USO - Northern Oil and Gas: Free Cash Flow Champion A Compelling Valuation

2023-04-10 11:19:33 ET

Summary

- Oil prices recently dropped and popped - a move above $80 means ample profits for many E&P names.

- Northern Oil and Gas sports very high free cash flow, and WTI's bounce is fuel to its bullish valuation.

- The chart, though, is not as appealing ahead of its May earnings date - I outline key price levels to watch.

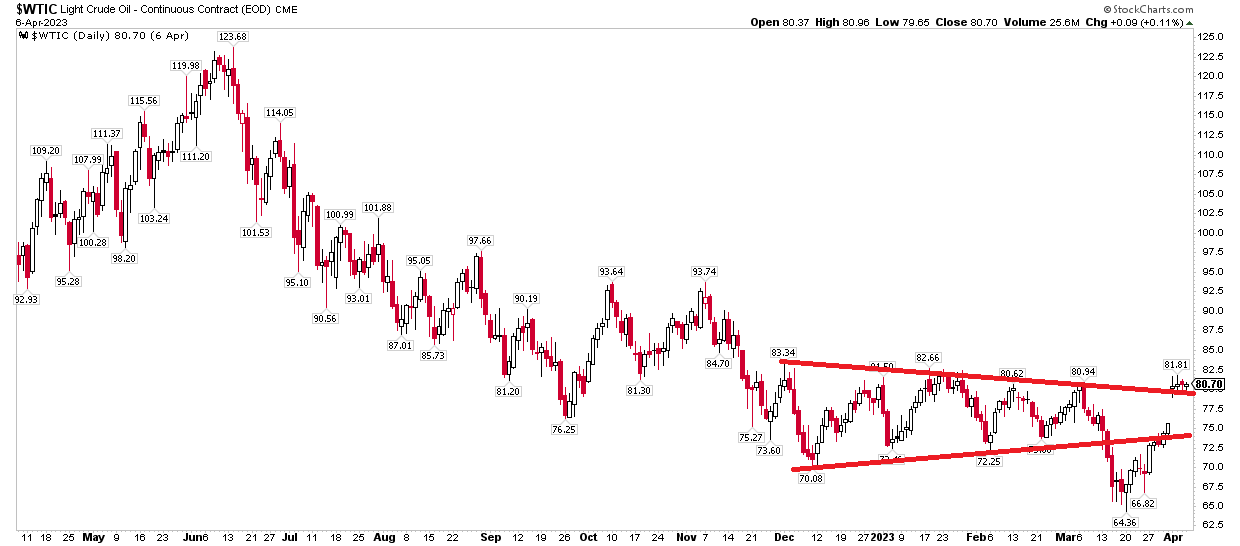

WTI crude oil cratered below the $70-mark last month. I view that as a bearish move, but the bulls proved me wrong. Or perhaps OPEC+ did. The consortium of energy policymaking countries announced a surprising production cut, and both WTI and Brent rallied. With domestic oil now hovering above $80, that is plenty high enough for many US-based exploration & production companies to operate profitably.

I see shares of Northern Oil and Gas a buy, but the technical chart still has work to do.

WTI: Bullish False Breakdown

{kind=link}

According to Bank of America Global Research, Northern Oil and Gas ( NOG ) is the largest publicly traded non-operated E&P. Its net production reflects a broad array of working interests in a series of oil and gas properties where it partners with operators and takes a cut of well level revenues for a proportional amount of capital operating costs. It has assets in North Dakota, Pennsylvania, and the Permian Basin.

The Minnesota-based $2.8 billion market cap Oil, Gas & Consumable Fuels industry company within the Energy sector trades at a low 4.0 trailing 12-month GAAP price-to-earnings ratio and pays a high 4.2% dividend yield, according to The Wall Street Journal. The stock also has a high 19% short interest, so swift moves higher in the shares could be accelerated by short-covering rallies.

NOG missed on earnings estimates back in February, though it beat on the top line. Following several acquisitions over recent years, free cash flow has turned impressive. A key risk, though, is if oil prices and Henry Hub natural gas prices decline. We have already seen natural gas sink to near $2, but WTI has rebounded back above $80. Overall, these should be sustainable prices for Northern to generate significant free cash flow.

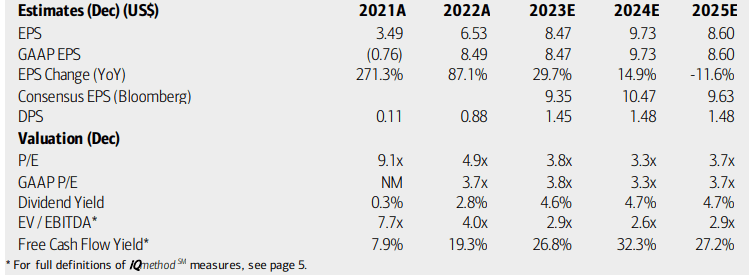

On valuation , analysts at BofA see earnings rising sharply in 2023 before moderating next year. Per-share profits are then seen as turning negative on a YoY basis by 2025. The Bloomberg consensus forecast is more sanguine compared to what BofA projects. Dividend growth may slow with NOG while its operating and GAAP P/Es remain quite low should the stock price hold near current levels.

