CA - North European Oil Royalty Trust: No Stay Away

2023-10-02 07:11:26 ET

Summary

- North European Oil Royalty Trust has consistently underperformed and has a negative 10-year return on investment.

- NRT's small size and limited operating area limit its appeal and potential for growth.

- The current dividend yield of 6.88% is not attractive compared to other investment options with higher yields and lower risk.

Dear readers/subscribers,

There's a very slim upside for niche companies like the North European Oil Royalty Trust ( NRT ). The company has a working and attractive business model, at least in theory. I've already covered it in numerous previous articles, the previous one being found here.

My thesis for this company has always been one best described as "hesitating". The company offers an undeniably attractive yield, but despite this yield, the North European Oil Royalty Trust has failed to perform with positive returns for at least as long as I have covered it. The current performance stands as follows, which might not be much of a negative compared to some investments and their poor performance, but it's an underperformance nonetheless, even inclusive of the company's generous dividends.

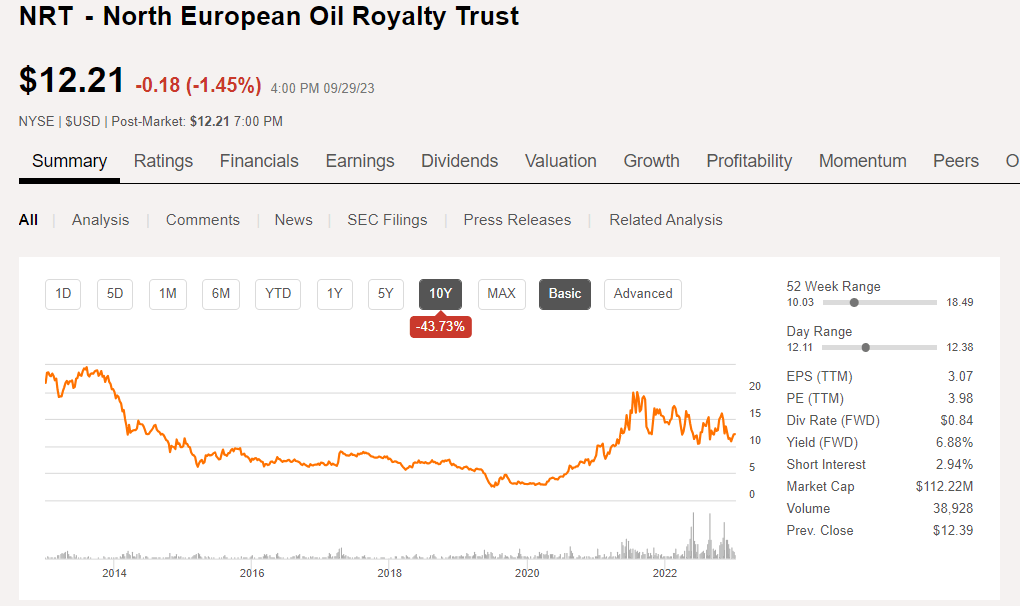

Seeking Alpha NRT RoR (Seeking Alpha NRT RoR)

As you can see, even from my very first article back in 2022, the company has still underperformed, despite some extreme dips and ups during that time. I'm going to take advantage of this time and provide you with an update for both bearish and bullish theses on the business - because there's room for both here.

North European Oil Royalty Trust - The up and the downside, but the downside reigns here.

The bullish thesis for a player like this is relatively simple. It's a straightforward look at the overall distribution growth rate, the dividend/distribution coverage ratio, and relatively strong fundamental KPIs such as the free cash flow yield, the simplicity of its business model, its position in the European energy value chain now that Russia has, to large extent compared to where it previously was, gone bye-bye, and the hope that the company can essentially out-navigate the typical ups and downs of the industry and the energy sector.

The problem with this bullish stance - and I know some of you, dear readers, do follow and invest in this company, is that it holds very little water when viewed in the context of the much larger or longer timeframe.

At least, viewing it with such simplicity does not work. NRT is, as I see it, not even close to being able to outnavigate fundamental ups and downturns in the energy sector. I would argue it even follows these trends more slavishly than other businesses do.

