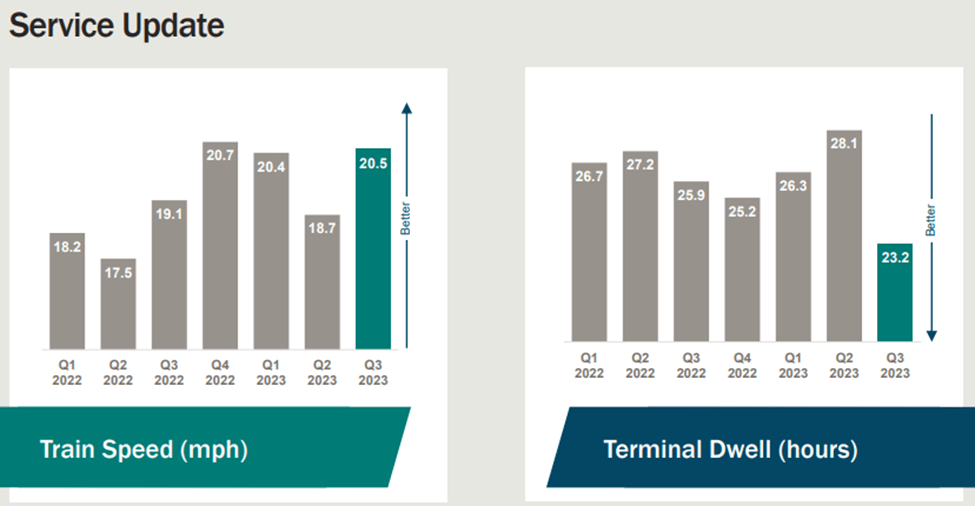

{kind=link}

From a service perspective, Norfolk has managed to significant increase the average speed of their trains to 20.5mph. This increase has been largely attributed to the shift towards a more reliable scheduling strategy moving away from the precision scheduled railroading utilized by Norfolk particularly during the COVID-19 pandemic.

Terminal dwell has also fallen sharply to just 23.2 hours which is great to see.

Fundamentally, Q3 for Norfolk has been slightly disappointing from a purely quantitative fiscal perspective. However, it is clear that Norfolk is set on achieving operational excellence with positive productivity and safety trends supporting this thesis.

I believe that all Norfolk needs is time for these operational improvements to bear fruit for the firm. In the long-term, a focus on high-quality enterprise should logically provide great opportunities for the firm to achieve sustained and robust volume growth.

{kind=link}

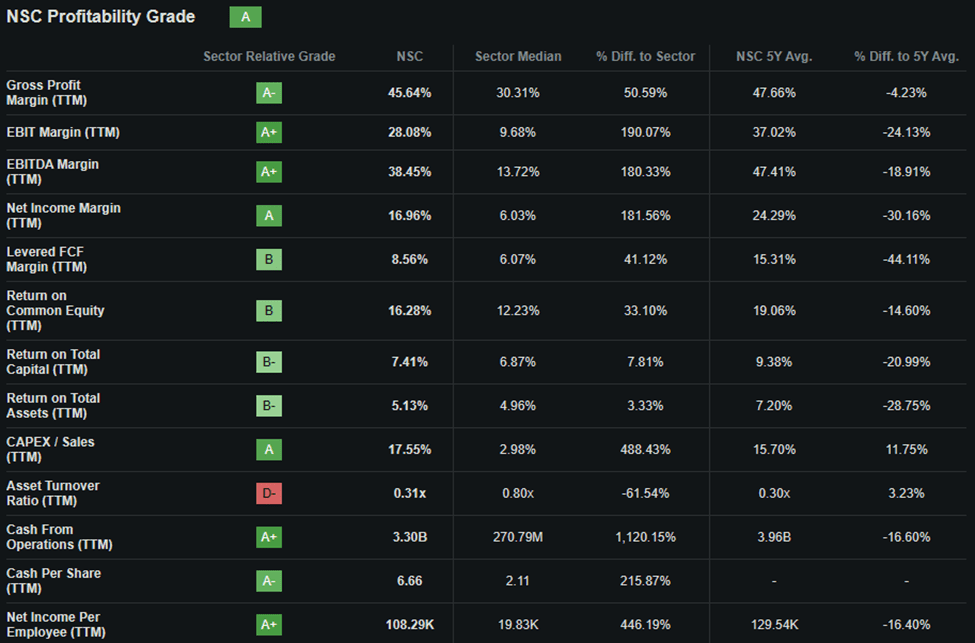

Seeking Alpha’s Quant calculates an “ A ” profitability rating for Norfolk Southern which I believe to be a pretty accurate relative evaluation of the firm’s current fiscal abilities.

When considering Norfolk’s balance sheets, it is clear that the firm is incredibly well run with conservative asset allocation at the forefront of management's fiscal objectives.

