CA - North American Construction Group: Heading For Mixed Days (Rating Downgrade)

2023-07-07 06:01:04 ET

Summary

- North American Construction Group has pursued vertical integration, leading to an increase in shop hours and stable equipment operating costs, gaining market share from OEM providers.

- Lower energy prices and economic uncertainty could reduce demand for mining and construction services, affecting NOA's cash flows and balance sheet; the company's stock is currently considered reasonably valued.

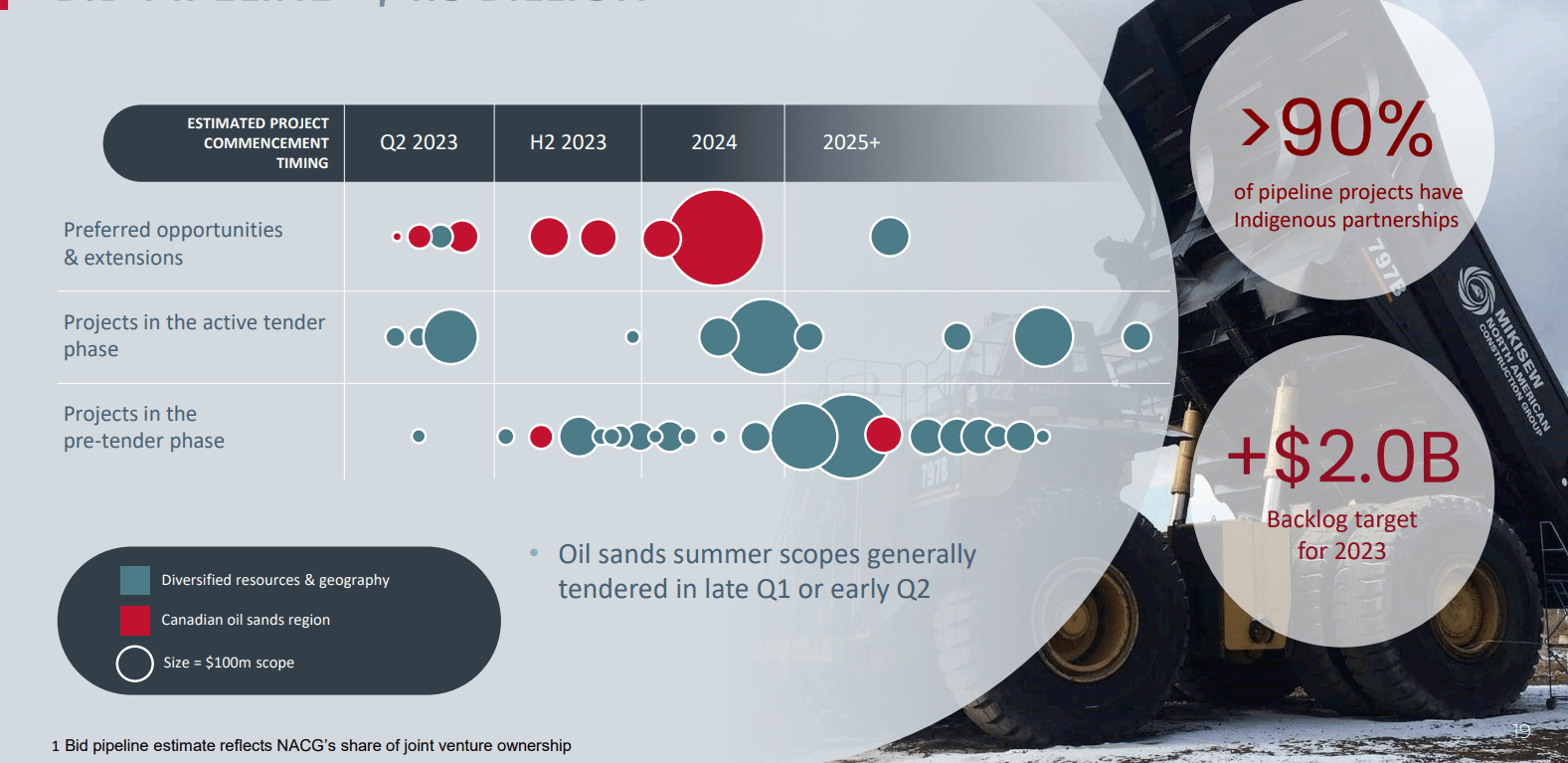

- NOA has a backlog of over $1.1 billion, expected to exceed $2 billion by the end of 2023, but global economic uncertainty could affect demand for its services and strain its balance sheet.

NOA's Strategies And Concerns

My last article on North American Construction Group (NOA) discussed its plans and strategies. Recently, NOA has pursued vertical integration, leading to a significant increase in shop hours. Through in-housing components and second-life rebuilds, its all-in equipment operating costs have remained stable, which allowed it to gain market share from the OEM providers. Nuna (its JV) recently acquired a five-year fueling and servicing contract. As the company looks to build on its backlog, asset utilization can continue to move north further.

But lower energy prices and economic uncertainty can lower the demand for mining, construction, and earthworks services in the near term, affecting its cash flows and balance sheet adversely. Although its liquidity is strong, a debt burden can be worrisome in an already leveraged balance sheet. The stock is reasonably valued versus its peers. I think investors should stay put and "hold" the stock with an expectation of a moderate return in the short-to-medium term.

Business Portfolio Mix

{kind=link}

In the oil sands and mining business, NOA's key advantage lies in the huge infrastructure costs of doing business in a capital-intensive industry. A new oil sands overburden fleet would cost an estimated $100 million-$150 million. Plus, it typically takes no less than two years to complete. So, only companies with deep pockets can venture into these projects. Currently, NOA is operating in Canada, the US, and Australia. It has ~30 project sites with clients producing a variety of commodities. Its services include infrastructure construction, mine management, and external maintenance services.