With an exceptionally low EV/EBITDA ratio and trading at less than just 4x free cash flow, the valuation is compelling even with the EPS growth slowdown. If we assign NOG’s 5-year average forward operating P/E of five on $9 of normalized earnings, then the stock should trade near $45. Thus, it is a buy on valuation in my view.

NOG: Earnings, Valuation, Dividend Yield Forecasts

{kind=link}

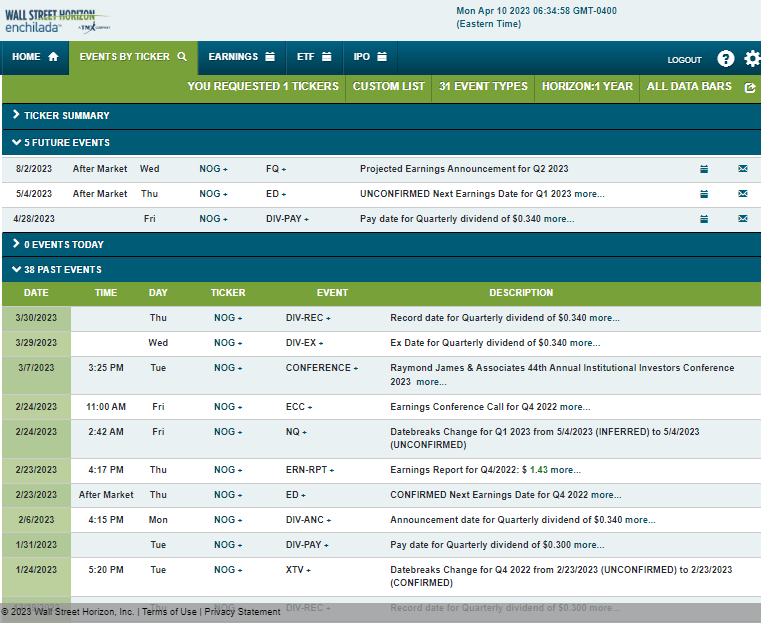

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q1 2023 earnings date of Thursday, May 4, after the market close. The calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Risk Calendar

{kind=link}

The Options Angle

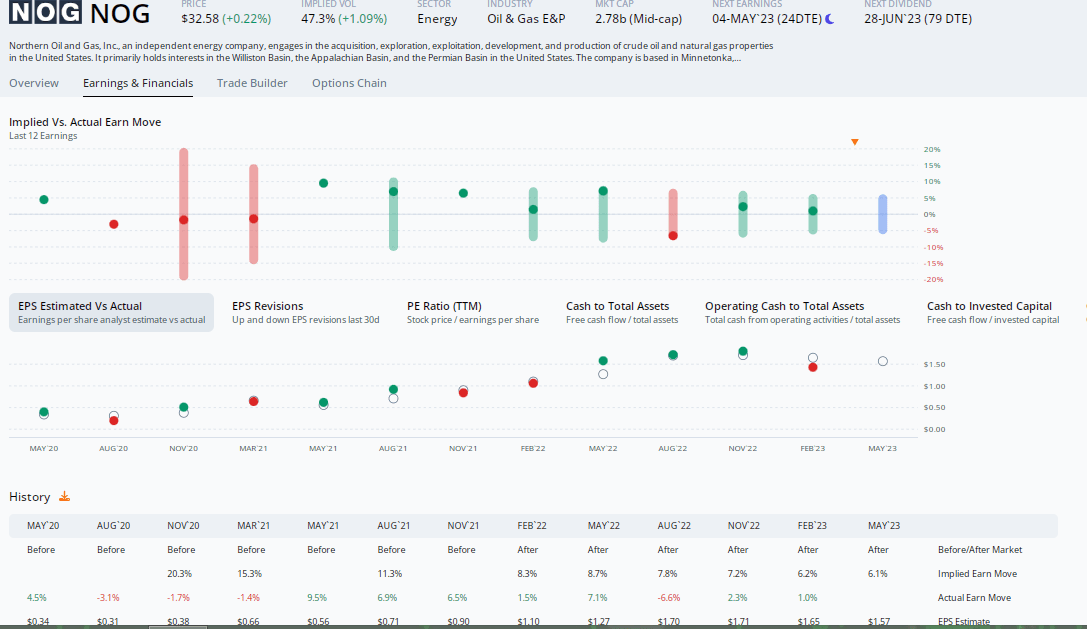

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS forecast of $1.57 which would be a 1% decline from $1.58 of per-share profits earned in the same quarter a year ago. The company has a mixed bottom line beat rate history and shares have not moved big post-earnings in recent quarters.