Take a look at what has happened to investors in the company for the past 10 years.

{kind=link}

What you see, is as the graph says, a 10-year post-GFC RoR of negative 43%, even with the recent bump. You'll also notice that that bump coincides very closely with the onset of the Ukraine crisis and the oil price increases/energy price increases that follow.

If you look at the company on a 2, 5, or even 7-year basis, you can get the impression that yes, NRT does indeed outperform its peer group. The problem is that this isn't a large enough comparison, as I view it.

NRT is a very small company. We're talking less than $120M in market cap. The company is, in fact, a NYSE-listed successor of the North European Oil Corporation and Oil Company, and those shares have been around on the market for around 40 years at this point.

But it's extremely small. Like, administered-by-five-trustees sort of small. The purpose of the Trust is to collect, hold, and verify royalties paid into the Trust by the operating companies, German subsidiaries of the Exxon Mobil Corporation ( XOM ), and the Royal Dutch/Shell Group of Companies ( SHEL ). And that is indeed what the company does, then paying out those royalties on a quarterly basis to shareholders.

On the positive side, there is no debt - and the trust is not permitted, in fact, to take on any sort of debt if you look into the filings of the trust agreement. So that's a nice detail.

But in the end, the proceeds and the dividends you're getting come from the sale of fossil resources, in the form of nagas, oil, sulfur, and condensates from sources of those commodities within the trust operating geography - in this case, those are found in Northern Germany in the form of concessions and leases - and only northern Germany. The trust has never, nor does it plan to according to filings, own assets or land outside of these areas.

That limits its appeal.

Why?

Because, as you may notice, until the onset of these macro troubles, NRT traded very differently from where it trades today. It traded at around $2-$4/share.

Why is that?

Because, if global trade "works", and countries like Russia with cheap producing assets are part of the network, then sourcing commodities from Germany is neither efficient nor cheap in comparison. In order for the company to make a good profit, the oil price/commodity pricing levels need to be high. That's why the company has a current yield of close to 7%, and that's why this stock has been trading so expensively for the past few years.

This brings me to another problem, and it's a big one, as I see it. The dividend/distribution.

The simple fact is that a 6.88% yield in a world where you can get 7-8% yield from BBB+ rated investments or equivalents just isn't very attractive. Why on earth would you invest capital into a not-rated $100M microcap company when you could have more yield and better upside with actual investment-grade credit rating and without the comparatively risky commodity exposure?

There exists a disconnect here, as I see it, between where this company "should" trade and where it currently does trade. The overall valuation trend since the company peaked in mid-2022 has gone down.

Despite fairly positive current trends, I do not see this changing.

But wait, there are more risks and negatives.

The company's limited operating area comes with proven reserve risks. Unlike much larger upstream players, the company has very limited availability of new sources of product. If you really want to invest in the company, I strongly encourage you to take a look at the previous articles I've written that go into more detail on the sources available to NRT, based on the Oldenburg concession. To be clear, NRT isn't as much oil as it is gas (especially as of late with gas price trends), but it's my view and the market's view that the worst in the Natgas sector is actually past.

When I first wrote about NRT, their dividend yield was 33%. It's now less than 7%. The normalization in dividend yield and payout that I forecasted in my very first article has now materialized almost in full, and I do not expect it to stop there. Even if there could be a momentary stop in the decline in commodity pricing, I expect expenses for the company to combine with inflation and put further pressure on distributable earnings.

That does not even go into the political risks here. Germany and energy production is not a risk-free venture. The German government has at times gone into and curtailed production and expansion of everything from lignite, coal, and other sources for both environmental and other reasons. This company, with its asset concentration and size, has very little recourse once its sources start to decline in terms of lifespan.

For all of these reasons mentioned, I don't consider the latest report and update to its distribution to be of material impact for a positive thesis. I in fact view this as a player piano that's currently playing the tune exactly as I expected it, in terms of direction, to turn out.

I would encourage any would-be-investors in NRT to really look at whether this is something they want to own long-term because I firmly do believe that from a fundamental point of view, the negative risks vastly outweigh the positive potential gain here.

Let's look at valuation.