The company's other distinct advantage lies in its low-cost operating model, which lets it work throughout any commodity cycle. It estimates that all-in equipment costs are more than half of the typical costs. It has been in-housing components, which saves the company 30% to 40% of the costs of going to the OEM dealers. It also saves through whole machine second-life rebuilds, which include 17 of its largest haul trucks. As a result, its all-in equipment operating costs have remained stable over the past several years.

Cost Advantages

The company has pursued vertical integration which led to a significant increase of shop hours. It also helped with internal maintenance activities. As the company kept its shop cost per hour stable, it garnered market share from other OEM providers when it increased charge-out rates in contract support.

Projects And Outlook

{kind=link}

In Nuna, the company expects to receive a contract award in Q2. Its scope of award includes a $75 million five-year scope for fueling and servicing. It will fall under the newly acquired ML Northern equipment servicing business (Mikisew partnership). NGS has over $1.1 billion in backlog, expected to exceed $2 billion by the end of 2023.

I expect demand to remain high throughout 2023 and continue into 2024. It will increase its maintenance labor workforce, leading to higher fleet utilization. In FY2023, NOA expects to generate an adjusted EBITDA of $265 million (at the guidance mid-point), representing a moderate increase over FY2022. Its adjusted EPS can increase more sharply in FY2023. Free cash flow, during this period, can shoot up remarkably.

Analyzing Q1 Results

{kind=link}

From Q1 2022 to Q1 2023, the company's total combined revenues increased by 36% (including revenues from affiliates and joint ventures, less JV sub-contract revenues). Contributions from adjusted equipment, unit rates, and better utilization led to the topline growth. In Q1, equipment operating hours increased by 20%. Revenue addition from ML Northern also added to the revenue growth. Asset utilization was 79%, significantly higher than a year ago (65%).