This time around, a 6.1% earnings-related stock price change is expected following the Q1 report in May, according to the at-the-money straddle expiring soonest after the May 4 reporting date. That is not far from what we have seen after recent releases, though the previous pair of events saw muted volatility after the numbers hit the tape. I see that premium as being near fair value.

NOG: Flat YoY EPS Growth Expected

{kind=link}

The Technical Take

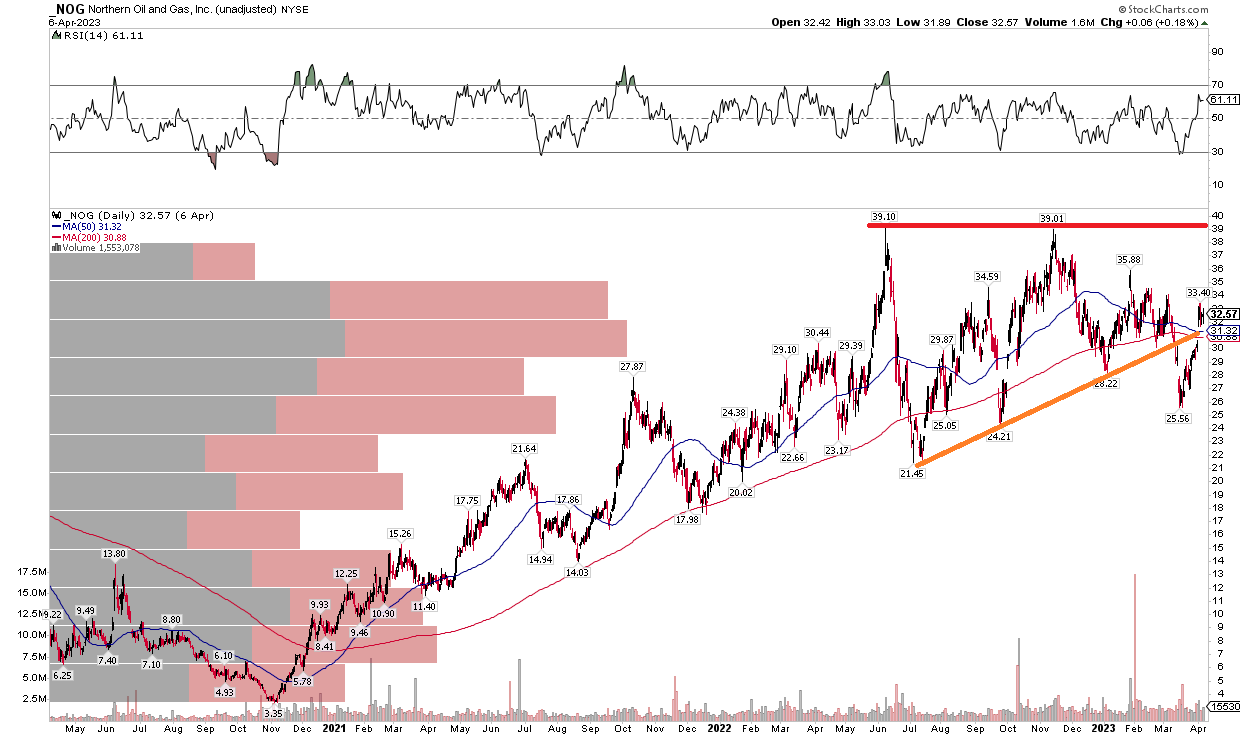

NOG put in a bearish double top pattern at $39 in 2022. Notice in the chart below that shares were in a steady uptrend after reaching a low in Q4 2020. A consolidation ensued during the back half of last year, then the stock broke below an uptrend support line in March. The bulls stepped up, and brought the energy name back above that key line just recently. So, there is a mixed bag here. I like the potential bullish false breakdown, but the double-top resistance remains in play.

Long here with a stop under the March low could work, or playing a momentum breakout above $39, which would trigger a measured move price objective to near $58, could be an option. Overall, the chart is neutral at the moment. And that argument is buttressed by the fact that the long-term 200-day moving average is now negatively sloped after being positive for several quarters.

NOG: Bearish Breakdown Reverses To The Upside

{kind=link}

The Bottom Line

I am a buy on valuation with NOG while recognizing that the technical chart is merely in consolidation mode.

For further details see:

Northern Oil and Gas: Free Cash Flow Champion, A Compelling Valuation