The firm has $3.14B in total current assets while total current liabilities amount to just $2.91B. This solid short-term liquidity leaves the firm with quick ratio of 0.93x and a current ratio of 1.08x. These liquidity metrics are particularly impressive when compared to Union Pacific’s quick and current ratios of just 0.51z and 0.72x respectively.

Total assets for Norfolk amount to $40.8B with total liabilities just $28.1B. The firm has $12.6B in total shareholders’ equity. This leaves the firm with an excellent debt/equity ratio of 1.31x compared to Union Pacific’s D/E ratio of 2.46x.

{kind=link}

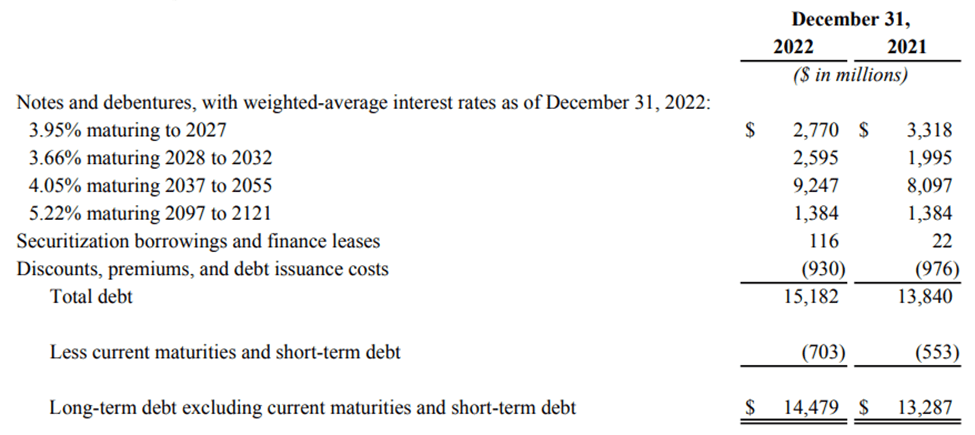

At the end of FY22, Norfolk Southern had $14.5B in long-term debt. While this is a relatively large sum of debt relative to their total assets, the firm has consistently been paying off maturities as they have arisen which has proven easy fiscally given their robust FY22 unlevered FCF of $1.49B.

Furthermore, their staggered debt profile consisting of mostly fixed-rate debentures illustrates management's conscientious approach to growth. Norfolk will be quite well protected against the higher for longer interest rate environment while their cashflows should allow the firm to easily service the debt maturing to 2027.

Moody’s credit ratings agency affirmed a Baa1 LT issuer credit rating for Norfolk with their unsecured domestic notes also affirmed at a Baa1 rating. The outlook remains stable. Moody’s classifies “Baa1” credit ratings as being of “medium investment grade”.

Considering Norfolk Southern as a whole it is clear that the firm is fundamentally profitable and that the management team has pursued the development of a high-quality railroad instead of huge debt-fueled growth.

Their very healthy balance sheets, smart capital allocation strategies and relatively solid credit scores illustrate that Norfolk Southern as a business has been engineered to remain robust despite even the toughest economic conditions.

{kind=link}

Norfolk Southern pays a relatively impressive dividend . The firm has continued growing their dividend for 7 years with a dividend yield FWD of 2.55% and an annual payout FWD of $5.40.

Furthermore, the 12.18% 5Y growth rate is outstanding while the 42.87% payout ratio is also truly remarkable to see. While an acute economic downturn would almost certainly lead to Norfolk Southern pausing or decreasing their dividend, I believe management’s fundamental desire to reward shareholders is excellent to see.

I eagerly await the Q4 earnings report which will significantly expand the ability for investors to understand how well Norfolk Southern has managed to navigate a tough FY23 along with some more guidance for the coming year.