The joint venture of Nuna Group of Companies added $18 million of additional revenues in Q1 2023 compared to a year ago. Higher activity in the gold mine in Northern Ontario rebuilt haul trucks, purchased excavators, and the Fargo-Moorhead flood diversion project primarily accounted for the revenue rise.

The Gross Margin Strength

In Q1 2023, the company's gross margin expanded by 400 basis points compared to a year ago. The company's operations in Fort McMurray, Northern Canada, and Northern Ontario experienced relatively steady weather, which benefited its margin. Updated equipment and higher unit rates benefited its Fort McMurray operation. Lower internal costs and a second-life rebuild program led to strong margins.

Capex And FCF

In Q1 2023, led by higher revenues, NOA's cash flow from operations increased by 32% compared to the previous year. However, its account receivable increased, which hurt the cash flow. Capex, in comparison, increased even more, resulting in free cash flow (or FCF) slipping further into the negative territory in Q1 2023 over the previous year.

NOA's liquidity was $172 million as of March 31, 2023. As free cash flow worsened, the company's net debt increased by $28 million. Its leverage (debt-to-equity) of 1.1x is higher than many of its peers (CESDF and NR). With limited drivers to push revenues and profit higher, it may not be easy for the company to generate $100 to $115 million in free cash flow as set in its guidance.

Relative Valuation

{kind=link}

NOA's forward EV/EBITDA multiple is expected to contract versus the current EV/EBITDA multiple. Also, the contraction is less sharp than its peers (CESDF, TTI, and NR). This typically means the company's EBITDA can rise less sharply than its peers in the next year, typically resulting in a lower EV/EBITDA multiple. The company's EV/EBITDA multiple (5.3x) is lower than its peers' average of 8x. So, I think the stock is reasonably valued versus its peers.

Analyst Rating

{kind=link}

From Seeking Alpha's data , six sell-side analysts rated NOA a "Buy" or "Strong Buy" in the past 90 days. Two rated it a "Hold." None of the sell-side analysts rated a "Sell." The consensus target price is $18.7, suggesting a 3.6% upside at the current price.

Why Do I Downgrade My Rating?

By the end of 2022, NOA had several value drivers, including higher asset utilization. Its telematics packages were installed on several primary heavy equipment assets. The Canadian oil sand operators were about to increase the 2023 capex budget. So, NOA's operating margin improved significantly in Q4, which allowed a recent dividend hike. I wrote :

Although the crude oil price has been volatile recently, the Canadian oil sands operators appear to be on a sounder footing about the industry as they increase the 2023 capex budget. This has allowed the company to roll out more telematics products and start rebuilding equipment by commissioning another 240-ton haul truck. Better performance at the Fort McMurray, Northern Canada, and Northern Ontario operations led to a significant operating margin improvement in Q4.

In Q1 2023, some of the drivers lost juice. Uncertainty over energy prices spelled worries over the oil sands production. Following the lack of robust growth opportunities, the company would look inward to save to improve its operating margin. Although the management expects its backlog to swell by the end of the year, I think the headwinds would curb the growth rate. So, I would downgrade the stock to a "hold" from the previous "buy".

What's The Take On NOA?

{kind=link}

NOA continues to enjoy the relative safety of working in an industry having substantial cost barriers and where it has already built a cost advantage over its peers. Through vertical integration, whole machine second life rebuilds, and in-housing, it has wrestled market share and lowered costs. It has over $1.1 billion in backlog, which can nearly double by the end of 2023. Asset utilization increased significantly in Q1 2023 compared to a year ago. So, the stock price outperformed the VanEck Vectors Oil Services ETF (OIH) in the past year.

But I think the demand for construction and mining can fall due to global economic uncertainty. This can affect the company's cash flows, even if the operating income improves. Its balance sheet is more leveraged than some of its peers. Lower cash flows can strain its balance sheet, as witnessed in Q1. Given its relative valuation, I would suggest investors "hold" the stock in the short-to-medium term.

For further details see:

North American Construction Group: Heading For Mixed Days (Rating Downgrade)