Northern European Oil Royalty Trust

In my previous article, I gave the company a conservative share price of $10/share. The company has not, since then, not once dropped below or very close to that price.

As of this article, I'm lowering it due to the deterioration of the distribution both current and what I see likely going forward. I'm cutting it to $8/share, at which point the company would currently yield around 10.5%. At that yield, I can maybe see some appeal to someone investing in this for income.

But at the same time, I would personally rather buy a 7-8% yielding BBB-graded pref stock than I would this company even at that level. In order for it to be something I would personally consider for my portfolio long-term, I would probably need a share price of $5-$6/share, and that's relatively unrealistic in the current macro.

The difficulty is that if you do invest now, and the directional trend of the company keeps up, which I believe it will, there seems to be a non-trivial chance that you're going to have a hard time coming out on top with this investment.

The continued (mostly) exception of Russian-sourced crude is an upside for the company, and I don't see the conflict there abating even in 2024. But this is not enough, as I see it, to justify a higher share price here.

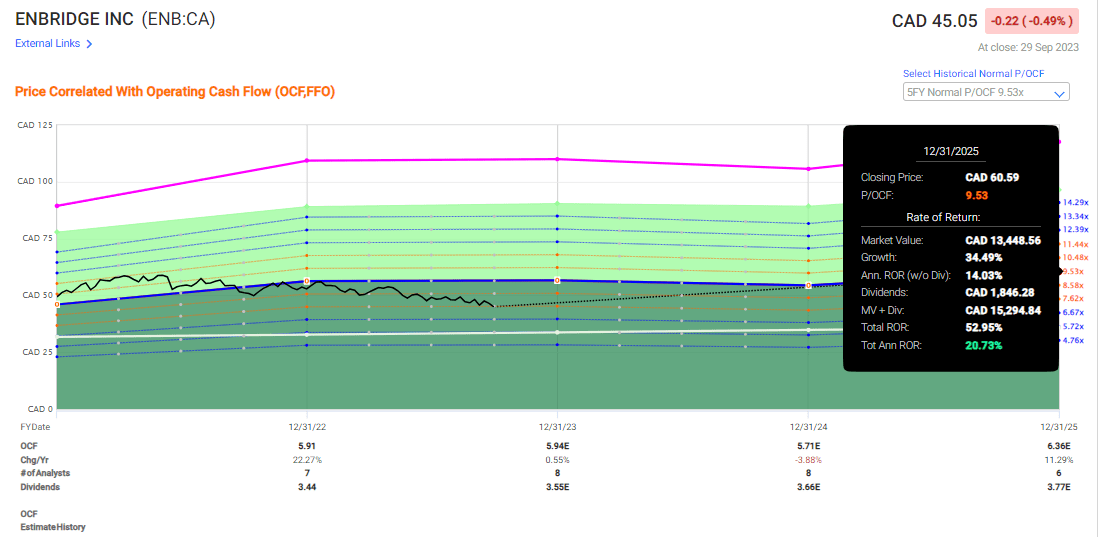

Not when you can literally "BUY" Enbridge ( ENB ) today, at a 7.89% yield with a significant conservative upside.

{kind=link}

I show this to you because this is actually an energy company that I recently invested in. NRT is not. I continue to believe that the company, at this price, in no way justifies what upside and yield there is. The fact that we're now down to less yield than a BBB+ rated player like Enbridge with a market cap, should give you some indication of just how far this has gone.

It's therefore very easy for me to say that I have no interest, at this time, in investing in this company/this trust.

I'll wait for a massive drop and that significant upside I at some point hope exists.

Thesis

My thesis for NRT is as follows:

- The company is an interesting play on a specific EU gas/Oil/sulfur asset in Germany. It's not without its general appeal, but I would say that there's too much risk to go fishing here, despite some improvement in price.

- As of October, I'm saying that the company is still too overvalued to make it an attractive "BUY", but I am giving it a continued, clear target.

- I would update my PT to account for a lower potential downside, and move to $8/share, making this a very risky play given the correlation to energy prices.

- I consider NRT a "HOLD" here and would wait.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fulfills only one of my criteria at this time in October of 2023 and I call it a "HOLD".

For further details see:

North European Oil Royalty Trust: No, Stay Away