Valuation

{kind=link}

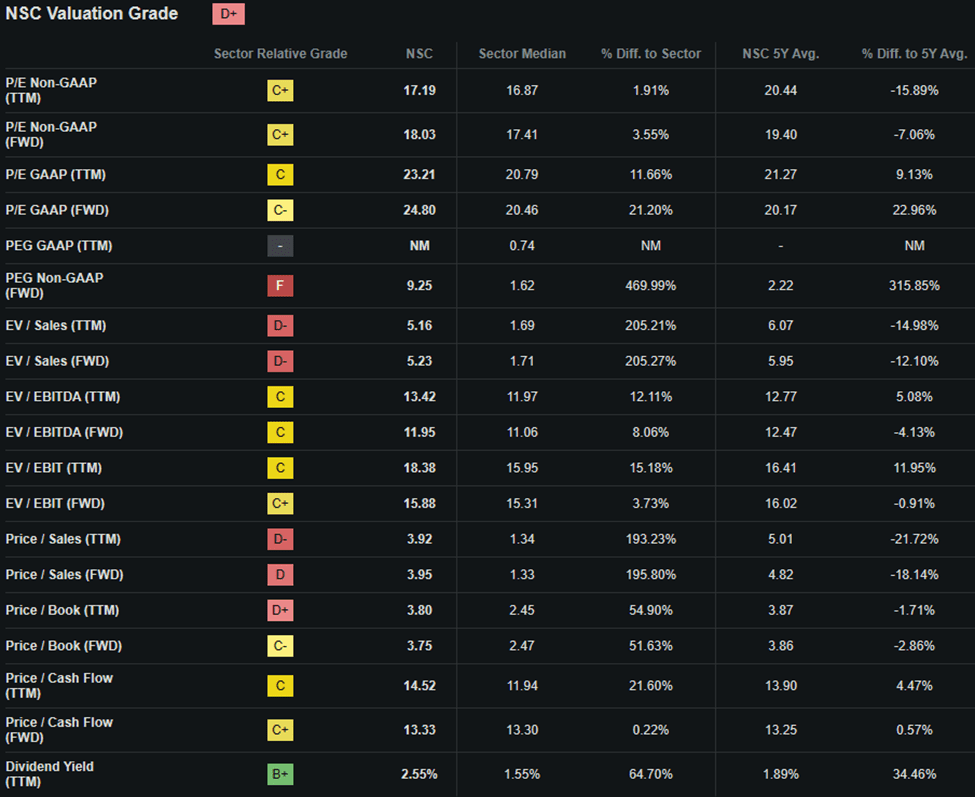

Seeking Alpha’s Quant assigns Norfolk Southern with a “ D+ ” Valuation grade. I believe this is an excessively pessimistic representation of the value present within the railroad’s stock and illustrates how very accurate relative quant ratings can sometimes poorly represent the absolute value present in a company’s shares.

The firm currently trades at a P/E GAAP FWD ratio of 24.80x. This represents a 22.96% increase in the firm’s P/E ratio compared to their running 5Y average. However, given the falling earnings and relatively more stable share price, this P/E compression is unsurprising to see.

Norfolk’s P/CF FWD of just 13.33x is positive while their FWD EV/EBITDA of just 11.96x is representative in my opinion. The firm’s Price/Sales FWD of 3.96 is excellent and actually illustrates an 18.14% decrease in relation to Norfolk’s 5Y average despite the D letter grade.

Considering these basic valuation metrics alone I believe Norfolk should already start to appear slightly undervalued given the stock’s historic averages. While the letter grade assigned by the quant is less optimistic, we must remember that this grading system is relative to Norfolk’s industry peers.

{kind=link}

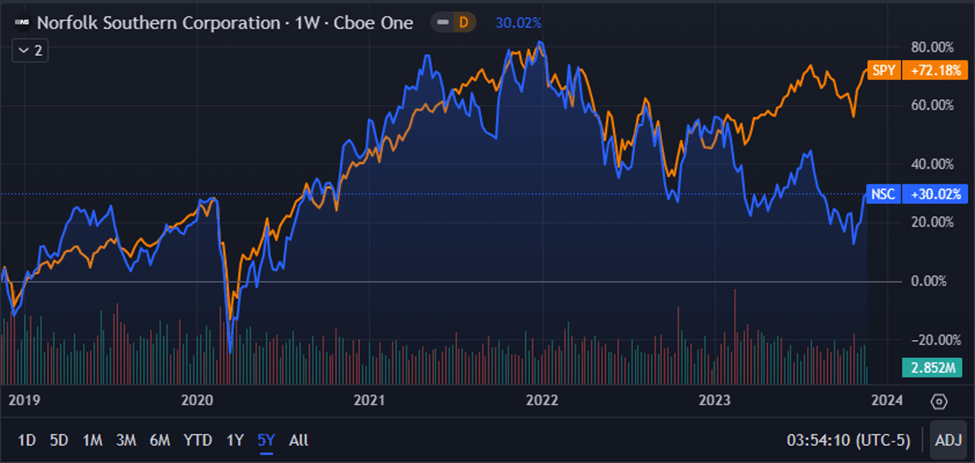

From an absolute perspective, Norfolk shares are trading at a significant discount relative to previous valuations with current share prices of around $213.00 representing close to three-year lows for the stock (not with counting the COVID-19 induced 2020 anomaly).

Still, even when compared to the 72% growth seen in the S&P 500 tracking SPY index over the past five years, Norfolk Southern has been outperformed by the U.S. market index as a whole by over 40%.

While the relative valuation provided by simple metrics and ratios along with the absolute comparison allow for a basic understanding of the value present in Norfolk shares to be obtained, a quantitative approach to valuing the stock is essential.

The Value Corner

By utilizing The Value Corner’s specially formulated Intrinsic Valuation Calculation, we can better understand what value exists in the company from a more objective perspective.

Using the firm’s current share price of $213.10, an estimated 2024 EPS of $12.90 , a realistic “r” value of 0.07 (7%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 5.61x, I derive a base-case IV of $248.90. This represents a modest 14% undervaluation in the firm.

When using a more pessimistic CAGR value for r of 0.05 (5%) to reflect a scenario where a globally spanning recession causes Norfolk’s revenue growth to flatline, shares are still valued at around $204.70 representing a fair valuation in shares.

Considering the valuation metrics, absolute valuation and intrinsic value calculation, I believe that Norfolk Southern is trading somewhere between a fair valuation and a modest undervaluation.

In the short term (3-12 months), I find it difficult to say exactly what may happen to the firm’s valuation. As 2023 winds to a close, the uncertainty around a recession occurring in 2024 along with how hard such a macroeconomic environment may bite the economy means forecasting a short-term direction for the stock is essentially impossible.

Tax harvesting could see Norfolk shares decline further as a less than stellar 2023 may lead some investors to cut the firm from their portfolio as the year winds to a close.

In the long-term (2-10 years), I believe Norfolk’s modernization strategy combined with a strategic goal to achieve operational excellence could see the firm outpace their closest rivals in terms of growth, income and margins. Their robust economic moat will continue to provide tangible competitive advantages to the firm which should ensure great returns in the long run.

Risks Facing Norfolk Southern

Norfolk Southern mainly faces risk from the cyclicality of the economy leading to declines in growth and profitability along with some tangible ESG risks arising from environmental degradation.

As mentioned earlier, railroads underpin the U.S. economy as a whole which ultimately means the industries are also tied to the economy when it comes to their ability to generate profits.

Given the risk of a recession in 2024 is quite elevated, Norfolk may see short-term revenues decline even further due to weaker demand across the country negatively impacting rail transport volumes.

However, I believe Norfolk Southern only faces a low level of threat from this scenario as their robust balance sheet and well managed debt profile should allow the firm to navigate even such a difficult macroeconomic environment without real concern.

{kind=link}

From an ESG perspective, Norfolk Southern faces mainly environmental pressures stemming from their reliance on coal transport for a significant portion of revenues along with some tangible risks arising from accidents.

Coal transport accounts for around 14% of Norfolk’s overall revenues. The overall reduction in the reliance on utility coal across the United States means Norfolk may face a long-term decline in volume demand for its transport.

While this threat equally impacts other Class I railroads too, it is worth mentioning and illustrates that Norfolk must continue to adapt their product offerings to accurately meet customer demand.

Norfolk also faces some real risks from the threat of one-off accidents leading to significant legal costs. The recent East Palestine derailment illustrates that while such events are remote, their impact on the firm’s income statement and reputation are real.

The East Palestine derailment also highlighted the costs associated with environmental cleanup with many of the 150 railcars transporting hazardous materials that had to be expertly disposed of.

While I do not believe any long-term damage has been done to the Norfolk brand or their fiscal health, the railroad must ensure measures are put in place to further reduce the likelihood of derailments.

Nonetheless, considering Norfolk’s ESG report, I believe the firm is acutely aware of the responsibility they hold towards ensuring that positive environmental, societal and governance impacts are achieved from the operation of their business.

The overall lack of any major environmental, societal or governance concerns suggest to me that Norfolk Southern may be a good choice for the more ESG conscious investor.

Of course, opinions may vary with regards to ESG material and I implore you to conduct your own ESG and sustainability research before investing in Norfolk Southern if these matters are of concern to you.

Summary

Norfolk Southern is an excellently managed and operated railroad that has simply hit a few bends in the tracks in recent times. Less than exhilarating FY23 performance combined with the East Palestine derailment appears to have soured investor sentiment in the firm which has led to a significant YTD selloff.

However, at its core Norfolk continues to be a well operated railroad with the firm’s new CEO Shaw embarking the firm on a cost-cutting mission to further streamline the railroad’s operation in the name of margin expansion.

When this profitable and fiscally solid firm is combined with a potential 14% undervaluation in shares, I believe now may be a great opportunity to buy shares of a lovely business at a pretty decent price.

While I cannot advocate building a position form a deep-value perspective necessarily, I really do believe Norfolk Southern is a great business available at what is respectable value.

Therefore, I assign a Strong Buy rating for Norfolk and have adjusted my portfolio composition to include a 16% stake in the railroad at present time.

I plan on holding Norfolk for as long as possible with the objective of never selling so long as the railroad is well managed and fundamentally profitable.

For further details see:

Norfolk Southern: All Aboard This Buy-And-Hold Freight Train